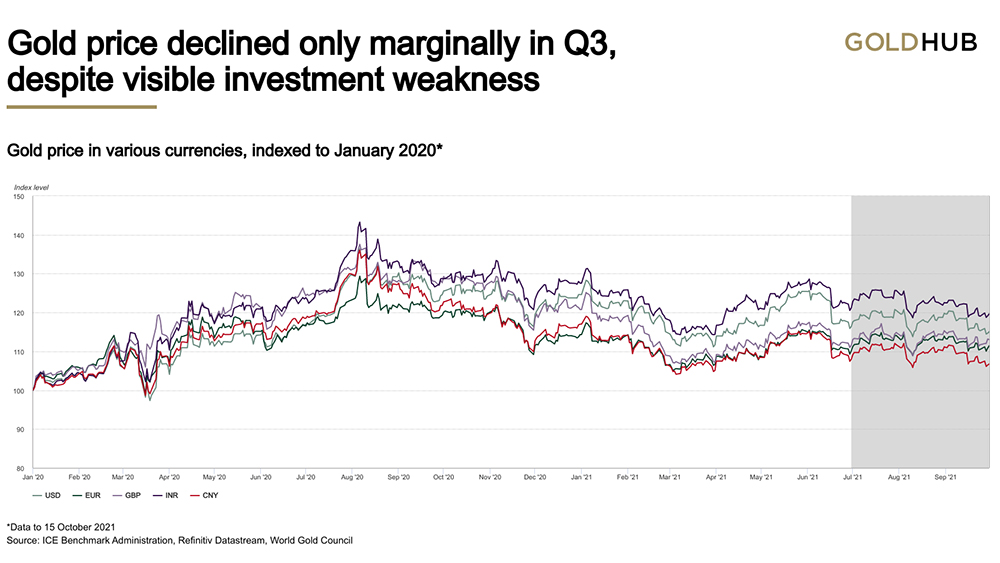

Gold holding up well despite ‘apparent’ underlying investor despondency was one silver lining. Another was the lacklustre performance of both equities and bonds. A general malaise appeared to have taken hold in financial markets during Q3, particularly during September. Seeing bonds and equities fall together ( -4.7% and -0.9% respectively)1 runs counter to the experience investors have grown used to for over two decades. Should that continue with gold picking up steam, it could boost gold’s appeal as a risk hedge going forward.

Outlook

Strong consumer, central bank and OTC demand faces off weakness in ETFs and solid growth in mine output

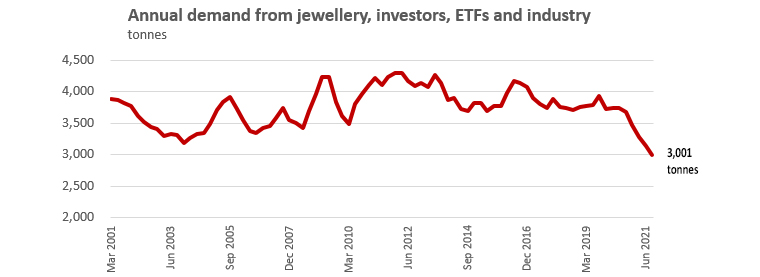

We anticipate jewellery demand will exceed 2020 levels and have raised our expectations slightly given current weak price performance. Jewellery will likely continue to benefit from the economic recovery. One risk to our view for the full year (FY) 2021 stems from China, where a fallout from property sector woes and power outages might negatively impact demand in Q4. Having said that, we feel that India’s stronger than anticipated y-t-d demand can offset potential weakness in China. In all, we tighten our FY2021 jewellery demand range estimate to 1,700–1,800t.

Unsurprisingly given its y-t-d performance, we expect investment demand in total to be weaker in 2021 compared to a stellar 2020. Bar and coin demand has impressed but has been offset by materially weaker-than-anticipated net gold ETF demand. Bar and coin demand should continue to be supported by the macro environment of high inflation prints and economic concerns. One surprising area of strength is the US, where the y-t-d total is the highest in our dataset. This was all the more notable given the weakness in both gold ETFs and COMEX futures.

ETF demand is forecast to be weaker than last year, but the extent of the weakness so far was vastly underestimated given a generally supportive macro picture. On balance, it appears the prospect of a higher interest rate environment is more of a concern than ‘transitory’ inflation.

A similar pattern has emerged in the futures markets. A continued drop in COMEX net positioning to a six-month low suggested that OTC demand may have gone the way of ETFs, given their linkages. But our OTC estimate, which is part of the balance of demand and supply, remains not only positive so far in 2021 but is sizeable.

We believe that the following factors are at play here:

- The issues faced by COMEX in 2020 are still reverberating in 2021. Coupled with a steeper contango in 2020, it’s unsurprising that some flows may have escaped futures and found their way into other forms of gold

- There is anecdotal evidence of inventory rebuilds in 2021 following a year of de-stocking in 2020 from some major consumer markets. This non-investment demand would contribute to our larger OTC estimate

- ETFs have experienced outflows this year but the vast majority of those are from the US. A regional breakdown reveals that both European and Asian ETF demand has been healthy. This dichotomy is supported by strength in US bar and coin and anecdotally via other sources of retail demand.

Central bank demand has surprised to the upside so far in 2021. Y-t-d buying as of Q3 sits at 393t and, based on historical performance and insights from our survey, we wouldn’t be surprised to see a figure above 450 by year-end.

With diminishing COVID-19 disruptions and a supportive economic environment, mine supply should have fewer impediments to healthy growth in 2021. However, producer margins have continued their downward trend in Q3 since peaking at the end of 2020. A prolonged continuation of this trend could be headwind to continued production growth at these levels.

Recycling is expected to be marginally lower this year, offsetting growth in mine output. Recycling is expected to contract slightly in 2021 (by between 50–150t). With near-market supplies appearing depleted following two years of relatively elevated activity, healthy economic growth to-date, and a muted gold price in 2021, there has been little incentive or capacity to recycle at recent years’ levels. But we remain open to the risk that Q4 could still see economic stress-selling in Asian markets as fallout from China’s property market travails and power shortages lingers.

![]() Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

To subscribe, log in or Register, and sign up in your Account page. It's free.

Comparative pricing

You can find our independent comparative pricing for bullion, coins, and used 'scrap' in both US dollars and New Zealand dollars which are updated on a daily basis here »

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.