No doubt the Reserve Bank's January figures for new mortgages make pretty dire reading.

But strangely maybe the figures suggest that the trough in housing activity may have now been passed. Maybe. Don't hold me to that one though. And I would stress I am talking about ACTIVITY - not house prices, which the RBNZ is still forecasting have a way to fall.

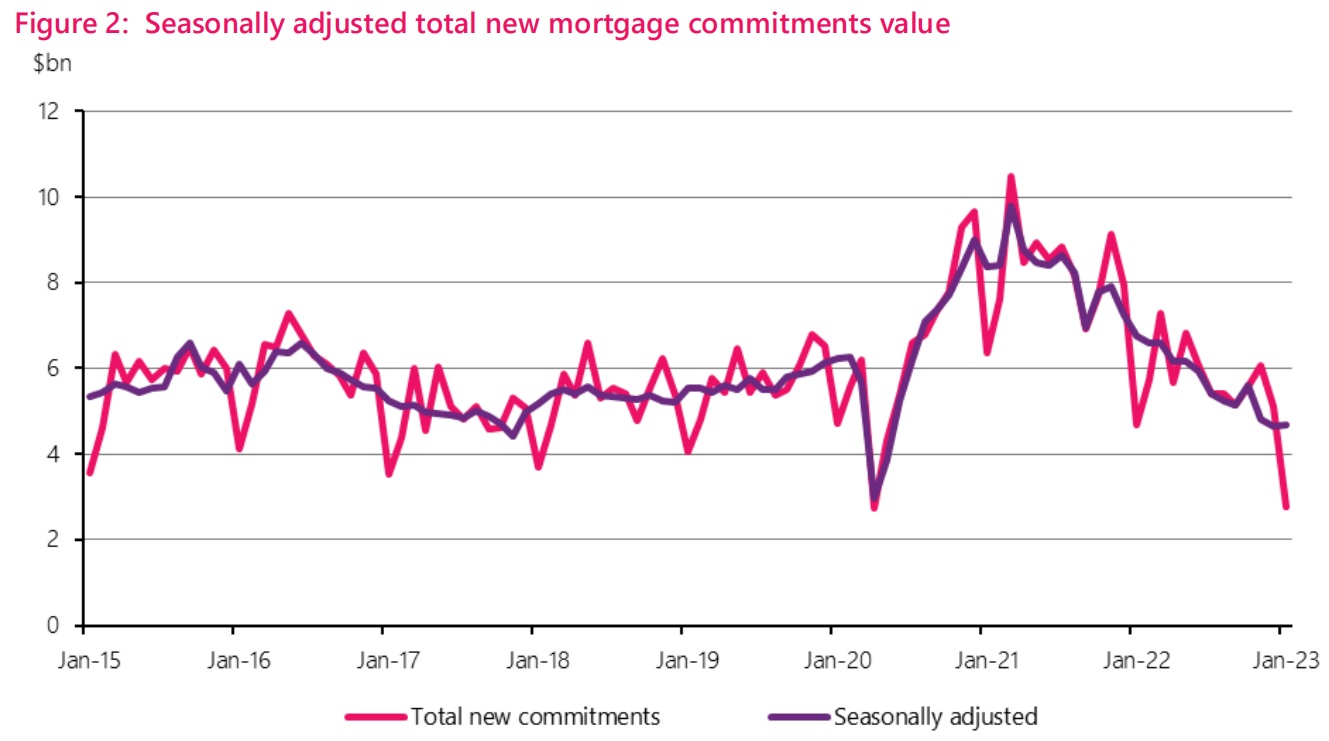

Anyway, taken in isolation the latest monthly figures show activity - in a numerical sense - hitting a new low.

However, the RBNZ's summary of the month's figures make the point that after seasonal adjustment the number of total mortgage commitments in January actually showed a 0.5% improvement on those for December 2022.

And yes, the December 2022 figures were pretty down there.

The January figures also, in relative terms, showed something of a bounce back for the first home buyers in terms of that grouping's share of the overall mortgage monies advanced during the month of January.

However, again, one should be cautious about any conclusions based on one month's figures and particularly when we are looking at such a low base. But for the record, the FHB's share of the mortgage money hit a new record high of 23.1%.

The investors, however, having had a slight uptick in December, saw their share drop to a new record low of 15.4%.

There were a lot of record lows recorded for January though - bearing in mind we are talking about relatively recent data that's been published by the RBNZ only since August 2014.

Here goes with some of the detail...

The $2.775 billion total mortgage money advanced in January was the second lowest since the data series began - beaten only by the $2.749 billion figure in April 2020 when we were all locked down.

Based on other criteria though the January 2023 figures are hands down numerically the lowest.

The 8680 number of mortgages issued in the month 'beat' the 9641 mortgages in April 2020 very comfortably (and yes, that's the next lowest figure).

Comparing January months, we can see that the latest number of mortgages for January 2023 compared with 12,033 in January 2022 and 19,186 in January 2021. Figures of around 18,000 to 19,000 mortgages have been about the 'norm' for a January - although in January 2016 there was 24,700 of them!

So, yeah, business is a bit quiet at the moment!

In terms of dollar amounts the $2.775 billion figure for January 2023 is down around 40% on the $4.68 billion in January 2022 and it's down a whopping $3.585 billion - that's 56.4% - on the $6.36 billion borrowed in January 2021 when the housing market was still operating on performance-enhancing drugs.

The housing market, as you may have noticed, of course is not faring as well now.

In its February Monetary Policy Statement released last week, the RBNZ revised again its forecast of how far house prices will fall.

In November it saw the total decline in prices being 20%, now it sees 23%.

"House prices have fallen by 15.2% since the peak in November 2021. House prices are projected to keep falling in 2023, consistent with very low sales volumes in recent months. House prices are assumed to have fallen by around 23% from their peak in 2021 to their trough in mid-2024, before recovering as interest rates decline toward their neutral setting," the RBNZ said.

There is, however, a bit of a silver lining in this for those who are out getting mortgages at the moment - albeit that they are now facing much higher interest rates.

The average size of the mortgages, which got quite jaw dropping for a while there, is falling quite fast.

In January 2023 the average-sized mortgage was (with some rounding) $320,000. That's down 17.8% on the figure in January 2022, which was $389,000. But that $389,000 average figure wasn't actually the peak high.

In fact the averages kept going up for a while last year even as house prices were starting to descend. It peaked at about $408,000 in May 2022, so the latest month's average figure is down 21.6% on the peak. You are paying more for the mortgage in terms of interest costs, but you at least don't have to borrow so much.

However, putting that in some perspective, if we go back to January 2021 the average mortgage size was $331,000 and in January 2020 it was 'just' $245,000. In very rough terms then we've come down to around late 2020-early-2021 levels in respect to mortgage sizes.

This shrinkage in mortgage size hasn't quite applied as much to the FHBs, however. The $549,000 average mortgage for the FHBs in January 2023 compares with $578,000 in January 2022, with $518,000 in January 2021 and $448,000 in January 2020.

To get back to the original question of have we now passed the trough in activity? Time will tell and one month's figures don't paint the picture.

But whether the 'trough' has been passed or not, the current figures suggest we aren't about to go scaling any new peaks particularly soon.

47 Comments

Have we hit the trough in housing activity - I don’t think so. At least a year out. 2021 mortgage fixers still on low rates awaiting higher refit and associated discretionary spending cut

Correct. The falls to date have been around what potential buyers can afford to borrow. So normal levels of new listings, but very few buyers, so increasing total properties on the market.

What we are yet to see is the full impact of rising rates on those who are highly leveraged, nor the impacts of a slowing economy. If we get increasing pressure to sell (either being forced to accept the best available offer on properties already listed, or increasing number of listings).

The idea things have hit the bottom already, when rates are projected to continue to rise and then hold at elevated levels for a year or more, into rising unemployment and slowing growth, is a pretty wild claim.

Great post as usual.

I agree Miguel as the trend since jan 2021 is down on new and seasonally adjusted basis and I don't saw anything that is likely to change the trend.

Like I keep saying: "Who can afford to build/buy?". You are looking at mega amounts of $$ just to service the loan and with equity dropping for the next year or so, could easily find yourself underwater. So the only people able to afford now are high income earners with a decent deposit already saved, who if smart, will just be keeping their deposit in the bank earning higher interest (we are getting 1k a month for nothing), awaiting the market to turn.

23% drop is beyond crash level, but they keep revising that higher, so its likely to play out somewhere in the 30-50% range. Don't think we have reached capitulation level yet, still a lot of talk about how housing is a sure bet.

I have lost count of how many times ANZ have revised their house price fall projections, must be about time for another revision!

They don't want to scare those indebted to them. Instead it's death by a 1000 paper cuts

The January figures also, in relative terms, showed something of a bounce back for the first home buyers in terms of that grouping's share of the overall mortgage monies advanced during the month of January. [...] But for the record, the FHB's share of the mortgage money hit a new record high of 23.1%.

Simply ridiculous to talk about one subgroups % of total lending as if that was an indicator of anything. If FHB borrowed the exact same as they did last month, but investors borrowed 100x what they did last month, the FHB percentage is going to look terrible - despite no change to the actual amount lent to FHB.

If you look at the actual dollar amounts advanced, FHB lending is incredibly low and dropping. It was $640m in Jan-23, if we exclude Apr-20 (lockdown) then you have to go back 5 years to Jan-18 to find a lower total. It's just that investors have backed off much harder than FHB, and so their share of lending is higher.

Do we think Adrian Orr will be happy with this; New Zealanders pulling their heads in and concentrating on the immediate cost of living, rather than asset speculation? Absolutely.

And that's the key to the future. New Zealand has far better things to do with its national debt than encouraging asset price appreciation not backed by national productivity increases.

We've created and voted to continue this mess over several decades, when all and sundry told us it was unsustainable (when they were looking for our votes, of course) and unwinding it has been left not to the political classes but to the RBNZ.

So if we want to know "Is this the bottom in market activity?" - don't look to National or Labour for the answer. Look to the RBNZ.

Unless there are further falls investors will not return, at the moment the numbers just do not add up.

RBNZ will introduce DTI limits at the bottom, we are not even close ....

Funny while we where near the top if we had a bad month the spruikers would tell us to look at the 3 month rolling averages, now like drowning men clutching at straws, monthly data is all the evidence of a green shoot they need.....

Lastly if the market takes off confidence will rocket, with it inflation expectations, and the RBNZ will be forced to come in agian and stop the party.

If house prices rise on a monthly basis for 3 months in a row, then the bottom may well be forming.

Not sure why spruikers would care as they dont believe in timing the market

Remember the best time to buy, was yesterday.

Do you even need to time the market? The real estate market doesn’t go crazy overnight, even if you waited a few months you won’t overshoot the bottom by much.

I doubt we can say it’s the bottom until after the election. If Labour were to win then boomer PIs may decide to sell up earlier than they would like as their rental returns are less than putting it in the bank. If they intended to hold it for 10 more years then 3 more years of labour may change their mind.

"I doubt we can say it’s the bottom until after the election." This is correct.

If Labour win there's going to be a lot more people besides boomer PIs selling up...& leaving NZ. After the last couple of years we can't say we weren't warned.

Bold claim. If Labour win there will be a lot of unhappy people, because New Zealand has become an echo chamber of misery and despair. Our sporting culture has been intertwined with our emotions, and it's become a competition on who can make themselves out to be the most aggrieved.

The people who have the least to complain about in life, typically successful and wealthy right wingers, make the most noise it seems.

Election day could be the bottom if National get in. Still a while away. If labour get in I’d expect a very quick sell off by property investors causing a big crash.

You are probably correct. That said, the market will go where its going regardless of how people initially react with a new or same govt after the elections - Nat or Lab...it will just be a timing issue for the market.

A big sell off after the elections is probably exactly what the market needs. I'd be calling 'the bottom' if that happened.

Exactly. Last thing Nz needs is 7houseluxon rebuilding the ponzi.

I am very happy to have another 4 years of a labour coalition if it means it breaks nz addiction to a housing ponzi for a decade or more.

..even though Labours "performance" over the last couple of years confirms that if reelected they will break NZs addiction to democracy forever ?

Anchor them with winston - and they will get nothing too stupid done as per the fitst term. And the while housing ponzi will fall. After that therr will be no rekindling it.. and nz will need to find a better way.

Short term pain is better.

I'm not sure how you have come to the conclusion that Labour are going to break NZ housing ponzi. All that has happened under their reign is prices have boomed, and now will bust.

But I can't see anything that they are doing that will prevent it from happening all over again, within a decade or more.

If retail interest rates stabilised I'd look into buying rentals again. There is a lot that's positive in that market with very strong rental demand.

The government is implementing pro-rental policies like increased immigration, it seems no matter where you sit on the political spectrum in New Zealand pro-immigration policies are a general economic panacea for all malaises. I suspect this will rapidly overwhelm any pessimism in housing once rates are appropriately set.

New builds or huge sections only, right?

Tony Alexander said we hit the trough 9 months ago 🤣

But he’s got his nose in the trough..

Based on his consistently wrong reading and predictions Id say his nose is close to his brain - located between his Gluteus Maximus

Mr Alexander is ever the optimist. As a rule, too many economists seem to believe change (sense?) will happen in a market way before it actually does.

An old CEO of mine used to say the economy is like a bellows, expanding and contracting, but you could never know when exactly the bellows would be either full or empty. Mr Alexander's timing (with many other economists predictions) aren't that flash but he's been largely right about when the bellows are expanding and the fact they'd inevitably have to contract.

Just to buck the trend - my prediction is that we'll not see a return to substantial house price growth for many years - 20 or more - for reasons already stated. Investing in 'houses to rent' should be seen for the next 20 years as just another form of low-return saving and/or a community service. I.e. your un-taxed capital gain at the end will - at best - match inflation.

you do realize if the un-taxed capital gain matches inflation, as you said, the yield is probably 3 ~ 5 times of inflation?

Even a disastrous situation like Ireland, the house prices has doubled from the bottom after 10 years.

Even a disastrous situation like Ireland, the house prices has doubled from the bottom after 10 years.

Sweet, all those houses people bought in 2007 are finally selling for what they paid for them 15+ years ago - not. House Price Index for Dublin still hasn't reached the level it was at in 2007, and it's falling again now too.

Correct, here's an article from last year. The property price index graph for 2021 still shows prices 10% off their 2007 peak.

https://www.irishtimes.com/business/economy/property-prices-defy-cost-o…

Exactly - this is just another case of property spruikers with vested interests stating wildly incorrect "facts". Just real estate agent speak, simply not worth considering at all.

The bad facts are everywhere. Many are predicting 70% falls and an end of times scenario where they stay low. But in Ireland, they've spent 8 of the last 15 years appreciating, this in spite of Ireland throwing the kitchen sink at suppressing housing. Rents went up 20% last year there, there are few houses for people to either rent or buy - there's some 80% less houses for rent than there was 10 years ago.

They have solved nothing, and their crash fixed nothing. So claims of this being some fundamental long lived shift have less validity than it being a period of stagnation - unless something else changes that currently isn't on the table.

These are all things to seriously take into consideration when people are trying to evaluate where housing will likely go - because the evidence tends to suggest there won't be any pivotal point being turned where house ownership gets any more affordable under the status quo.

Stating that 70% falls are possible on the basis that our house prices are falling at a much faster rate, and from a much higher altitude, than a place that experienced nearly 70% falls is not "bad facts". It's critical thinking.

Do you know what else happened in Ireland at that time? Their mortgage rates rose from an average of 3.49% in 2005 to 5.25% in 2007. Hmm, peculiar.

Do you think the economic climate of 2005-2007 is any more or less peculiar than the one of 2020-2022?

If you're making analogies, you need to apply critical thought across the width and breadth of all the main parameters.

The Irish bubble has played out remarkably different from the Japanese one. I bet when the Irish one was happening, people were using the Japanese one as a case study, expecting history to repeat, when usually it only rhymes.

Japan was what? 50% down in 20 years. Ireland was what? 60% down in 5 years. End result, both down a shit load. The latter had steeper falls than the former, and fell further.

We have even steeper falls after the biggest bubble of all time, but 70% is absolutely off the cards?

- Tripling of mortgage rates

- Interest deductibility phasing out

- Record numbers of Code Compliance Certs

Maybe migration, demand from the cyclone, and National will save the property market. Curious to know what else you think will stop the falls we're seeing.

it has doubled from the BOTTOM, and has recovered to its peak price. if you talking about the people who bought on the peak, yes, it took 15 years to get back where it was, for home owners they paid a lot, for investors, they get a lower return than average.

but my point was there is still opportunity in property market, depends on how you pick, where you pick and when you pick.

if you got burnt on 1930s from the market crash, does it mean share markets are bad investment vehicle?

Even a disastrous situation like Ireland, the house prices has doubled from the bottom after 10 years.

Yeah I'm just giving context to the "disastrous" adjective in your sentence, since you seem to just want to cherry pick a 10 year period starting at the bottom of a massive bust and repeat a stupid trope.

Yes, in 2022 prices in Ireland finally matched the previous peak of 2006. So 16 years to recover….I’d say the 20 year recovery projection might be about right. We’re falling faster than Ireland was at same stage of correction (see Miguel’s graph)

Yeh, it was just a trough, back to normal next week.

Have we passed the trough in market activity? (yes that was the question posed in the article, as opposed to asking about the trough in prices)

I'd suggest that a market which is moving in non-extreme ways will see normal levels of activity. Extreme drops will stifle activity, extreme rises just somehow stoke the kiwi FOMO story and activity levels stay high. So continued dropping price statistics but without total collapse might match with improved activity levels.

But how much of this do we need to dent the eternal kiwi optimism for future price recovery...

To quote a movie about misallocation of money..."the markets in a tinsy wee valley at the moment"...

March is seasonally the busiest month in RE land. If 2023 follows historical patterns we will see an uptick in activity. Nothing more to see. Sales at very low levels and sighting regular seasonal variations as green shoots is misleading.

The hostile takeover of Interest.co.nz comments section is complete....

Even the editorial position borders on spruikerish - ‘slow but steady’ is an interesting way of describing the market.

We still have some of the highest real house prices relative to income in the world.

As long as the immigration tap isn’t fully opened again house prices will keep falling.

I will be voting for anyone who taxes equity release to buy property as income. Why should fhbs pay 36% tax on the saved dollar to stump up a deposit. The person releasing equity pays no tax even though they have spent the money. It must be income, tax it.

Well to be fair it's a loan. And a loan is "taxed" by the interest it incurs. I'd say banning equity release for a deposit all together, if doable, would be the way to go.

As John Mauldin says , nothing goes to hell in a straight line. Bubble took 14 years to inflate and the Pollyanna chorus think the reversal of cycle is done in a year . Have a listen to what Wilf Richter says on USA

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.