Westpac economists say the average mortgage rate that households are paying will rise by more over the coming year than it has so far during the period of rising interest rates.

In a Westpac Economic Bulletin, senior economist Satish Ranchhod said the full impact of interest rate hikes is yet to be felt.

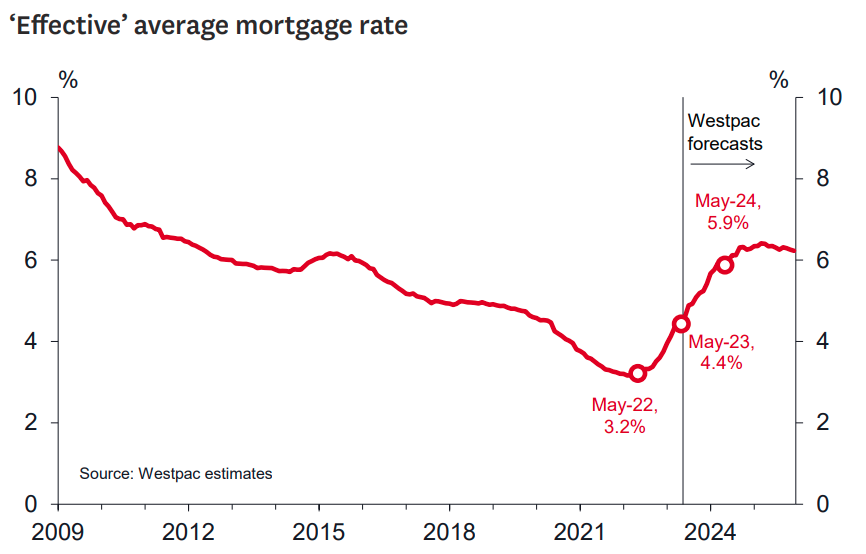

"With 90% of New Zealand mortgages fixed for a period, the pass through of rate hikes has been gradual. In fact, accounting for the extent of mortgage rate fixing, we estimate that the average mortgage rate households are actually paying has only risen by around 120 basis points to date (as a comparison, the OCR [Official Cash Rate] has risen by 525 basis points since late 2021).

"Over the coming year around 50% of all mortgages will come up for repricing and will expose increasing numbers of borrowers to higher rates.

"As a result, the average mortgage rate that households are paying is set to rise by a further 150 bps."

The Westpac economists are estimating a current average mortgage rate for households is 4.4% - and set to rise to 5.9% over the coming year.

They stress that the increase in debt servicing costs they are forecasting is just due to borrowers rolling off earlier low fixed mortgage rates and onto the rates that are currently on offer – "we’re not making any claims about what will happen to interest rates going forward".

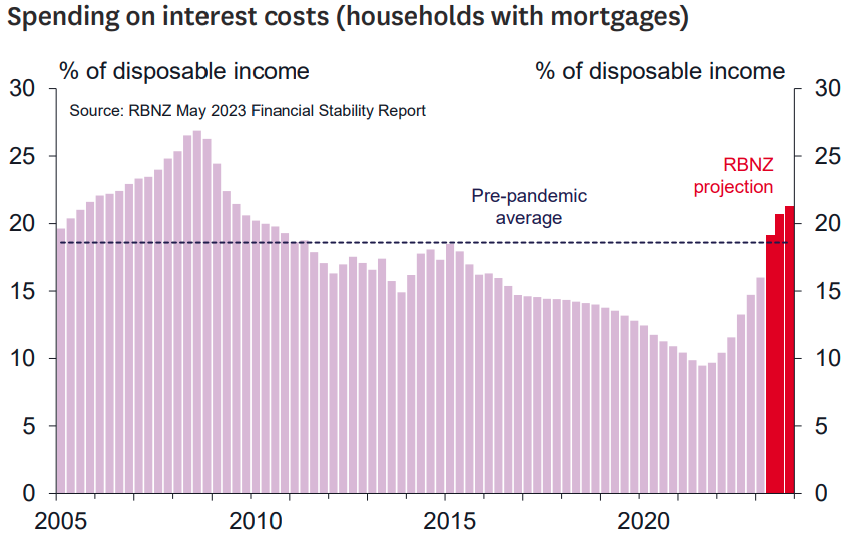

Ranchhod notes that the RBNZ has estimated that households with mortgages could see the share of their incomes spent on interest costs rising to over 20% by the end of this year.

But Ranchhod says the Westpac economists estimate that household incomes have also been pushing higher, rising by around 6% over the past year. "That reflects the strength in the labour market, which has seen wages rising at a rapid pace over the past few years," he says.

"The solid growth in disposable incomes over the past year has seen household spending continuing to rise at a brisk pace, with nominal household spending levels up around 9% over the past year."

Ranchhod said the continued growth in spending does point to resilience in spending appetites in the face of the other headwinds currently buffeting New Zealand households.

"However, as we’ve noted before, a big chunk of the rise in spending has been due to the 6.7% increases in household living costs over the past year. Adjusting for higher prices, the amount of goods that New Zealand households have been taking home has effectively remained flat over the past year even as we’ve splashed out more cash. And some of the increase in overall household spending has been on outbound tourism, which for the most part does contribute to the local economy."

The other impact of those strong price rises is that savings rates have started to ease back," Ranchhod says.

"New Zealand households are now saving around 1% of their disposable incomes, down from over 2% last year. This might imply a reduced buffer to support spending in future."

Ranchhod notes that Stats NZ’s latest update also revealed that the level of household wealth fell by $42 billion in the first three months of the year. That was the fifth consecutive quarter of decline in household wealth levels, with a total drop of 9% since the end of 2021. That decline has mainly been due to the 17% fall in house prices since interest rates started rising in late 2021.

"That’s a particular concern for those families who first entered the housing market in the past couple of years. Many of those families will now be looking at higher debt servicing costs, while the value of their homes has fallen since taking out a loan. In addition, they will not have had the chance to rebuild their savings since purchasing a home. More generally, lower levels of household wealth might also discourage future spending.

"That said, it does look like the housing market is now finding a base. With signs that borrowing costs are close to their peak and population growth surging, the past few months have seen earlier declines in both house prices and sales flattening off. Looking ahead, while we don’t expect further material house price falls, we don’t expect to see house prices rising sharply given the current contractionary level of interest rates."

Ranchhod says he expects the pressure on households’ finances will continue to mount.

"That’s mainly due to the continued rise in debt servicing cost. At the same time, even though inflation is starting to ease, cost of living pressures remain intense. Those pressures are being felt by every family across the country. However, they’ve been especially tough for those families on lower incomes due to the large increases in the prices for necessities, like food and utilities. Such families will also typically have smaller savings buffers that they can draw upon.

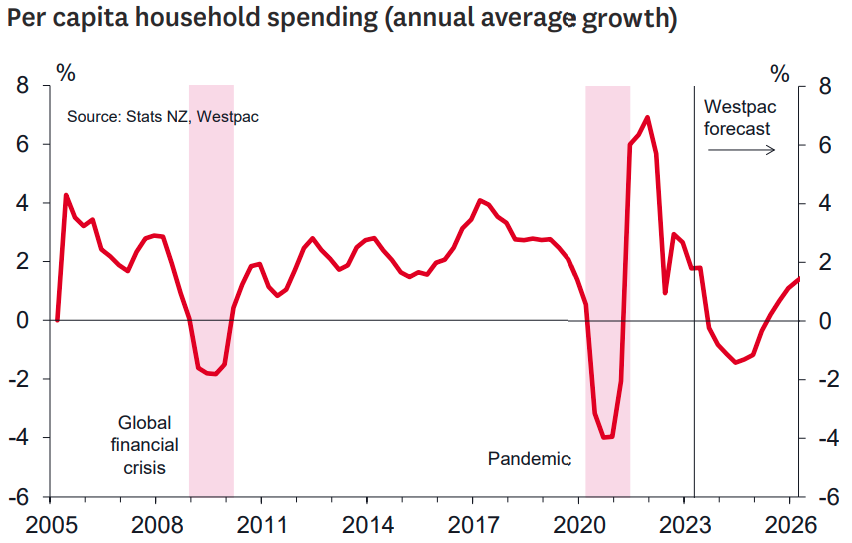

"Those mounting financial pressures will see per capita household spending falling by around 2% over 2023 and 2024 combined. And with household spending accounting for around 60% of total economic activity, that will be a significant drag on economic growth."

124 Comments

Not sure where the 120bps increase in the average mortgage rate comes from. Ours went up 300bps & we're still 150bps behind where it is currently. Timing perhaps.

some people split that mortgages into few chunks, and fix for different terms and rates. for some who fixed 3 years or more back 2021, they will still be on lower rates while part of the loan may renew on higher rates. On average it'll be lower than the running mortgage rates of the day.

It is partly the result of using "averages" when they shouldn't be used because they're misleading. See my post below.

You are correct, averages are misleading. So what’s your point?

We just got the dreaded email saying that our high 2% mortgage was due for re-fixing soon. Going to be high 6% now. I suspect there will be a lot more people like us that the real belt tightening has only just begun. The second half of this year is going to be "interesting"

Belt tightening for the average households has meant fewer overseas trip, putting off home renovation and sweating the old couch for a bit longer but we're still buying the daily latte with cheese scone. Hospitality and food retailers are reportedly still witnessing strong sales (up 9.4 YoY to June 2023) and also have been able to pass higher costs on to customers.

Survivor bias too. Those that are alive today will be doing better because of those that have closed.

What rate were you on late 2019 / early 2020?

It is not the rate that hurts, it is the level of debt.

How does this reconcile with banks saying that the property market is at bottom?

The Goldilocks scenario as they have mentioned. Not too hot. Not too cold.

"Looking ahead, while we don’t expect further material house price falls, we don’t expect to see house prices rising sharply given the current contractionary level of interest rates."

After reading this whole commentary, you get the feeling Westpac is trying to worm itself out of any kind of responsibility and trying their darnedest not to spook the sheeple.

How is that even possible considering distress is just beginning with likely incoming job losses.

How is that even possible considering distress is just beginning with likely incoming job losses.

Well you cannot prove that conclusively. As I said, Westpac is doing its best not to spook the sheeple. Not in their interests.

I get the distinct feeling that the majority of people already know we are on the economic downturn and accelerating, but everyone around us in business and parliament is smiling and sweating bullets trying to tell everyone that everything is fine and to stay optimistic. While I appreciate we don't want bank runs and complete loss of confidence in the investment side of things, the disconnect is growing by the day.

Liam Dann at the Herald argues we're wealthier than we were before the pandemic because monetary tightening has failed to curtail household spending across the economy. The man conveniently left out fiscal easing from his entire analysis.

The Crown is on-track to spend $30b more in the year 2023/24 than it did in 2019/20. Over 1 in 3 jobs created since 2019 are either in central government, aged & residential care, hospitals, local councils or allied health services.

I actually don't have a problem with Public Debt spending, as long as it's counterbalanced with an equivalently less Private Sector Debt take-up. And as your paragraph looks to indicate, that's not happening enough - yet. We need to reconstruct our economy - the natural disasters of recent times being an obvious one. But also our neglected critical infrastructure. And if that means more Crown Debt, so be it if it's balanced in our national accounts. But you're right - we certainly aren't wealthier, and haven't been increasingly so for a decade and more. Just more in indebted.

That's right. I recently came across a Treasury paper from 2011 that said (paraphrasing) " longterm wealth can be measured by a nation's investments in productive capacity for exports".

Barring a small portion of spending since Covid on apprenticeship subsidies and a select few shovel-ready projects, much of this borrowed money is just propping up aggregate demand (welfare payments, hiring bureaucrats and consultants, agency rebranding, etc.).

I don't think you can welfare spend your way out of this (recession or whatever we call the next few years).

The classic musicians on the Titanic scenario.

The Banks are huffing jenkum to believe that. They are doing everything they can to keep the bubble from burning them or earning them blame despite being the primary facilitator of the whole crisis.

Interest rates are roughly as high as they are going to get (supposedly), so the demand side shouldn't change too much from now. The supply side will be affected by this as more sellers come under mortgage stress. Will this be balanced out by other factors (such as immigration, changes to tax rules, etc), who knows?

Exactly.

Also lots of new housing supply hitting the market now and over the next 5-6 months.

Because what you can afford to buy is determined by current mortgage rates. Not the rate fixes of a year ago rolling off. So if interest rates are at/near peak then this this is the bottom of the affordability issue for buyers.

What about inflation of everything else and the affect on affordability?

Has almost nothing to do with mortgage affordability and house prices.

That’s not quite true, if cost of living has increased significantly - as it has - then people have less money to spend on housing (servicing a mortgage)

Yes, that's how i see it. Perhaps pragmat could explain rather than slamming the point made.

slamming? lol.

Nope, I think i'll let the DGM conclave enjoy their mutual self pleasuring.

It doesn’t

The talk of a Market Bottoming is total Real Estate agent/Onegoofy Tosh!!

Its marketing BS on Roids!

The bottom talk is like a 20ft deep pool, full of thick mud, being tread by a fat and tired 5.6ft woman......its not going to end well.

Looking around, there are lots of these in NZ! - male varieties this length too.......

dp

Ominous!

Another way in which the older generations are kicking the younger ones.

My wife and I crunched the numbers on what it would take to buy our first property. Same property, 12 years ago. It has gone from $750k to $1.8m (it is in Remuera). Adjusting for incomes we would need about a ~$1m deposit now and we only had $100k... there is no way we could have bought it.

When people say the older generations are pulling the ladder up behind them we tend to think back 30 years but it is also far more recent.

Smashing interest rates now is unfortunatly smashing the same people that have struggled to buy.

Sadly you cannot bring house prices down without someone getting hurt and sadly this will be those with mortgages as opposed to those who have multiple houses mortgage free from having highly favourable economic conditions to allow them to do so with less risk and mass capital gains. I'm interested to see if TOP can get enough votes to influence the implementation of a land tax which would level things out somewhat.

I’m seriously thinking about voting Top, not sure if it would be a wasted voted though.

Do it Nellbell - there'll be at least two of us.

When’s the last time an election was swung by one vote? Almost all votes are wasted; vote for who you want.

I counter that by pointing out that votes for both Lab and Nat have arguably been a wasted vote. Both are equally as complicit with many of the issues now rearing their head.

TOP can have my vote, i don't consider it wasted at all.

Voting Top is voting labour, greens and maori. Vote National, ACT, and once they are in by all means vote TOP. I say that as someone who doesn’t care now, it’s Australia for me in the future anyway. A National Government will slow my exit but unfortunately the decline in this country and the racist undercurrent from Māori has been enough for me to say nah.

[Aside from on here] TOP seems to be no public profile anymore.. a wasted vote.

They're focussing their resources on Ilam at the moment.

Have had many conversations around the water-cooler at the moment just like this.

For the past 30 years I have voted for either Labour or National, if I keep on voting for these 2 parties for another 10 + years expecting some progress and betterment in the productive and lower income sectors I am very sadly mistaken. If you keep on doing the same thing expecting a change, don't, it will not change.

So vote TOP with me, at least they have a plan.

They should set up one of those vote swap sites. Basically get Raf Manji voted in and then work up from there.

Hugh

You make valid point; yes, it is going to get pretty tough for those with a mortgage.

However, you really need to get over the "poor me" envious, boomer blame-shifting attitude.

For heaven’s sake; you live in a $1.8m Remuera home and no doubt are in a well-paid job.

There are plenty doing it really tough. You and your family are far better off than those without a home and living in emergency housing; or those working long hours in a shite job on minimal wages and living in comparative poverty; or those farmers who are not also facing increasing mortgage rates but are facing loss of production due to recent heavy rainfall; or all the victims of Cyclone Gabrielle – both in Auckland and rural areas - who have lost their homes and contents and face a very uncertain future.

You really are in need to appreciate what you have. Yes, you are going to have to belt tighten and for you it’s no doubt for you its going to be relatively tough, but your comment come across as self-centred and entitled blame-shifting. Maybe you have had it too good so far for all your life?

Cheers

Have a happy day.

"you really need to get over the "poor me" envious, boomer blame-shifting attitude."

Huh? we sold it years ago and have done numerous things, property and non-property. I/We are sorted so this was illustrative only.

I think you need to re-read my post and focus on improving your reading comprehension.

He’s in the business of misrepresentation. Or maybe he’s going a bit senile. I have never been certain with him. Perhaps a bit of both.

He’s certainly good at pompous and self righteous condescension, as amply demonstrated above.

We bought a section in Wigram CHCH for $240k in 2015.

Sections less the half the size in Halswell (about 2-3km away, further from the city) are now being sold for $450-500k.

It would be fair to lay blame on Robertson 51 Ardern 42 and Orr 60 so its just your bias blaming Boomers who simply responded to what these clowns legislated. Ardern was the critical component which reminds me of the saying young enough to know everything and understand nothing whilst decrying the wisdom of the oldies who built the country she was appointed to ruin rather than run.

We could definitely have property down 40% nz wide by this time next year. That’s the drop that will be required to get a sale across the line with the return of long term normalised interest rates.

I would think places with low turnover such as the West Coast would take 2years to catch up to other places such as AKL/WLG with high turnover and hence more responsive to interest rate change.

The Westpac economists are estimating a current average mortgage rate for households is 4.4% - and set to rise to 5.9% over the coming year.

No, no, a certain person who is indeed very certain, knows better than the banks who issue the loans, mortgage rates were 7% last year and they are going to be 10% this year, not 5.9%, this he/she guarantees by… well… absolutely nothing!

He who speaks for the prophet hold the highest of reputational risks. No need to bag on them, just wait and time will be the ultimate reckoner of opinions. Maybe them, maybe you. Until then we are all free to make our own predictions for all to see.

"He who speaks for the prophet"

Are you guys from Gloriavale ?

by Yvil | 10th Jul 23, 1:10pm - "He who speaks for the prophet" - Are you guys from Gloriavale ?

Stereotyping now - LOL!

Follow what you preach.. else stop preaching

Average across everything (including old fixes). Currently current lending is a lot higher than 4.4%.

Reality approaches. Those selling now may want to think about that or simply delist and plan to hold for the medium term. The window of massive speculative exit is over. Paper gains are theory until an actual sale occurs and the funds have transferred.

Letter in the mail this lunchtime with the obligatory, "Your variable rate mortgage is going up. The Standard Rate on 21/7 will be 8.49%" That's more like it! (One day, they'll also have a good look at whether Offset Loans are a good idea) Still a way to go, though - and it's going to go on for way longer than most anticipate.

"If it's not hurting, it's not working"

That’s a nice risk free return you’re getting on that money right there.

Indeed. And there's no way I'd get it now. But, it distorts the stats on both sides of the national balance sheet. It shows both an increase in the banks' liability column, Deposits, and their asset column, Loans Outstanding, when is net reality it's neither.

This use of 'averages' in banking communications disgusts me.

Sure - use them if you're talking normal distribution curves. (aka bell curves.) This is okay where the bell curve is tall and narrow but far less okay when the bell curve is low and wide.

But are mortgage holders nicely distributed on a bell curve? Hell no! (I know this from analysis I did some years ago.) In fact the shapes are about as far away from bell curves as you can imagine. And they vary by lender. And over time. Talking 'averages' in such instances is a nonsense and only serves to play down the fact that that the OCR is a massively unfair tool.

As I said, this use of 'averages' disgusts me. Even more so when banks and the RBNZ - that have highly skilled people wo know that using averages like this is misleading - continue to do it.

It clouds the problem and ends up pretending "we" are all in the same boat. "We" are not.

Another issue for the banking inquiry to look into? Methinks so.

(Remember the room of 20 people and John Key walks in? The average wealth in the room went up. So yeah - averages are massively misleading when the distribution is highly skewed and/or fractured!)

Sure - use them if you're talking normal distribution curves. (aka bell curves.) This is okay where the bell curve is tall and narrow but far less okay when the bell curve is low and wide.

This is called 'variance.'

I disagree with you about averages (mean is a better word). They are good. As long as you also understand var, median, popn size, sample sizes (without these you can't work out std dev, MoE anyway) - the fundamentals of measures of dispersion.

Most people have a dreadful knowledge and understanding of statistics.

re ... "Most people have a dreadful knowledge and understanding of statistics."

As - apparently - do you.

To prove me wrong - please suggest what sort of distribution curve you think the major lenders of residential property have on their book?

By all means - if you can't describe succinctly - provide examples with pictures from the internet.

Unless you've been privy to this 'closely guarded commercially sensitive' distribution curve ... Your talking out of orifice that I can't mention. ;)

As - apparently - do you.

To prove me wrong - please suggest what sort of distribution curve you think the major lenders of residential property have on their book?

They have a distribution curve of all the property on their books. Nothing more, nothing less. To the extent their portfolio is representative of the wider mortgage market can likely be estimated. But much easier to merge data sets.

Trust me. I know my stuff.

Your reply says nothing. Ergo - You know nothing. Time to climb down.

Worth a read - for those like J.C. that think I'm moaning about nothing ... https://hbr.org/2002/11/the-flaw-of-averages

Sorry ... Maths is a bitch. But if you don't understand the maths you become a "mum and dad" investor and banks - that love profits before their customers - will just love you to death. (Which in too many cases - is the only way you'll ever break their loving embrace.)

Worth a read - for those like J.C. that think I'm moaning about nothing ... https://hbr.org/2002/11/the-flaw-of-averages

This article supports what I say. The more information one has about a data set (particularly popn, sample sizes, variance, and mean) the more accurately one can determine what we call the statistical margin of error.

And another .... https://towardsdatascience.com/why-averages-are-often-wrong-1ff08e409a5b

Because I'm cross. No other reason. :-)

This should be reported as a 'weighted average' rather than a plain average. Weighted by mortgage size. If it is, then there's nothing wrong with this as a measure of health (or not) of the mortgage market.

For them to report a weighted average - they'd have to explain how they calculated the weighted the average.

They never will. It is (supposedly) hugely commercially sensitive.

It actually isn't - it just persists the myth they are working in dark magic that nobody could ever understand except them.

It also helps the RBNZ hide behind the fact they are lazy, inept people unwilling to come up with something better than the OCR when inflation must be tackled.

This level of discourse from banks - when real facts could be used to inform - rather than obfucisate - disgusts me.

I listened to the property hour on 1ZB yesterday.

Callers saying prices might go down were cut off with: we're not here to crystal ball gaze.

Then the hosts went on to say why some rural areas may go up because of working form home, retirees, etc. Recommended people use the OneRoof property valuation calculator.

Both (ZB and oneroof-Herald) are owned by NZME - so no surprises there.

Use censorship where legally possible - it protects the narrative and keeps the advertising revenue flowing.

It's sponsored by One Roof 'The One Roof Radio Show'....come on now don't be surprised that they dont want anything negative said about the market in this hour...it's not what One Roof is paying for.

Why would you expect anything else?

The "Nifty1 Arousal Hour"🤣

I don't listen, it's the anti spruikers that get some kind of kick out of it... kind of like you and TA, RP...

Something weird going on with the DGM's fixation with TA, Do the Spruikers even follow TA ? I don't but I get labelled one on here.

Zwifter, like TA, you've got fixated with bottoms. Despite the stacked odds against a sustainable recovery (or bottom), every month you predict one is coming the next month!

I say, as long as you're comfortable being the entertainment - like TA, go hard out.

Ok RP you win, the whole of New Zealand is waiting on tender hooks for YOU to call the bottom of the housing market.

LOL! The whole of New Zealand will know when its not - when you blindly follow TA and "call it".

Remember, it was you that said quote "predictions don't need to be supported by facts"

Recent FHB's can be excused for feeling mislead by some previous "calls" made by TA and other high profile "professionals" of this industry.

Tones the Comb has led many FHB sheep to the slaughtermans knife......he promised his sheeple a good 5% gains will be had in 2022.......all his intelligence said so.......

He is a roach.

Just like a roach, he keeps coming back and is hard to get rid of.

How long till Comb-Over?

It's probably easier to predict when The Comb will "step away for personal reasons"

This is the perfect storm that for some, are weathering right now, others can see it on the horizon. High inflation, stalling wage growth/unemployment and high interest rates. It’s going to be a hell of a ride for business to maintain a profitable level of sales and for households to get through

I read a lot of rhetoric about 'boomers' robbing the future of the younger generations. I wonder exactly how much fact there is in that.

What is the demographic spread of investors owning multiple properties?

When I sold my home by tender in Karori in 2018 (Western valley bottom), not premium location, it was bought by a FHB in their 30s. No tenders submitted from property investors. I felt a bit quilty accepting the 50% increase in cost since purchase in 2014, which I banked. Believing at the time that property values were ridiculously high - then 3 more years rolled by...

And what did you do after you sold your home? Rent? Buy another?

But don't be fooled into thinking a FHBer of a few years back wasn't an Investor. The 'advice' given back then was "If you can't afford to buy in Auckland, buy in (Hawkes Bay) where it's cheaper and wait for the capital gains to increase you deposit money for back in Auckland. Get on the first rung of the ladder anywhere you can!"

Of course, that pushed the prices in the regions; places like Gisborne, out of reach of true homebuyers there, and so we have the problem that IS being solved for us today by higher mortgage costs.

I banked the gain then did a 2 year volunteer posting in Timor Leste. When I got back in 2020, I semi retired and bought a house debt free back where I hail from in rural Hawkes Bay.

Just got off the phone with Kiwibank as my pre-approval is due to expire. Six months ago I was tested at 7.75%. Now I am being tested at 8.75% ... ouch. That is tight alright!

And 2 years ago the test rates were mid 5's. Amazing how a long term test rates can be so fickle, it's almost like those setting them either don't know what they're doing.

Or maybe they were motivated to "push the envelope" to increase their loan book size and got caught out by inflation so are hurriedly ratcheting them back to where they should have been to begin with. Borrowers should have known better anyway.

Orr to the banks: "Have some free money on meeee it's called the FLP"

Banks: "yoink"

I think Kiwibank stress-tested us at 19%, using affordability calc on other banks we could potentially borrow double what they gave us for pre approval.

There will be a few X and Y who will be wishing they had not listened to their parents, agents, advisors and bankers who all said” you cannot lose by buying property”. They would have been better waiting for the inevitable pull back after the silly times we recently experienced. Some will lose their homes. I hope mum and dad reimburse the deposits lost.

For those who bought in recent years, much of the deposit came from Mum and Dad anyway.

"There will be a few X and Y who will be wishing they had not listened to their parents, agents, advisors and bankers who all said” you cannot lose by buying property”

These are some reasons given in the mainstream media, property market commentators, property market promoters, bank lending promoters masking as bank economists, real estate agents, property market mentors & other sources as to why property prices in Auckland will not fall by much and that there is a low probability that property prices will fall dramatically:

1) during the GFC, house prices in Auckland fell only 7-10%

2) over the past 50 years, house prices in Auckland have averaged 7.2% per annum (or commonly referred to as house prices doubling every 10 years). This trend can be expected to continue into the future - https://youtu.be/Agp9xFWoBX4?t=172

3) there is a shortage of underlying housing in Auckland, so property prices won't fall by much - https://www.interest.co.nz/property/97513/auckland-councils-chief-econo…

4) there is a growing population which means that there will be more demand for houses - https://www.stuff.co.nz/business/106883553/house-prices-have-fallen-but…

5) we have inward immigration which means more demand for houses

6) Auckland is an attractive city with an attractive lifestyle - that makes it desirable and attracts foreigners to move to Auckland and hence raise the demand for houses

7) we mustn't forget either the vested interests in ongoing stability. No government, central bank or trading bank with mortgage exposure wants materially lower house prices. Nor does an incumbent Beehive want falling house prices going into an election campaign https://www.stuff.co.nz/business/110499233/think-house-prices-are-going…

8) the economy is doing well, with low unemployment - https://www.stuff.co.nz/business/110499233/think-house-prices-are-going…

9) there has been insufficient construction of new builds to meet the housing shortage - https://www.stuff.co.nz/business/106883553/house-prices-have-fallen-but…

10) there are high construction costs to building a house. House prices cannot fall below their construction cost. - https://www.stuff.co.nz/business/106883553/house-prices-have-fallen-but…

11) people don't sell their houses at a loss - https://www.stuff.co.nz/business/106883553/house-prices-have-fallen-but…

12) continued inflation means that house prices will continue to rise in the future

13) The fact is, debt levels have barely changed from the beginning to the end of those 10 years, compared to GDP levels, compared to household assets, compared to household disposable incomes. And much more importantly, debt servicing is very much easier now, an item that is almost universally overlooked. We are not pushing out to unsustainable levels now, and even if they creep up a little, we are far from that point. https://www.interest.co.nz/opinion/95894/if-you-think-new-zealands-hous…

14) in aggregate household debt servicing is low in New Zealand - currently at just under 8% of disposable income of households - https://www.rbnz.govt.nz/statistics/key-graphs/key-graph-household-debt

15) property market participants & commentators who have been correct in their predictions about recent property price trends have more credibility and hence their predictions of upward prices are believed by a wider audience (such as Ashley Church, Tony Alexander, Ron Hoy Fong, Matthew Gilligan, etc). - https://www.stuff.co.nz/business/84322204/all-predictions-of-an-aucklan…

16) previous warnings about a house price crash have been wrong - property prices have continued rising upward significantly since these warnings were given, so there is little reason to believe these warnings.(such as Bernard Hickey) - https://www.stuff.co.nz/business/84322204/all-predictions-of-an-aucklan…

17) its unlikely Auckland prices collapse. I think the main two reasons though are: a) Affordability has been this bad, and worse, in the past and it only resulted in about a 10% drop. b) The number of homes built over the last decade has been too low and will take some time to recover

18) Not a single person who bought 10 years ago has ever regretted buying / have you met anyone who has bought a house and regretted buying it?

CN you have missed out on one reason why some FHBers are in a pickle. Some of them borrowed large amounts to buy their first home when interest rates were at a low artificial level and houses were at silly high prices because of those rates. We now have much higher borrowing rates, falling house prices and the cost of living has gone through the roof. Some would call that a cluster disaster or words to that effect.

It wont feel like a big problem until it feels like a big problem...

Not just first home buyers who got themselves into a pickle.

There are other residential real estate owners in cashflow stress.

How many of these owners will be unable to hold on?

Under conditions of rising house prices, many buyers chose to ignore this message in February 2021:

https://www.stuff.co.nz/national/politics/300238808/reserve-bank-govern…

"Some will lose their homes"

FYI, here are examples of owner occupier collateral damage from falling house prices elsewhere around the world:

1) https://www.investorschronicle.co.uk/.../aft.../article.html

2) https://youtu.be/iKPG_l1P7lk

3) https://youtu.be/ugBKnP2FKDM

4) https://youtu.be/fiCXsu_4BoA

A relation in Auckland is currently trying to sell as the interest rate on his $900k debt is about to double. He cannot service that loan and live. He will not be the only one up there. To say he is currently feeling very flat is an understatement. And he has a big salary.

In case you missed it

https://www.stuff.co.nz/business/property/132483897/mortgage-rate-pain-…

How many owners will be unable to hold on?

I hope it has many bedrooms to rent out.

What were property commentators saying at or just after the peak?

1) Tony Alexander - 19 reasons why there's no crash - December 2021

https://ndhadeliver.natlib.govt.nz/delivery/DeliveryManagerServlet?dps_…

2) Catherine Masters - July 2022

Why the New Zealand housing market is nowhere near crash point

https://www.oneroof.co.nz/news/why-the-new-zealand-housing-market-is-no…

3) Ashley Church - April 2022

Four reasons the housing market won't crash

https://www.oneroof.co.nz/news/ashley-church-four-reasons-the-housing-m…

4) Kelvin Davidson - Dec 2021

“But will prices actually fall? I’m not convinced because in the past a serious housing downturn has come with a recession, but no one is suggesting that and unemployment is low at 3.4 per cent.”

https://www.stuff.co.nz/life-style/homed/real-estate/127305870/what-lie…

5) Nov 2021 - Here's why it might be fruitless to pin your hopes on a house price crash

https://www.stuff.co.nz/business/300449314/heres-why-it-might-be-fruitl…

I wonder how long it will be before those links don't work anymore :)

The Dec 2021 publication of Tony's view has been removed from his website already.

The link above is to the archive version at the National Library of NZ. Previously this site was searchable for previous publications of Tony's views but this collection is no longer accessible or searchable at their website to my knowledge.

The Scrolls will always be available to ALL.

The Prophecies of The Prophet are 100% Correct.

Those who heed the Warnings will Prosper .

10 reasons! 15 reasons! 19 reasons! Do I hear 20?

One of the reasons must be right, right?

This shows the volume of mortgages due for refixing in the future - some pain to come yet https://datawrapper.dwcdn.net/mXAfw/1/?utm_source=substack&utm_medium=e…

uuuhhh, great link!

Setember and October look interesting...

As an average Joe this article reads like Interest rates are going to go up more next year than they have in the past couple of years. Which is absolutely ballocks. This whole article is bloody ballocks.

This bloody fear mongering needs to stop!

I don't think they'll go up too much more than the relatively normal rates they're at now.

Mortgage size is directly proportional to perceived fear mongering of any given literary work.

They're predicting the average rate people fix on will go up as more people roll off past lower fixed rates to present higher fixed rates. Not that the average market rates will increase by that much. In fact, most banks called "peak" already, but has since been a little upward movement.

It's not fear mongering. Simple as: "As people move from 2.x% to 6.x%, they will be paying a higher interest rate."

Appreciate the explanation

I'll tell you what I think of the doom and gloom. I've just spent $1.225m on a couple of acres on the outskirts of Auckland in an area I think has potential.

Yes and I suppose you got it dirt cheap and you've already been approached by a cashed up developer (if there is such thing) who has ambitious plans to build a Retirement Village. For someone who repeatedly states to ad-nauseam they ignore the advice of DGM's, you felt compelled to become a member here 6-months ago.

Is there something on your mind?

No I haven't been approached by a developer. I discovered decades ago that listening to doom merchants was a failed policy, it cost me a lot of money. Since then I've made decisions based on some research and gut feeling.

For a bit of fun I started debating with goldbugs about 20 years ago. They kept telling me how the world economy was going to collapse, WW3 was imminent, Russia would rule the world because they had a heap of gold, the USD would collapse, interest rates would go exponential, the US economy was doomed and gold would soar to US$10/20/30,000 etc. etc. There's very large numbers of goldbugs out there.

Poor ol' gold 'stackers' are still staring at a pile of useless metal while I've made a fortune out of property.

I wish I'd bought a bunch of 'useless metal' 20 years ago. Returns are more than 500%. Maybe property was a better bet but gold bugs have done ok.

Depends on when you bought it , goldbugs always start from 20 years ago, but go back further and it's been a disaster. And there's no income off a 'stack'. Goldbugs never adjust their gold price for inflation, for very obvious reasons, it would make their 'investment' look terrible.

New technology can locate oil and metals faster than ever, so each time the price spikes up there's more exploration which soon moderates the price. That's why Putin's war against Ukraine has blown up in his face, the oil price has plunged, the opposite of what he anticipated.

People need a place to live, they don't need a pile of metal.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.