For the first time in quite a while gaps have emerged between banks' carded mortgage rate offers. A tight spread has given way to a wider range.

This started with ANZ's aggressive rate hike on April 15, was matched by Kiwibank's equally strong rises on April 15, but not followed by BNZ's changes on April 23. And so far, ASB has made no recent moves.

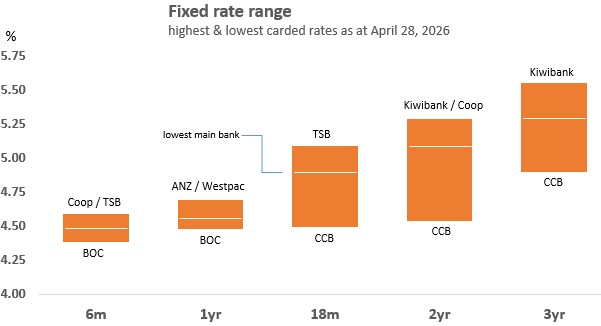

That has spread out the rate offers, allowing borrowers real choice of "lower rates".

But don't expect ASB to stay on the sidelines for much longer.

However, at this time, there are strong reasons to choose lower rates at some banks rather than others.

The spread between the lowest and highest offers are marked for a two year fixed mortgage. Kiwibank and the Co-operative Bank have a 5.29% carded rate, whereas China Construction Bank still has a 4.54% carded rate for this popular term.

That is a 75 basis points (bps) spread.

Even just among the main banks, the two year spread from lowest to highest is 20 bps, still a worthwhile difference.

Wholesale swap rates continue to rise and this trend is unlikely to be over, so locking in a rate is something you should think about. The next local market influence will come next week when the Reserve Bank of Australia (RBA) will tip its hand about how it sees the inflation risk they face. Financial markets have priced in 20 bps of a 25 bps rate hike for the RBA May 5 review.

The Reserve Bank (RBNZ) reviews the Official Cash Rate next on May 27. Financial markets have priced in half of a 25 bps hike then, and fully priced a hike for the following July 8 review. OCR reviews don't directly affect two-year fixed rates, but they do indicate central banks, and markets, are worried about future inflation.

To compare mortgage rate offers in a way that includes the application and account fees costs, or break fee costs if you need to do that, and applying the impact of a cashback/legal fee reimbursement, or other incentives, you can use our home loan comparison calculator. You can find it here. Or, for convenience, we have added it to the bottom of this article.

Negotiate, (even with your mortgage broker). How flexible banks may be will depend on the strength of your financials.

One other useful way to make sense of the changed home loan rates is to use our full-function mortgage calculator which is here.

And if you already have a fixed term mortgage that is not up for renewal at this time, our break fee calculator may help you assess your options. Break fees will be minimal in a rising market.

Here is the snapshot of the lowest advertised fixed-term mortgage rates on offer from the key retail banks at the moment.

| Fixed, below 80% LVR | 6 mths | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| as at April 28, 2026 | % | % | % | % | % | % | % |

| ANZ | 4.49 | 4.69 | 4.99 | 5.29 | 5.49 | 6.19 | 6.29 |

| 4.49 | 4.59 | 4.85 | 5.09 | 5.39 | 5.55 | 5.69 | |

| 4.49 | 4.65 | 4.85 | 5.09 | 5.29 | 5.59 | 5.79 | |

| 4.49 | 4.65 | 5.29 | 5.55 | 5.89 | 5.99 | ||

| 4.49 | 4.69 | 4.99 | 5.19 | 5.29 | 5.39 | 5.59 | |

| Bank of China | 4.38 | 4.48 | 4.68 | 4.78 | 5.08 | 5.38 | 5.58 |

| China Construction Bank | 4.40 | 4.49 | 4.49 | 4.54 | 4.90 | 5.10 | 5.20 |

| Co-operative Bank | 4.59 | 4.65 | 4.99 | 5.29 | 5.49 | 5.75 | 5.89 |

| ICBC | 4.39 | 4.49 | 4.65 | 4.89 | 5.15 | 5.45 | 5.65 |

| |

4.49 | 4.59 | 4.85 | 5.09 | 5.29 | 5.55 | 5.69 |

| |

4.59 | 4.59 | 5.09 | 5.19 | 5.49 | 5.69 | 5.79 |

Fixed mortgage rates

Select chart tabs

Daily swap rates

Select chart tabs

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.