On June 3 ANZ increased its fixed home loan rates across all periods.

We wondered first when their main rivals would follow.

And then we assessed what the wholesale swap rates were telling us. There didn't seem to be urgent market pressure to raise rates at that time

It has now been more than a week, and only two of the challenger banks have followed ANZ. But none of their main rivals.

And that has opened up a competitive disadvantage for ANZ.

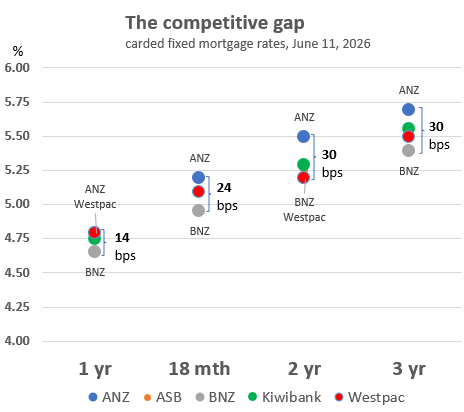

For a one year fixed rate, their carded rate is 14 bps higher than some key rivals.

For 18 months fixed it is a 24 bps gap.

And for two and three years it is now a 30 bps gap. And 30 bps is a lot.

Of course in the competitive cut and thrust of individual deals, ANZ can discount even if it doesn't change its carded rates.

But the perception remains that ANZ is the most costly option for home loan borrowers at this time. And the only way to dispel that view is to back-track on those week-ago increases. Or of course, perhaps others will eventually raise rates too. But there isn't obvious cost pressure to do so.

And that is reinforced by ANZ not raising term deposit rates other than for two specific terms, and not to any level that makes them special.

To compare mortgage rate offers in a way that includes the application and account fees costs, (or break fee costs if you need to do that), and applying the impact of a cashback/legal fee reimbursement, or other incentives, you can use our home loan comparison calculator. You can find it here. Or, for convenience, we have added it to the bottom of this article.

Negotiate, (even with your mortgage broker). How flexible banks may be will depend on the strength of your financials.

One other useful way to make sense of the changed home loan rates is to use our full-function mortgage calculator which is here.

And if you already have a fixed term mortgage that is not up for renewal at this time, our break fee calculator may help you assess your options. Break fees will be minimal in a rising market.

Here is the snapshot of the lowest advertised fixed-term mortgage rates on offer from the key retail banks at the moment.

| Fixed, below 80% LVR | 6 mths | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| as at June 10, 2026 | % | % | % | % | % | % | % |

| ANZ | 4.69 | 4.79 | 5.19 | 5.49 | 5.69 | 6.39 | 6.49 |

| 4.49 | 4.65 | 4.95 | 5.25 | 5.49 | 5.69 | 5.89 | |

| 4.49 | 4.65 | 4.95 | 5.19 | 5.39 | 5.59 | 5.79 | |

| 4.49 | 4.75 | 5.29 | 5.55 | 5.89 | 5.99 | ||

| 4.69 | 4.79 | 5.09 | 5.19 | 5.49 | 5.59 | 5.79 | |

| Bank of China | 4.38 | 4.58 | 4.68 | 4.88 | 5.18 | 5.48 | 5.68 |

| China Construction Bank | 4.40 | 4.49 | 4.49 | 4.54 | 4.90 | 5.10 | 5.20 |

| Co-operative Bank | 4.59 | 4.79 | 5.15 | 5.39 | 5.65 | 5.85 | 5.99 |

| ICBC | 4.39 | 4.49 | 4.75 | 4.99 | 5.25 | 5.45 | 5.65 |

| |

4.49 | 4.69 | 4.95 | 5.19 | 5.39 | 5.55 | 5.69 |

| |

4.69 +0.10 |

4.79 +0.10 |

5.19 +0.10 |

5.25 | 5.59 +0.10 |

5.89 | 5.99 |

Fixed mortgage rates

Select chart tabs

Daily swap rates

Select chart tabs

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.