The Reserve Bank (RBNZ) has decided to leave mortgage lending restrictions as they are, citing concerns low interest rates could prompt banks to lend more to borrowers with small deposits.

Governor Adrian Orr said loan-to-value ratio (LVR) restrictions will stay at current levels as there remains a “risk that prolonged low interest rates could lead to a resurgence in higher-risk lending”.

The RBNZ also said, in its biannual Financial Stability Report released on Wednesday, that "there are early signs that housing lending risk may be increasing again".

"House price growth has strengthened in recent months, even with high price-to-income ratios, and it is unclear how long this strength will persist."

Currently banks are allowed to make no more than 20% of their residential mortgage lending to high-LVR (less than 20% deposit) borrowers who are owner-occupiers, and no more than 5% of residential mortgage lending to high-LVR (less than 30% deposit) borrowers who are investors.

These restrictions took effect in January. They are looser than the restrictions that preceded them.

Some economists had thought the RBNZ would further ease restrictions on Wednesday. However Orr said, at a media conference, the RBNZ didn't come "particularly close" to doing so.

Asked what the likelihood of the RBNZ changing tack and tightening restrictions was, Orr said: “It’s not sitting on our agenda, but why would you rule out optionality?”

The RBNZ explained in its report: “Indebtedness in the household sector is high, and some households face particularly large debt burdens.

Orr said the bank would monitor key indicators, like key asset price to earnings ratios.

“High debt leaves borrowers exposed to cash flow stress in the event that interest rates rise or incomes fall.

“Banks could experience significant losses if a large number of borrowers became stressed in an economic downturn, particularly if this were accompanied by a significant fall in house prices.

“Restrictions on high LVR mortgages are in place to limit the amount of high-risk lending and thereby reduce the vulnerability of banks from a severe downturn affecting the household sector

“The risk of large housing losses has reduced somewhat over the past three years.

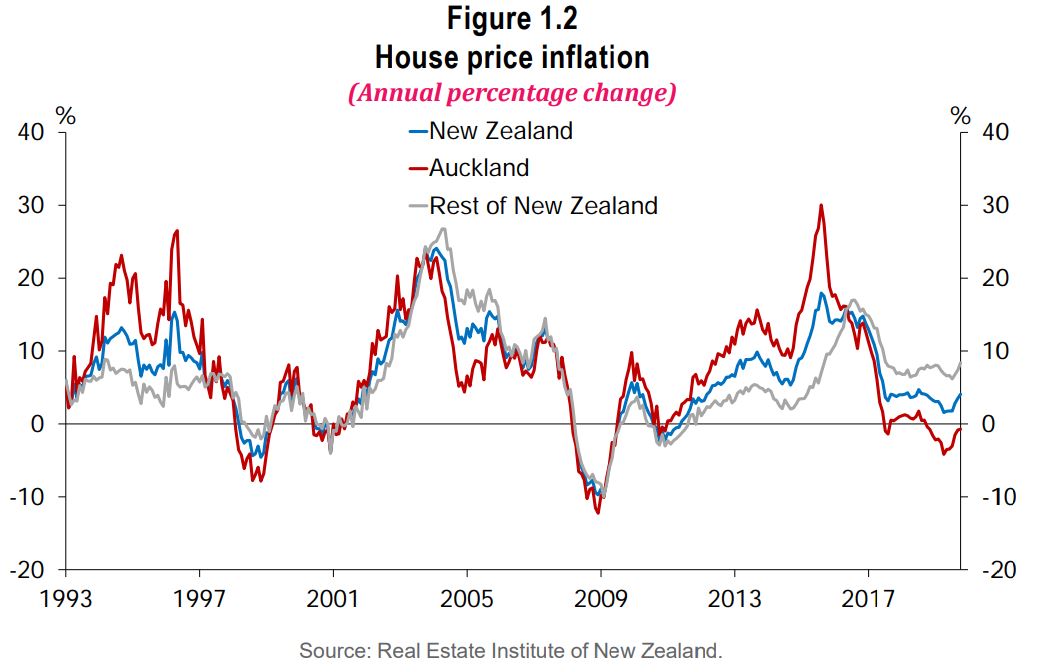

“House price inflation has slowed, particularly in Auckland, reducing the likelihood of a future sharp house price fall. And bank mortgage lending standards have tightened somewhat, reducing the volume of loans with a higher risk of defaulting in a downturn.

“As the risk has eased, there has been less need for LVR restrictions, allowing for a gradual easing in the policy.

“However, there are early signs that housing lending risk may be increasing again…

“There are also early signs that banks are easing mortgage lending standards in response to the low interest rate environment.

“Given the uncertainty around the future trend in housing lending risk, it would not be appropriate to ease LVR restrictions further at this point. We will continue to review LVR restrictions, and will adjust them in line with changes in the overall risk environment.”

Here's a press release from the RBNZ:

Financial system vulnerabilities remain elevated and more effort is required to ensure that the system remains resilient over the longer-term, Reserve Bank Governor Adrian Orr says in releasing the November Financial Stability Report.

International risks to the financial system have increased. Global growth has slowed amid continued uncertainty about the outlook for world trade. This has resulted in reductions in long-term interest rates to historic lows, including in New Zealand. While necessary to maintain near-term inflation and employment objectives, prolonged low interest rates can promote excess debt and investment risk-taking, and overheat asset prices, Mr Orr says.

Mr Orr noted that the Reserve Bank’s Loan-to-Value Ratio (LVR) restrictions have been successful in reducing the more excessive household mortgage lending, thereby improving the resilience of banks to a significant deterioration in economic conditions. But, there remains the risk that prolonged low interest rates could lead to a resurgence in higher-risk lending. As such, we have decided to leave the LVR restrictions at current levels at this point in time.

Mr Orr says the Reserve Bank is committed to bolstering the long-term resilience of the financial system. “Strong bank capital buffers are key to enabling banks to absorb losses and continue operating when faced with unexpected developments. The Reserve Bank has proposed increasing these buffers further with final decisions on the Capital Review proposals to be announced on 5 December.”

Deputy Governor Geoff Bascand says good governance and robust risk management processes within financial institutions are important to maintain long term resilience. Our recent reviews of banks and life insurers, and the number of recent breaches in key regulatory requirements, reinforces the need for financial institutions to improve their behaviour.

“We are engaging with industry to ensure that they strengthen their own assurance processes and controls. We have also reviewed our own supervisory strategy and will be taking a more intensive approach, which will involve greater scrutiny of institutions’ compliance,” Mr Bascand says.

“Some life insurers have low solvency buffers over minimum requirements. Recent falls in long-term interest rates are putting further pressure on solvency ratios for some of these insurers. Affected insurers are preparing plans to increase solvency ratios and are subject to enhanced supervisory engagement. This highlights the need for insurers to maintain strong buffers, and insurer solvency requirements will be reviewed alongside an upcoming review of the Insurance (Prudential Supervision) Act.”

124 Comments

Seems wise, given what's going on in the regions. No more stimulus needed there.

And capital controls in a week, seems debt is a big concern

Low interest rate in itself is an indicator of how bad the ecenomy is.

Last months or so has been a slight jump but will it continue - what has to be seen is, if it will stabilize at the new price rise or fall again as no fundamental change in ecenomy to boost the market - important that foreign money has stopped (If not totally atleast minimized) and FHB on NZ wages have limited resource.

"Low interest rate in itself is an indicator of how bad the ecenomy is."

Actually low inflation environment, economy not bad

Relative who is the viewer that is; when we met, your left hand is my right hand, 98% bad economic outlook - 2% is growth potential, petrol increased by 200%-We've reduced subsidy by manifold twice, When profit is to be made whilst peoples suffering then what constitute a problem for peoples, I received profit - it's not a problem as it's my business.. it's all relatives. Put the voting age to 16, more voices at the ballot - it will be like current Hong Kong admin govt & China - the recent voting results speak for itself ;-)

"It's all relatives" - how true!

Yes, although low inflation environments and weak economies are usually strongly correlated.

That's right. Loosening LVR restrictions could prop up household consumption in the short run but is not worth the longer term increase in financial risk.

Perhaps keeping FHBs at the forefront of the housing market would eventually force a change in the construction industry towards more development activity catering to the lower and middle end of the market instead of continuing to chug out premium assets for speculation.

Just a thought to make landlord readers spit out their all bran:

if Auckland has a shortage of good quality housing for sale at an affordable price and landlord investors are buying 30% of new build stuff, approx, in order to increase stock available, why not preclude landlords who own 3 properties or more already, from buying more? Then all that stock would be available to FHB. Of course, government would have to subsidise the $180-250k surplus of Auckland median cf rest of NZ by some sort of benefit. This would serve purpose of stopping rich accumulating endless supply of rented stuff for their retirement and also reduce prices by flooding market. Of course this will never even considered because it would upset white voters over 65 who tend to vote more than those under 40 with no assets.

Yes, if only we could have a good old fashioned dictator in place that would allow us to eat the rich. Life would be good then.

HeavyG, we do have a dictatorship.It’s called central banking, yet you probably support the imbalance they have dictated over many years.

Yes good idea, though like you say Mike it's unlikely to get the older vote. What might be a more feasible would be to introduce 'Buy To Let' mortgages for Landlords which have been around in the UK for quite some time. I must admit, I was quite surprised to find that NZ banks have no controls over Investors spending habits. For more info: https://moneyfacts.co.uk/mortgages/buy-to-let/

"why not preclude landlords who own 3 properties or more already, from buying more?"

Trusts and companies always make such rules as this difficult and costly to implement.

I'd be in favour, but it would be pretty easy to get around I suspect.

A married couple with 6 properties individually owned between them doesn’t need a degree of being clever to circumvent the proposed 3 house rule.

May we should tax any wealth greater than $3m at 100%? or increase minimum wage to $400 an hour so every one is rich?

Just because it is an appealing idea (and off course it is, free money will always be appealing) it does not mean it is a good idea.

They didn't drop the OCR for fears of stimulating house prices further. Leaving LVR restrictions as is is consistent with that stance.

It shows they are taking their financial stability mandate seriously.

Even though the guy's personality can be odd, he seems not to shy away from confronting areas of concern

they need to add DTI as well

they know of what has been going on in aussie that the banks can not be trusted

DTIs of less than six would cripple most home owners who bought in the last three years.

DTIs of over six are useless. They're a tool for a low-price environment, not a high one. Unless the real aim is dishing out yet another thrashing to millennials who couldn't put off buying any longer if they wanted a chance to do things like have families, etc, while the older generations who got us into this mess and profited from it can just cash out and live the life of Riley.

DTI of 3 would be about right I think.

Phase them in over 5 years. No DTI for refinancing existing mortgages. DTI of 6 for new lending. Reduce by 0.5 every year over the next 5 years. Tweak the numbers/timeframes as desired.

Yep. DTI is required. A staged phase in seems the sensible way to map it forward. Need a plan for home owners (not investors) those who have brought in the last three years, perhaps they can evacuate their kiwi save as well, or some otherwise form of low govt rate to ride out the next ten years.

I think you'll find most of them sunk their Kiwisaver into getting a stable roof over their heads to begin with. Which is then going to go backwards if DTIs are slammed in.

If you want to kneecap me financially then you better have gone after those who made a lot of money tax-free with rentals that never turned a profit but posted massive capital gains first.

Grandfathered DTIs might be a good idea for existing registered mortgage holders over a long period of time, but it should come with an obligation that Govt will actually follow through on RMA, population and supply reform issues like they have all been promising for the last decade but not delivering. As long as someone else picks up the tab eh?

Perhaps some spot auditing of approved loan applications is required. I was listening to one of the jolly swagman podcasts with John Hempton talking about the dodgy loan applications that mortgage brokers were putting in in Sydneys western suburbs, 10x DTI, no worries..

ETI, not DTI which is an accounting nonsense

Go yell that at the RBNZ and see how you get on.

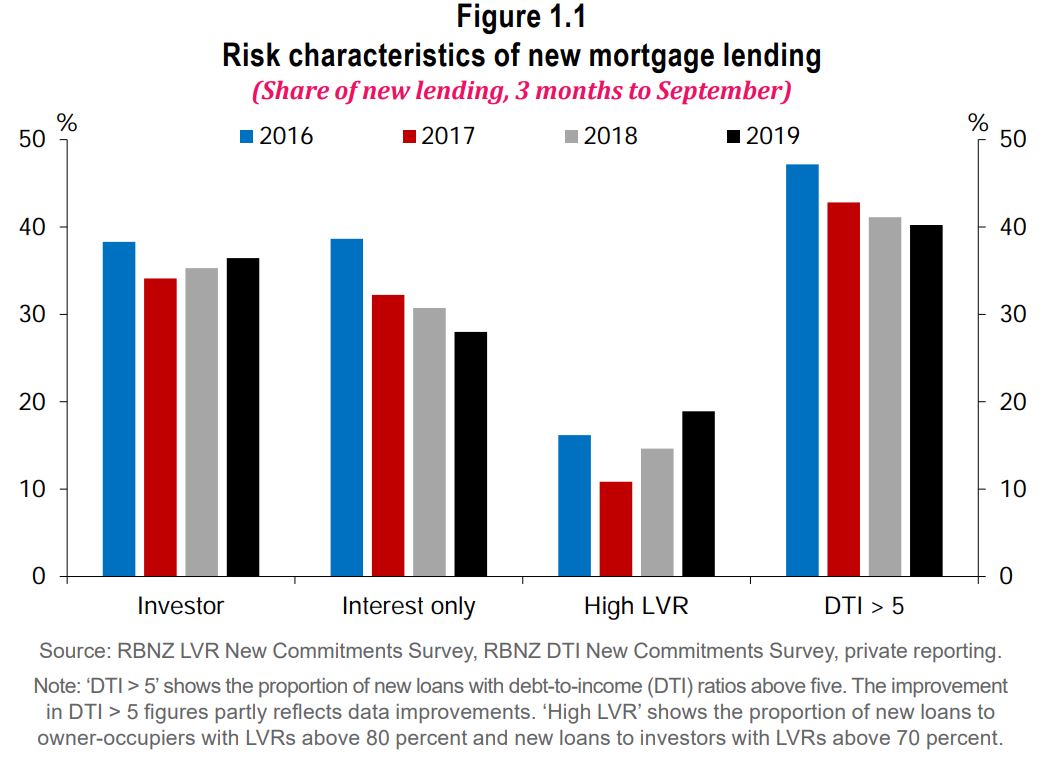

Prior to the introduction of LVR restrictions in 2013, banks’ lending

standards appeared lax on several metrics. Since 2013, banks’ lending

standards have tightened in general, and we have seen continued

improvement in some metrics, with less new mortgage lending on

interest-only terms and to borrowers with debt-to-income (DTI) ratios

over 5 (figure 2.6). However, LVR restrictions have been eased twice

in the past two years, and banks have responded by increasing high-LVR

lending. Furthermore, while high-DTI lending overall has reduced, the

proportion of loans at both high-LVR and high-DTI has increased from

around 2.6 percent to 3.5 percent over the past year.

https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Financi…

ETI can be easily gamed.

Look at the people currently gaming tightened bank loan application criteria in order to get mortgages. For example, I have heard stories of people cancelling credit cards, reducing credit card limits, cutting lifestyle costs for 6 months prior to loan application, to meet debt servicing calculations.

sensible decision

Well done, wise move RBNZ. You need to leave some tools still available to you, and you're right there is no point in letting our younger generations to get so indebted that the won't have a cat in hell's chance of ever paying it off. That path only leads to financial crisis.

Agree, very wise.

I was expecting them to change it, because historical evidence shows a very strong bias towards boosting the housing market by policy makers and government.

Yes though, If the RBNZ and our Government really want to slow down Landlord spending sprees they could introduce 'Buy To Let' mortgages with longer fixed rate deals to help prevent house flipping. Most UK mortgages are at 2, 3 & 5 year fix rates. Also the UK banks have tighter controls over people breaking their mortgage deals, where you would need to pay back 3% of the overall mortgage value (plus fees) if you wanted to redeem your mortgage early.

Cat's well out of the bag on that one I'm afraid.

Well done, RBNZ.

Where is risk profile in the graph for FHB?

We know what happens next, don't we !?

Banks will start slashing their mortgage rates to keep the debt flowing to their books. And...

they'll want 'the good stuff' - old and new, so poaching of each other's customers is going to be front and centre....

TSB Price matching would suggest you are on the money with your comment

We can only hope.

BW. Westpac will probably at the top of the list offering great mortgage deals.... they will need the income to pay the “bank busting” fine over in Australia.

I remember when LVRs were introduced they were meant to be temporary! Can't see them going away in my lifetime!!

Thats probably a good thing, they are an economic safety feature, a bit like ABS brakes, seatbelts and airbags in cars, you have to ignore the idiots that object, and make them compulsory.

It's definitely a good thing.

Only thing better would be permanent DTIs.

yes eidikos - and a good thing too!

They provide a good tool to ensure that we don't again see the significant increases over a sustained period as occurred especially in Auckland from 2012 to 2017 with consequences for FHB and associated risks.

We can agree!

I trust that the comment "reducing the likelihood of a future sharp house price fall" in Auckland is noted.

I trust the adverb "sharp" is noted.

Yes, the "bubble burst" brigade have either become very silent or left the party, but still the "slow leak" advocates about.

As I have posted previously, while factors especially including high levels of immigration, housing shortages and low mortgage rates persist, then Auckland prices will remain firm and some small degree of upside could be more likely.

FHB - buying for long term, and not as an investment, short to medium term movement is irrelevant so they have little to fear. However, affordability might not be any better than currently.

What is driving your bias p8? Do you own more than one property?

My property ownership is not relevant - it is just over quite a period I have seen wild unsubstantiated comments.

Just making sure you're conscious of any confirmation bias that could be present in arguments.

I have a very different view on that comment by the RBNZ.

They clearly see a risk of a sharp fall in prices, which would be heightened if the market took off again and prices rose.

Yet, prices are already extremely high by all measures, which is suggestive of there already being risk of a crash.

Property bulls don't seem to understand that inflating a bubble even further increases the risk of a crash.

Absolutely Fritz. FHB, however interested or motivated they may be to move into their own house in Auckland should also be able to afford million plus house (Question is even if FHB want to but Can They Afford It?). Why does everyone forgets affordiability.

From here on, even if OCR is dropped further - chances on interest rate going down much is limited.

RBNZ understand - should relize that FHB under pressure may take more debt and if the interest rate changes will be worst hit so a soft landing is better than crash.

Next week Capial Control is very important to protect borrowers as well as depositor/investor to avoid future catastrophe (Which at some stage is inevitable)

Nymad, I know you like your fancy words, you say "I trust the adverb "sharp" is noted." "sharp" is the adjective, not the adverb, "sharply" would be the adverb when added to a verb for example, i.e "it fell sharply"

After the interest rate cut, DGM hyperbole fell sharply .....

"Sharp Falls' in any asset are actually easier to deal with. They may be more painful for the holders, but a slow squeeze over an extended time stops current owners from liquidating ( that the idea?). They hold on, and hold on, and hold on convinced that "if I sell now, it might be the bottom. Things must go up from here?" and it rarely is.

Much better to get a big, quick fall done and dusted, then new calculations can be made, and those that want to take over assets from those who no longer want them, can and do.

More' at risk lending. We built our society around the exponential growth of debt. We are fools.

(Wrong spot for a response!)

Great. Supporting an further increase debt speculation seems unwise. Would be akin to tipping fuel on the fire.

Unless you are aiming for to big to fail?

True. If I was a bank that's exactly what i would be pushing for. Max bonuses on debt with abdication (govt bail out) of risk via size and potential impact on economy. All reward and no risk.

The issue is that most of the bank CEO's of NZ banks who have benefited financially from performance bonuses have now left the scene. They have taken their bonuses and left. Now what do they see coming (just like why did John Key resign being PM unexpectedly)? Now there is a new generation of bank CEO's in NZ to potentially clean up any mess.

Fuel has already been tipped. Notice the spike on the graph which correlates very well to the sudden dropping of the OCR.

Capital control next week will be good.

Have to control debt to avoid future burst.

From a financial stability perspective, this move is 100% reasonable. Thus the right move from the RBNZ. the higher the LVR the more secure the banking sector.

However, while controlling borrowing ability of buyers does affect prices, it does not fundamentally change the power imbalance between a rich investor and a middle class first home buyer competing for properties. As long as NZ economy is unable to offer any other investment opportunities that outperform investment in properties, investors will grab as many houses as they can.

Crazy interest in property is a symptom of an economy who has nothing else to offer. If this does not change, nothing else really matters. Money will go where it can get the best return. Even foreign money. Even borrowed money.

"Crazy interest in property is a symptom of an economy who has nothing else to offer"

Well put.

And changing that is up to Adrian because professional politicians aren't about to do much.

How? The RBNZ HAS to make further residential property speculation such negative choice that those with investment 'cash' WILL find another outlet for their money.

Without real, viable options, the money will leave NZ, it will not go to non-existing NZ investments. With real, viable options a decent portion of the money will go there instead of property (thus making punitive actions unwarranted). RBNZ actions are just pain killers at best, do nothing to improve the condition, potentially masking the real issue until things become too dire.

And I am not blaming the RBNZ. This is not a problem that RBNZ can cure. It is a problem that only New Zealand as a nation can solve.

You could be right - initially.

Funds could flow out of the country at NZ$1=US$64 cents but at 34 cents what will happen?

That money could come back in, and more, and maybe the exchange rate will settle at 54 cents.

Who knows.

But that ...is how it supposed to work! ( including those wise enough to see it coming, and that 'sell up' in (pick a suburb) beforehand?)

No investment opportunities locally? Ship the cash out

A good exchange rate and the possibility of 'doing something' with the money ( something ALWAYS turns up) then it comes back in.

The trick is to stop investment in non-productive enterprise and encourage it in the opposite.

At 34 cents it's far more economic to make movies here; set up internet companies and even make electric cars ( all just suggestions!) and....export the product.

Will it be painless? Absolutely not. But that's the economic corner we have painted ourselves into - a corner of no other escape. That alternative is to paint ourselves even deeper in, and that would be worse.

100% agree with you.

Good decision. NZ does not need looser lending and house prices to rise any further at this time. It would be inviting instability and a further pumping of the bubble. They are trying to reinflate it in Australia after the air started to come out, because the Australian economy relies so much on it these days - so does NZ’s unfortunately.

.. both the Gnats ( do nothing ) and Labour ( do stupid ineffectual things .. and do them badly ) are happy to see house prices continue to rise ...

And as long as the flood of immigrants continued unabated ( the Gnats wanna keep wages low / Labour promises to cut , but fails to do so ) ... house prices will remain stretched , regardless of the Reverse Bank ...

We’ll see. It’s quite a building boom going on. Chances are we’ll still overshoot.

We desperately need to fix our migration system that heavily favours international students for both work and resident visa applications. The system is simply acting in the interest of our tertiary institutions, protecting their export revenue.

Under the current settings, most international students under the age of 40 with 'a job' paying median wage after gaining 'a postgraduate qualification' from any NZ institution is enough to secure permanency in NZ.

Prop up the education lobby. Under Helen and now COL was always going to be the case.

“However, there are early signs that housing lending risk may be increasing again…

“There are also early signs that banks are easing mortgage lending standards in response to the low interest rate environment".

Very telling on the quality of the banks' assessment of risks in lending and how they are able to fiddle with standards to boost business, focussing on short term gains, ignoring the long term risks.

Well done, Orr for once again doing the contrarian thingy.

Waiting for December 5, sir.

Yes he's quite the contrarian

Yeah doing the right thing and now looking at capital control to protect the system.

Definitely need to ensure financial stability in NZ as a priority. Anyone who has experienced or understands the financial and social costs involved when a financial system breaks down can see that financial instability can also lead to potentially extreme political outcomes in democracies.

Page 25 of Financial Stability Report

"Financial instability can be very costly for affected countries, in terms of lost economic growth, increased indebtedness, and higher unemployment, which ultimately translate into lasting impacts on social cohesion and wellbeing.

New Zealand’s banking sector was exposed indirectly to the GFC in the form of significant liquidity challenges, but did not experience the levels of credit losses that banks in many other countries faced. The system is now more robust to liquidity stresses than it was pre-GFC, but attention has now shifted to ensuring that the system is sufficiently resilient to reduce the probability of future financial crises."

As a comparison, look at what amount the US banks would be willing to lend on the same income and similar interest rate as the median household income in Auckland, plug in $95,000 in household income and adjust for 5.5% interest rate (comparable to NZ interest rates), and a 30 year mortgage.

https://www.bankrate.com/calculators/mortgages/how-much-money-can-i-bor…

1) $95,000 income

2) interest rate 5.5%

3) mortgage amount of $300,679 (a debt to income of 3.2x)

4) $2,217 monthly mortgage payment (annual amount of $26,604 - a debt service to income ratio of 28%)

While in NZ:

1) $95,000 income

2) interest rate of 5.2%

3) mortgage amount of $542,000 (a debt to income of 7.1x)

4) $2,977 monthly mortgage payment (annual amount of $35,724 - a debt service to income ratio of 37.6%)

https://www.asb.co.nz/home-loans-mortgages/calculator-borrowing.html

Since the early 1990's banks in NZ have changed two key lending constraints:

1) increased debt service to income ratios from 25% to 37.6%

2) increased the mortgage term from 20 years to 30 years.

Taking the current $95,000 median household income in Auckland what has happened to mortgage sizes?

A) Changing the debt service ratio increases mortgages by 50%

1) 25% of $95,000 is $23,750. At current floating interest rates of 5.2%, and a 20 year term, this would mean a maximum mortgage of $291,000 (a debt to income ratio of 3.1x)

2) 37.6% of $95,000 is $35,724. At current floating interest rates of 5.2%, and a 20 year term, this would mean a maximum mortgage of $437,746 (a debt to income of 4.6x) - so that is an increase of 50% from changing the debt service to income ratio

B) changing the mortgage term from 20 years to 30 years increases mortgages by 23%

1) 25% of $95,000 is $23,750. At current floating interest rates of 5.2%, and a 20 year term, this would mean a maximum mortgage of $291,000 (a debt to income ratio of 3.1x)

2) 25% of $95,000 is $23,750. At current floating interest rates of 5.2%, and a 30 year term, this would mean a maximum mortgage of $356,918 (a debt to income of 3.75x) - so an increase of 23%.

C) combining the multiplicative effects of increasing debt service to income ratios to 37.6% and extending mortgage terms to 30 years has resulted in an 86% increase in mortgage sizes

1) 25% of $95,000 is $23,750. At current floating interest rates of 5.2%, and a 20 year term, this would mean a maximum mortgage of $291,000 (a debt to income of 3.1x)

2) 37.6% of $95,000 is $35,724. At current floating interest rates of 5.2%, and a 30 year term, this would mean a maximum mortgage of $542,000 (a debt to income of 5.7x) - this is a 86% increase in mortgage sizes.

As a result, this is likely to have contributed to higher houses prices.

1) an 80% LVR on a mortgage of $291,000 (25% debt service to income, 20 year mortgage) would mean a house price of $363,778 (a house price to income of 3.8x)

2) an 80% LVR on a mortgage of $542,000 (37.6% debt service to income, 30 year mortgage) would mean a house price of $677,500 (a house price to income of 7.1x) - so an increase in house prices by 86%

3) Put another way, could house prices today be 46% lower if the lending terms by banks had remained the same as in the early 1990's as owner occupiers were constrained on mortgage amounts lent by banks?

Refer mortgage calculator and plug in $95,000 for household income which results in maximum mortgage amount of $542,000, monthly payments of $2,977 ($35,724 per annum or 37.6% of gross household income), and a 5.2% floating rate mortgage for 30 years. -

https://www.asb.co.nz/home-loans-mortgages/calculator-borrowing.html

What happens....banks and their owners make more money for longer, and the borrow has an increased debt servitude. In some ways a form of enslavement. But its all good if you can use a tenancy agreement to pass the risk onto someone else...

A tenancy agreement doesn't pass the risk, it's still your name on the mortgage.

A very good outline of how the system has tilted the playing field in favour of investors and banks, to the cost of FHBs.

Given that lending limits determine what the marginal buyer can pay, this summary shows why house prices are now at the level they are.

The gains of investors over the last 20 years is not due to their investing acumen, but rather by the coordinated decisions by the banks to lower their lending standards in their own interest.

This show the critical importance for central banks to provide permanent lending constraints (LVR and DTIs). At the moment, at DTI of no greater than 5 should be imposed as soon as possible to prevent more FHBs being lured into this precarious market.

In other words the banks also played a part as property spruikers/spoilers ?

V well done CN.

The precise point I would like to have made but was not able to do sums! Point is banks lending limit has a determinative impact on what a house can be bought for. Lower the limits and house prices would have to fall

Fact check! "1) increased debt service to income ratios from 25% to 37.6%

2) increased the mortgage term from 20 years to 30 years."

Those of us who have bought properties might well know better than this misinformation.

Feel free to refer page 4 of RBNZ research paper. "Credit Constraints & Housing Markets in NZ", by Andrew Coleman 2007.

The loans were subject to quite stringent conditions: for instance, in 1981 a leading bank noted that “principal and interest payments should not exceed 20% of the breadwinner’s annual gross earnings, or at most 25% where other commitments are of little consequence,” and that in making such calculations a 20 year table mortgage would be the standard contract.

Moreover, banks would not normally lend more than 75 percent of the value of the house. Following deregulation, banks started to relax some of these requirements. At the end of the decade revolving credit mortgages were introduced, so that customers could draw down additional funds if they wanted, and banks made finance available to people who did not have an established saving record with them. Nonetheless, at the start of the 1990s the banks retained fairly conservative conditions. The same bank noted that a mortgage applicant needed “sufficient discretionary income available to meet minimum monthly payments without recourse to overdraft”; that repayments must be “covered within 30 % of sole income or 25 % of joint income”, where the repayment amount was assessed with reference of table loan repayable over 20 years; and that the size of the loan should be less than 75 percent of the value of the property.

During the 1990s, most banks relaxed the terms and conditions of their loans in response to better information technology and a desire to increase the fraction of residential mortgages in their overall lending portfolios. If customers purchased mortgage indemnity insurance, they could borrow up to 95 percent of the value of a property, rather than the previous 75 percent, and mortgage-repayment-to-income ratios were progressively relaxed.

Moreover, by the end of the decade banks started to customise their requirements according to the demographic and income characteristics of their clients. For instance, couples without children on near average incomes could borrow until their repayment-to-income ratio was 33 percent, or slightly more if they had a large deposit. Couples with children had lower limits, but their maximum mortgage-repayment-to-income ratios still typically exceeded 25 percent unless their incomes were very low."

So that is not quite how you put it in the earlier comment.

Besides the number of mortgagee sales has fallen and is at a very low level. The worst time for mortgagee sales was during the 1980s. To me that means banks are making the right calls when the loan is provided. Oui oui?

Could mortgagee sales be at a low because borrowers could just re-mortgage under the new lower standards, and suck up the consequential capital gains over the same period? Mortgagee sales take a while to flow through because they are the last resort for borrowers and lenders. They usually hold the nonperforming loan for over a year, trying to find a solution. They are a lagging indicator of the state of the market.

Fact check! "2) increased the mortgage term from 20 years to 30 years.

A family member took out a mortgage in the mid 1990's. Their mortgage term was 20 years. Also it was a table mortgage.

I predict that the RBNZ is all too well aware of the externalities building internationally which when they land will do more to take the bubble down than anything the RB could muster itself. The last thing to do is repeat what Alan Bollard did in 2008...Brexit is going to be a big enough shock but I anticipate China executing a bloody crack down on pro democracy protestors in HK shortly and the international community will be forced to intervene and in the process send all markets into a tailspin. There will be no housebuilding overshoot due to these events.

There by already be overshoot. There are plenty of places to buy in Auckland for instance, they are just too expensive at the lower end, and it’s really expensive to build. That is not a recipe for plain sailing.

FHB market in Auckland? Roughly priced between 650k and 900k?

If we agree on that:

Residential sales in 2018, April to September: 3867.

In 2019 = 3660 (- 5.3%) Apartments 427 v 274 (- 36%)

If you think 2018 was aberrant because of front-running OBB, the 2017 comparison for same 6m is:

Residential only: 3480 and apartments 294.

Which puts 2019 ahead of 2017 by 5% and in apartments shows 2019 with 6.8% lower sales.

BUT bear in mind 2017 was atrocious for sales due to Chinese stamping on hosepipe in first 6m and also the election delaying investments.

If interest rate cuts were helping in last 6m....what is happening?

We keep being told, for ALL of NZ that FHB are borrowing more.

How many are new mortgages in Auckland however, we are not told.

Plainly Auckland is affordability problem centre so WHY cannot banks and RBNZ not give us figures for

1. Auckland v rest of NZ new lending at different price levels

2. Ditto for FHB.

I read somewhere that 8% of borrowers have 40% of mortgage debt. Can anyone enlighten me as to source for this?

Link to full Financial Stability Report

https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Financi…

Good to see more bank capital risk is clearly called out there. Kinda jumps the gun on the announcement next week. Interesting highlights that insurance companies have solvency risks as well.

I don't think there was ever any doubt that the RBNZ was going to want the banks to hold more capital, I think the question is how much more, and how soon?

The Reserve Bank Governor is not buying into the corrupted economists, who do nothing that encourage more business for their masters. He is certainly not the puppet his predecessors were. Clowns they were.

While low interest rate might have the effect of encouraging more lending and in turn facilitating higher prices being paid, the gains in value will only be temporary. Only the foolish will be leveraging themselves up in this market. Long term prices have to meet the market of the new entrant; and it would be the cheap labour we are importing presently.

Agreed. Bubble theory is always predicated on expecting the status quo to continue on to infinity.

"Bubble theory is always predicated on expecting the status quo to continue on to infinity."

Lessons from the US GFC 2008 / 2009

Cause of the housing and credit bubble in US

From the May 2010 FCIC interview with Warren Buffett, a reknowned investor and Chairman and CEO of Berkshire Hathaway

MR. BONDI: As I mentioned at the outset, we’re investigating the causes of the financial crisis. And I would like to get your opinion as to whether credit ratings and their apparent failure to predict accurately credit quality of structured finance products, like residential mortgage-backed securities and collateralized debt obligations, did that failure, or apparent failure, cause or contribute to the financial crisis?

MR. BUFFETT: It didn’t cause it, but there were a vast number of things that contributed to it. The basic cause, you know, embedded in psychology –- partly in psychology and partly in reality in a growing and finally pervasive belief that house prices couldn’t go down and everyone succumbed –- virtually everybody succumbed to that. But that’s –- the only way you get a bubble is when basically a very high percentage of the population buys into some originally sound premise and –- it’s quite interesting how that develops –- originally sound premise that becomes distorted as time passes and people forget the original sound premise and start focusing solely on the price action.

So every -– the media, investors, the mortgage bankers, the American public, me, my neighbor, rating agencies, Congress –- you name it -– people overwhelmingly came to believe that house prices could not fall significantly. And since it was biggest asset class in the country and it was the easiest class to borrow against, it created probably the biggest bubble in our history.

Of course Mr Buffett knows nothing compared to some of our resident Property Spruikers.

We are diffrunt! How many properties does Mr Buffet have in NZ? None? See, he doesn't know what he's talking about!

NZ is special, our economy is special, the laws of mathematics and psychology do not apply here!

oh yeah, I forgot

:'D

That wordings, 'not even close' an ample warning as what currently boiling up in place.. unproductive, speculative... greed, some sort of regulations & sanity need to be maintained. Wild west approach (leave it to the market to sort things out, won't work) - like anything else, the regulatory body is there to oversee things from running wild.

Debt to Incomes is a silly way of working out how much someone can afford to borrow.

For property investors it just is not sensible as there is income coming in from every property whereas the owner occupiers are not getting income from their property, they are relying on income from a different source.

The only sensible way is looking at how much a family would have after their expenses with a bit of fat in the system as well.

Our cashflow and surplus from rentals allows us to live very comfortably as well as afford to buy additional rentals.

Whereas a working couple is reliant on both having employment and therefore a property investor that is running a professional cashflow positive business is a far safer risk to the Bank than the owner occupiers

Debt to income is a useful metric.. it helps show how exposed you are to interest rate changes

No it does not. Say you have a DTI of 5, interest rates double, what's your DTI now? Yep still 5!

DTI is an accounting nonsense because it compares a measure of financial position "D" (taken on one precise day of the year) with a measure of cashflow "I" (typically taken over 12 months).

ETI is the correct measure and the one that properly complements LVR (or to be more consistent DTV)

Yeah, thats not what I said, you may want to engage brain next time.

Who is more exposed to a change in interest rates, the guy with a DTI of 6 or the guy with a DTI of 3?

For some reason the RBNZ finds it a useful metric, but Yvil doesn't. I think i'll go along with the RBNZ.

DTI...Debt that may remain static/ go up whereas Income may vanish/ decline, making it riskier. Of course, income can also go up, but risk assessment/stress test doesn't usually include that possibility

ETI....Expenses tend to go up while there is no guarantee of income staying the same or going up. Again, risk assessment/ stress test has to look at that adverse possibility.

And what is ETI?

Expenses.

Earnings to income?

Expenses to income?

Earnings to interest?

Expenses to interest?

Other?

Seems some confusion over Yvil's use of acronym "ETI".

Only one of those makes sense.

Of course, Expenses to Income. Accounting 101

If there was any consistency with LVR, DTI should be renamed LIR

I think the convention abroad is often LTV and LTI

So many acronyms. I'm guessing:

a) LTV is loan to value (equivalent to LVR)

b) LTI is loan to income (equivalent to debt to income)

What is LIR? Never heard of it.

How do you calculate it?

(Edit: just got you. You mean LTIR - "loan to income ratio" similar to DTI "debt to income")

Please remember, readers on here come from diverse backgrounds and experiences. Some readers here are financial accountants, some are tax accountants, some are management accountants, most are non accountants. Some are economists, some are commercial bankers, some are investment bankers, most are non bankers. The definition of the word "income" is different for all those groups just mentioned.

Use of specific or infrequently used acronyms is likely to mean you are more likely to be misunderstood. Other readers cannot read your mind (I know I can't, so maybe it's just me). Please use the entire phrase, at least once, so readers can try to understand what you are talking about. Capiche? (In case you don't understand, capiche means "do you understand?" in Italian)

Just to clarify with you,

A) are you applying the above formula to households or to businesses or both?

B) In the context of the formula above and applying it to households:

1) does expenses include :

a) interest payments only or both P&I payments (this is cashflow that is paid out by households), or neither

b) does it include depreciation, or only actual cash paid for repairs and maintenance?

c) does it include capital expenditure for capital improvements for an owner occupiers's home?

d) does it include capital expenditure for capital improvements for a property investor's investment property?

So not sure if you are using:

a) cashflow accounting, or accrual accounting,

b) tax accounting or management accounting or financial accounting for credit risk purposes.

2) income is defined as

a) gross household income or

b) gross household income after taxes but before expenses, or

c) gross household income after expenses and before taxes?

d) Other.

Please clarify.

"Debt to Incomes is a silly way of working out how much someone can afford to borrow."

It's not designed to work out how much someone can afford to borrow by the banks in their credit assessment.

It is used by the RBNZ to assess risk to the overall financial stability of the banking system.

The RBNZ has exhibited a glimmer of self awareness.

Wait and see what they do with capital control next week. Should really tighten it in current environment.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.