This article was first published in our email for paid subscribers this morning. See here for more details and to subscribe.

By Gareth Vaughan

The head of retail banking at ANZ New Zealand, the country's biggest bank, says there's a "bit of pressure" on fixed-term mortgage interest rates at the moment following recent rises in wholesale rates, hinting that rather than another round of cuts by the banks as seen in April-May, the next major moves may be up.

Kerri Thompson, managing director for retail banking at ANZ NZ which includes both the ANZ and National banks, told interest.co.nz in a Double Shot Interview the fixed-term mortgage rate cuts of April-May were less a mortgage war among the banks in a low growth environment as touted in the media, and more moves by banks to cut rates following drops in wholesale interest rates.

"So it made sense for us to change our fixed rates," Thompson said.

"(But) we're seeing wholesale rates move in a different way at the moment. And wholesale rates are so impacted by the global economy, whether it's Europe or the US, or what's going on in China. So it really depends on that as to whether our interest rates will go up and down. There's certainly a bit of pressure on fixed rates at the moment so we'll see what happens in those markets. But you need a crystal ball to work out exactly what's going to happen next."

Asked, (yesterday before Kiwibank unveiled a fresh six month "special offer" this morning), whether the next major moves could be up rather than down Thompson agreed that potentially they could be.

Swap rates have been on the rise over the past month. The one-year swap rate, for example, was at 2.73% yesterday, which is up 38 basis points since June 6. The two-year swap rate was at 2.85%, up 43 basis points since June 6, and the five-year was at 3.34%, up 38 basis points. (Also see the swap rates chart at the bottom of this story). Nonetheless, the most recent mortgage rate move by a big bank was ASB cutting its advertised five-year rate by 51 basis points to 5.99% this week.

More customers choosing to fix than float

Meanwhile, Thompson said fixed-term rates are back in vogue with customers, confirming monthly data out from the Reserve Bank this week showing the first drop in the industry wide value of floating mortgages since last August.

"We're seeing that 60% of the new mortgages are being fixed whereas a year ago it was the other way, 60% were floating so there has been a change," said Thompson.

"And you can understand people are saying 'we're at a very low interest rate at the moment and what is going to happen in the future?' We're (also) seeing many customers fix part of the loan and float part of the loan which is a sensible option."

With fixed-term rates, one-year was currently the most popular timeframe followed by two-year.

Market share growth

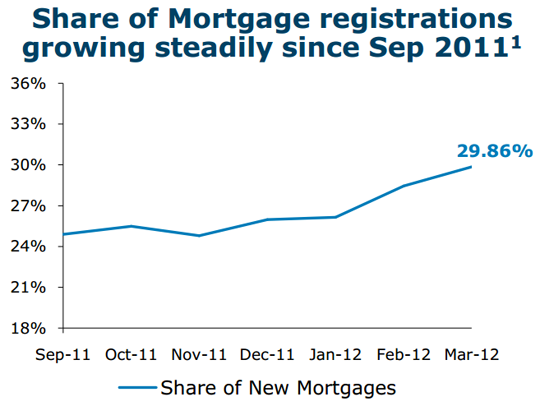

ANZ NZ has been growing its share of the residential mortgage market, with this up to about 31.70% as of March 31 from about 31.03% a year earlier, based on data from the banks' general disclosure statements. Its share of mortgage registrations has also been rising, something the bank pointed out in its half-year financial results via the chart below based on Terralink data.

Thompson, who took the retail reigns in March 2010, said there has been a lot of focus on mortgage lending.

"We've increased the training in our front line, we've changed some of our processes, we've made it easier for our bankers, easier for our customers. But we're still focussed on making sure that we are making good quality credit decisions. So that hasn't changed at all," said Thompson, who has previously worked for ASB's parent Commonwealth Bank of Australia and General Electric.

"We see the buying of a home as something that's really important to Kiwis and we put more Kiwis into homes than any other bank in the country and we're proud of that. We want to continue to do that."

"We've put on more mobile mortgage managers that are there when customers want them."

'We certainly like to make sure that we're giving our customers what they need to stay with us and to come to us'

With much anecdotal evidence of banks' offering discounts of up to 50 or 60 basis points on advertised mortgage rates, throwing in thousands of dollars of cash to customers to cover the likes of legal and valuation costs, and even being prepared to pay - or contribute towards - break fees to help win business from customers on fixed-term loans with rival banks, Thompson said ANZ does what it calls "A to Z reviews" with borrowers whereby bankers talk to customers about their mortgage, insurance, KiwiSaver and other banking business.

"In doing that we develop that relationship where we can have a relationship with them if they are thinking about moving and we can encourage them about what's the total package that's best for them. So I think it's more about a long-term relationship than it is about stealing a particular product off each other in the banking market," said Thompson.

Specifically on reductions to advertised rates she said: "We certainly like to make sure that we're giving our customers what they need to stay with us and to come to us so we like to be able to understand what we're competing against. But at the same time we've also got to be careful about profitability and our long-term sustainability, which is terribly important. So we carefully and rationally make those decisions about whether we do discount off what the carded rate is."

Thompson acknowledged that competition was a factor in the ANZ and National banks continuing their NZ$1,000 cash back offer, which launched on October 26 last year, for longer than they may otherwise have done. To be eligible for this customers must take out new home lending of at least NZ$100,000, have their main transactional account with ANZ NZ and their salary or wages credited to this account, and have a credit card or insurance product with the bank.

"We had a lot of feedback from customers that when you're buying a home it's a tough time and it's also an exciting time. It's nice to put new curtains in or a new piece of furniture at the same time as you're going into a new home. So people have really appreciated the NZ$1,000 cash back so we've continued that perhaps longer than we would have normally and partly because of the competition in the market," said Thompson.

Home loans at 80-85% LVRs 'not as big a risk' as over 90%

Competing in a market that's growing only an a 1.5% annualised rate compared with double digit growth between 2003 and 2008, Thompson said ANZ encourages borrowers to have a deposit for a house of at least 10%. Earlier this year ANZ NZ CEO David Hisco hit out at rivals ASB, BNZ and Westpac over loan to valuation ratios (LVRs) above 90% on home loans saying this wasn't necessarily the right thing for customers or the best use of funds by a bank.

"We encourage people to have at least a 10% deposit," said Thompson. "An 80-85% (LVR) is not so big a risk, but once you get over 90% we get a little bit concerned and we get a lot more careful in that area."

"A couple of percent of the loans that we've written in recent times have been over 90% so we're very selective. And what we look for is what's their long-term employment sustainability, have the customers got good savings history, are they likely to be able to manage through a crisis that might happen. So it is a wholistic look at the customer's situation. In those situations we're pretty keen to make sure they've got insurance."

No chart with that title exists.

18 Comments

Accdording to Westpac

"NZ 2yr swap yield: Opening today 1bp lower at 2.80%. We expect a move towards 2.35%

within the next month."

That doesnt suggest upward pressure on retail rates...unless of course one of them has got it wrong.

He wouldn't be trying to scare borrowers into fixing their mortgages early and become locked in customers would he?

Yes one of them has it wrong and we will see... BUT impressive really, this woman (edited from guy/bch) Thompson, Head of Retail lending at ANZ/National now has the power to make a statement like this and analyse the impact on his customers. How many over the next week, two weeks, month etc, switch some of their mortgage to fixed. We who keep an eye on mortgages see some potential for rates too rise sooner rather than next year (recent media). What a great anlytical tool, this scaremongering, testing his customers, getting his analysts to look at the reaction and make extrapolations of different scenarios, information after all is king. And when you are dealing with hundreds of millions of dollars why wouldn't 0.1 % be of interest, if you could milk it a little!! Without breaking any rules, without being exposed, without any real repercussions... thats got to be worth a $50,000 bonus at xmas doesn't it!!!

Thank God for Kiwibank or maybe BNZ or maybe ASB... because if I catch these naughty little corporate execs playing round with my National bank mortgage I will have no qualms about angrily severing my allegiance to a bank that I like but .... let's see. I hope some of you out there keep watch over the Swap rates in the near future.

I think Thompson is a "her" !!!!!!!!!

Batooh - that's quite a conspiratorial view you have.

Why would a bank want to lock customers into fixed mortgages right now when margins are squeezed and much better margins are available on floating mortgages?

The 1 year swap has moved about 0.35% up since these 1 year fixed rates were set. I'm surprised these haven't been lifted yet. Ignore the Kiwibank and ASB moves - these are just marketing gimmics.

Isn't it smart to lock some (a portion - maybe small) into fixed now at these low rates? I'd leave the rest on floating and perhaps lock in some more if fixed rates move lower again?

Have you fixed or are you floating and waiting for rates to fall further?

We traded off between ANZ and Kiwibank and Kiwibank won. Floating at 5.25% (discounted variable rate 0.4) for 2 years, no Low Equity Fee on 85% borrowing and $1500 in cash. This website and the many folk like you have given us first home buyers the confidence to haggle hard with banks.

I don't pretend to be an expert but this "chat" from Westpac and ANZ is simply scaremongering.. as you put it. Perhaps rates will rise but in reality do these banks want to continue record mortgagee sales?

Interestingly, I'm surprised so many have locked into fixed rates and not negotiated lower floating rates... we'll consider fixing around Xmas time - that is, if Europe doesn't melt further into the mire!

Be careful dobryan, if europe blows up, credit markets will freeze, banks won't be able to get money at any price (certainly a ALOT higher if they can), they will have to try to fund totally locally over time - great news for investors, because it will mean deposits rates go higher, and then mortgage rates follow thereafter...... of interest, the RBNZ will probably slash the OCR to 1.00 - 1.50%, but wholesale floating rates won't go much lower (the spread between the OCR and floating bank bills will explode higher), as well as bank funding spreads, hence higher mortgage rates....that is what a credit crisis does. They are aleway great news for investors, bad news, or in some cases terminal, for floating rate borrowers

Thanks Grant A, I appreciate the concern. I'll be following events in the EU closely to minimise any risk to our mortgage although I feel somwhat reassured with who we're dealing with at KB.

Grant@

Yes you could be right but, the RBNZ is more likely than not to follow the ECB's recent actions. It will offer to accept any collateral against cash at the low rates you have quoted or lower.

In the ECB's own words: "It's very useful [for the banks] to lend to the real economy; as the banks generate collateral that they can now use for funding themselves"

Get that old hp financed law mower out and wander on down to the local ANZ/National branch to get it refinanced in anticipation.

"We encourage people to have at least a 10% deposit," said Thompson. "An 80-85% (LVR) is not so big a risk, but once you get over 90% we get a little bit concerned and we get a lot more careful in that area."

15 to 20 percent down is down right speculation. Tthere is no other term to describe such an endeavour other than gambling. On this basis it is always best to engage in such an undertaking with others people's money. and a negotiated profit retainer. I guess that's the deal Ms Thompson enjoys. The other side is serfdom.

People are trying to buy a place to live. Not trade CDO indices. It should not be so hard. There are more important matters to attend to.

Not quite sure what you're getting at here Stephen. How can new market entrants get into their own home if banks don't lend to them with only small deposits?

Ted we are inevitably building a debt pyramid which is impossible to liquidate. Collectively the loss has to be taken and a realistic price levied against non-productive assets.

We can wait for another decent earthquake to force the reinsurers to abandon our domestic residences as an uninsurable asset class or we institute the necessary changes locally. The costs of housing ourselves dwarfs all our activities when all ancilliary servicing costs are accrued to the current exiorbitant capital values, relative to disposal incomes.

Compound interest growth requires the price of property values double at least, inside 20 years - there is little discernible prospect of average salaries rising enough to enable any deposit to be saved. - It is a proven fact that the majority of working US citizens have not enjoyed an inflation adjusted rise in income since 1973. I imagine it is little different in NZ.

well interest rate world wide going to zero and the bank says fix quicky. let me think about that. world leader ship i guess i feel so proud of NZ

Banks don't own the property: they have rights in the event the borrower can not met his / her side of the loan contract.

If they owned it then the Bank would have rights over the capital gain (when / if this happens).

The Bank was only entitled to what debt was outstanding agianst the security property.

There could still be a mortgage registered over the property but if their is no debt outstanding its a bit hard for the Bank to envoke any of its rights (and ownership is not one of them).

I just fixed in for one year @ 4.85%......pretty happy with that!

If the Banmks ownes the property I guess its enttitled to the capital gain on the property or funds some of the loss if equity is lost?

Think deeper and tell me how my Banks gets it share of my property (equity over 75%) when I sell it which as an owner it will be entitled to do????

Tell me when I do up my house with my savings I am using the Banks money?????

Yes there are a portion of people with very high debt / incomes too low to service but the way you go on you woulf think it is every house in the street.

Yes untill you are mortgage free the Bank has certian rights on the basis you are in default of your loan. Pay your mortgage and you never hear from the Bank.

To use your words "the facts are" you own your property, you are on the title, you can paint it, plant a new tree etc without consent of the Bank.

Stay floating ... still plenty of downside in all economies & ours ...

Are 11% floating rates just around the corner? Probably not, unless you can envisage total freeze-up of the property market.

A person who has experience will always make the best of decision,as he Boss day statuses know properly what is wrong or wright,yes I'm talking about the best boss is who done the best.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.