By Sharon Zollner*

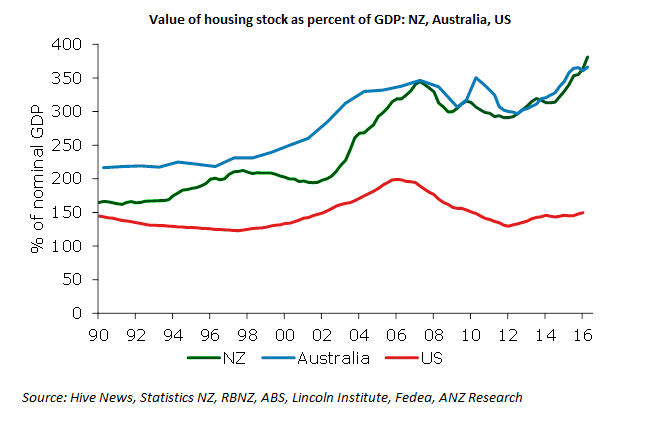

The Reserve Bank of New Zealand’s most recent M10 housing report shows the value of New Zealand’s housing stock (capturing changes in both the price and the number – and quality – of houses) increased in the June quarter to $NZ 959,850 million, or 381% of nominal GDP. Australia has followed a very similar trajectory.

An unusually high ratio does not in itself imply a nasty correction is imminent but it can certainly be a warning light, as it indicates either house prices are very elevated and/or there is housing oversupply.

Typically, oversupply leads to a sharper price correction when the market turns. Housing oversupply is certainly not an issue in New Zealand which has experienced very strong population growth. But there is broad agreement house price to income ratios are unsustainably high, particularly in Auckland.

In Australia, house prices have also risen strongly in the past 15 years or so, while oversupply is generally considered to be limited to pockets such as Melbourne apartments.

The US housing stock peaked at around 200% of nominal GDP before the global financial crisis (oversupply was a widespread problem and house prices then dropped 30%), while in Spain it was around 460% before the GFC – house prices subsequently dropped almost 40%.

Spain has a large number of holiday homes owned by foreigners, so would be expected to have a higher ratio on average over time, but oversupply was clearly a significant issue there too. The current UK ratio is around 240%.

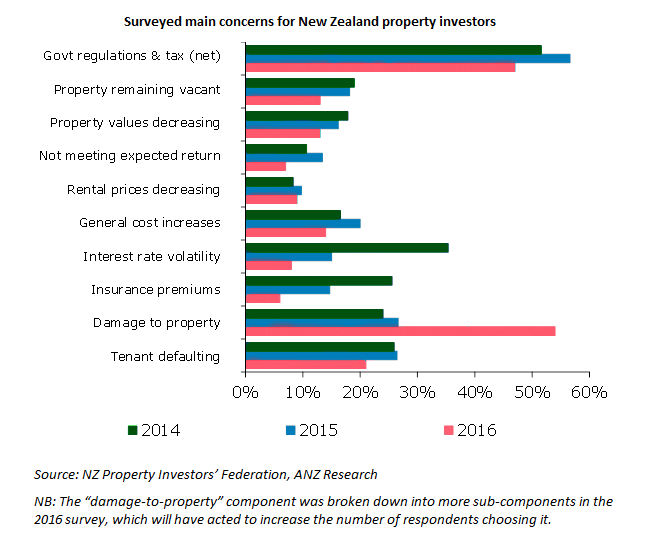

Feeling bulletproof

Despite the highly stretched state of housing affordability, the latest ANZ-Property Investors’ Federation Survey suggests not many investors are worried about cyclical risks to their property portfolio.

Concerns such as tenants not paying, difficulty finding tenants, rents falling, property prices falling, or not meeting expected returns are not rising. No wonder nearly 70% cent are intending to buy again.

The recent tightening of the restrictions on high loan-to-value-ratio (LVR) lending has certainly been noticed by investors, with nearly a third saying LVR restrictions had already impacted their investment strategy and many expressing concern that the restrictions would further cramp their style going forward.

But few seem to be extrapolating from impacts on their own purchase decisions to the broader market, with expected capital gains still very strong – and as shown in the chart only 15% of investors contemplating house price falls as a significant risk.

(Updated to insert missing 'not' in third paragraph from bottom)

------------------------------

*Sharon Zollner is an Associate Director & Senior Economist, ANZ NZ. This article first appeared on the ANZ BlueNotes website here, and is used with permission.

41 Comments

While I would expect a banker to be concerned over this type of analysis of housing, but for me the relevance is less of an issue than the cost of accommodation for the average Kiwi. this would cover both the purchase cost (and subsequent mortgage servicing) and rents. Both of which IMHO are totally out of whack and need to be addressed.

Banks are private institutions and they need to front up to the intrinsic risks in their own business practices. The fact the Governments have allowed laws to be created that provides banks with rights over those of their depositors is an unmitigated breach of trust with their constituencies.

"Banks are private institutions and they need to front up to the intrinsic risks in their own business practices."

Banks do on the most part. We have a very good example just recently of the non mandated restriction of lending to highly leveraged customers.

When they do not, it is because they are incentivised by you, the voter, not to. If there was never any illusion of taxpayer bailout, we would see a much different banking environment - costs, risk premiums, investment return, etc. You can't blame an institution for undertaking what it is incentivised to do under the direction of the people, though..

"The fact the Governments have allowed laws to be created that provides banks with rights over those of their depositors is an unmitigated breach of trust with their constituencies."

Ahh, that's called "investing"... No risk, no return.

I doubt you are saying the same thing about equities issuers?

Ahh, that's called "investing"... No risk, no return.

I doubt you are saying the same thing about equities issuers?

I dont think it is as simple or black and white as u imply.... eg.. transactional accounts. ie... has nothing to do with risk/return.

Central Banks exist because the Banking system is inherently unstable ... ( eg.. they borrow short and lend long.... they, generally, are highly leveraged ).

in this regard it is a public/private partnership..... SO.... it is not unrealistic/unreasonable to argue that deposit holders might be safeguarded , in some way, outside of the context of risk/reward.

And it is also understandable why prudential policy exists and , essentially, serves the greater good ie... stability of the Nation ..etc..

AND... I do realize the moral hazards of things like "deposit insurance"..... AND.... i also see how the OBR will have unintended consequences... ie. will amplify and accelerate Bank runs.... like a domino effect.

Transactional accounts don't really factor, do they? No one deposits a substantial amount of money in a transactional account unless it is interest bearing..

Agreed about Central Banks and regulation. There does need to be prudential monitoring to smooth cycle volatility. However, these institutions should be as close to independent as possible to mitigate the influence of public opinion.

It is an implied condition that we already have deposit insurance factored into our returns, isn't it?

What is the justification for introducing a significantly larger amount of moral hazard into the system for something that already exists?

I'd kinda consider M2 money as being parked in banks for reasons beyond risk/reward and investment..??

That is about $150 billion..

Point I'm making is that I don't think the argument is as simple as u imply. ...

Banks, hand in hand with Central Banks, ARE the payment system.. Thats' a very big reason why we park our money in Banks, in on call deposits ( which dont earn risk related returns. )... in my view.

We don't "park our money in banks", we put it at risk with the banks and hope that they return it.

There is risk and so there should be a return. This is most starkly explained as follows:

1848 in Foley vs. Hill and Others, Lord Cottenham in the House of Lords held that “

“Money, when paid into a bank, ceases altogether to be the money of the principal; it is by then the money of the banker, who is bound to return an equivalent by paying a similar sum to that deposited with him when he is asked for it. The money paid into a banker’s is money known by the principal to be placed there for the purpose of being under the control of the banker; it is then the banker’s money; he is known to deal with it as his own; he makes what profit of it he can, which profit he retains to himself, paying back only the principal, according to the custom of bankers in some places, or the principal and a small rate of interest, according to the custom of bankers in other places. The money placed in custody of a banker is, to all intents and purposes, the money of the banker, to do with it as he pleases; he is guilty of no breach of trust in employing it; he is not answerable to the principal if he puts it into jeopardy, if he engages in a hazardous speculation; he is not bound to keep it or deal with it as the property of his principal; but he is, of course, answerable for the amount, because he has contracted, having received that money, to repay to the principal, when demanded, a sum equivalent to that paid into his hands."

I agree that, ideally central banks should be as close to independent as possible to mitigate political whimsy.

However, particularly in the context of OBR applying, the RBNZ has a responsibilty to be very cautious and prudent, and quick to respond to misapplication of credit.

To date they have not yet done so adequately, they have been tardy in their application of LVR and DTI limits (compared to Korea, Singapore, Ireland, UK).

There is a question mark about continuing their independence if they continue to be too cautious in reducing easy credit.

True. Good points.

"Banks do on the most part. We have a very good example just recently of the non mandated restriction of lending to highly leveraged customers." they only did it under pressure from a public out cry over the overall risk to the economy from out of step house prices and a manipulated market, not through any internal monitoring of their business practices and the consequences. If they'd been doing that I would have expected action a lot earlier to cool and control the market.

" that's called "investing"... No risk, no return." Rubbish, money in a savings or cheque account is not an "investment", it is simply put there for safe keeping. It is a Bank and Government con job that that money is still "mine" when the law actually states it becomes the bank's, and I am simply an unsecured creditor!

Actually that is why I think the Governments are increasingly afraid of a bank collapse due to poor business practices, because when that happens and the banks STEAL the depositors funds to save themselves, the general populace will demand action from the pollies to stop this, and when they realise they can't because they wrote the law in favour of the banks, not the people, then there will likely be a few lynchings and the pollies will be first!

"they only did it under pressure from a public out cry over the overall risk to the economy from out of step house prices and a manipulated market"

I disagree.

Unless of course you refer to their shareholders when you state the "public'. If it was the case that the banks peddled to the every whim of the greater public, why don't we see them going out of their way to pass on all of the OCR reductions?

"Rubbish, money in a savings or cheque account is not an "investment", it is simply put there for safe keeping."

I can see that perspective. However, don't expect to realise any return on that deposit.

You can have it one way or the other. Return in the form of period interest or zero risk/fully guaranteed deposits.

"Governments are increasingly afraid of a bank collapse due to poor business practices"

The one thing the governments can do to all but ensure that business practices become poorer is guarantee funds in financial institutions. You can see this throughout financial history. It completely removes the incentive for a business to maintain long term sustainable internal practice.

This is exactly the reason why the RBNZ shuns such measures.

they don't pass on the OCR reductions because they don't have to, but under public pressure they bowed to putting some controls on. They either had to do that or have them imposed on them.

I agree there is little to no return on a simple deposit or savings account currently, that is why I keep them to a minimum. I invest in places other than a bank.

What you suggest that Governments can do is the conventional wisdom, and what has been done, but only protects the banks, not the depositors. It is a measure I disagree with. More effective would be the Government rewriting the law to make depositors funds the property of the depositor and not the bank, and the banks being liable to their depositor for how that money is managed.

Please.

The banks didn't have to impose voluntary restrictions, either. They knew the legislation was coming, so why implement prior to that if there was no economic benefit to them.

First you argue that Banks are unsympathetic thieves, but now they are very altruistic in light of public pressure?

Why do the depositors need protection?

They are already receiving it in the form of interest return...

Okay, rewrite the law to reflect that. You watch how fast people will react to the fact that they receive no interest return on their 'deposits'. The problem is that everyone wants to have their cake and eat it too..

We already get next to no interest and a whole raft of charges for using banks. You forget the original principle for why banks exist - putting money to work on behalf a multiple depositors and paying a return for that use (called interest). Currently the banks have become a power unto themselves and abuse that. Look at the GFC in 2008. Governments bailed out the banks who caused it, while many of their depositors lost their shirts. What would have been the outcome if the Governments had returned the depositors funds to them and left the banks to wallow in the mess of their own failure? Have the banks learnt anything, other than they are largely immune to consequences of their own behaviour?

Yes change the law, IMHO it will make banks more careful, less abusive, and less risky.

Concerns such as tenants not paying, difficulty finding tenants, rents falling, property prices falling, or not meeting expected returns are rising. No wonder nearly 70% cent are intending to buy again.

I'm having difficulty with this statement. Shouldn't "no wonder" be replaced with"yet" considering concerns are rising or shouldn't it be concerns are not rising? Or is 70% a notably low figure? In which case it should be only 70%....

Yes I wondered about that as well Zach but looking at the bar graph the trend is for all concerns to be declining - not rising - with the exception of the damage to property concern. That probably reflects a recent case of dogs pissing on the carpet that received huge publicity - I'm not making this up BTW.

False sense of security ? I guess as long as immigration holds up its not misplaced, as long as speculative capital gains aren't your sole driver, and you have a long game.

Oops, well spotted - sorry, the BlueNotes editors accidentally changed the meaning of what I wrote. Bernard H has now kindly changed the article above for me.

The fact that our housing stock is 'valued' at 381% of gdp shows what a joke property has become. Distortion to the extreme.

I think its more accurate to say it shows what a joke the economic system has become. Just a whole lot of distorted values and numbers which disguise the coming storm ... that our energy supply is about to be majorly disrupted. Your average Auckland property will then have as much value as those luxury downtown Aleppo villas.

Do you have an approximate date when this is going to happen?

Thats the big question - when you see things such as Caterpiller recording their 46th consecutive month in falling sales you wonder how it can continue to hold

http://www.mining.com/caterpillar-rally-hindered-by-fresh-drop-in-sales/

Desperate times calls for desperate measures - so its likely we will see

- government spendups

- helicopter money (disguised as training/education/grant schemes)

- some sort of sanctioned war to generate growth

But I cant see how they will get us much past 2020.

Apparently the Hills group gives it 6 years http://www.thehillsgroup.org/

This is worth a listen if you want more opinions

https://www.peakprosperity.com/podcast/102796/gail-tverberg-why-theres-…

Tax and Govt Regulations are the major concern though. Actually paying tax would be a good start, level the playing field, provide disincentive to the speculative end of the market, incentivise business investment, and potential economic growth.

Or sit on hands, at least they'll be warm.

Tax treatment has allowed housing to become a tradeable commodity same, so in simple terms they have gone from homes to investments first and foremost.

the problem you have is those that make the laws are into it up their eyeballs, just check the list of MP's assets.

all parties are into it so why would they change the laws to reduce their own advantages

In response to persistently low CPI inflation New Zealand’s Reserve Bank is widely expected to cut the official cash rate from its current level of 2.0 per cent in November, with ANZ predicting a further cut in February.

And the risks defined by Federal Reserve Vice Chairman Stanley Fischer are:

First, and most worrying, is the possibility that low long-term interest rates are a signal that the economy’s long-run growth prospects are dim. Later, I will go into more detail on the link between economic growth and interest rates. One theme that will emerge is that depressed long-term growth prospects put sustained downward pressure on interest rates. To the extent that low long-term interest rates tell us that the outlook for economic growth is poor, all of us should be very concerned, for–as we all know–economic growth lies at the heart of our nation’s, and the world’s, future prosperity Read more

One really ought to pay attention to this graphic debt to disposable income outrage and the potential financial instability it presages. Get aggregate incomes up and debt down or OBR will follow. Currently, the NZGS 10 year bond yield ~ 2.69% barely forecasts economic growth at the upper limit of the RBNZ's CPI target band - the "real" growth discount factor..

Get aggregate incomes up and debt down

yes.... And this can be quantified into a really valuable indicator..... in regards to being alert to financial crisis.

For me.... the precursor for a financial crisis... is private sector debt to GDP at over 160% AND the growth in that ratio by 16% + over prev 5 yrs...

http://debt-economics.org/index.php

If most of the growth in private sector debt is in real estate.... watch out... the financial crisis will spill into an economic crisis..

In my view, in regards to NZ... its not "if"... but "when"...... most of our growth in private sector debt has gone into speculation....whoops... I mean investment... :)

New mortgage lending month on month is about 2/3 residential 1/3 investors roughly. New lending is in decline with respect to total value but it's still $6.1b per month.

The 160% household debt to GDP ratio has become a significant risk to the financial system and long term growth. We don't have enough inflation to diminish the debt and insufficient productivity improvements to increase incomes. If this does lead to an Icelandic style collapse of our financial system I have no doubt it will destroy the Government at the time it occurs.

Better put the greens in power at the next election then :P

Or maybe vote National in and make them clean up their mess?

Sheesh, no worries mate. In Shenzen the number of years of median household income needed to buy a property of median value is now 41, according to The Wall Street Journal. So Auckland has room for lots more rope.

The shift of money from the stock market to property hasn't just pushed up the ratio. Now people are wondering how far away the property collapse is and if the Chinese Government will prop it up like they did with the stock market.

yes if you could pick the next fad they all pile into after it crashes you would be a multi

The article says:

"Concerns such as tenants not paying, difficulty finding tenants, rents falling, property prices falling, or not meeting expected returns are rising. No wonder nearly 70% cent are intending to buy again."

???

Oops, well spotted - sorry, the BlueNotes editors accidentally changed the meaning of what I wrote. Bernard H has now kindly changed the article above for me.

Re the headline :- NO IT WONT !

Oh, you mean mortgage approvals going down is a bad thing?

http://www.interest.co.nz/charts/credit/mortgage-approvals

Check out the Change in value tab....

In Australia, house prices have also risen strongly in the past 15 years or so, while oversupply is generally considered to be limited to pockets such as Melbourne apartments.

The Australian over supply "pockets" the article refers to are Melbourne, Perth, Adelaide and Brisbane/Gold Coast in 2018; Sydney by 2023. Combined these cities equate to 70% of the entire population of Australia.

Big pockets.

http://www.dailytelegraph.com.au/realestate/all-but-one-of-the-major-ca…

Bank deposits have never been more risky with this new era of 'bail ins' where now not only do shareholders and bond holders lose their money but depositors as well. Over 100 years of fractional reserve banking and the central banks globally bring this legistlation in now. The four big Aussie banks in NZ hold 4.5 trillion dollars of derivatives. How can people not see what will eventually happen. Ignorance is not a defence in law nor is it in financial markets. Don't say you haven't been warned.

As long as "investors" in residential property aren't using the family home for funding any correction should not be too bad, as it is looking more and more likely. A very wise man once told me"always pay your taxes and never borrow against your home except to buy it!!"

We all know nothing new in below

http://m.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11737…

Ask national government and will come out with denial, lie and manipulation.

interesting that RE knows the make up of population in the suburbs and how they became that way but our government does not. or do they know and are not wanting us the people to know what they have been doing by having the entry doors flung wide open

Most investors will have their family home mortgaged to provide positively geared rental property.

I know many on here will disagree, but you should being using the equity in your own home, otherwise you are not investing wisely.

I am not talking about buying overpriced negatively geared property!

If you are worried that one day you may lose your family home then clearly you are not confident in your investments.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.