ASB economists don't see much likelihood of a "significant" housing correction and expect "mild" price rises this year.

In their latest Economic Weekly publication, the ASB economists pose the question about a housing market correct and do point that complacency during a period in which global asset values are hovering around record highs, "can be dangerous".

"However, at the current juncture, most homeowners still look reasonably well placed to meet mortgage commitments," they say.

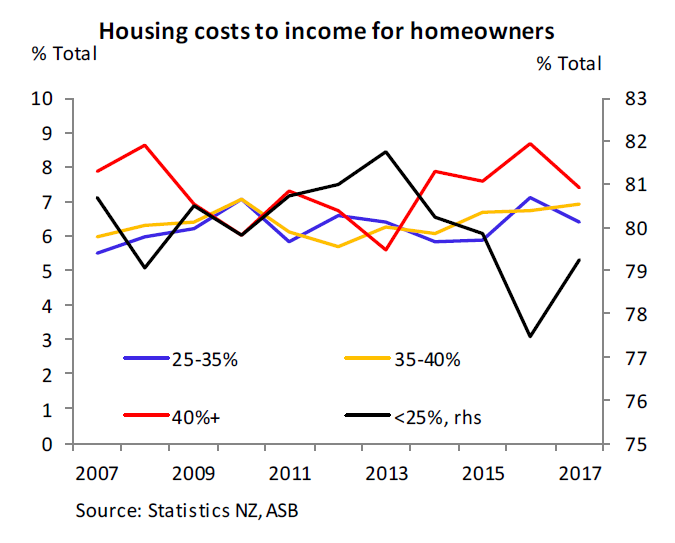

They say that according to Statistics New Zealand figures, close to four-fifths of all households with an outstanding mortgage spend less than one-quarter of their beforetax incomes on housing.

Only around 8% of households with an outstanding mortgage have housing costs exceed 40% of household incomes, and these households tend to have considerably higher than average incomes.

"If homeowners don’t have to sell during a housing downturn, they won’t.

"It would take a sizeable climb in mortgage interest rates coupled with a shock that significantly hit employment and local incomes to drive a significant fall in house prices.

"In the current goldilocks backdrop, it is hard to put an exact timeframe around when (or if) this might occur."

The economists do say, however, there is the risk that a "localised shock" could cause significant disruption.

"Mortgage debt holdings tend to be heavily concentrated, with RBNZ figures suggesting that around 8% of households hold about 40% of total housing debt," the economist say.

They are expecting a period of "mild rises" to house prices during 2018.

"Despite strong population growth, stretched affordability and policy changes, both here and abroad, are expected to prevent the housing market getting a fourth-wind since the GFC."

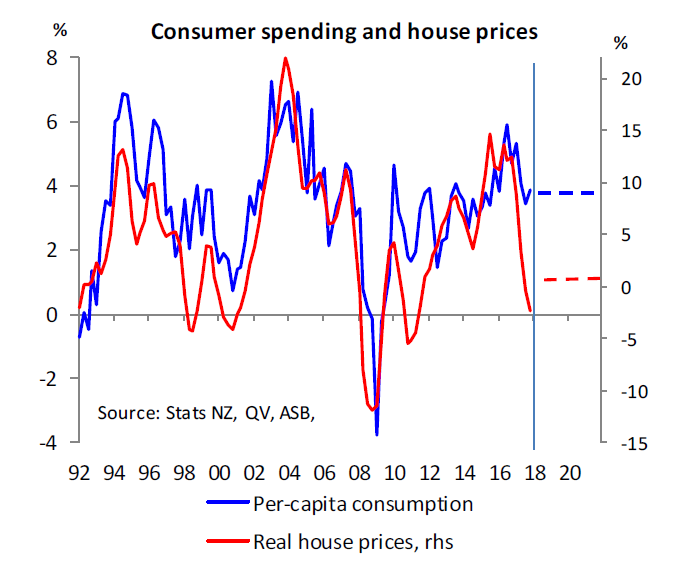

Consumer spending volume growth, however, is expected to advance "at a solid clip", supported by increasing labour incomes, the historically high terms of trade, still-low interest rates and a solid outlook for residential building.

The economists say much of the strong run-up in consumer spending volumes looks to be from consumers purchasing relatively more items experiencing relative price falls (e.g. consumer durables), with nominal consumption spending as a portion of nominal GDP around historical norms.

They say that one of the puzzles of late had been why consumer spending had been so mild despite the tightening labour market, sizeable increases in housing equity (which historically is closely correlated to consumer spending), still–reasonable consumer sentiment and strengthening residential investment.

It was thought that the global financial crisis (GFC) had elicited more caution from asset-rich consumers, wary of another downturn.

Unlike the run-up to the GFC, the household sector in aggregate had not used the rising equity of their dwelling as an ATM.

"However, recent revisions have helped solve this puzzle. Upward revisions to consumer spending (and overall economic activity) have helped to reassert the historically close linkage between house prices and consumer spending."

There are, nonetheless, the economist say, good reasons to expect the two to diverge over the next year to two.

132 Comments

If equity is no longer used as ATM en-mass, as was pre GFC, then how is it then so many have used their new found equity to speculate on additional houses?

WARNING! - ASB are suggesting this time it's different than pre GFC ;-)

As 8% of households hold about 40% of total housing debt and of course there is dairy, there is obvious risk lending standards will only tighten if banks are hit with defaults. House prices have to keep (mildly rising) to preserve equity and contain the debt mountain of the 8%.

As the saying goes, it's too big to fail. Is this why many feel so confident to leverage so much? There are many examples where authorities have lost the battle on this front.

The next trigger will reveal all.

You will be right eventually if you say it long enough rp

Next two years are looking up not down as you'd hoped sorry

IMF hails ‘broadest’ upsurge in global growth since 2010

https://www.google.co.nz/amp/s/amp.ft.com/content/d900ef2e-ff74-11e7-96…

That should hasten further destruction of the natural world and get the sixth great extinction moving along a bit faster.

Why don't nz just build up like most other countries instead of out. Even labour is going down the build out route which in auckland means more traffic chaos and gridlock from bombay

because this mass immigration cycle is coming to an end and Kiwis like to live in houses. Auckland apartment market could be flooded over next 18 months as current projects come to an end and off the plan speculators struggle to move their "investment"

Houseworks - ha-ha, nice one! Your comment just made my morning;-)

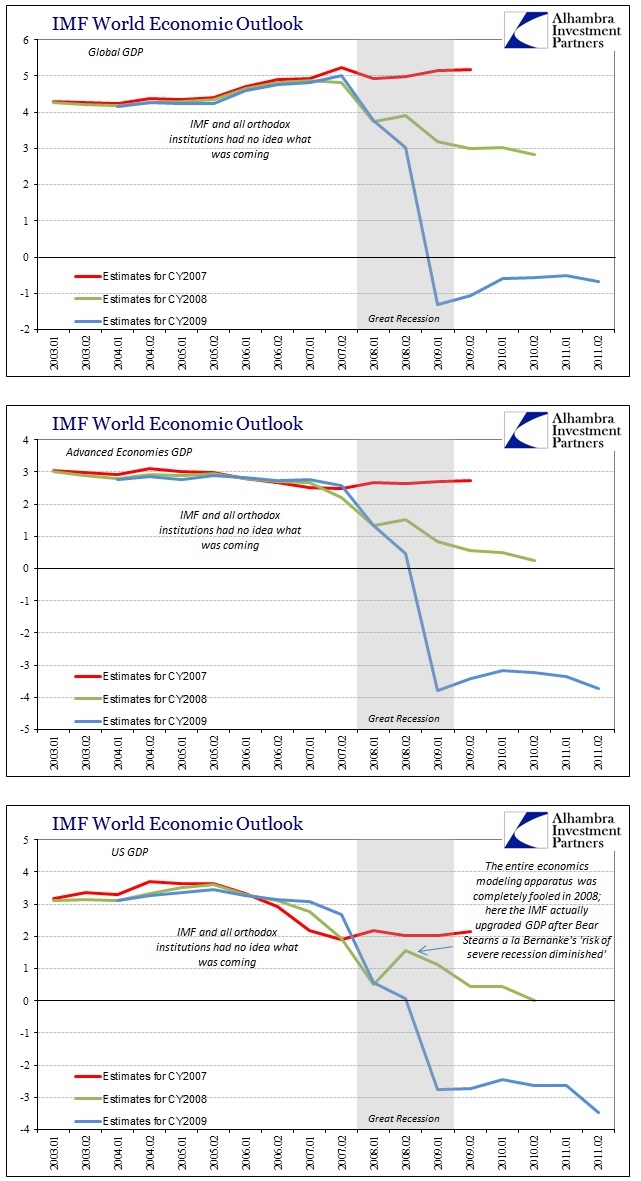

As reported elsewhere on interest.co, this is one example of the IMF track record;

http://www.alhambrapartners.com/wp-content/uploads/2015/07/ABOOK-July-2…

{kind=link}

I intend to be around long enough to see several more booms and busts so, that said, even you can be right at least once ;-)

Stay diversified!

I hope you don't include cryptocurrencies rp

Diversification is a sound theory and practise for hands off investors imo

From what I've seen every boom bust cycle is different. You may not recognise the signs of the top or bottom of the cycle when they come. Long term property investment will probably cover multiple cycles so doesn't need the blips to be successful. Imo it's a lot better than waiting for the bottom of the market rp

Uh-huh..there is nothing wrong with a little research into human behavior (the herd mentality) If you cannot understand this then you're more than likely part of the herd.

Greed is greed and fear is fear no matter the century. How can you say each boom bust cycle is different?

Human behavior hasn't changed and unless you can prove that the global investment community have learnt from past mistakes then we are surely doomed to repeat them - period.

Fear and greed are the drivers but not the catalysts for change and those catalysts are what to watch out for but I do agree that the economy will take a hit at some point. We just don't rely on that happening in order to run our investment decisions. People always need a roof over their heads in good times and bad. You can have the sharemarket all to yourself rp I once had a workmate who other staff would follow his sharemarket lead by doing the opposite because he was so bad at picking stocks. I am sure that you are very good at picking the right stocks to put your money

The banks are worth listening to because these jokers know how lax their lending standards are.

Prices are determined by a willing seller and a willing lender, and we know that the banks are very willing to push beyond the boundaries if they can get away with it.

The banks are worth listening to because these jokers know how lax their lending standards are.

The banks know the risk levels of their lending parameters....based on their own methodology for quantifying those risk levels. Any feeling about how lax their standards are would be subjective and on an individual level.

Much like the insurance companies were managing their risk very well, prior to the Canterbury earthquakes.

At which point it turned out they weren't so well.

It's a bit of a concern.

https://www.interest.co.nz/business/90905/very-disappointed-rbnz-increa…

You expect banks to tell the truth about risk in the economy? They pay good money to suppress the truth.

Nick Tuffey & co look well trained in how to pump out "everything on song" commentaries with the necessary caveats for ass protection, but there are some good points raised:

- Is there anything to suggest that incomes and job security won't keep purring along?

- Why is consumer spending relatively flat? That is a surprising claim but the data doesn't lie. It would not surprise me if most consumer-focused businesses increase revenue and profit going forward in the near term. Those businesses that sell products and services perceived as having relatively low costs to quality will fare better than most. McDonalds for example.

Unfortunately another problem that has developed while National were asleep at the wheel is the ever growing threats to coastal property. Sadly it will probably benefit National party property spruikers.

http://www.radionz.co.nz/national/programmes/ninetonoon/audio/201862894…

Yeah because erosion is National's fault.

Yet again Skudiv you either miss or choose to ignore the point. These threats have been emerging for a long time but National had the same answer as you seem to have. Hope they go away. They wont.

8% of homeowners hold 40% of because 8% of homeowners are landlords and own 40% of the homes. So it's not really a scary data point.

skudiv, in the event of this precious and self entitled 8% getting into financial distress, do you believe there is now a strong case the taxpayer should be first to the rescue? After all, Landlords are first to say they provide an essential, professional and quality service to their tenants? ;-) ;-) ;-)

When the speculator Landlord disappears, their houses will change hands at a price that reflects the prevailing market sentiment on the day.

Wow !! ...BAD NEWS for the doomers ...!! the Sun is shining afterall !!

So " They say that according to Statistics New Zealand figures, close to four-fifths of all households with an outstanding mortgage spend less than one-quarter of their before tax incomes on housing. "....!!

Does that tell us something about the affordability song that has been played for the last year or so ??...

And .. "If homeowners don’t have to sell during a housing downturn, they won’t." simple common sense fact isn't it ....

So ASB economists don't see much likelihood of a "significant" housing correction and expect "mild" price rises this year......"Mild" increase = What? is that .... 2-5%pa ?....

The tide is down and naked gloomy swimmers are getting exposed! ... more data on the way ...

Don't forget interest rates are at historical levels

that's right, and that is one of the basic factors which lead NZ and many other countries in the world to where we are today ....inflated Real Estate prices.

Put all the above with attempts to lure more people into fixing their mortgages with lower short term rates as TSB is doing ( the rest will follow)

The future is not as Dark as some here have been trying to make us all believe !!

"Put all the above with attempts to lure more people into fixing their mortgages with lower short term rates as TSB is doing ( the rest will follow)"

if you've noticed, yields are rising globally, nz is largely dependent on wholesale funds, this homeymoon run of low interest rates cant last forever ..

Yes, I did indeed and it broke the 50 year descending trendline ... So most economists are just assuming that text book rules should apply in this case and we are heading for a 2008 like crash - and this is the last leg of the bull market ..... well, maybe ,, or maybe Not !! ---

I did take notice of one CEO who said: But the world financial dynamics have changed - debtors and creditors have changed positions and QEs has made things very unpredictable !! .. so he didn't think that IRs would change dramatically in the next 3 years.

BTW, nothing lasts forever ... but you make hay while the sun shines ...

Davos 2018 starts this week - it will be fun to follow ...

I wonder how many Auckland investors out there who are like me, who owns a mortgage free family home in an amazing DGZ suburb, and very little mortgage across the portfolio (< $200k) which can be paid back within 5 years. Interest rates are largely irrelevant in this case.

wonder how many Auckland investors out there who are like me, who owns a mortgage free family home in an amazing DGZ suburb, and very little mortgage across the portfolio (< $200k) which can be paid back within 5 years. Interest rates are largely irrelevant in this case.

The point that you live in DGZ (or anywhere else in the country) and are mortgage free is irrelevant. The ASB commentary is looking at aggregates. ASB says that "four-fifths of all households with an outstanding mortgage spend less than one-quarter of their beforetax incomes on housing". That point, to them, is the overarching "hook" to communicate to the sheeple that all is well.

Interest rates are extremely relevant in the absence of substantial income growth and benign income growth expectations.

If incomes aren't already growing they will be pretty soon I think. Spectre of inflation is becoming more likely

If wages go up, as an employer I need to be able to pass those costs on, if production improves it's not an issue but if efficiency stays the same then I become uncompetitive in a global world. The big inflationary times in the late 70's, were after an oil shock and before globalisation. If my costs go up I can move, if I haven't already in a globalised world.

The other option is that I take it on the chin but capitalists are no so good at that, look how much industry we have lost, when I was young thousands worked in Wellington reassembling cars, that today looks ridiculous and it was.

Our problem is an inefficient state , growing all the time. The non-tradable sector increasing costs, it's inflation but not as we know it.

DGZ could be talking about baking a cake and he would say did you know I live in DGZ.

1050 nuff said.

Crate of Lion Red

Actually Im more into my craft beers these days.

What about the rest that are paying exorbitant prices at over 90%lvr?

Soon or later school zone will be reformed and that "DGZ suburb" could be Otara

Somethings gotta. How many apartments are due to come on line in DGZ. Both schools are already stuffed, what are their options...- rezoning - exclusion of apartment dwelling kids - increase classroom sizes to 60. All of which would lead to court action.

Is that a surprise?.. given that a typical mortgage is 25years, there are a lot of mortgages that have been getting paid down for decades, and were taken out when house prices were reasonable. How many new mortagages (not refinancing) taken out in the last 3 years exceed that 40% of income number?

Well yeah, but the ASB doesn't want to be too inquisitive in their media releases.

"if homeowners don’t have to sell during a housing downturn, they won’t"- Unless they need to, in which case they will.

LOL, they don't have to sell = they don't need to .... same thing? No ?? ...haha

My assumption is that some people will always need to sell e.g. divorce, moving to a new area, job, etc which will lower the market price and fhb will be able to buy houses at a reasonable price.those that don't need to sell will be fine.

Hi Eco Bird,

If housing appreciates by 2-5% this year then its yield will likely be better than bank deposits (after tax) - especially after you factor the rental return in.

Personally, I think a 1% capital gain would be pretty good for 2018 - given the enormity of the capital increases through 2014-16.

On average, house prices in 2017 rose by more than I had anticipated. But I tend to be on the conservative side with my forecasts......

So, I accept that house prices could rise by a bit more than 1% over 2018.

TTP

Hi TTP,

Possibly, but surely depending on the town and area -- and we have to be careful not to get lost in generic percentages .... my reading could be a bit different and outside the box because: ...

- I could see a minimum 2% rise in Auckland for "Good Houses " by end of 2018 ... and 2-5% in Hamilton - you may have noticed that Tauranga is riding on the back of its growth momentum too ...so will the others, even Palmy and Hbay).

Following Home.co.nz, and TradeMe property estimates, my properties have gone up by 5 - 9 % in 2017 in both Auckland and Hamilton ( Hamilton is yet to increase more in few years)

- I Don't see much correlation in the short term between $$ Yields+CG vs low risk saving accounts or investment funds after the good run of 2014-2017 ....BTW there are investment funds which return 10 -12% pa before tax on a good year ( and the future for these is brilliant going forward) -- Investors would have only put 20% down ( or equity) as deposit and borrowed the rest --- Most won't have the same full amount of money to invest elsewhere (unless they bought properties with cash) .... hence the lower investing capital would bring smaller $$ yields ! ... obviously these are only people who still believe in the share markets both here and O/seas .. However, these people bought property because it had better return than saving accounts..

- Today, I strongly believe ( and see) that market prices are mostly governed by S&D forces , and the speed at which building new homes can catch up with the monthly rising backlog .. that is now the core of the housing problem.. And I don't think that kiwibuilt will have any effect on the current $1M+ houses anywhere in the country! However,....Kiwibuilt will drive the price of currently outdated houses significantly lower and that alone will benefit some FHBs who like to take the challenge of restoring them.

- The housing market in the big centres lost a lot of steam since last June 2017-- less immigrants buying, banks' restrictions, LVR , and Lower than usual sales volumes --- Well, all these factors are still in place until now, however prices did not budge much, and we see prices still on the rise ...despite yields from rentals dropping like a stone ...so I called July as a bottom ..and it still is . we haven't seen a lower low... yet!

Another reason is that ( as you have mentioned before) houses are not commodities, the majority are Homes for 65%+ of property owners - these will not be selling in a hurry and that will keep prices where they currently are and appreciate by at least the annual CPI rate - why? because we have a strong economy and employment ATM, low IRs and low inflation... no one needs to sell or move unless they have to, as the report correctly mentioned ... so there is no Pressure to sell and are happy to wait for another turn of the market in the future .. why drop prices when there is serious shortage in the market? makes no sense.

- All quality stock will be influenced by the Rising Building costs which is a good 7-10% pa

At the same time, all the rubbish Rental stock will depreciate in 2018 because of the introduction of Healthy Home bill and changes to tenancy and Tax laws etc (so some newbie investors will find it too hard to hold) In addition to pressure from kiwibuilt ( if ever started in 2018)

the three coming reports from REINZ and others will give us all a better handle to where we are heading and possibly by how much ...

In my view, Serious Investors should diversify and have a sizable portion invested prudently in other asset classes nowadays albeit through reputable fund managers or even a good kiwisaver scheme if they are close to retirement --

Houses not on the market do not set the price, stronger economy will not help house prices because a truly strong economy will mean normalized interest rates and no money printing stimulus, its a long way down to a price that can be supported by income.

.

Only need a shock like China or the US come unstuck and all offshore borrowing cost go up and put a squeeze on Mortgage holders interest rate yields start to rise.

Nah we will just print more money here and lend it out at low rates.

"one of the puzzles of late had been why consumer spending had been so mild despite the tightening labour market, sizeable increases in housing equity". On the other side of the fence, is it possible that as prices rise, those who don't own are reducing spending in order to afford a home? As we see home ownership rates decrease, and these people become a larger proportion of the economy, does this result in a decrease in average consumer spending. e.g. renters spend less, Home owner spend more, but renters are growing in number.

Does this all lead to lower mortgage rates?

While mortgage rates are “historically low”, they are relatively ( to most developed economies) high.

If 4.x% is the new normal for the last 8 years, then low rates mean lower than the last 9 years, not lower than the pre-GFC era.

Economists, experts and analysts - all good stuff.

And possibly more often than not on the money or within cooey.

However, certainly not infallible and their predictions are ultimately just that - they can trip over an unexpected event or be side swiped by a darker shaded swan along with the best of them.

There is a clip that is, with the benefit of hindsight, just so damn "funny" - however, nothing was "funny" in terms of the ultimate economic devastation wrought.

Fox had a weekly financial program called "Bulls and Bears" - everything in the US looked so rosy late

2006 - except for the opinions of Peter Schiff in this case, who in the eyes of many was simply making a nuisance of himself.

https://www.youtube.com/watch?v=_HFNJw7xGSA

One of those fateful times when an outlier is proven to be so right - and self proclaimed experts were just so very, very wrong.

Tauranga out-ranks Auckland as NZ's most unaffordable city for housing - It's more affordable to buy a house in London than in Tauranga, a new study shows .

Surely the doomsters here will switch their target and launch their attacks on Tauranga now LOL!

https://www.stuff.co.nz/business/property/100763642/tauranga-outranks-a…

From that Stuff article:

Rochester, New York is the most affordable place to buy in the world, with households needing roughly 2.5 times their annual income to pay off a house.

However Wikipedea has this to say:

In 2012, Rochester had 2,061 reported violent crimes, compared to a national average rate of 553.5 violent crimes in cities with populations larger than 100,000.....17.1 murders per 100,000 people.

While New Zealand has a murder rate of about 1.5 per 100,000 people.

Rochester, New York is the most affordable place to buy in the world, with households needing roughly 2.5 times their annual income to pay off a house.

Columbus, Ohio has a multiple of 3.1, Also, according to Wikipedia:

The city has a diverse economy based on education, government, insurance, banking, defense, aviation, food, clothes, logistics, steel, energy, medical research, health care, hospitality, retail, and technology.

Columbus is home to the Battelle Memorial Institute, the world's largest private research and development foundation; Chemical Abstracts Service, the world's largest clearinghouse of chemical information; NetJets, the world's largest fractional ownership jet aircraft fleet; and The Ohio State University, one of the largest universities in the United States.

As of 2013, the city has the headquarters of five corporations in the U.S. Fortune 500: Nationwide Mutual Insurance Company, American Electric Power, L Brands, Big Lots, and Cardinal Health. The food service corporations Wendy's, Donatos Pizza, Bob Evans, Max & Erma's and White Castle and the nationally known companies Red Roof Inn, Rogue Fitness, and Safelite are also based in the metropolitan area.

In 2016, Money Magazine ranked Columbus as one of "The 6 Best Big Cities", calling it the best in the Midwest, citing a highly educated workforce and excellent wage growth. In 2012, Columbus was ranked in BusinessWeek's 50 best cities in America. In 2013, Forbes gave Columbus an "A" rating as one of the top cities for business in the U.S., and later that year included the city on its list of Best Places for Business and Careers. Columbus was also ranked as the No. 1 up-and-coming tech city in the nation by Forbes in 2008, and the city was ranked a top-ten city by Relocate America in 2010.In 2007, fDi Magazine ranked the city no. 3 in the U.S. for cities of the future, and the Columbus Zoo and Aquarium was rated no. 1 in 2009 by USA Travel Guide.

Columbus homicides hit record-high in 2017

The 2017 murder rate is 16 people killed per 100,000 and rising while ours is going down.

That's because NZers are nicer people.......

And that's part of the reason why so many people want to live here. They want to get away from the crime.

TTP

okay that proves it, I'm calling BS!. Columbus! that place really is a shi$%hole. Take it from someone who lived there. Its a dangerous place. On my first day the Mexican in front of me at the 7/11 on North High St pulled a gun and robbed the store. Six months later I almost got carjacked. The zoo has a mural of the world without New Zealand! Oh and get this.. There's a live kiwi on display, labeled as an "Australasian Kiwi". Its a miserable looking thing in a 3mx3m pen with no shelter and nowhere to hide. I almost cried when I saw it, and wanted to take it away with me. Its probably dead now because I'm going back over 10 years. The university was able to lower it's abduction and rape statistics by reducing the area it surveyed the stats from.

Combing back to Tauranga being overpriced, please! Its a paradise! What are the median prices in Matua or Mount Maunganui? 786K and 834K respectively! That's dirt cheap for the boomers who're buying the homes there. Compare that to Kohimarama 1.7 Million! Who's supposed to buy that in 10 years time? the millennials? gen X.. What's really overpriced! get real.

@Fat Pat unfortunately Kohimarama can't quite make it to the Top 10.

Top 15 Suburbs - QV Median Home Value Jan 2018:

1 Herne Bay $2,568,050.00

2 St Marys Bay $2,253,400.00

3 Remuera $2,091,600.00

4 Stanley Point $2,043,800.00

5 Campbells Bay $1,973,800.00

6 Orakei $1,918,900.00

7 Westmere $1,902,200.00

8 Epsom $1,901,950.00

9 Mission Bay $1,878,250.00

10 Ponsonby $1,785,250.00

11 St Heliers $1,783,050.00

12 Kohimarama $1,762,700.00

13 Takapuna $1,758,450.00

14 Devonport $1,728,850.00

15 Glendowie $1,714,350.00

I’m not sure which property types are included, but Kohi has a lot of small units, many of which are leasehold. If those are included in the median then it will never be in the top 10.

I love the way these numbers are padded out to the cent. It must make these elite property owners feel so big.

okay that proves it, I'm calling BS!. Columbus! that place really is a shi$%hole. Take it from someone who lived there. Its a dangerous place. On my first day the Mexican in front of me at the 7/11 on North High St pulled a gun and robbed the store. Six months later I almost got carjacked

Oh I see. So low Demgraphia multiples are explained by the higher incidence of crime and murder.

Right. Got it.

sorry J.C I just got rattled. Comparing Tauranga & Auckland to Columbus Ohio is too much for me. Even saying Tauranga is more overpriced than Auckland makes me balk. Tauranga's two most expensive prestigious suburbs are Matua and Mount Maunganui. They're both paradise on earth and super cheap considering the buying demographic. Kohimarama in Auckland by contrast is not just a little bit overpriced, it's obscenely expensive in my humble opinion, and it's not even in Auckland's top 10.

Make that truly obscene when you realise that a ful site home is more likely $2,250,000 plus, however there is a logic to it when you look at the household income and lifestyle mix.

yeah I liked kitesurfing by the beach after work, but the incomes don't justify the house prices. They did in 2010 but not now.

Columbus Ohio is a very boring place. Plus high crime compared to Auck.

Interesting option, but no, I think I'll just put my "idiot" hat on and celebrate the fact that the simply disgraceful results of the previous administration's inane policies have now spread to other towns and regions.

My goodness, wearing an "idiot" hat and not attacking is much better as you suggest - I find myself completely mindless and self centred, but pleasingly and oddly quite content in such a state.

The mist has cleared and suddenly it seems that if only every region and town could knuckle down and become even more unaffordable - we'd all be happier.

What a revelation - I suggest all NZer's remain focused and work towards a National victory next election to ensure it happens.

Happy Days!!

I would spend about a third of household income on housing however live on a third leaving the other third to cover any unexpected rise in interest rates or other costs. While things are good half of that third would go into my war chest and the other half into luxuries like overseas holidays and unnecessary things.

Talk of small interest rate rises causing stress and calamity are over-stated imho.

Now would seem like a good time to purchase as there are undoubtedly good buys about for those with an eye for a bargain and willing to play hardball. Easy do-ups offered by vendors who have held the property for a while would be my recommendation for FHBs. Waiting unnecessarily would be a mistake or a bit of a gamble. The 40% correction is looking more and more remote.

I read a comment the other day saying Remuera home owners now have to pay for people to buy their 300sqm house LOL!!

I heard the past few decades that people expect other people to pay their mortgages, aided by taxpayers who actually pay their taxes and aided by banks who actually never work for their money, just multiplied it from those who actually saved and clipped the ticket as best they can in the process. Then sent the proceeds overseas to a foreign ex-con Nation who borrowed the idea from a time immemorial, thereby compounding the problems, worldwide.

I may have been wrong, because that was actually a Total 'fraud' I thought was Totally illegal.

Governments and honest people would never countenance that...surely.?

Ok, it’s from Zero Hedge... but this could kick off something even if it is only half true...

https://www.zerohedge.com/news/2018-01-21/200-million-investors-may-hav…

Hence the popularity of real estate in places like NZ, Australia and Canada. We've built up quite a reputation for being stable with high trust and sound property law.

Apparently investors have lost an average of $55 each!

A comment on the article:

These ponzi's are exactly what's pushing Chinese into RE and gold. If you don't hold it (or live in it) you don't own it.

Not just that, All 3 of those countries benefit from the Anglo-Saxon monetarist hegemony; are commodity exporters; are heavily reliant on house prices as the key driver for bank income; and have the inability to transform from high-cost strictures without economic degradation. At the very least, Canada has proximity to the U.S. and its economies of scale to make the transition easier for consumers,

Is that why Vogel's bread is cheaper in the UK than New Zealand?

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=119…

Is that question to me? NZ is a high-cost producer of consumer goods and services largely because of the market size and the lack of economies of scale to make goods / services cheaper. That is why some companies in Japan and the U.S. have been able to make the transition to consumer needs after collapsing asset bubbles.

No mention of what's these economists forecasted in previous years and how close to reality they were?

It almost as of they have a free pass to make up whatever horse**** they like.

ASB actually have the best paragraph in their article to explain why prices haven't dropped and what could make them drop. I think 90% of readers don't know which paragraph I'm referring to

Is it this one: "Unlike the run-up to the GFC, the household sector in aggregate had not used the rising equity of their dwelling as an ATM."

Yes, My thinking too

"Unlike the run-up to the GFC, the household sector in aggregate had not used the rising equity of their dwelling as an ATM.

How do you explain that then? The ASB does not have the ability to determine the relative difference between wealth-driven consumer spending at different points of time without the relevant data sets. Do you know what inferences they're making? From what data sets?

Parroting a media release does not make something fact.

Can someone tell me if 23 Ranui Rd in Remuera has been sold? Kate?

https://nz.hougarden.com/en/23-ranui-road-remuera-816033

http://rwepsom.co.nz/properties/residential-for-sale/auckland-city/remu…

The Flight of the Migrant Millionaires

Top countries that millionares flee from:

France

China

Brazil

India

Turkey

Top countries that millionares flee to:

Australia

USA

Canada

UAE

New Zealand

Interesting that NZ makes it onto the list.

Is that why we have flee markets?

It's why many commenters here consider Auckland to be a flee-pit.

Interesting that there are so many stories that report of corruption and money laundering from the fleeing "millionaires".

A real feather in our cap - as a nation, we should be, and it would appear in many cases are, proud.

Custard, you know that the say, behind every great fortune there is a great crime. I don't think little old NZ is world ranking in its ability to attract millionaires because it turns a blind eye to crime. It's more an endorsement of our advanced social system, solid foundations and high level of freedom. These people want their children to grow up here where it is not dog eat dog all the time and you are protected by laws that have been developed over centuries to protect property rights. It is our system of laws that make Western civilization so superior and New Zealand ranks #1 as top Anglo-Saxon country. That's why even though we are so tiny we still rank in the top five of millionaire magnets.

Here is a good article that explains things

New Global Rankings Confirm, Rule of Law Makes Western Civilization Superior

In all honesty I think it's a bit of both with our system.

Enforcement and regulation of many of our laws relies on an honesty and trust

provision - but equally there exists the ability to "hide and conceal" behind our legal system.

It's the apparent ease and ability to sidestep and abuse the above that gets my goat.

Other less "enlightened" jurisdictions might simply run you down for similar behaviour.

I also suggest the behaviour of some of our new millionaires does not match that of our "superior" Western civilisation - so for how long do we continue to just shrug and turn a blind eye?

And how is this ultimately to NZ's betterment?

People, who appear mostly to be immigrants, flagrantly ignoring laws that we have, who while they appear to being caught out, probably are not in total and probably have made a poultice out of flouting our laws until such times as they do. We have allowed ourselves to be used by some pretty shady characters, who should not even be in this country as far as I am concerned.

With little inflation it's unlikely RBNZ would be anything but supportive of asset price inflation. In reality no political party plans to substantially change the housing supply situation. That said there may be a change in the employment market if productivity continues to fall and wages rise, eventually we must reach an inflection point for businesses.

As noted by me in an earlier thread, NZers are becoming accustomed to the elevated house prices brought about by the 2014-16 upswing - and are steadily adjusting to them. Exactly the same process is underway now as with previous market upswings.

I imagine that as the year moves on, fewer and fewer people here will push the line that, "a major correction is about to happen". As the property market consolidates, that particular view (desire?) further weakens in credibility.

Anyway, there's no need to fear a stable property market - even if it remains relatively quiet over the next year or so (which is what I foresee).

TTP

Welcome back TTP, hope your evening walk tonight has been enjoyable. I definitely feel a lot more at ease and calm after reading your comment...very wise comment indeed.

Good to see a rather simplistic and mindless comment can ease your troubled mind DGZ - and indeed proof that it is the little things that are sometimes the most rewarding and comforting.

Yes, speaking of the moment, a most pleasant evening in Whangamata currently - a lot of great childhood memories from what seems a very long time ago - happily it's still a wonderful spot, and real Kiwiana to boot!

However, real estate, as always it seems, continues to take centre stage on the site, thus a couple of thoughts for some newbies.

In the end yield matters, having your property actually rented may matter, having tenants that actually have employment matters, the possible end of a 30 year bond bull run may very much matter and for what it's worth, the end of a mind boggling China real estate bubble to dwarf all will probably certainly matter.

If some of these potential problems should come to pass, perhaps NZ's monster economy can continue to swat this this all aside.

The ask though, may well be insurmountable at some point in the future.

No matter - stay calm, and invest on!

Good to hear from you, DGZ.

I trust you're hale and hearty - and wish you a great year with the markets.

TTP

" As noted in an earlier thread, NZers are becoming accustomed to the elevated house prices brought about by the 2014-16 upswing - and are steadily adjusting to them. Exactly the same process is underway now as with previous market upswings."

That is correct TTP .... I would also add that the recent QV valuations have cemented these prices ( at least in the minds of the sellers and Banks ) .. so unless a big disaster or two happen as ASB report explains, property prices will hold and only fluctuate based on its own dynamics of S&D and improving affordability ..

"Exactly the same process is underway now as with previous market upswings."

I would suggest it is possibly a push to use the word "previous" within the context of the last few years - unprecedented money printing coupled with ultra low interest rates does not fit the historical norm - and to top it off simply goodness knows what's been going on under the financial hood both internationally and domestically within this brave new world.

Couple that with a flood of mass migration into New Zealand and combine with a handbrake on construction and in the and you have all the elements of runaway prices - while all the while NZ facing historically low inflation and minimal wage growth.

I don't think NZ has previously has faced such a confluence of factors.

A simplistic observation - QE is in the process of being wound down, interest rates, whilst still low, are currently rising world wide, migration numbers are going to be reduced and new builds are on the increase.

I'm saying again that I don't think, in my lifetime anyway, that we have been in this space before.

Although I love custard, it's delicious, I don't think it understands NZ property

"NZers are becoming accustomed to the elevated house prices brought about by the 2014-16 upswing"

Thats all well and good, but if NZers cant afford to buy the houses and the banks wont lend at those prices, it means very little.

I hope they are right ...............

@Zachary you might want to keep an eye on this one...I think I have seen multiple RE's trying to sell it without much luck in the last couple of years including Ricky Cave! https://www.trademe.co.nz/property/residential-property-for-sale/auctio…

Yes it seems to be tough selling these types of places. I remember commenting about them when they were selling new. Have to be fit living there with all the stairs. Nothing beats a standalone bungalow with nothing shared which is what it is competing against in the area.

Hi Zachary,

You write: "Nothing beats a standalone bungalow with nothing shared which is what it is competing against in the area."

That is absolutely correct. A stand-alone dwelling on fee simple (freehold) title has a huge advantage over the other forms of property ownership. But not everyone understands that.....

TTP

And the reality remains. New Zealand houses must eventually reset to the prices that the various stratas of our population can correctly afford. The questions I cannot answer are how and when. However, such answers may not be too far away.

How: Asset prices are driven by credit cycles. Credit cycles are fundamentally driven by demographics. In the last cycle, there were a number of factors that enabled an expansion in prices beyond our per capita borrowing capacity. Few of these factors will exist in this down turn - and the next up turn, however there has also been structural changes. In particular, we now have KiwiSaver which has had the biggest impact of all the factors. Without getting technical, it is easy to appreciate how after 10 and a bit years (since its inception), a large number of Kiwi's have saved a considerable amount of money, which they probably wouldn't have done so otherwise. If you do the math, combine it with the demographics, then look at the KiwiSaver statistics for each region (withdrawals for FHB in particular) you start to see a familiar picture for each region (house price increases/activity).

When: Analysis points to a correction appearing in house prices around Sep 2018 - Mar 2019 followed by a weak attempt at recovery then a final low appearing around Dec 2020 - Mar 2021.

"When: Analysis points to a correction appearing in house prices around Sep 2018 - Mar 2019 followed by a weak attempt at recovery then a final low appearing around Dec 2020 - Mar 2021."

The spurious illusion of precision.......

Anyone who thinks he/she can predict the future as accurately as that deserves to be ignored.

TTP

I have good news Didge, such is already the case. There are plenty of affordable houses around New Zealand.

Be gone with your Marxist agenda for Auckland.

Didge: "New Zealand houses must eventually reset to the prices that the various stratas of our population can correctly afford"

Why do you think that Didge? Because it would be nice? Or why?

I'm really surprised that everyone has seemed to conveniently forgotten that there's a Foreign Buyers Ban that's scheduled to be enforced later this year. So understandably there has been a bit of an up swing for Auckland in the last few months since the announcement of this ban to beat the restriction.

And don't forget that the more Auckland's property rises the sooner it the ban will be enforced.

https://www.bloomberg.com/news/articles/2017-10-31/new-zealand-to-slap-…

CJ099 Thanks for finding a reason why the property market has not crashed 40% yet,. but it will right? Soon?

You know as well as the rest of us that the Foreign Buyers Ban will be a game changer for Auckland.

I thought the game changer was the Chinese Government restriction on capital flight? Mind you, wasn’t that close to a year ago?

Yes and look at the impact that China's capital flight restrictions have had on the NZ property market. We've gone from Auckland's massive prices increases year on year and pretty much everything selling at auction towards the end of 2016, to now where hardly any property is selling at auction.

But we still need to tackle the money launders, having a foreign buyers ban will help to prevent them from using Auckland as a Swiss bank account.

No I don't know the impact of the foreigner ban. I did hear today though, that Labour are postponing its Introduction

Hi CJ099,

I don't think people here have forgotten the foreign buyers ban - but few believe it will be very effective. It's too little and too late....... In case you haven't noticed, the housing horse has bolted.

There's a good chance that (average) house prices will continue to increase this year - even if sales volumes remain low.

TTP

In case you haven't noticed Ttp there very few properties selling at auction at the moment to fetch top prices. Not sure how you expect FTBs to afford Auckland's million dollar price tags.

Come to think of it has Auckland had any successful auction sales this year?

Hi CJ099,

Auctions are so deja-vu. Auckland has moved on.

I don't follow house auction statistics these day - because they've become so meaningless.

TTP

TTP, auction statistics. Are they meaningless to you personally or to interest.co.nz and its membership commentators? If auction clearance rates were back to 80-90%, instead of 30%, would they mean something to you then?

You say Auckland has moved on, where to exactly? Are Aucklanders no longer interested in selling houses to each other at a whopping profit?

They've become meaningless? or they don't say what you want to hear so you put your fingers in your ears and shout "lalalalalalala". I believe thats called confirmation bias in scientific circles.

Hello readers. Please note that I will no longer try to educate property spruikers. They are unable to learn.

....it's a bit like undoing the handiwork of property investment seminar! Best to try educating those before they enter. Sadly, for many, it's already too late. I don't know what tools they use on those poor souls but its all property-property and property on the outside and nothing else.

Thanks Didge, great news

Interesting choice of words Ttp. By that do you mean that Auckland's property is simply not selling a top price, well it is a buyers market now. Lets watch the paper millionaires deflate. ;)

Back in 2016 I did a similar exercise based on the HES data from Stats NZ (up to 2015). But I focused on Auckland.

Suffice to say: Things are very different for Auckland, where the estimates suggest that a quarter of owner-occupied households are spending more than 40% of their post-tax income on the primary mortgage.

However, these surveys are based on rather thin numbers, and so there is a large margin for error. There may be other methodological differences, too.

These issues could be put to rest if the government provided funding to Stats NZ for a comprehensive survey of consumer income and finances. We need the data...

Totally agree with the ASB report, as long as interest rates stay at the current levels the economy is going to keep on trucking on. You guys should watch more Aljazeera news and see what a mess the rest of the world is getting in and its only going to get worse not better. New Zealand is paradise in the Pacific by comparison and its no wonder millionaires are coming here to escape the Chaos. Smart people realize that all the money in the world cannot save you if you don't get out in time.

How about reading the facts again!

'close to four-fifths of all households with an outstanding mortgage spend less than one-quarter of their beforetax incomes on housing'

It says BEFORE Tax Incomes! why do we continually accept this sort of manipulation by banks!. When you go to the supermarket to buy groceries your food budhet is not worked on before tax but net after tax that's in your pocket and disposable. How about the banks re run the numbers with net incomes then those whom comment that risk is not that high may think twice next time.Give me strength, I've been banging about this for years!!

Wow that is dirty. So that figure would be more like 40% of after tax income.

Those figures are telling me a completely different story, and it is that most of the property is owned by people who have either owned it for some time, thus their repayments are a lower % of their current income, or it is owned by people with well above average earnings.

I would like to know how many of the properties are owned by buyers who have only entered the market in the last year or so, maybe even five, then the tale might well be very different.

For a Bank, this looks like a pretty bleak outlook. They normally talk it up alot more than this.

"Most homeowners still look 'reasonably well placed to meet mortgage commitments', ASB economists say; they see 'mild' house price rises this year"

Translated

"over 50% of homeowners could possibly still pay their mortgage in a downturn Gulp! House prices could rise in some places but Auckland looks doomed"

Dont worry though DoubleGZ will be one of the lucky ones and still be able to squalor around in his own little piece of paradise that he keeps going on about.

Time will tell! Global deleveraging has started and its effects will hit our shores.If the trend of declining sales volumes continues, pressures will rise. Circumstances change and people need to sell for a variety of reasons.

Going to be an interesting year none the less

.

Asking bank economists whether they think housing is destined for a correction is like asking the oil industry if we should all move to cleaner energy.

Im thinking we're all in for a rough ride in the coming years. We should spend our cash while we can on some well earnt hedonism...i mean ovwr the top never forget type hedonism. For your wealth and hard work may be squandered by the mechanisms of our economic structure...it operates in well defines cycles based on human behaviour and one thing is certain we always behave the same. Im thinking big boats, loose morals and copious libations for the long weekends.

Bluff. Now you’re talking. Although Im too tight to buy a boat, take a certain pride in maintaining a consistent moral code and gave up alcohol a few months ago. But go ahead without me and Ill just revel vicariously in your exploits

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.