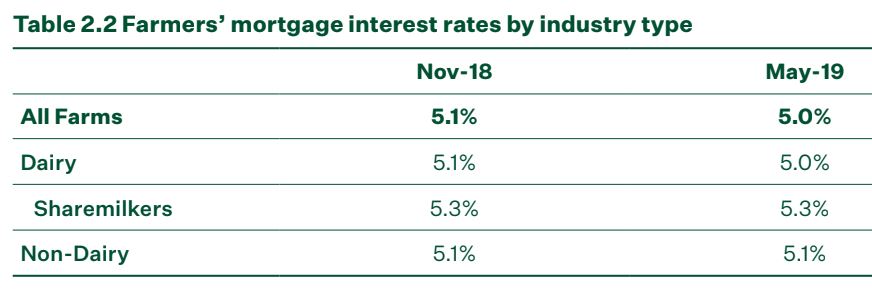

The average mortgage interest rate paid by farmers dropped by just 10 basis points over the six months to May, Federated Farmers' latest banking survey shows.

The May 2019 survey shows average farmer mortgage rates dropped to 5.0% in May from 5.1% in November last year. The Reserve Bank cut the Official Cash Rate by 25 basis points to a record low of 1.50% in May. And KPMG's latest annual Financial Institutions Performance Survey shows banks' funding costs at their lowest level in the 32-year history of the survey at 2.69%.

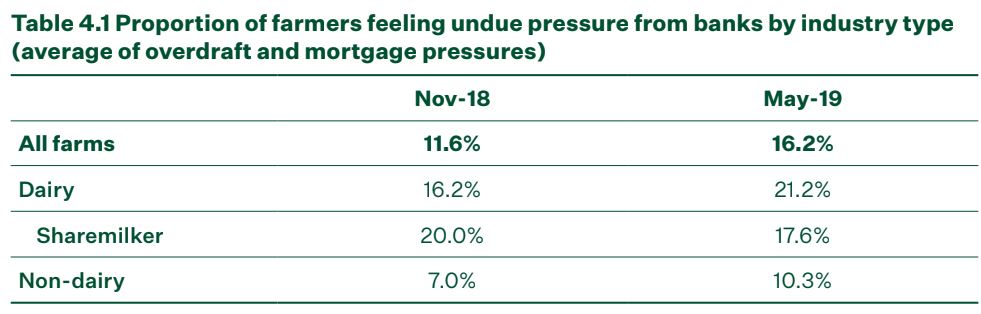

Meanwhile, the Federated Farmers survey shows the proportion of farmers who say they feel undue pressure from their banks increased five percentage points over the six months to May.

"As a group, more farmers feel undue pressure than any time since August 2015. This is largely driven by the dairy industry. Share milkers remain relatively stable experiencing less pressure. This will likely be due to their mortgages that are substantially less than dairy farms," Federated Farmers says.

The survey shows farmers' satisfaction with their banks continues to decline reaching its lowest point since the survey began in August 2015. Satisfaction with banks dropped to 71% in May from 74% in November. Federated Farmers says falls are most apparent in the dairy and share milker groups.

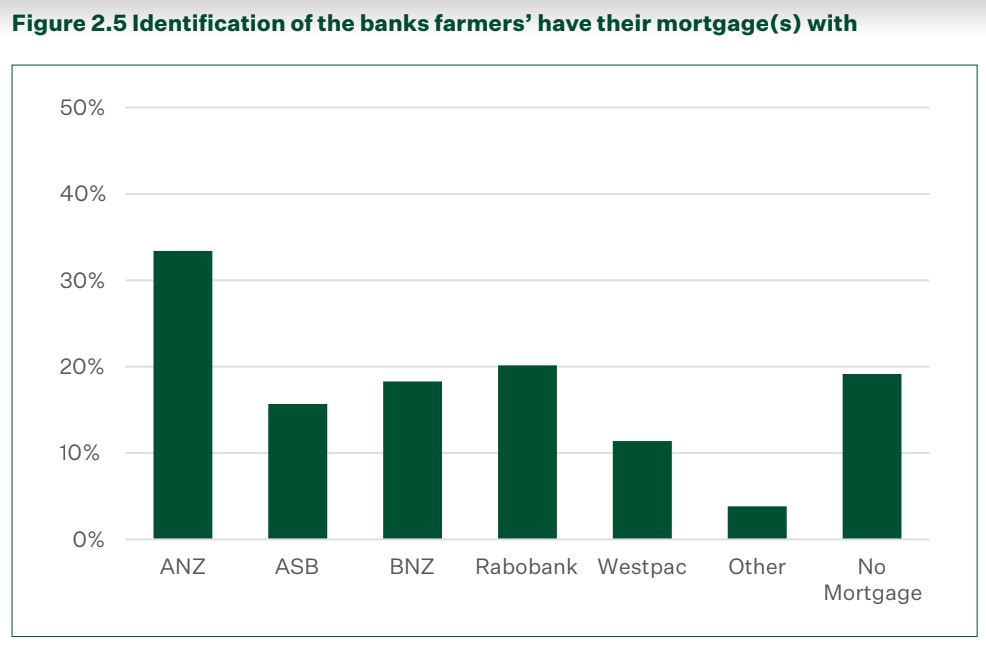

ANZ, the country's biggest rural lender, continues to be the most common bank used by farmers for their mortgages, with just over one third of farmers banking with ANZ. Westpac was the only bank showing an increase, albeit of just 1%, in the number of farmers holding a mortgage with it. Almost 20% of farms have no mortgage, down four percentage points from six months earlier.

ANZ, which has $17.8 billion of rural lending exposure giving it 28.5% market share, is currently under regulatory pressure. ANZ is increasing its risk weighted assets by more than $10 billion after the Reserve Bank reviewed the bank's capital adequacy on farm lending and residential mortgage lending. The increase in risk weighted assets comes with a minimum regulatory capital requirement of $800 million. ANZ says the Reserve Bank reviewed its farm lending and mortgage models and determined the outputs weren't in line with its expectations nor the outputs of peer banks. This is because the regulator believes the quality of ANZ's loan books isn't sufficiently better than its competitors to justify lower risk weights, ANZ says.

In its latest bi-annual Financial Stability Report last week the Reserve Bank said most dairy farms have been profitable for the past three seasons with dairy prices and production good.

"But some farms struggle to make profits at current prices, particularly those with large debts. Around 35% of dairy farm debt is to farms that have more than $35 of debt per kilogram of milk solids (kgMS) produced annually. On average, these highly indebted farms require a price of $6.20 per kgMS just to break even. Fonterra currently forecasts a price range of $6.30 to $6.40 for this season," the Reserve Bank said.

The May 2019 survey is the eleventh iteration of the Federated Farmers survey. It's conducted twice a year typically in May and November by Research First. There were 1,326 respondents.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.