By David Hargreaves

Fonterra has produced a very mixed bag of announcements with its interim result - raising the forecast milk price to farmers by 15c, but lowering the forecast dividend for the year by potentially as much as 15c also.

Contrary to some expectations, Fonterra has fully taken on the chin the fall in market value of its 18.8% stake in Beingmate Baby & Child Food Co, acquired in 2015 for NZ$756 million. Beingmate made a loss this year of about NZ$208 million.

Fonterra's written its holding down by $405 million, to a value of $244 million, which reflects recent on-market prices.

The co-operative's declared an interim dividend of 10c a share and forecast a full dividend for the year of between 25c and 35c. Last year the dividend was 40c.

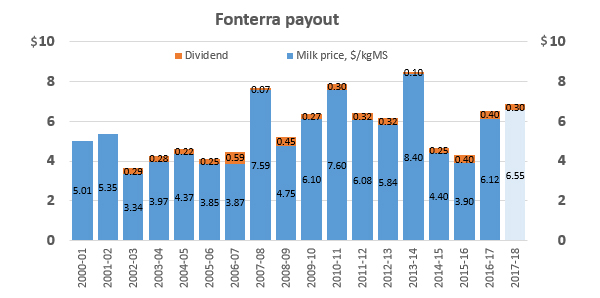

With the dividend and the forecast milk price of now $6.55 per kilogram of milk solids, this will mean a cash payout for farmers this year of between $6.80 and $6.90 - which Fonterra says would be the third highest in the past decade.

Fonterra chairman John Wilson said the payout was "good news for New Zealand as it represents around $10 billion flowing into the country’s economy". See here for the full dairy payout history.

"However, we are very aware of the challenges many of our farmers are facing this season with difficult weather conditions impacting production. While the global supply and demand picture remains positive and we expect prices to stay around current levels, we will be watching for any impact on market sentiment as spring production volumes build in Europe.".

During the half year Fonterra was also hit by the $183 million damages payment to Danone.

This and the Beingmate write-down have led to a reported half-year loss of $348 million. On a 'normalised' basis, taking out one-offs, Fonterra says the net profit after tax comes to $248 million. The Fonterra published half-year report is available here.

On the Beingmate write-down, Wilson said while Fonterra appreciated the "substantial opportunity and privilege" of its business in China, "our shareholders and unitholders will be rightfully disappointed with this outcome".

"Beingmate’s continued under-performance is unacceptable. The turnaround of the investment is a key priority for our senior management team," he said.

"The opportunity in the Chinese infant formula market remains, as does the potential for our Beingmate partnership – but an immediate business transformation is needed for Beingmate to benefit from the ongoing changes in the market."

Wilson said the board would decide how the Beingmate impairment and the Danone payment would be treated for final dividend purposes after the end of the financial year when it would have the full picture of Fonterra’s operating performance.

"Given the possible impact of these decisions, the Board is providing a forecast dividend range for the full-year of 25 – 35 cents per share, rather than just the earnings per share guidance normally given.

"Based on our dividend policy, this forecast dividend range would allow for the Board to add back the Beingmate impairment at the lower end through to an adjustment for both Beingmate and Danone as one-off events at the higher end.

"In the circumstances, we have taken a prudent approach in determining the 10-cent interim dividend."

Results Highlights

• Forecast Farmgate Milk Price $6.55 per kgMS

• Interim dividend of 10 cents per share – to be paid in April

• Full year forecast dividend range 25 – 35 cents per share

• Total forecast cash payout $6.80 - $6.90

• Revenue $9.8 billion, up 6% from the 2017 interim results

• Normalised EBIT $458 million*, down 25% from the 2017 interim results

• Beingmate investment impairment $405 million

• Normalised Net profit after tax (NPAT) $248 million*, down 36% from the 2017 interim results

• NPAT $348 million loss, down 183% from the 2017 interim results

• Normalised interim earnings per share 15 cents*

• Ingredients normalised EBIT $558 million*, up 9% from the 2017 interim results

• Consumer and Foodservice normalised EBIT $193 million*, down 38% from the 2017 interim results

30 Comments

Surely this is the final nail in Theee -o's coffin. That's the 2nd 'invest in China' shambles he's resided over. He must have written down close to 3/4 of a billion dollars now. Phenomenal.

But there is no democracy in Fonterra so he'll probably still be 'leading from the front' in 12 months time.

and expecting a bonus

The $750 million should have been put into A2Milk but no they knew better. The CEO and chairman should resign. As per usual in NZ they will stay on and everyone will pretend it never happened.

A good suggestion Gordon, but I'm afraid you'll never see voluntary resignations here. The board are simply too self serving in their interests and actions. The 15 cents increase in forecast payout is to distract the farmers from the $405m write down, and do you know what......it will work

John Wilson is up for re-election this year so can be voted out this year.

That's right CO, the election will be decided on the age old (decades) cooperative principle of share backed milk solids. If John remains it is a fair reflection of shareholders satisfaction with governance, direction and performance, much the same as any listed trading company.

Heres a question.

Could what Leonie Guiney wants to talk to media about, shave 30 cents off they payout if it got out into the general market?

Reducing dividend will likely affect share price. I'm looking to buy shares so I have no problem with them dropping - they will rise again.

'they will rise again',... based on? .. engaged shareholders, a unified culture, and exceptional governance?

Hi omonologo - Based on the investment community 'playing' with the FSF units and Fonterra shareholders having to share up. When units go up shares are not far behind. The FCG band of trading in the last 12months (21/3/17-21/3/18) has varied between $6.68 & $5.81. FSF is $6.66 and $5.81.

A bit of perspective on both the milkprice and the profit. Synlait just announced a huge increase in profit, despite paying the same or more for the raw ingredient i.e. the milkprice. If that is repeated by the rest of the 20% of non Fonterra milk proccessors then its a pretty good indicator of where Fonterra is sitting.

To my mind over the last few years the smaller companies have been able to react so much faster, by building a single plant they have due to their size been able to shift a large percentage of production to value add. Conversely Fonterra would need to build Ten plants plus to have the same effect. To big, to slow, let alone not having any real direction save for the 3 Vs which no one understands.

Just looked at Synlaits halfyear profit. $40m from 70mkgs or so. Thats nearly $0.60 a kgMS. Fonterra "normalised" profit is only $0.16 kgMS.

Apples and oranges. Synlait and Tatua should be compared if you are looking at relative comparisons. Does Synlait have an advantage in having Chinese shareholders? What value do they bring to the business?

Fonterra should be compared to like sized multinationals.

No not apples and oranges, thats horticulture. Milksolids price vs milksolids price, and profit per kilo vs profit per kilo. I dont see the problem with that basis for comparison.

Link to the Synlait announcement: note the A2 milk involvement they have.

Note also their shareholding:

- Bright Dairy Holdings 39.04%

- Mitsui (two holdings JP and AU, 5.03% and 3.35%

- Munchkin (USA/CA) 3.87%

- That's 51.29% right there

A small, furry mammal, cf the lumbering dino that is the Big F. A Munchkin, no less...

A CEO able to destroy around $750mn of value in recent years is worth a salary of $8.3mn p.a. to Fonterra. Presumably someone capable of destroying double this would be worth at least $16mn p.a. to the board.

Theo Spierings is stepping down. The Fonterra Board started their search late last year for a new CEO.

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=120…

Imagine not too many people will be upset about it. John Wilson should be shown the door at the same time.

Will anything change in the direction and performance of Fonterra with Theo stepping down?

No disciplines. No accountability. No competition. Political high circles aplenty. Sound a bit familiar. Solid Energy, Fletchers for instance.

Foxglove you are ignorant in regard to claiming there is no competition. One of the competing processors Synlait was mentioned above.

I think I have the talent to be a Font-error executive, I can milk it with the best of em.

Tis a strange World, where people are rewarded for doing the wrong thing, when those who do it right, pay their way.

Butter is now pure gold...here in NZ....World Market prices plus...

Pity the poor consumer..Tis why I am seeking a Font-error easy peasy job, I can spend up large, if really desired.

From an outsiders point of view, this all seems very typical of current governance at Fonterra. Balance the bad news by some false hope. So announce an increase in payout. A 'forecast' increase. Roll it back in another couple of months.....The chair needs to go as well. Didnt they provision something like 17 mil for the Danone debacle. They swore thats all it would cost. Well just times that by over 10 then add some for legal.

Ive mentioned on here before that I thought Fonterra took corporate spin and communication to a different level and been told no they all do it. But I still reckon Im right, they have it so down pat.

Belle, increase in payout - JW is up for re-election and it puts pressure on the competitors - Synlait and OCD in the Waikato and Mataura Valley & OCD in Southland. ;-) Doubt it will get rolled back as it's too late in the season to do that - many in the north dry off in April/early May.

Fonterra is keen to get Danone back as a client, so it can't have been all bad. The provision they made was what was in the contract they had with Danone, but the arbitrators saw it differently and awarded more.

They were going to announce Theo's resignation in April but I guess as they have been looking for a replacement since November it was going to be hard to keep it under wraps.

Seven of the eleven Board members have been on for 3 years or less so have largely legacy issues to deal with. I will give them another three years to see where it goes as I believe the current Board is better skilled to hold management to account. Imo there are others there more than ready to step up to the role of Chair.

Interesting thoughts and information CO. Yes I have also noticed election time the payout goes up. I guess they will keep the good news out there til after then.

None of you seem to get that the Chinese govt will not be interested in having a huge foreign entity being the biggest player in their dairy market. Best everyone get used to the idea that the demise of Fonterra is in their sights. They want control from paddock to plate and the purchase of the Crafar farms was just the start of that. Do we really need another drying plant in the Waikato?

Beingmate was just bait, what has happened was probably pretty sticking to the script.

Fonterra is not the biggest player in the Chinese market. They are perfectly capable of setting up mega farms themselves as this Russian-Chinese backed farm shows - 100,000 cows http://www.nzherald.co.nz/rotorua-daily-post/rural/news/article.cfm?c_i…

Just read the summary from the shareholders council. It doesn't make good reading even excluding Beingmate.

Revenue up 9% on 11% less volume giving a "Normalised EBIT" 25% down on last year ($458 vs $607). So presumably costs have blown out way more than just the milk price.

Consumer foodstuffs normalised EBIT 38% down.

The bit on Capex and working capital and Debt makes it sound like they're paying now for previous sins, i.e. they propped up last years payout with a bit of accounting. As usual its a bit hard to tell with the info given, for me anyway.

Appreciate your comment red cows, cheers.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.