By Gareth Vaughan

They may have given overall stamps of approval, but the three academics commissioned by the Reserve Bank of New Zealand (RBNZ) to review the analysis and advice underpinning its bank capital review proposals have pointed to improvements they believe could be made.

These include rethinking countercyclical capital buffers, reconsidering removing Tier 2 capital from regulatory capital requirements, and looking at how executive compensation could influence how banks respond to higher bank capital regulatory requirements. (To see detail on what the RBNZ's actually proposing, see the bottom of this article).

Overall the three external experts have, probably not surprisingly, largely provided positive conclusions.

The RBNZ's analysis seems to have been done with care and in an open minded way with impressive thoroughness, says David Miles of Imperial College London.

Ross Levine of the University of California, Berkeley says with a few exceptions the RBNZ conducted a sound analysis of bank regulatory capital requirements in NZ. It employed appropriate data, methods and evidence, considered a broad and proper array of factors, addressed submissions by banks and others, and focused on the NZ-specific features of regulatory capital reform.

Macquarie University's James Cummings says the RBNZ's proposals are based on sensible analysis and advice in the NZ-specific context, with the analytical approaches appropriately capturing the relationship between bank capital and financial system soundness and efficiency.

Executives' incentives and the 'dynamic response' of the economy

Levine argues that, in terms of the RBNZ's analysis of how much capital is enough, there isn't enough focus on executives' incentives or the "dynamic response" of the economy to the proposed capital increases. The RBNZ analysis doesn't consider the potential for ownership structure, executive compensation, or governance to shape the impact of changes in bank regulatory capital requirements on either the stability or efficiency of banking operations, he says.

"Abundant research explains that when executive compensation takes the form of option-based contracts tied to the bank’s return on equity (ROE), this tends to encourage risk-taking relative to situations in which a bank compensates executives with either a simple salary or with a compensation package that penalizes executives for excessive risk-taking, regardless of how those risks materialize."

"Thus, executive compensation could shape the response of banks to higher bank capital regulatory requirements. For example, if executives receive bonuses based on ROE and increasing capital regulations increases bank equity, executives might have stronger incentives to increase risk-taking to generate the previous ROE. This might mean the bank capital regulatory requirements need to be that much higher to create a sufficient cushion against these incentives. Or, it might mean that the RBNZ should modify executive compensation systems so that they do not encourage excessive risk. Bottom-line: The RBNZ’s analyses should consider the potential impact of capital regulatory reform on risk-taking as a function of executive compensation," Levine says.

He also suggests focusing more on incentives might also enhance the analyses of the comparative impact of the proposed capital regulations on banks using Internal Ratings Based, or IRB, capital models and other banks using standardised capital models. Levene argues that complementing capital reforms with reforms of executive compensation schemes would be especially beneficial.

Bank subsidies

He also suggests another key weakness in the RBNZ’s analyses is a lack of focus on what he calls the dynamic effects of changing capital regulations on the economy. The Government, Levine says, subsidises banks in the form of implicit guarantees on bank debts, which currently tilts the financial system in favour of highly-levered banks with excessive risk-taking incentives and away from other financial service providers.

"To the extent that capital regulations reduce this subsidy for banks, the regulations will increase the cost of banking in New Zealand. The overall impact on the economy, therefore, depends on the degree to which new financial institutions can arise and compete with incumbent banks in financing households and firms," says Levine.

"Thus, the RBNZ should evaluate the degree to which legal, regulatory, and tax systems are well-prepared for the emergence and expansion of non-bank forms of finance. The ability of the overall financial system to respond to changing capital requirements and provide financial services to households and firms is relevant for evaluating the impact of capital regulations on the economy."

At their most basic level, distorted incentives can cause banking crises, Levine adds. As well as large shocks, banking crises can also be caused by banks having incentives to take excessive risks due to moral hazard.

"The RBNZ’s analyses should include this additional source of bank instability," says Levine.

However Levine says increasing bank regulatory capital is unlikely to reduce the big banks’ cost of raising deposits and debt by much due to too-big-to-fail expectations by the buyers of those debts that already keep the costs of debt low. And he argues that because bank profits are comparatively high in NZ compared to neighbouring economies, banks are unlikely to move their activities elsewhere due to a change in regulatory capital requirements.

"However, the fact that bank profits are comparatively high also suggests that there are barriers to competition. This is problematic if those barriers limit the dynamic response of New Zealand’s financial system to the regulatory change. The RBNZ could analyze the likely dynamic response of the financial system and the economy in more depth to the proposed capital regulatory changes," says Levine.

Reconsidering countercyclical capital buffers

Levine also urges a reconsideration of the analyses underlying countercyclical capital buffers (CCyBs), advising additional analyses on their practical implementation. RBNZ analysis makes the "unsubstantiated assumption" that policymakers are well aware of where the economy is in terms of business and financial cycles and can adjust CCyBs with sufficient lead time to navigate troubled times.

"For example, the background paper that the RBNZ pointed me to argues, that: 'To be effective, a positive CCB must be implemented at least one year before risks crystallise.' Is there any evidence of such prescience on the part of bank regulators? Is there any evidence that central bankers implement monetary policy actions at least one year before financial system risks emerge?" Asks Levine.

"There is also an implicit assumption that policymakers will not use CCyBs when the economy is not facing banking system distress. I am skeptical. By mistake, CCyBs might be used at the wrong time, or not used at the right time. Furthermore, CCyBs could be abused for political purposes. Moreover, the RBNZ does not make convincing arguments for allowing banks to distribute dividends/bonuses during times of such great distress that authorities allow them to reduce their CCyBs."

'Well-designed Tier 2 capital can enhance incentives and complement Tier 1 capital'

Levine also suggests the RBNZ might want to reconsider removing Tier 2 capital from its regulatory capital requirements.

"If the RBNZ expands its focus to consider capital as both a cushion and an incentive device, Tier 2 capital can be a valuable complement to, not a substitute for, Tier 1 capital. To the extent that holders of Tier 2 capital (a) do not believe that the government will bail them out in times of distress and (b) influence bank decision-making either directly or through the price of Tier 2 capital, Tier 2 capital can dampen risk-taking within banks," says Levine.

"While it is well-established that diffuse shareholders in widely-held companies typically have strong incentives to increase corporate risk after obtaining funds from debtholders, uninsured debtholders have incentives to limit this risk-shifting. Thus, well-designed Tier 2 capital can enhance incentives and complement Tier 1 capital."

Levine also discusses the RBNZ's decision to stop counting contingent debt as regulatory capital, something banks oppose. Contingent debt is debt that the bank would no longer owe, contingent on some “triggering” event, such as a large decline in market values, a material drop in the accounting valuation of assets, or a regulatory decision. The debt would be extinguished by writing off some or all of the debt or by converting the debt into equity.

Ultimately he notes the RBNZ concludes that rather than counting contingent debt as equity because it might act like equity, the RBNZ will simply count equity as equity.

"Given current conditions in New Zealand, I found the arguments in favor of this conclusion prudent and persuasive."

Levine says the RBNZ draws a logical set of recommendations on reforming the definition of regulatory capital.

'Criticism melts away'

Miles says an "over-arching" criticism of the approach taken by the RBNZ "melts away" given the procedure actually followed by the central bank.

"This is the criticism that in starting with an arbitrary assumption on risk appetite - and not undertaking any cost benefit analysis - the validity of the proposals is undermined. In fact the way that the analysis converged on the 1 in 200 year estimate of an acceptable degree of banking risk was by reference to what that implied about the average level of GDP it generated. And in calculating the impact upon average GDP the analysis was undertaking a cost-benefit analysis in which the measure of welfare was average total incomes in New Zealand," says Miles.

"That measure of welfare assumes risk neutrality. So rather than being based on an extreme and arbitrary view of risk which could be seen as being excessively averse to low probability bad outcomes, the analysis actually rests on something closer to risk neutrality."

On contingent debt, Miles says it seems very attractive to banks who argue it's an effective way of meeting capital requirements largely on cost grounds.

"Some banks put the cost of Tier 2 capital and senior bail-in debt at between 3% and 3.6% while the cost of equity capital is put at around 14.5%. The reasons for the apparent enormous difference in cost are something of a mystery...Tax advantages of debt over equity are one reason why in practice there could be an advantage of contingent debt. But the imputation system in New Zealand, and in Australia, means that this source of advantage should be low," says Miles.

"Perhaps the apparent huge cost advantage might reflect unrealistically low perceived chances of conversion triggers being pulled. Perhaps a belief in very low chances of conversion or write-off of contingent debt reflects a rational belief that the authorities would be wary to trigger conversion or write-off of hybrid capital instruments. Neither interpretation is encouraging for the view that such contingent debt can be relied on to maintain stability."

"A key point is that the RBNZ is focused on reducing substantially the probability of insolvency. Contingent debt is a form of loss absorbing capital – it can protect large classes of other debt holders, and the NZ government, from losses should bank insolvency become very likely or inevitable. Whether it is effective in reliably reducing the probability of bank insolvency and allowing banks to remain going concerns is less clear."

He concludes that the proposal to exclude contingent debt, at least initially, has merit.

Cost of equity assumption 'high'

Meanwhile Miles argues that the RBNZ assumption of a cost of equity funding to banks in NZ of slightly above 14% seems high.

"Particularly to the extent that it relies on past returns on the historic cost of bank equity, that is the book equity, rather than its market value. The largest banks that operate in New Zealand trade at a price to book premium so that the return on the market value of equity would be significantly lower than the 14% to 15% figure and much closer to 10%. The 14% figure compares to an assumed annual average cost of debt of 2.3%, generating an equity risk premium of just over 11.5% - a value substantially higher than is considered likely for an overall equity risk premium on all stocks which is closer to 5%, and which is rarely considered to be as high as even 7% or 8%."

In terms of the big four banks Miles notes it would be their Australian parents issuing new equity if this was the preferred route to satisfy higher capital ratios in NZ.

"The case has been made strongly by the Australian banks that shareholders buying new equity that they, and not the NZ subsidiary, issue are unlikely to demand a lower rate of return because the relatively small subsidiary has lower gearing. Whether they would or not is hard to judge; if there was no offset for lower risk it would imply a degree of irrationality or myopia on the part of investors in equity or perhaps a failure of Australia parent to successfully explain that the extra equity would reduce risk in the part of the banking group where the funds would be directed," says Miles.

"And even if there was no reduction in the required return of shareholders that does not prevent the Australian parent taking into account the lower risk in its internal setting of hurdle rates on capital made available to its NZ subsidiary."

In terms of IRB models Miles says they're both difficult to assess and can generate puzzling differences in risk assets for banks that appear to hold similar portfolios. Many regulators share the RBNZ's concern with these, he adds, and their "surprisingly low assessments of risk weighted assets."

"Furthermore, the limited resources of the RBNZ means that understanding how the IRB models have been applied is particularly challenging. In principle it makes sense that banks should use their detailed knowledge of their current and past portfolios – and the credit losses they have experienced – to generate a more accurate assessment of risk than the broader brush treatment under a standardised approach."

And on the CCYB he says it adds complexity to the rules.

"More significantly its effective operation would seem to require that the RBNZ is able to assess where in 'the cycle' the economy sits. This is no mean feat."

'The RBNZ has probably not over-estimated the appropriate level of bank capital'

Furthermore Miles defends the fact the RBNZ's proposals would make NZ banks' regulatory capital requirements amongst the highest in the world.

"That the RBNZ proposals would make banks in NZ better capitalised than in almost any other developed economy – and is in that sense 'out of line' – is in itself not a powerful argument that the proposals go too far. They should be judged in terms of their effects on banks and on the wider economy in NZ – which is what the RBNZ analysis sets out to do. If the answer from a careful analysis is that capital will be different from that in most other countries then so be it; other countries might usefully ask whether the divergences are a reflection of economic differences between NZ and their own country or whether they have not done enough of the sort of analysis done by RBNZ."

Additionally he suggests the RBNZ has probably not over-estimated the appropriate level of bank capital.

"This concerns supervisory philosophy; perhaps strategy is a less pompous term. The RBNZ has adopted a principle of being conservative as regards bank capital to offset possible risks from its light-handed approach to supervision. That is a choice and one partly based on the view that having very large resources devoted to intrusive oversight of banks is not the most efficient road to go down. That is a conclusion that engineers and safety experts often apply when dealing with the design of structures. There is a choice between building bridges many times stronger than you expect them to need to be OR you having large teams of inspectors who pay frequent visits to examine all bridges and monitor flows of traffic over them. It is clear that nearly all countries follow the first strategy. That may be a useful guide for bank supervision, " says Miles.

Three recommendations

For his part, Cummings provides recommendations on three specific issues. These are detailed below.

1. Contractual loss-absorption features

The proposal by the Reserve Bank to remove the contractual loss-absorption features from the definition of non-common equity capital instruments is reasonable, taking account of the uncertainty about the way in which the features can be used to recapitalise unlisted banks that are wholly owned subsidiaries of foreign parent banks. However, the proposal places greater reliance on the powers of a statutory manager to restructure the claims of preference shareholders and subordinated debtholders if a bank’s common equity capital base falls below minimum regulatory requirements. There may be limited sources of new equity available to a statutory manager to support the restructuring of a failed bank.

I recommend that the Reserve Bank continue to monitor the performance of the Basel III loss-absorption features in other countries and assess whether the mechanisms can be adapted to suit New Zealand’s circumstances. The monitoring should take account of the experience of the contractual loss-absorption features in countries with a significant presence of foreign-owned and unlisted banks. The contractual features that incorporate conversion to common equity may become feasible in New Zealand, if one or more of the large banks opts to list its common equity on a public stock exchange.

2. IRB approach to credit risk

Research commissioned by the Bank for International Settlements (2013a; 2016) identifies shortcomings in the modelling practices of IRB banks that contribute to unwarranted variability in the calculation of RWA for credit risk between banks. However, the research literature provides little guidance to prudential regulators about the extent to which internal models provide more accurate estimates of the capital required to support credit portfolios in an economic downturn than the Basel standardised model. This gap in the literature can be addressed using data made available by the proposed dual reporting of RWA using both the IRB and standardised approaches to credit risk.Using the data provided by the banks through the dual reporting process, I recommend that the Reserve Bank investigate the extent to which the RWA amounts calculated using internal models provide a more accurate prediction of unexpected credit losses for IRB banks than those calculated using the standardised model. If the credit risk differentiation properties of the IRB approach cannot be supported empirically following the implementation of dual reporting, the Reserve Bank may wish to reconsider its policy of retaining the IRB approach as part of the capital framework.

If the IRB approach were to be removed from the capital framework, banks could be expected to continue to utilise their proprietary credit risk models, but only to the extent that the models are valuable to the banks for loan pricing and loan portfolio allocation decisions.

3. Impact of the proposals on bank funding costs

The estimates derived by the Reserve Bank of the impact of higher capital requirements on bank funding costs are overstated. The Reserve Bank estimated that a one percentage point increase in the unweighted tier 1 capital ratio from current levels will lead to an increase of 6 basis points in banks’ overall funding costs (Reserve Bank of New Zealand, 2019b:). The calculation by the Reserve Bank assumes that a representative equity risk premium for banks is 11.7 per cent above the cost of debt and that returns to shareholders in the form of dividends and capital gains are taxed at the same rate as interest receipts at the personal level.

However, the four large New Zealand banks can raise additional equity financing either by sourcing the equity through their Australian parent banks or by listing their equity on the New Zealand bourse. Based on data for equity returns and consensus analyst forecasts of earnings per share and dividends per share over the 1993-2017 period, Cummings and Nguyen (2019) estimate that the average equity risk premium for the Australian parent banks is about 6.7 per cent above the bank bill interest rate. This estimate is substantially lower than that used by the Reserve Bank. Furthermore, Dimson, Marsh and Staunton (2019) report that the long-run average equity risk premium for the New Zealand market is not larger than that for the Australian market. A lower equity risk premium will reduce the impact of increased equity financing on bank funding costs.

The cost of increased equity financing will be further reduced to the extent that returns to shareholders in the form of dividends and capital gains are taxed less heavily than interest receipts at the personal level. A cost-effective response of the four large New Zealand banks will be to raise additional equity financing by listing their common shares in New Zealand. The Australian parent banks need not relinquish their controlling stakes in the banks for the listings to occur. The raising of the additional equity financing in the New Zealand market will reduce the risk for the Australian parent banks that they potentially violate limits set by the Australian regulator on exposures to related parties. This response will allow the large New Zealand banks to distribute a substantially greater amount of imputation credits to New Zealand resident taxpayers. The value that investors attribute to the imputation credits for reducing their personal taxation liabilities will reduce the impact of increased equity financing on bank funding costs.

In its formal cost-benefit analysis of the capital proposals, I recommend that the Reserve Bank validate the parameters that it uses to estimate the impact of the proposed higher capital requirements on bank funding costs. The parameters used to capture the values of the equity risk premium and debt tax shield for banks should reflect market-based estimates that are relevant to the New Zealand banking industry.

RBNZ working on suggestions made by its experts

RBNZ Deputy Governor Geoff Bascand says the RBNZ is continuing work on some technical suggestions made by the experts, as well as finalising its decisions.

"The Reserve Bank is continuing its stakeholder outreach programme, which includes general public focus groups and engagement with wider industry groups on the potential costs and benefits. Along with the external expert reports and submissions received, these inputs will help us to make robust, well-calibrated policies and decisions that best represent society’s interests," says Bascand.

"Responses to the reports and the submissions on the fourth consultation paper will be published alongside final decisions, expected in the first week of December 2019. Implementation of any new capital rules is proposed to start from April 2020, with a transition period of a number of years before banks would need to meet the new requirements."

Levine's full report is here, and Cummings' full report is here, and Miles' full report is here.

The terms of reference for the external experts' reports are here, and their biographies are here.

The RBNZ wants to increase bank capital requirements so bank shareholders have a "meaningful stake" in their bank providing a greater incentive to ensure it is well managed, and provides stronger protection for depositors. It notes the economic and social costs of bank failures can be very high and persistent, saying its proposals are designed to make bank failures less frequent.

Announced in December last year the capital proposals would see NZ banks - led by ANZ NZ, ASB, BNZ and Westpac NZ - required to bolster their capital by about $20 billion over a minimum of five years.

For background and detail on the proposals and bank capital in general, and the nuts and bolts of what's proposed, see our three part series here, here and here. Additionally the RBNZ proposes to designate the big four as systemically important banks meaning they'd have capital requirements above and beyond other banks.

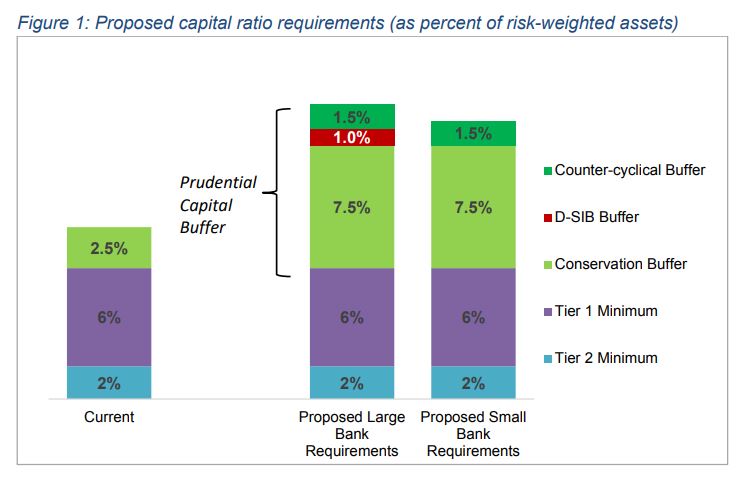

The chart from the RBNZ below demonstrates the proposed changes.

3 Comments

Too much of a read for most.

Might I suggest the best measure and rules to lending growth would a debt to income ratio. This could and should be applied to government, business and households. It’s quite clear we have overshot the mark on all of these fronts.

Using households as an example, debt levels could be regulated to not more than 50% of take home pay. If lenders are found to exceed this, they lose their loan. In reality, debt shouldn’t be more than 30% of take home pay, but I fear in a lot of cases it’s gone way beyond this.

Sustainable debt levels are the answer, rather than those encouraged by banksters.

Maybe would have helped to have a NZ expert opine who could have pointed out that the RBNZ have failed to provide a regulatory impact assessment as required by the RBNZ Act.

David Miles does comment on this by suggesting the impact of a bank failure has been considered and therefore addresses the concern raised by banks. That's assessing the impact of doing nothing... but fails to assess the impact of the proposed capital reforms specifically. Noone doubts the costs of a bank failure.... but there are many ways to manage or minimise the risk... there has been no impact assessment of the current proposal.

I note the experts do acknowledge the use of Tier 2 capital and question the RBNZ's decision to remove it. The RBNZ seem to be of the opinion that investors in Tier 2 don't understand the risks (clearly not the view of the FMA who have no such concern regarding the disclosure statements of those investments).... leaving the question as to who is it that doesn't understand Tier 2?... RBNZ's recent form in this space is not strong.

I will have a read of the opinions... but a little surprised nothing seems to be called out about the reduced focus on banks investing in their internal models.... notably completely at odds with the rest of the global banking supervision line of thinking. By promoting the RBNZ standard model it means the RBNZ's blind spot/s will be the banking system's blind spot/s.

The report is endorsing RBNZ's move to strengthen the capital/reserves of the banks, right ?

On the right track then...Let us see how the Bankers Association responds to this salvo.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.