The jury is out over whether the Reserve Bank (RBNZ) will ease its mortgage lending restrictions when it reveals its biannual review of them on Wednesday.

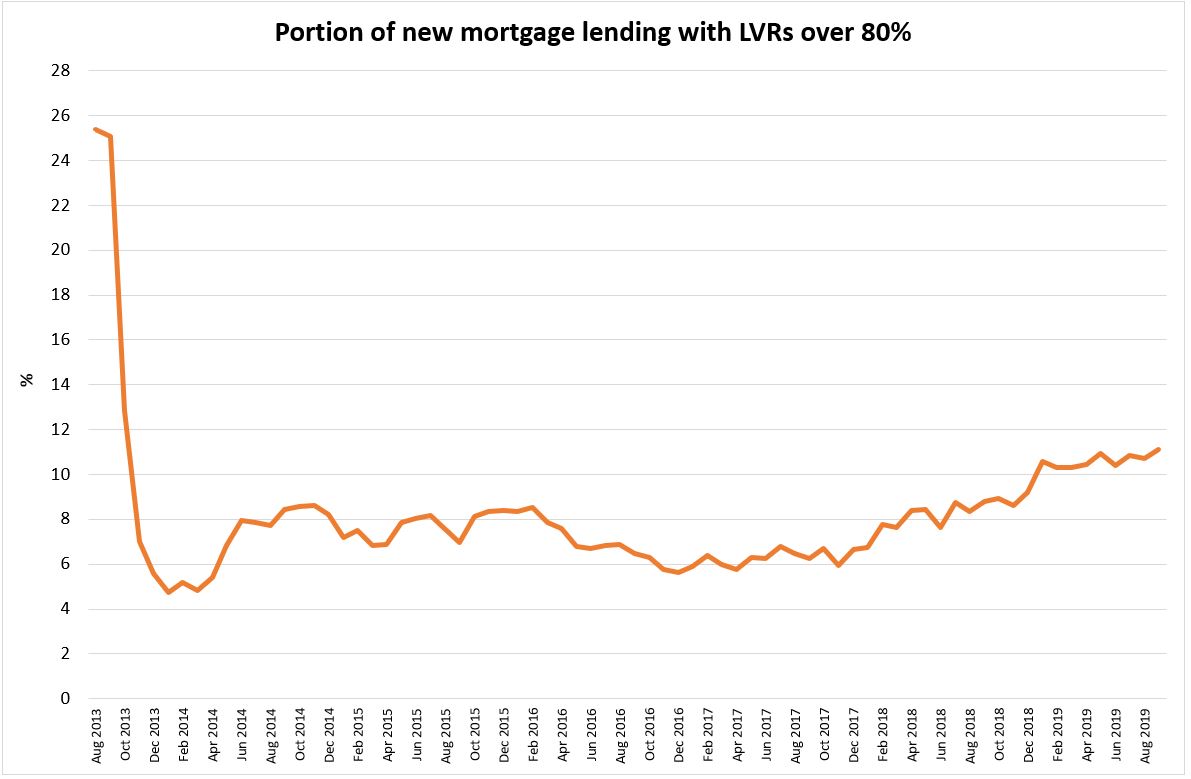

The portion of all (investor and owner-occupier) new mortgage lending going to borrowers with deposits of less than 20% rose in January when the most recent easing of loan-value-ratio (LVR) restrictions kicked in.

It then tracked up a little in the nine months to September (the latest available data). Yet it’s nowhere near the level it was at before LVR restrictions were introduced in 2013.

Looking at new lending to owner-occupiers, the portion that went to borrowers with deposits of less than 20% has hovered around 12% to 13% this year. This is below the RBNZ’s “speed limit” of 20%, indicating banks aren’t lending to as many high LVR borrowers as they’re allowed to.

So, with banks already taking a more risk adverse approach than required by the RBNZ, the question is, will loosening LVRs have any impact at all?

Cave Financial Authorised Financial Adviser, Brett Sargent, believes it wouldn’t.

He saw a fair bit of high LVR lending over March, April and May, but said banks have been increasingly risk adverse since then, making it more difficult for borrowers with 10% deposits to get approval.

Both ANZ chief economist, Sharon Zollner, and CoreLogic’s head of research, Nick Goodall, believed banks’ own mortgage serviceability requirements, rather than LVR restrictions, were constraining their lending.

LVR restrictions aren’t all that binding at the moment, Zollner said.

Goodall said an uptick in house prices was affecting affordability. “Lower interest rates have helped, but otherwise we do think things are generally tighter.”

Goodall said he’d joked with RBNZ staff that the only thing a loosening of LVR restrictions would do is give them some good public relations; make them look like the “good guys” ahead of them on December 5 announcing the outcome of their capital review, which will likely require banks to hold much more capital.

Zollner maintained banks’ prudence when it comes to debt serviceability is in part a result of Australia’s financial services royal commission putting the spotlight on their conduct and culture.

She believed banks’ consciousness around “doing right by their customers” had had more of an effect on their risk appetites than looming capital rule changes.

John Bolton - the founder of Squirrel, which provides mortgage broking services - had the same view around serviceability being the issue.

He believed the current restrictions were working well.

He said the housing market, particularly in Auckland, was showing signs of life, meaning there could be more lending at higher debt-to-income ratios.

“People can only stay out of the market for so long,” he said.

Goodall had thought there was a 70% to 80% chance of the RBNZ loosening LVR restrictions, but shifted his view to 50% to 60%.

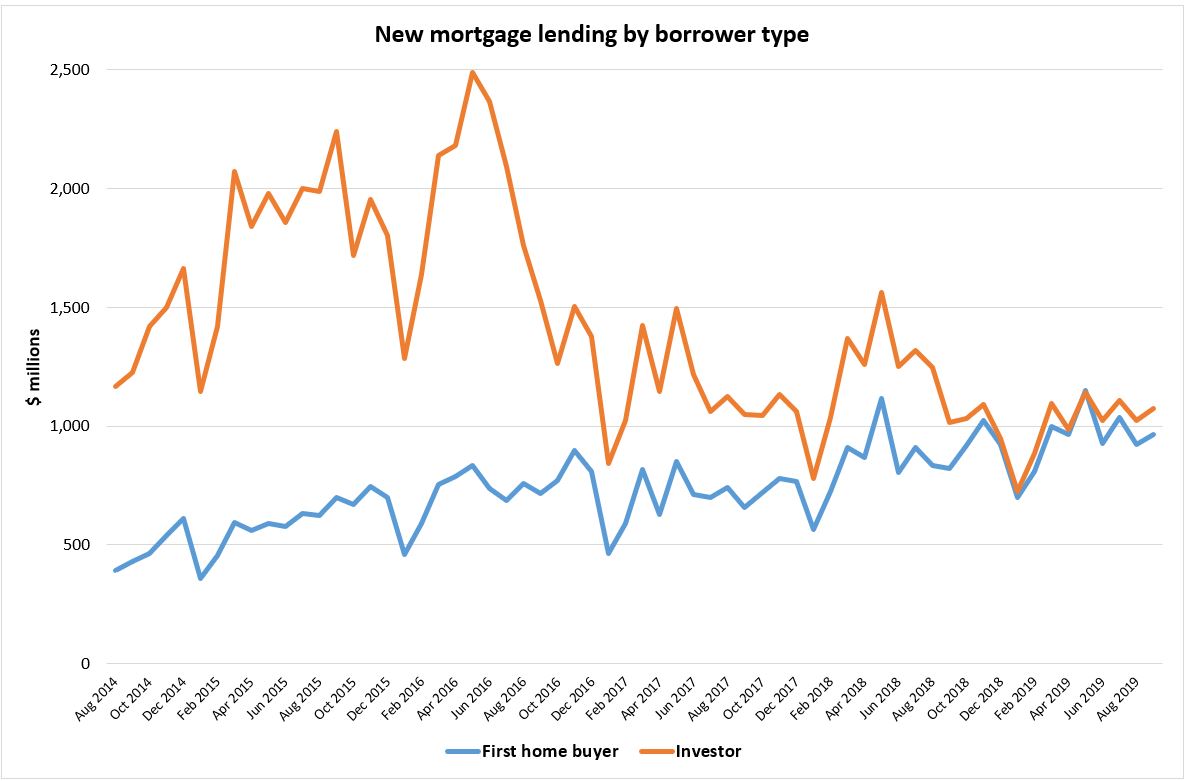

He’d noticed an increase in investor borrowing in recent months, as well as a small uptick in high debt-to-income lending.

Zollner believed the RBNZ wouldn’t loosen LVR restrictions, even though she said after the November 13 Official Cash Rate review that keeping the rate at 1% would increase the likelihood of an easing.

“The housing market’s showing pretty clear signs of responding to the lower mortgage rates… housing affordability is stretched,” she said.

Movements in the housing market stood out to Westpac senior economist, Michael Gordon.

Unlike the others, he believed easing LVR restrictions would prompt banks to lend more to borrowers with low deposits.

“The RBNZ must be satisfied that loosening the LVRs won’t lead to a resurgence in the housing market and hence in financial stability risks,” he said.

“We think that this will be the sticking point. The housing market is already accelerating on the back of a steep fall in mortgage rates and the removal of the prospect of a capital gains tax. House prices are up by 3.2% in just the last three months, which is about 13% annualised

“Loosening the LVRs would add even more fuel to the fire.”

Median price - REINZ

Select chart tabs

Currently banks are allowed to make no more than 20% of their residential mortgage lending to high-LVR (less than 20% deposit) borrowers who are owner occupiers, and no more than 5% of residential mortgage lending to high-LVR (less than 30% deposit) borrowers who are investors.

The Government is considering whether to give the RBNZ the ability to restrict bank lending with a debt-to-income tool. The matter is up for discussion as the part of the Reserve Bank Act review.

The RBNZ has always wanted the tool, but its head of financial system policy and analysis, Toby Fiennes, in August said that even if it had it, “we would be very unlikely to be using it right now".

78 Comments

" the only thing a loosening of LVR restrictions would do is give (the RBNZ) some good public relations; make them look like the “good guys”

I'm glad it was a joke because it's not the RBNZ's job to look like the Good Guys; in fact quite the opposite.

Taking the proverbial punchbowl away from the party isn't easy or popular, but THAT is the RBNZ's job, and albeit too late, now is the time to continue pulling it off the table.

People have to reach a point at which the pain of staying the same is worse than the pain of making a change. Only then will they take the hard steps. ( via Mauldin)

Yes, God forbid that the RBNZ act to prevent a disaster from happening, instead of waiting until after the fact and attempting to clean up the mess. Making housing more unaffordable through higher prices, and saddling people who cant really afford to borrow with eye watering amounts of debt, does not make you the "good guy".

There will be no changes for investors, with the probability of them actually increasing the lvr for investors..

In reality, with the number of houses being built and the government house building program, there is less reliance on investors...

... in reality we are still building fewer houses than we did way way back in the 1970's ... but , we are flooding the country with new immigrants at a rate not seen since the 1800's . ..

I would suggest before the RBNZ decides to loosen mortgage LVR restrictions, putting borrowers and bank lenders at high risk. I'd suggest they look at the commonalities that cause the Global Financial Crisis.

There were four main features to the GFC that the RBNZ should consider:-

1) Asset price increases that turned out to be unsustainable. (Check we're already there)!

2) Credit booms that led to excessive debt burdens. (Check we're already there)!

3) Build-up of marginal loans and systemic risk. (Do you really want to allow soft lending)?

4) The failure of regulation and supervision to keep up with and get ahead of the crisis when it erupted. (Who is going to clean up the mess)?

IMF Lessons and Policy Implications from the Global Financial Crisis

https://www.imf.org/external/pubs/ft/wp/2010/wp1044.pdf

RBNZ knows and admit that low interest rate is a blunt knife / tool and may have unintended consequence (House price rise and which has started and happening).

If RBNZ is serious and not want the house price to rise again or control, should it not be using other tools like LVR to control the unintended consequence (If boosting house price is really unintended) so the least theycan do is not touch LVR restriiction.

Irony is that only ecenomy in NZ is housing ponzi. So like it or not have to support it to delay the bust as much as possible (Can delyay but not avoid) and who cares if debt level goes beyond.

If LVR is reduced it is bound to effect the sentiment giving another push to housing ponzi and will know soon what RBNZ and governments wants - intention will be clear and cannot hide behind unintended consequence.

RBNZ knows and admit that low interest rate is a blunt knife / tool and may have unintended consequence (House price rise and which has started and happening).

RBNZ forever chasing trickle down economics.

a Wealth effect or wealth illusion? The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects. Link

If RBNZ is serious and not want the house price to rise again or control, should it not be using other tools like LVR to control the unintended consequence (If boosting house price is really unintended) so the least theycan do is not touch LVR restriiction.

Bank shareholders self regulate credit extension:

Since money – and this includes bank money – is so useful, there is always some demand for it by someone. As a result, the short side is always the supply of money and credit. Banks ration credit even at the best of times in order to ensure that borrowers with sensible investment projects stay among the loan applicants – if rates are raised to equilibrate demand and supply, the resulting interest rate would be so high that only speculative projects would remain and banks’ loan portfolios would be too risky. Link

Some are so convinced in the promises of investor school some would just go an another borrowing spree which really shows why we need debt to income levels for specuvestors. The crux is whether the banks would actually loan more money to specudebtors or not. With increased bank capital likely to arrive it would be interesting to see what the banks would do.

Increased money supply needs be in step with increased GDP.

More better jobs, increasing incomes for those jobs together increasing good GDP and per capita GDP.

That would be my key GDP.

And looking to PMs department to bring together those "enabling" policies.

....... all the provinces show a steadily rising unaffordability of house prices until ... until you click " West Coast " .... man , that chart is so bizarre ... absolutely schizophrenic....

No mental health condition there my friend its just the west coast proving my long standing claim that it is literally stuck in the last century ( based on the regions stubborn refusal to move beyond coal mining and take up new tech like coding for example) the house prices are certainly that way too. Perhaps as the UFBB comes on line in that area it will enable a rejuvination as modern skillsets relocate there to take advantage of its low cost houses and natural beauty. Its happened in areas like Cornwall in the UK and in the USA, Vermont and Michigan too...with stunning results.

... don't get me wrong , I love holidays on the coast ... went to an awesome Sunday market at Fox River recently ...

But , the coast does need to shake off its reliance on mining , forestry and dairying ....

What's your unhappy experience of there.

Spent much time there when it rains?

The Coasters like all New Zealanders are able to use the assets & resources located locally to provide jobs and rising incomes.

You can imagine how coasters feel about current government policy & proposals taking away opportunity for jobs and income. It hurts more because they are the history of the Labour party. The Labour party is theirs.

Banks won't lend to your elevated levels when the path to jobs and rising incomes disappears.

Labour has abandoned its roots ... its formation was West Coastian ... Helen Clarke banned their sustainable logging ... Damian O'Conner is berating their dairy farmers for not applauding Labours onerous new emissions and water pollution laws .. .

... Labour knows , they can kick coasters from pillar to post , but in 2020 ... they'll still vote Labour !

Yep, loyalty,

Gummy, here is the assurance to delight you prior to tucking into Sunday dinner.

The science is with you.

https://chriskresser.com/debunking-the-game-changers-joe-rogan/

.. cheers , Henry .. I got some way into that interview ... very informative ... the stuff about the vegan diet of gladiators was amazing ... fattening them up to survive cuts , rather than being killed off too soon ..

The new religion of veganism , and the lies around its promotion ... are right down their with climate change and the anti CO2 brigade ...

. . witness the vegan couple in the US charged with manslaughter after their 18 month old son died ... he weighed just 7 kgs ....

Yes.

How does the awareness and value of rotational grazing, it's what makes us different and great, get communicated to the PM's department?

Our existing systems are carbon sequestering, soil regenerative and soil improving.

1. Grass fed dairy, grass fed red meat, poultry are nutrient dense superfoods. She/we need get behind it. I see she/they are legislating for overseas farming systems, massive monoculture plant production. It's not us. She/we gotta stop that. We gotta lift production of our great food.

2. I would advise her to hangout less with Hollywood celebs & woke media. She/we being used. The tourism argument is misdirection.

3. She should be less like AOC, AOC is 28, like AOC she needs ditch the rag tag gang. Greens & Winnie, they gotta go. She has gotta go back to labour roots, enable jobs, enable rising incomes, look after our own.

Interestingly, with its highly volcanic/tectonic terrain the west coast is thought to be riddled with precious high value rare metals, I'd have no issue with those being mined if it was done in a manner that wasn't hugely damaging.

GBH,

your comments are funny, until their not-just silly. The anti CO2 brigade. Just what does that mean? Nobody is 'anti CO2'-it's essential for life as we know it. The problem arises when THERE IS TOO MUCH CO2, as is happening now. I would refer you to the Keeling Curve as evidence. Their findings are corroborated right here in NZ at Baring Head. It is simple science that as CO2 builds up in the atmosphere, our temperature will get warmer.

I am not a vegan and never will be,nor am I vegetarian, but like many I eat less meat and thoroughly enjoy cooking and eating vegetables. It is my view that many NZ farmers seriously underestimate the growth of plant based meat substitutes.

"Loosening the LVRs would add even more fuel to the fire."

Just the sort of news the doomie gloomies do not want ... it will only make them more doomie gloomie.

Yeah, Ok Boomer. Just so you can keep your false economy ponzi scheme going.

... if only some of those hundreds of $ billions that've gone into house mortgages ... inflating the property bubble .... had've gone into productive endeavours instead : food processing , medical research , hi tech , education , genetic studies ( GM ) , alternative energies , waste management .. we'd have diversified and strengthened our economy ... created jobs and profits ...

And that's from a " BB " ...

The lynch mob has again got wrong end of stick. I DID NOT SAY THAT I AGREE WITH LOOSENING JUST THAT DOOMIE GLOOMIES WOULD BE PACKING ANOTHER SAD. There now is that clear enough CJ? A couple of weeks ago I 'told' the rbnz I did not agree to a drop in the ocr level. they took note of that and followed my advice. And how would you know if I am a boomer or not

.. take it easy ... some of us do read and digest your posts as you mean them ...

Its warm ... relaxing on a lazy Sunday ... kick back with the Gummster and have a cool beer . . Gummy beer ... while the crickets on the telly ... life is good , friend . . Very very good ...

. . Ooooh look... one of the English cricketers is on 88 ... about to bring up his hundred ... cool ... its their demon fast bowler Archer .. 0/88 ... ah haaaa de haaaa ....

I love the Kiwi summer ....

Ksh glug glug.... enjoy the cricket GBH am off to Auckland myself

8 Wired .. Liberty .. Galbraiths ... Urbanaut ... Shakespeare ... Hallertau .... no shortage of awesome craft brewers there ... enjoy ! ...

I would expect static the least more into increase the OCR, until recently being exposed to a training method of either re-booting the comatose induce body & the quick antibody nuke process, in order to administer a extremely dangerous drugs. Both are in the cutting edge/for different illness. May be the same principal can be applied? so although a bit reluctant, I would now rather choose the removal of LVR, put OCR lower & leave the Banks alone, they're very robust on their market/self regulatory lending practices. The housing price elevation, is just a side effect.

A key theme of the article is that even if LVRs are loosened tightening in other areas will balance that out

The housing bubble is now so damaged that any patch work will not be effective in preventing the leak

... leaky homes !

We only need loosening of LVRs if we need lax lending by the banks.

The existing LVR limits are already more loose than they should be, even at existing limits the ability of investors and homeowners to leverage their equity keep homes unaffordable for FHBs.

Its not so much the LVR's keeping investors in check. Lending to investors is not loose, all the main banks are stress testing investors at 7.25%. Many investors have good equity that far exceeds LVR requirements but it is the ability to service debt at 7.25% that is holding them back

"all the main banks are stress testing investors at 7.25%."

Heard that ANZ is now stress testing at 6.65%.

Lvr loosening may create a minor boost, but dsr is a stronger factor now. Royal commish in oz will continue to temper nz lending based on dsrs.

Correct

Westpac, bankers to NZ Givernment

https://www.smh.com.au/business/banking-and-finance/devil-in-the-detail…

https://www.smh.com.au/business/banking-and-finance/westpac-s-23m-breac…-

"Would an easing of mortgage lending restrictions set the housing market alight?"

Why ask this question as everyone knows that LVR is used to control housing market. LVR was increased to control the housing speculation/price rise so is obvious that if RBNZ is reducing the LVR it is boost the housing market which is already only fire, once again.

Also though asking the question : Would an easing of mortgage lending restrictions set the housing market alight? - the writer/experts knows the answere as anyone and everyone knows How, Why and When the LVR tool is used.

This is definitely not to help FHB - as price rise and increase in debt as a result of house rise is not in favour of FHB BUT YES this opportunity of price rise, will help so called investor/speculator to offload their investment that they are suck since last 2 or 3 years.

Judge whom will lowering LVR help, first home buyers or speculators ???

Why the hell would you want to set the housing market alight? Have we not got enough problems with housing affordability already? I would have thought that the responsible thing to want would be a careful deflating of the housing bubble to sane and affordable prices. The question suggests that a large proportion of the population has come to expect house prices to sky rocket ad infinitum. In other words a colossal bubble started by the previous Labour government and perpetuated by every government since. It has gone on for so long now that it has become situation normal for a large part of the lives of many younger people so maybe the question is not so surprising.

Labour initially bannd foreign buyer as was forced by election promise pressure but soon realized that only feel good ecenomy in NZ was and is housing so let the housing ponzi continue so now will now ......

We gotta check assumptions!

The only feel good economy in NZ was and is housing. NOT!

This is terrible thinking and NOT true!

It does not have to be this way!

Henry_tull you are 100% correct but tell this to politicans and all so called experts, media, real estate associations and people who are benefiting by this housing ponzi and have strong and powerful lobby to influence.

NZ democracy : To the Rich, By the Rich and For the Rich. Media fourth pillar of democracy too is run and managed by people with vested interest who believes National's John key policy that housing crisis/issue a Good issue as most benefit if this ponzi continues.

It is hard to believe that they that facile and stupid; however the evidence suggests otherwise.

With Interest rates falling, LVR as one of the tool to control house price becomes more important than before and if RBNZ do not want to repeat rise in house price, it is important to increase the LVR(As house price in Auckland has started to rise and debt level rising) and if cannot increase best to leave it untouched so where does the question of losening it arises in current environment. Definitely RBNZ could not be that stupid unless they want to add fuel to fire.

I have no problem with anyone setting anything alight IF they suffer the consequence of that action if it fails; be that the RBNZ or commercial bankers or any other risk taker - but they don't! Fire of any sort - especially economic fire of an untested nature - can be both good and bad and should be treated with caution and consequences should apply to failure.

“The money placed in the custody of the banker is to all intents and purposes, the money of the banker, to do with it as he pleases. He is guilty of no breach of trust in employing it. He is not answerable to the (lender) if he puts it into jeopardy....Groupthink quickly takes bankers from being greedy for more business to fearful of it. Initially, banks stop offering circulating credit, the facility that lubricates business activity. But former lending decisions begin to be exposed as bad when the credit tap is turned off and investments in foreign lands begin to reflect their true risks. Lending in the interbank market dries up for the banks with poor or marginal reputations, and banks begin to report losses. Greed turns rapidly to fear....With frightening rapidity, all the hope and hype created by monetary expansion is destroyed by its contraction.

https://www.goldmoney.com/research/goldmoney-insights/150-years-of-bank…

BW consequence will be worse for FHB who are buying now by borrowing more because of the fear of missing out and no politicians or so so called experts / media cares about them and RBNZ or politicans or anyone who cares.

It is this attitude that is giving rise to Trumpism.

Family and friends care dont they, not media

Talking about FOMO. Stuff 27/2/2009 "Financial commentator Bernard Hickey, from interest.co.nz, says prices will fall 30% by the end of 2009. He says properties that are difficult to sell or need to be sold in a hurry are already going for 15-20% less than their on-paper value. "The worst is yet to come. I think 2009 will be a horrible year for house prices because credit is drying up and the economy is going into an extended and deep depression".

The FHB for a affordability measures is 25~29 years old. The REINZ median house price in NZ was $330,000 when that article was written. Now those potential FHB are 35~39 years old and faced with a median house price of $607,500. It was $537,000 when Jacinda promised homes for all so 13% more price appreciation. At some point you either take the pain or rent for life.

If the property ponzi keeps going up we will just end up with people earning 6 figures eligible for accommodation supplements..

Correct

Eventually we will once inflation gets us to the point where a 6 figure income is low-paid, but that should be 30+ years away.

And i'm not usre why you are so sanguine about it, should it get to that point, the govt will be paying out 100s of millions more in accommodation supplements, and there is no point giving with one hand and taxing the same people with the other, so the govt will start looking for new sources of tax, and guess who is going to be in the firing line? It won't be wage and salary earners...

Nationwide, more than 290,000 people are now receiving an accommodation supplement.

The government is having to pay $27.9mn / week in housing supplements ($1.450 billion per year). That money is going to landlords.

https://www.tvnz.co.nz/one-news/new-zealand/accommodation-supplements-n…

“At some point you either take the pain or rent for life“

No prizes for guessing which camp you are in. Pre-approval isn’t worth the paper it is written on if you never use it.

I thought you had no respect for me... why are you bothering to try to talk to me? We'd both be happier if you just scrolled on past any of my posts, as I will do for yours.

Hey ex expat. Bernard was the first DGM, a title he wears proudly I believe. I'm glad to say that most fhb did not listen to him just as they have not listened to those DGM who came later :) Those 35 to 39 yo will be much deeper in their family life by now. We all know that when the kids come it becomes a monumental task due to loss of one income as well as greatly increased expenses.

Many people are unaware, that outcome was an unintended consequence of financial support for the banks by the government in 2009.

How many people expected the government to provide financial support for the banks to access liquidity in 2009?

In free markets, banks are left to market forces, and government support should not be expected. In the US, government support for banks came only after credit markets froze, and a number of banks had failed. When government support came, it was in the form of equity injection, not in the form of guarantee to access liquidity.

In the UK, a bank was unable to access liquidity in capital markets. The government did not step in to provide a liquidity guarantee for the bank. There was a limit on the amount of liquidity by the Bank of England. As a result, the bank subsequently experienced a depositor run (reportedly, the first such run in over 140 years), and was nationalised by the government. That was the case of Northern Rock.

Will the NZ government provide financial support in the same form if banks in NZ need liquidity?

30 years to pay back debt is multiplied by the numbers involved and the leverage required.

That we have multiple Banks and no encouragement to Save a dollar is compounded by the theft of excessive taxes and the Key figures who shave a large proportion of Bank profits and fiddling the books.

That suckers are required to get into more and more debt, by lowering rates since I was a lad is just compounding what is supposed to be an inflationary pressure to pump up the desired effect.

When is enuff enuff, when it all comes to a grinding halt, when I and many others have had enuff as a sensible consumer.

Ticky tacky boxes are not the answer, had enuff of them in the past. Mortgages are the long term debt, filling them with Chinese and other crap is now the biggest war on earth, financially.

The RBNZ knee capped locals at a time when Auckland was hyperinflating due to the influx of Chinese foreign capital, and all that welcomed at the time by John Key. The Auckland upper quartile has stalled since 2017 because the foreign capital has gone and now the banks and RBNZ are looking to the domestic market to support the nose bleed prices.

No political parties are different at least National party was open about supporting their friends and supporters from China and rich kiwi unlike Labour who says that feel for average Kiwi but behave like national and just to prove that are for poor go with dole which too does not help hard working average Kiwi.

National supported housing crisis as good crisis openly and now Labour realizes that housing crisis is a Good crisis to have a rock star Ecenomy (Only difference is that are not open about it).

Think you'll find there was no housing crisis under the National Party (at least according to them). Distinctly recall them denying a crisis until after the election when Simon put his foot in his mouth and admitted there was one

Yes, yes & yes - loosen up, reduce the OCR further & cancel/delay that 5 Dec.? announcement for the Banks.

We need to keep increasing the beat tunes, keep more borrowing to spend against the loan. The only way!

WHEN Stats NZ finally gets figs out for owner occupation in Auckland we will know what a wonderful affordable market we have.

What does "set market alight " mean?

Do we (who are "we") want 20% pa price rises?

Who gains from this, unless you want existing equity owners to regard and treat their house as an ATM.

Some members of electorate want lower prices and others want higher prices. One is generally under 35 and other is generally over 60 and owns a house or many, other than one they live in.

Potential for parents over 65 to lend to offspring is impacted by falling deposit rates.

Notice that interest rates on deposits are returns on money EARNED.

Lower interest rates on mortgages are simply reducing interest debt owed on speculative asset.

If the objectivists is to raise demand, as most central banks seem to want government to do now , now that they are to of ammo, then that means more money in wages to those on lower incomes. RATHER than, here boys and girls, have some more debt for 40 year mortgage. is this really all we have as an political economic debate?

banks telling government to spend more when they told them for 10 years to spend less because supposedly they caused the GFC by over spending. Utter idiocy. Meanwhile government dithers over investment at lowest borrowing rate in history when ACC is sitting on $40b and Superfund on $50b that need safe domestic investment vehicles. All so Labour doesn't upset the "markets"

"then that means more money in wages to those on lower incomes"

Yep, leading to a bit of CPI inflation.

Im sorry, I thought I had been reading that the gov was trying to dampen down house prices for the last 5 years...now they want to increase them!!!!!!!!!!..and I thought trump had the monopoly on flip flopping...

I have no problem replacing LVR with DTI but they will never do that because then many many people could not load up on debt.

and as we now know since the GFC debt makes the world go around

and now we have a phase GOOD debt,

in my day all debt was bad and the way to get ahead was positive investing and positive cashflow

I first learnt the phrase Good Debt vs Bad Debt donkeys years ago sharetrader. Where have you been? I agree with your other comments.

Just out of interest, what is your definition of "good" debt?

It is not MY definition CN so I'm sure you can look it up yourself.

Some people have different interpretations of the same phrase. I have seen different definitions - some from property mentors, which is the reason that many property investors have been willing to take on large amounts of "good debt".

Just to clarify, I was interested in understanding your understanding of the phrase "good debt" to see if I understood your definition correctly.

The RBNZ will drop LVRs as compensation for the increased bank capital requirements. Banks will want to stop lending to "risky" farmers and businesses, and will instead pump everything they've got into the "not risky" residential mortgage market. Aided and abetted by this Govt whose new "Kiwibuild reset" housing policies are to allow FHB to only have a 5% deposit and to increase the number of people eligible to exhaust their Kiwisaver accounts.

Is this what RBNZ wants. All money going to passive assets

This passive investment is the sole indicator of Rock Star NZ Economy

According to one Aussie Bank verbally today, they are not lending on Commercial Property anymore as they need to address their core retained balances and there is no other way.....actually possible.

Aussies usually know where their bread is buttered, or they will be toast. Not so bright at laundrring ..though.

Hong Kong has similarities

https://www.scmp.com/comment/opinion/article/3034626/restore-peace-hong…

A market that's heating up with more demand is the last thing this country needs. I can tell you also the residential tenancy changes banning 90 day terminations will FUK this market even more. No more old rentals that housed people and were relatively cheap. And those people desperate to get a rental due to past problems will be shut out completely imo as no one will take a risk. You may disagree. You may respond to the contrary and tell me I'm wrong. This stupid govt with it's stupid provocative approach has got it wrong.

I think the message from the government is that the people will have to step up. Cheap housing is no longer an option and you are going to have to up skill and prove you are a valuable citizen if you want the only rental accommodation that is available, premium rental accommodation. It's pretty harsh on these folk but you have to admire the government's brutal determination to raise standards.

It's great having premium housing :) problem is there is a cost for both sides. We just re did our 60s flat, instead of reletting while the prev tenant was still in place we had to wait then do up (over 2 months) and now wait another 3 weeks for new tenant giving notice. Unit looks brand new almost.

I wrote a Haiku for the Auckland housing market. I call it "Ode to 2016"

Bricks and mortar shimmer as though golden, and glistening with euphoria.

I watched a young woman sobbing in the Barfoot & Thompson auction room.

Her dreams and aspirations vanished, as have I from this place.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.