Credit rating agency S&P Global Ratings says New Zealand's major banks should be able to absorb rising bad debts without posing significant risks to their creditworthiness.

In a report entitled New Zealand banks buckle down for lockdown, S&P says it doesn't expect the COVID-19 pandemic to weigh heavily on bank credit ratings, given significant support measures from the Government and Reserve Bank helping to smooth economic shocks. Additionally S&P credit analysts Lisa Barrett and Nico DeLange say the major NZ banks - ANZ NZ, ASB, BNZ and Westpac NZ - would be likely to receive timely financial support from their Australian parents, if they needed it.

S&P has AA- credit ratings on ANZ NZ, ASB, BNZ and Westpac NZ, equalised with their Aussie parents. The four hold nearly 90% of NZ banking system assets. Credit rating downgrades typically increase the rated entity's borrowing costs.

"We estimate that COVID-19 will contribute to the New Zealand banks' credit losses escalating in 2020 from historic lows of about 10 basis points in 2019. Nevertheless, in our view the credit losses should remain low compared with international peers as well as our expected long-term averages," Barrett and DeLange say.

"The banks' profitability should remain adequate to absorb increased credit losses notwithstanding headwinds from low interest rates and flat demand for credit. We believe that the banks retain headroom in their earnings to absorb a rise in credit losses even beyond our expectations, without posing significant risks to their creditworthiness."

As previously reported by interest.co.nz, the big four banks had non-performing loan ratios, a combination of impaired loans and loans at least 90 days past due, of between 0.3% and 0.9% in the December quarter.

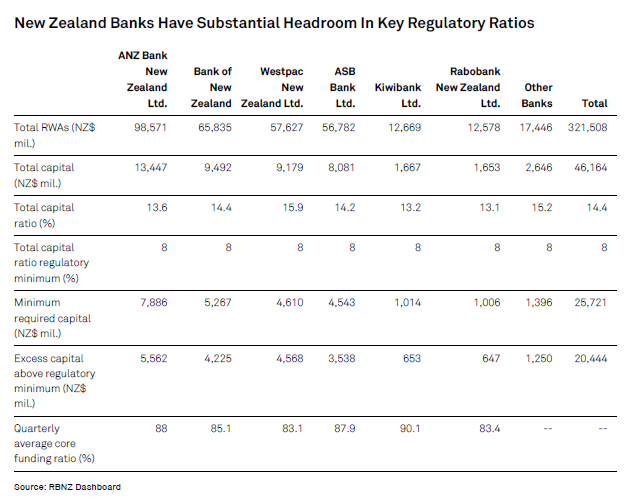

Barrett and DeLange also point out the banks have "substantial headroom" in their key regulatory ratios.

"New Zealand banks have substantial headroom in key prudential ratios, in our view. As of Dec. 31, 2019, the banking system had $26 billion above the minimum required capital. The core funding ratio for the four major banks also averaged 86% as of Dec. 31, 2019, well ahead of the minimum requirement that was lowered to 50%."

"Even though credit losses may escalate we think the banks' profitability should remain adequate to absorb increased credit losses, notwithstanding headwinds from low interest rates," Barrett and DeLange say.

S&P says NZ residential mortgage lending growth is likely to be flat to slightly negative over the next year.

"We foresee downside pressure on property prices for the remainder of the year given the lockdown, rising unemployment, depressed consumer and business sentiment, and the wealth effect; this is despite low interest rates. That said, we believe the downturn will be short lived and expect a rebound in early 2021."

"We believe that the New Zealand major banks, as material wholly owned integral subsidiaries of their Australian parents, the ratings on which are linked to the Australian sovereign, are highly likely to receive timely financial support from their parents, if needed," say Barrett and DeLange.

"We believe that even though the fiscal and monetary stimulus initiatives may increase pressure on the New Zealand sovereign rating, this will not have a direct impact on the New Zealand major bank ratings, and would be supportive to the credit profile of the domestic banks."

New Zealand has an AA foreign currency rating with a positive outlook from S&P, and an AA+ domestic currency rating. (See more on NZ sovereign credit ratings here and see credit ratings explained here).

S&P acknowledges there's a high degree of uncertainty about the rate of spread and peak of COVID-19. It's working off the assumption the pandemic will peak about midyear.

"We believe the measures adopted to contain COVID-19 have pushed the global economy into recession. As the situation evolves, we will update our assumptions and estimates accordingly."

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

12 Comments

S&P Global Ratings says NZ's big four banks have substantial headroom as they buckle in for a COVID-19 driven increase in bad debts

What is the RBNZ up to then?

Precisely. If the financial markets needed no intervention, why do we need to intervene?

The why is obvious - Reserve Bank mantra = "PROPERTY PRICES MUST NOT DROP!" In fact it's more like "PROPERTY MARKET MUST KEEP GOING UP!"

“we believe the downturn will be short lived and expect a rebound in early 2021”

Quite a big assumption there.

Let's hope they are right.

Time to watch the Big Short again.

Ratings agencies advice and $7 would get you a coffee anywhere in Auckland last month.

Funny - my first thought when I saw this headline was 'The Big Short'.

Ratings agencies are a joke. They will pretend everything is OK until it's too late.

before long the impaired loans will appear,they will be on the books at P2P entities,assorted finance cos and credit unions.the new virus will create the new poor and they will have to surrender their hardwon shiny new cars,smart tvs and fridge-freezers.

It would be morally unjustifiable ,if the dividend is maintained and passed on to benefit shareholders, given the extraordinary assistance provided to these organisations.

Do they get invited to the ANZ xmas function?

Bit irrelevant stating they have headroom, because it takes time for the pain to bite mortgage holders and actually hit the banks balance sheets

I guess we'll find out how much in the months to come...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.