KPMG's annual Financial Institutions Performance Survey (FIPS) highlights another year of record profit from New Zealand's banks just days before the Commerce Commission is due to release the draft report in its market study into personal banking services.

According to the FIPS, annual net profit after tax across NZ banks rose $20.2 million, or 0.28%, to $7.21 billion having burst through the $7 billion barrier for the first time last year following a $1.06 billion rise. The 37th annual FIPS covers the 12 months between October 1, 2022 and September 30, 2023.

The profit rise comes with net interest income up $2.22 billion, or 16.89%, to $15.34 billion. Much of this increase was offset, however, with non-interest income down $1.09 billion, or 33.07%, to $2.21 billion, operating expenses including amortisation rising $0.56 billion, or 8.85%, to $6.91 billion, and impaired asset expense up $0.49 billion, or 339.30%, to $0.64 billion.

The banks' combined net interest margin, measuring the difference between what banks borrow money at through the likes of deposits and what they lend it out at, rose 24 basis points to 2.34%.

Market study & select committee probe

The Commerce Commission is due to issue the draft report in its market study on retail banking competition focusing on deposit accounts and home loans, on March 21.

The Coalition Government's also promising a select committee banking inquiry, which Commerce and Consumer Affairs Minister Andrew Bayly says could look at how to encourage banks to lend more to "productive" sectors of the economy rather than having such a big focus on "unproductive" housing lending.

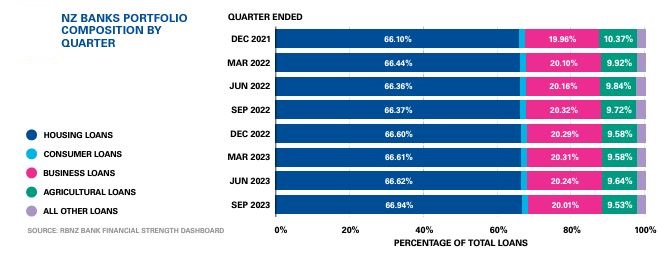

The FIPS shows housing lending continues to grow as a percentage of total NZ bank lending, reaching 69.94% as of the end of September 2023. (See chart lower down this article). ANZ, NZ's biggest bank, has 72% of its total lending in the housing sector. (Also see our Of Interest Podcast episode on why banks love housing so much here).

Annual profit performance across the big four banks was mixed, with ASB and BNZ recording increases, and ANZ and Westpac decreases. ASB's rose $164 million, or 11.29%, to $1.617 billion, and BNZ's rose $95 million, or 6.72%, to $1.509 billion. ANZ's dropped $128 million, or 5.57%, to $2.171 billion, and Westpac's fell $114 million, or 8.78%, to $1.184 billion.

Net interest margins & funding costs rise

In terns of net interest margins, ASB's rose 36 basis points to 2.48%, ANZ's rose 21 basis points to 2.35%, Westpac's rose 31 basis points to 2.32%, BNZ's rose 23 basis points to 2.42%, and Kiwibank's increased 33 basis points to 2.49%.

Banks' funding costs also rose, up 214 basis points to 3.49% across the sector. In terms of individual banks, BNZ's funding costs recorded a notable rise, climbing 280 basis points to 4.29%.

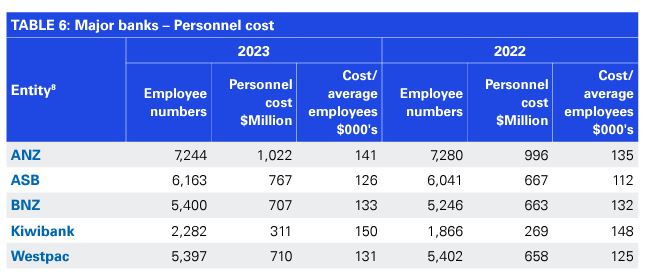

Personnel costs rise with Kiwibank & ANZ leading the way

On personnel costs, Kiwibank had a higher cost to average employee than the big four banks for the second straight year, at $150,000 up from $148,000. This follows a 26% increase last year, which Kiwibank's Chief People Officer Charlotte Ward explained here.

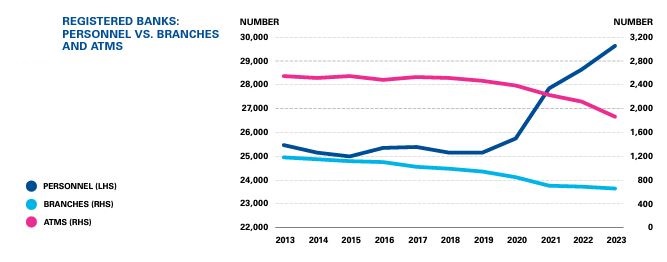

ANZ, meanwhile, recorded annual personnel costs of more than $1 billion for the first time, a $26 million year-on-year increase. Total personnel costs across the big five banks rose $264 million, or 8.11%, to $3.517 billion as staff numbers across the big five rose 651 to 26,486. (See more on personnel in the chart below).

Personnel expenses across the whole sector rose $310.73 million, or 8.60%, to $3.925 billion. Among the smaller banks TSB recorded a notable $53.12 million, or 39.11%, increase in operating expenses.

Return on equity (RoE) across the sector dropped 92 basis points to 12.48% with the 0.28% profit increase coming up against a 7.97% rise in total equity. TSB's RoE tumbled 252 basis points to just 2.74%.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

33 Comments

Only 2nd most profitable banking sector on the whole planet, we can do better. https://www.thepress.co.nz/business/350094635/nz-banks-some-most-profit…

Is it just me? When anyone in government says things like "The Coalition Government's also promising a select committee banking inquiry" I just hear the hissing and honking of a goose? I might need to see someone for that.

I think I might, as when the government say things like they would "look at how to encourage banks to lend more to "productive" sectors of the economy" I just hear the plantiff meowing of a kitten.

When you're able to more or less create your product out of thin air; the taxpayer covers your back; and you operate within an oligopoly, you should be ashamed if you're not increasing your profits.

Reminds me of the expression 'a monkey could make money in these markets.'

Oh and while I am on hold, waiting to book that appointment, I note that ANZ in their Aussie Retail bank made $1,874 M and ANZ NZ made $1,552 M in a four times smaller market. The "we are looking after our people and paying tax" virtue signalling is suspect, number of FTE in Aussie - 11,313, number in NZ - 6,766, Operating expenses to operating income in Aussie 55.6% (largely salary) - in NZ 36.3%.

Gouging lol, gotta get me some shares in these gold mines!!

Absolute cretins, and people wonder why the general population despise bankers and REA’s.

Yet we keep feeding the machine.

You can bank on property, to hell with business.

This is going to bite us down the road.

I'll play devil's advocate.

Has worked OK up to now so why shouldn't it be OK going into the future?

Because it would need to be backed by forward looking exponential growth in cheaper energy. Otherwise resource inflation, which would deflate asset values. As we are witnessing.

Because it would need to be backed by forward looking exponential growth in cheaper energy. Otherwise resource inflation, which would deflate asset values.

Sorry? I don't understand. How is credit creation underpinned by energy?

There is a cloud of dust approaching...I think I can see an outline of the mighty PDK... "incoming!!"

A lot of what PDK says is worth spending time thinking about. Our ability to expand and consume the way we do is due to growing our ability to offset offshore, like we'll try to do with our emissions pledge. Offset our footprint by claiming some other nation barely has any emissions at all.

When the cheap offshore alternatives run dry, when things simply cannot get any cheaper, where will we turn? The US is well aware, look at all of the industrial spend happening right now. Maybe they're thinking it will be cheaper to have local factories than ship everything from China in the next 10-20 years. Who knows.

All can be summarised by his statement “debt is a forwards bet on resources”. When you think on that and work it out, suddenly the penny drops. You can create debt out of thin air, but to pay that debt down will take tome and resources, of which we will, if not already, reach a point where the resources aren’t there to use to pay the debt.

As I've commented previously humans are an aberration in the natural world. No other species consumes today against the promise of doing work tomorrow. If the bear doesn't eat enough before winter hibernation it will die.

We simply cannot keep expanding the balance sheet at the pace we have been without deflating the price of everything, and attributing more and more to the servicing of debt existing debt. This is the bankers dream, and the reality from 2008, through 2021. The deflating of wages, costs matched with lower and lower interest rates to juice asset prices. And by assets I mean mortgages.

Energy is the numero uno input cost of almost everything we consume in NZ, and most of what we derive our income from. Look at our major exports: dairy, meat, tourism. Massive energy costs. If those energy costs do not continue to get cheaper, and allow for exponential growth of income, then credit creation as we've become accustomed to will no longer be possible without massive inflationary impact. The cost of resources will increase significantly, and so too will the cost of credit. Which is what we are witnessing now, witnessed through the 2000s, and 70s/80s. The inflationary impact of energy and resources has a massive counter-weight impact to the balance sheet. If you look at CPI through the last 10-15 years, see the deflationary impact of our imports, cheaper and cheaper goods, cheaper and cheaper input costs. This _must_ continue exponentially as it has for decades if bankers want to push interest rates lower and credit creation higher.

The ability to service a $1m mortgage on ~$100k income is a clear example of the need for cheap input sources, cheap food, cheap services, cheap wages, cheap everything. Without cheaper and cheaper energy, cheaper goods, cheaper resources, the credit creation falls flat and becomes inflationary itself. Can you imagine the state of the economy if we were dealing with high inflation through 22/23, and dropped the OCR from 0.25 to 0.125 to put downward pressure on interest rates and expand the balance sheet? If the cost of food doubled due to higher energy costs, what would that do to the ability to pay rent, service mortgages?

So unless energy is cheaper and cheaper and cheaper, we cannot grow our assets like we have done. We will have to look for cheaper alternatives eventually if that's what we want to do.

OK. Got it. And I think you have a point.

But banks can issue credit regardless. If the Ponzi needs to be fed, it will be.

Absolutely - until they can't anymore. Which is most likely to be due to energy growth constraint, which was more or less what I was trying to get at with the initial response.

Absolutely - until they can't anymore

But they can. Energy constraints is not a variable in their decision making.

Until it (energy constraints) forces* itself into their calculations ... ?

* whether by sky high price or inability/unfeasibility to extract due to falling EROEI

70% of our banks' investment capital sitting in houses. And we all wonder why our per capita output continues to sink.

Yes, but who needs investment capital when you have the wealth effect? Incremental consumption is much easier than making stuff.

Only 10% of us actually create the nation's wealth. The rest of us just consume stuff.

What is this nation's wealth you speak of?

Tell me you don't consume anything to create said wealth.

ANZ, NZ's biggest bank, has 72% of its total lending in the housing sector. (Also see our Of Interest Podcast episode on why banks love housing so much here). Hmmm....

Banks have migrated away from lending to productive business enterprises because the risk weights can be as high as 150%.

{kind=link}

Probably the reason housing is such a safe bet is our continual ability to import people at a faster rate than we build houses. The demand outstrips supply so prices are forced up.

Thus the boom and bust cycles in the property sector are important... as it means we often stop consenting and building houses for a few years and lose our tradies...

The biggest threat is that our tax take doesn't keep up and thus nor does investment in infrastructure/public service spending... so as per now as we pump asset (house) prices we simultaneously reduce our standard of living coz we catn build enough new infrastructure nor maintain what we have.

So ultimately the biggest threat to the economy is the point at which our water/education/transport systems start to fail and so people will leave nz and we will no longer be an attractive destination for immigrants (even at 20 to a house). And if the population starts to decline and we have over supply of houses... Kapow the ponzi collapses.

If your net profit only goes up 0.28% when inflation is up 5.2%, you have made a loss and it is not record profit.

This whole banking system and our inability to invest in anything other than property is just depressing to be honest. Doesn’t matter if you own or rent it’s such a wasteful and overpriced asset which is ultimately stopping us from making NZ a great country. I just listened to our new prime minister yesterday trying to avoid answering some pretty basis questions around interest deductibility and he couldn’t bring himself to answer the question truthfully. Why are we just accepting all this rubbish. When was making an error of judgement or getting a policy financial outcome so wrong that you are forced to talk crap. Why don’t we just call this rubbish out and help our politicians focus on doing what’s right for this lovely country.

They are all donkey deep in property from Five House Helen, to Seven House Luxon

Both sides too deep in the Donkey

The problem was when we started calling homes assets. A spillover of the corporate/investment/financial world into human living and the people bought into it because of the promised riches.

Look who was the major financial donors to the National party - was RE industry (Luxon’s property policies are a thank you promise to them).

So 70%of banks exposure is to housing. How many SME’s have put up their house equity as collateral for their businesses? I have no idea but my gut tells me plenty given a mortgage is around 2% over swap rate and commercial is easily on average 4% over. So banks exposure to housing is not 70% it’s more likely quite a bit higher. Isn’t this a bit concerning? Where’s the rating agencies ?

You got it. With 90%+ off NZ businesses being SMEs, you can be sure some of the collateral is from the Ponzi.

Has any other country even seen net lending to housing get to 70%, looks bubble to me

Yes NZ is the bubble that Ireland once was......Down at least another 10% by years end after a very very tough winter.

40 to 50% collapse peak to trough.

China and Housing - NZs twin Achillies heals.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.