The Reserve Bank is proposing that banks will have to hold between 20% and 60% more "high quality" capital, noting this represents about 70% of the banking sector's expected profits over a five-year transition period. Nonetheless the regulator expects only a "minor impact" on customers' borrowing interest rates.

The Reserve Bank has issued a consultation paper as part of the broadest review of bank capital adequacy requirements it has undertaken, which has been running since early last year.

It says it wants bank owners to increase the level of capital they contribute to their business.

“Insisting that bank shareholders have a meaningful stake in their bank provides a greater incentive to ensure it is well managed. Having shareholders able to absorb a greater share of losses if the company fails also provides stronger protection for depositors,” says Reserve Bank Deputy Governor and General Manager of Financial Stability Geoff Bascand.

“Bank crises happen more often than many people care to remember, and the economic and social costs of bank failures can be very high and persistent. These proposals are designed to make bank failures less frequent. With these changes we estimate the banking system will be resilient to shocks that might occur only once every two hundred years,” Bascand says.

The Reserve Bank says its proposal would see banks’ capital levels increase materially.

"We are proposing to almost double the required amount of high quality capital that banks will have to hold. In practice, actual changes to the amount that they hold will be less than double and will vary. The increase will depend on their current levels of capital, how much extra they choose to hold above the required minimum, and whether they are a large or small bank. Generally, it will be an increase of between 20% and 60%. This represents about 70% of the banking sector’s expected profits over the transition period. We expect only a minor impact on borrowing rates for customers, " Bascand says.

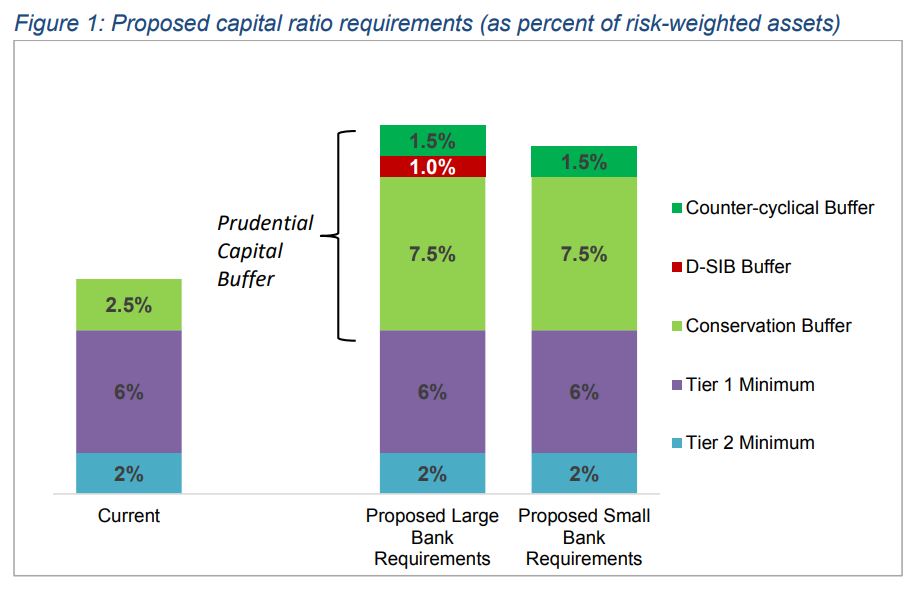

Controlling 88% of banking system assets, the big four banks - ANZ NZ, ASB, BNZ and Westpac NZ - this year made combined net profit after tax of $5.128 billion. That was an increase of $433 million, or 9% year-on-year. They paid annual dividends of $3.39 billion. The Reserve Bank is proposing that the four will be treated as domestically systemically important banks (D-SIB) and be required to hold a capital buffer above what other banks hold. (See figure 1 below). A final definition of systemically important banks is yet to be settled on, meaning potentially Kiwibank could be added.

Systemically important, or too big to fail, criteria to be introduced

The Reserve Bank proposes systemically important banks have a Tier 1 capital requirement equivalent to 16% of their risk weighted assets (RWA), with other banks requiring 15%. Currently all banks require a minimum Tier 1 capital ratio of 6% plus a common equity buffer ratio of 2.5%.

“While borrowing costs may increase a little, and bank shareholders may earn a lower return on their investment, we believe these impacts will be more than offset by having a safer banking system for all New Zealanders,” says Bascand.

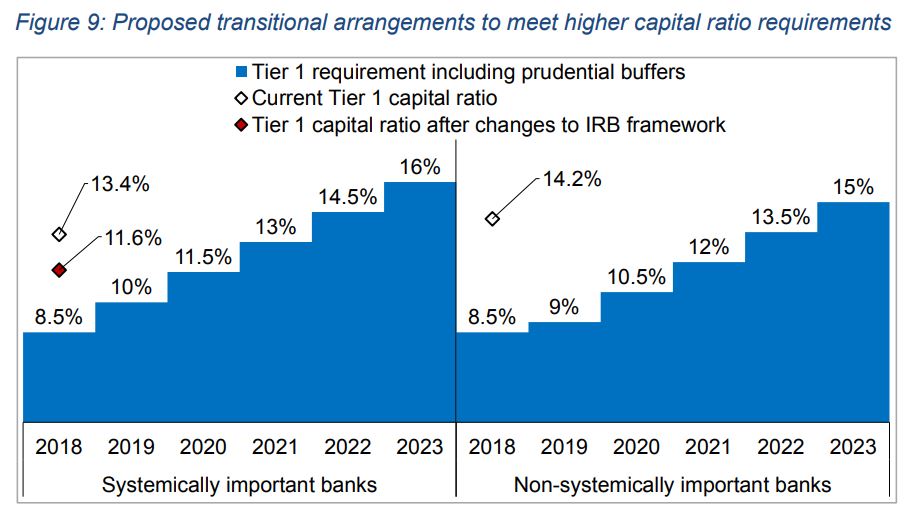

The Reserve Bank is consulting on a five year transition period for banks to meet the new requirements. The deadline for submissions is March 29 next year, with the Reserve Bank aiming to make final decisions by June 2019.

Meanwhile in terms of the potential impact on borrowers, the Reserve Bank says; "We consider a reasonable point estimate is that a one percentage point increase in a banking system's Tier 1 capital ratio from current levels may lead to a six basis point increase in the price of bank credit."

"A Tier 1 capital ratio of 16% of RWA is needed to ensure our banking sector retains creditor confidence after enduring an extreme shock."

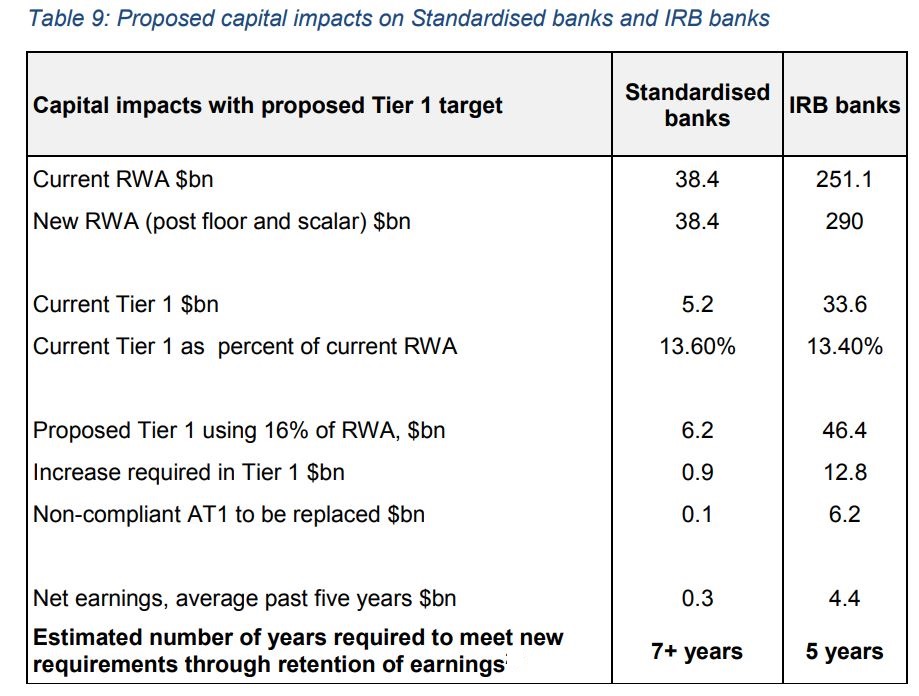

(Note, the Reserve Bank analysis in table 9 above assumes 6% annual credit growth and a stable return on interest-earning assets. IRB banks are the big four and standardised banks all others).

Bank lobby group's initial response

Asked by interest.co.nz for comment, the New Zealand Bankers’ Association acting chief executive Antony Buick-Constable says;

“Capital buffers are essential to the strength of the banking system. New Zealand’s banks are currently very well capitalised and among the most stable and secure in the world. Reserve Bank stress tests show banks can withstand a 40% fall in house prices."

“Buffers ensure banks have sufficient capital to get through a serious economic downturn. However, too large a buffer limits banks’ ability to innovate and enhance customer outcomes."

“The industry will work closely with the Reserve Bank and stakeholders during this consultation period to achieve the best outcome for customers," says Buick-Constable.

Meanwhile the ANZ Banking Group, parent of ANZ NZ and thus the major Aussie bank with the largest exposure to New Zealand, issued a brief sharemarket release on the Reserve Bank capital paper.

"RBNZ today released a 58 page consultation paper titled 'Capital Review Paper 4'. Responses are due in March 2019. ANZ is currently reviewing the consultation paper and will update the market once it has done so," ANZ said.

There's more detail from the Reserve Bank available through the links below;

·Consultation paper: How much capital is enough?

·Speech: Higher capital better for banking system and New Zealand

·Video: What is capital adequacy?

·Video: Governor Adrian Orr describes importance of bank capital

·Earlier consultations: Review of capital adequacy framework for registered banks

52 Comments

Three cheers! Lower leverage is the key to resilience. Shareholders must have more skin in their investment. Banks need to be banks, not leverage investment plays. Better capital backing is key.

C'mon the way to extraordinary bank profits is leverage. Look at Deutshe Bank with 0.1% capital. Oh wait, they are losing money and trying to merge with a functional bank so they can shift the bank debt into a shelf company, and go through an orderly shut down.

I imagine it must be fun being on the board of directors at one of the big 4 with shareholders voting down everything. They will be even more impressed with low profits and dividends from the NZ branches for the next 5 years.

I get where you're coming from David, but i still see depositors as being shafted here. there is no move to protect their rights. Indeed in some respects it may be argued that this move would actually undermine them, as a part of that capital that is referred to will be depositors funds. So in effect the RBNZ will be forcing Banks to dig their claws deeper into those funds.

Murray86,

Well, in the absence of deposit insurance, I applaud this move,even though it will have a negative effect on my bank shareholdings. Lobbying from the banks will be intense,but I hope that the RB can hold its nerve.

"Lower leverage is the key to resilience" Absolutely - and that applies to more than bank capital....

Interesting that this comes out just after they allow the banks to let investors and homeowners increase their leverage by adjusting LVRs.

Overall is it just shifting more risk (and interest costs) to the homeowners?

Yes. This is good news. But its going to take ages before it's put in place. Cross fingers in the meantime.

(But there are kiwisaver funds flowing in which reduces the probability of bank runs plus the 30 day notice period to take out term deposits).

While I totally agree, its probably too late. This should have happened before 2008 let alone after 2018.

Comment of the day goes to the Guvnor of interest.co.nz Mr Chaston. Article of the day to Mr Vaughan.

A sensible play from Mr Orr in the light of the current Australian situation.

David,

Spot on.Inmy feedback to the RB on the Dashboard,I raised leverage as a specific issue. I referred to Melvyn King’s writings on this in relation to Northern Rock.

In early 2008,it was regarded as one of the best capitalized banks in the UK,on the basis of its risk-weighted capital,but turned out to have leverage of over 60 to 1.

Is anyone else happy to see over $1000 per person head overseas in bank profits alone?

I reckon we start selling off our hospitals to foreign investors as well, they're pretty run down and the private sector always does things better than the public sector.

There can't be a problem here, as the Commerce Commision only made mutterings about Auckland Airports $53 Mil profit. ANZ's near $2 Bil wasn't worthy of comment from them. And there i think amy lie the problem!

Nah, the last time the Commerce Commission actually did anything was force Telecom to hand over the keys to the local exchanges. This was after all the software and movie pirates complained about lack of Bandwidth and Data Caps due to the monopoly Telecom had.

Less than 10 years later the Government embarked on its own Fibre Rollout so the whole Commerce Commission exercise was pretty pointless.

Hmmm, had to be done. Telecom had the country over a barrel. Coms costs have come down 1000% since those days and everyone using UFB is getting that benefit.

Yep Telecom was screwing us royally. I was on the ADSL trial in 1997~8 and I was paying about $99 a month unlimited volume while a mate of mine in Hamilton had 2 x 64K DDS lines at 2.5k per month plus volume. This of course was in private hands so whether publicly or privately owned a monopoly is simply abusive if it can be.

I do remember the days of 128/128 connections with 10 gig caps. Everyone got excited when Telecom announced some new plans, 2mbit/128k with a 10 gig cap If i'm not mistaken, they released some new even faster plans at 3.5mbit/192k (because 128k was insufficient for the ACK packets on a 3.5mbit download), these plans too had 10 gig caps.

I hope you are being sarcastic, because the USA's health system consumes x2 in % terms of GDP ours does.

Banks will be excited.

HANG ON - The RBNZ APPEARS to have taken a strong stance on capital adequacy - or has it really? The simplest way to make the banking system safer would have been to increase residential lending to 100% risk weighting from 50%.

The RBNZ are not looking to amend the Tier 1 and Tier 2 capital requirements. So what are they really proposing - an increase in the conservation buffer (relates to trading bank dividend policies) and counter cyclical capital only. This is by far the easier part of the capital to be adjusted in future as it is by definition a temporary amount - to be judged by future RBNZ management. This is a steel on the outside - marshmallow on the inside move by the reserve bank. Which will no doubt from past observation be negotiated down by the banks.

it actually is

"The Reserve Bank proposes systemically important banks have a Tier 1 capital requirement equivalent to 16% of their risk weighted assets (RWA), with other banks requiring 15%. Currently all banks require a minimum Tier 1 capital ratio of 6%."

To be petty IS NOT

Tier 1 capital requirement level does not change. Conservation capital level increases - but this is a voluntary contribution that only limits the trading banks ability to actually distribute their profits to their shareholders. In an extreme case a bank could choose to be a growth stock, pay no dividends, retain their funds internally, hold no conservation capital at all and rely on share price growth.

Correct me if I'm wrong, but the banks themselves decide what their level of risk-weighted assets are - they have an internal assessment policy and do not have to subscribe to an International Standard Level as suggested by the Basel Accord.

Only the Aussie banks, but their model has to be approved and rbnz have required that their model outcomes for RWA have to be no less than 90% of the standardised Basel Models, which all the NZ Owned banks use. That 90% floor, together with the systemic buffer ad on has the effect of neutralising the bank’s internal models, and therefore leveling the playing field in nz and ensuring that debt is correctly priced. Fuerhermore, because of the current sof growth in demand for credit....se rbnz stats numbers, passsing this onto the public will be harder. Large bank ROE will have to be reset and profit expectations down graded. About time too

And you making the residential risk weighting to be equivalent to 90% of standardised, some bank risk weights on mortgage assets will double. A triple whammy. Risk weighted assets effectively double, capital requirements almost double, and use of instruments apart from pure share capital is about halved. Ouch.

"the Bankers Association - which represents the retail banks - has responded with a warning that raising the capital buffers too high "limits banks' ability to innovate and enhance customer outcomes."

I'm not sure limiting leverage to sane level really stops actual innovation. And they must have made a mistake, they've slipped "customer" in where they clearly mean "shareholder".

"the Bankers Association - which represents the retail banks - has responded with a warning that raising the capital buffers too high "limits banks' ability to innovate and enhance customer outcomes."

The financial stability of the financial system in New Zealand should have a higher priority over the limitation of banks ability to innovate and enhance customer outcomes resulting from higher capital buffers.

The banks are talking about their own interest, whilst the RBNZ more concerned about the wider national interest.

hahahaha....."enhance customer outcomes" is code sentence for screw customers harder for longer, use no lube and not pay for any consequences.

I'm curious, what kind of innovations do the banks come up? Better ways to extract wealth from people?

In any industry, when I hear: "we want less prescriptive rules because we want to be able to innovate....", this frightens the hell out of me. Or frightens it into me to be more accurate.

"The Reserve Bank proposes the big four have a Tier 1 capital requirement equivalent to 16% of their risk weighted assets (RWA), with other banks requiring 15%. Currently all banks require a minimum Tier 1 capital ratio of 6%."

Remember that the banks can achieve this target ratio in 2 ways. (it will most likely be a combination of both)

1) increase in capital - through accumulation of retained profits (profits less dividends paid), new capital issuances

2) decrease their risk weighted assets

Decreasing risk weighted assets can be faster and has traditionally been done when banks are not profitable.

Decreasing risk weighted assets might result in banks reducing assets with higher capital risk weightings. This could include their higher risk loans in their loan book as these loans mature - particularly bullet repayment loans (which would include interest only loans, lines of credit, overdrafts,high LVR interest only loans, etc). Note that loans to certain sectors have higher risk weightings.

I see this move greatly restricting the Oz parent banks abilities to syphon off profits in order to bolster their own. After all, their collective misadventures are well documented as is their much heavier reliance on wholesale funds from New York.

Considering the rising risks, it's a timely move. "About $260 billion of Australia’s $486 billion 90-day debt comes from Wall Street" https://www.news.com.au/finance/economy/australian-economy/the-phone-ca…

too late I suspect, by a decade if not 2.

someone is going to pay for this.

Seems like a great idea. Hopefully the RBNZ haven't left it too late.

heh, just saw this mentioned on Bloomberg TV Ticker " RBNZ wants banks to Double capital buffers for Massive Shock"

Adrian Orr you sneaky little hobbit! Dangle the LVR Carrot then hit them with a stick.

I suspect the banks 4 and 5 year books are getting thinner and thinner at the moment with 5 yr TDs under 4%.

Well that is a surprise. Greenspan did say he thought equity of 20% to 30% of the loan book was needed, and nothing else seemed to do, but I thought the central banks had all decided to ignore the obvious. Banks don't need equity when all is well, only when they lose money.

What will be the knock on effect to productive businesses? As in not housing? There has to be some unintended consequences will pop up somewhere.

It's a fiction that returns on bank shares are excessive. On a total returns basis they have been only average performers since the GFC. I haven't added to my bank shareholdings for many years. I'm not arguing against the need for them to improve their capital adequacy positions but the 'screw the bastards' mob sentiments and uncouth Aussie politicians putting the boot in at every opportunity will make any capital raising exercises interesting. I wouldn't participate even if facing a significant dilution.

Maybe people see the returns as excessive in relation to the value provided? (I do at least).

Can’t argue against capital requirements but I’m not sure I agree with the reserve bank on who will pay, shareholders expect businesses (inc. banks) to deliver a certain level of returns so banks can typically pass through excess costs assuming that the sector is proportionate to the size of service demand.

Another positive will likely be banks looking to diversify revenue away from credit products.

Really interesting they do this as the Australian housing market is crashing with a probable flow-on effect to NZ's bubble. Should have been done way earlier, like 5 years earlier if it's going to take that long to complete. Hope it's not too late.

I guess the RBNZ can see whats coming and want to make sure our banks are ready. Might be too late though...

The focus of discussion to date is on the potential increased costs to borrowers. The other way to maintain their margins will be for the banks to pay a bit less for NZ deposits. $5,000 with the ASB can earn you the princely sum of a $1 a week on 60 day term deposit. How low will we go?

Help, I’m trying to understand everything fully but I’m having difficulty finding exactly what the core funding ratio is comprised of and the best answer I can find is from investopedia which is a US site. Can anyone bullet point what makes up the core funding ratio for me?

In short . cost of borrowing is about to go up irregardless of cash rate.

ECB is also unwinding QE purchasing this month. Bank funding from overseas is also going up.

RBNZ can see whats coming?

whats coming?

6% T1 is low, but its based on the traditional gold model where the customer could not carry the gold physically.

Today however the RBNZ is now it appears concerned with a collapse of the global financial system.

Ok what happens next,,,, well if you own bank shares you sell them into a loss holding company like next week and offset the loss against other trading and dividend income.

Bank shares take a huge hit and the shareholders take a hair cut.....

ooops looks like bank share holders have already taken a HUGE hit this year in NZ banks already....

Idiots... RBNZ hits the banks at the worst time and scare the market .....

its the the most stupid announcement you could EVER MAKE... OR IN THE MARKET.....

Its a total F**.... UP....

SELL <,SELL SELL, SHORT SHORT SHORT the banks NOW!!!!

and maybe SHORT THE KIWI......

now its not that its a stupid plan but the way it was announced was really STUPID.

because shocks like this dont come every ten years!!!!

You dont need to implement this by dropping a nuclear device over the MARKET .......

You implement it slowly by stealth......

BANK shares were almost entering free fall before this was announced....

Timing could not be worse....

A desposit insurance scheme should also have been looked at. There needs to be some serious no panic thinking here first.

THIS SMELLS of PANIC....

and the reaction.... automation of the banks will increase at a very fast pace... those farms that managed to escape auction this time... not next time,,, that business that was was given an extension on overdraft when dairy prices collapsed... gone....that bank employee that used to be available for you to talk to about your new farm budget... gone...

...... and that is just the START!!!

banks dont yet use the full array of advanced IT that is lurking to collate you as a customers but now it will be deployed and you wont like the result when you realise that its no longer a person protecting you from BIG DATA...

.... and it will decide to sell you any time it decides you are the RISK....

AccountingS. The reduction in risk appetite you describe will be inevitable as banks scramble to shore up their margins, in an attempt to avoid a destabilising collapse in support from already nervous shareholders. Bascand's proposition that shareholders will blithely accept a multi year diversion of earnings to capital reserves is naive. His prediction of only minor increases in borrowing costs, is RB spin that flies in the face of logic.

I wonder if the banks actually do a mark to market evaluation of the underlying collateral to their loan books. It might be easier to pretend it's worth what it was worth two years ago.

About time too. Levels the playing field between the large model banks and the smaller standardised banks. Means that competition and pricing will be fairer and will not be structurally biased to the large banks. From the point of view of depositors in nz it’s great. Means that depositor preference in Australia is less of an issue, and a really good time to introduce it, while lending growth is slow, meaning its more difficult to fund the requirement through a straight increase in rates. Capital will now have to return to nz.

Bit concerned about the capacity of the mutuals to raise the tier one capital, especially when you look at the banking dashboard and see the low levels of capital for SBS and TSB. Maybe it’s time for a merger of the mutuals. Get economies of scale and a capital structure that allows the issue of their one, without loosing mutuality. Time the boards got over their egos and did what is right for their communities. Maybe even link up to Kiwibank. This was well signalled and expected. Well done rbnz. You’ve got it right. No wonder you could get rid of the highlvr speed limits. This regime will kill them anyway, apart from the most creditworthy.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.