As house and share prices reach record highs, people are turning their attention to the impacts of the Reserve Bank’s (RBNZ) $100 billion quantitative easing (QE) programme.

Most of the focus has rightly been on whether the RBNZ’s stimulus will in fact flow into the ‘real economy’, boosting inflation and employment in line with its monetary policy mandate.

However, in critiquing the policy, one has to consider the counterfactual. What would’ve happened had the RBNZ not launched its QE, or Large-Scale Asset Purchase (LSAP) programme in March?

Some would argue the central bank could’ve essentially printed money and given it to Treasury to inject directly into the economy, rather than rely on this stimulus flowing through the banking system.

But when it comes to the RBNZ achieving its other mandate of maintaining financial stability, there’s more widespread agreement it had no other option but to become a buyer of last resort in the bond market.

“I don’t think the Reserve Bank could or should have done anything else,” ANZ senior economist Liz Kendall told interest.co.nz.

“Part of the reason the bond market has stayed functional now is because the Reserve Bank is always there and able to conduct purchases with the LSAP…

“If the RBNZ just did temporary financial stability measures, we can’t say for sure whether they’d be enough or whether they’d be long-lasting enough relative to the LSAP, which gives them [the RBNZ] a lot of ammunition.”

Four days before the RBNZ launched its QE programme on March 23, Kendall and her ANZ colleagues released a note saying it “urgently” had to intervene in the New Zealand Government Bond market to “restore smooth functioning in the wake of the recent blowout in yields that is threatening to undermine monetary policy settings”.

Kendall explained, uncertainty caused by Covid-19 saw a lack of trading, which led to bond yields spiking at a time the RBNZ’s monetary policy settings were aimed at keeping these yields, and thus interest rates, low.

She saw this tightening of financial conditions in the midst of an evolving crisis as a “red flag”.

Kendall and her colleagues could not have been clearer at the time: “We believe the market needs RBNZ action of a larger magnitude than anything seen or envisaged before. Times are anything but normal and time is of the essence.”

When the RBNZ on March 23 announced its QE programme, set at $30 billion at that time, it made it clear it was doing so to “meet its inflation and employment objectives” - IE for monetary policy purposes.

However, it noted the connection to financial stability, saying: “Committee members’ attention was drawn to the tightening in financial conditions over the past week.

“Interest rates on long-term New Zealand government bonds had risen significantly, affecting the cost of wholesale funding for any banks accessing the market at this time.

“Such increases mean that the reduction in the OCR announced on March 16 was not effectively passing through into interest rates faced by borrowers.”

Kiwi Wealth’s head of fixed interest, Diana Gordon said: “Should he [RBNZ Governor Adrian Orr] have intervened in the market? Absolutely.

“It was really scary time for our market in terms of liquidity and I think their intervention was well-timed and definitely necessary…

“It just took a willing large buyer in the market to stabilise everything.”

Gordon also pointed out how essential it was for the RBNZ to commit to buying Local Government Funding Agency Bonds.

“Considering we were… on our knees in March, it’s quite remarkable we’ve been able to come back,” she said.

However, unlike Kendall, Gordon said: “I don’t think you need to do $100 billion or $60 billion [of QE] to stabilise that market.”

Investment banker, turned risk and strategy consultant, Raf Manji, agreed.

He said the RBNZ simply signalling it was there to buy bonds off bondholders would’ve been enough to calm markets.

But contrary to Gordon and Kendall, Manji has been calling for the RBNZ to do QE by buying bonds direct from Treasury, rather than doing so through the secondary market (enabling banks to clip a ticket in the process).

Had the bond market not been so flooded by New Zealand Government Bonds, Manji believed the RBNZ would not have had to get as involved as it did to ensure smooth market functioning.

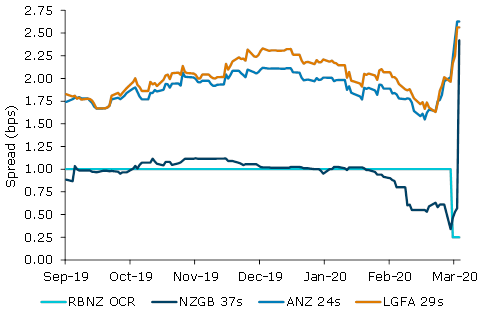

The RBNZ has to date bought $29 billion of New Zealand Government Bonds and $1.3 billion of Local Government Funding Agency Bonds via its QE programme.

It also has a number of other initiatives set up specifically to support liquidity in the market.

NZ Government bond rates

Select chart tabs

86 Comments

Complete BS. Let the market be the market. The market would have sorted the distortion out and there would have been winners and losers. Those who have been fueled by debt the losers. This QE intervention is simply to socialize losses but keep profits private all the while inflating houses. Then encourage further debt based on the inflated houses and spend that money on the next car, boat or 8k tv.

The banks should not be making a margin by buying from treasury and selling to the RBNZ to ensure "independence". With no plan to pay back this new debt Orr and Robertson are practicing defacto MMT.

Whenever I see economists at our banks quoted it reminds me of US President's quote Lyndon B. Johnson Making a speech on economics is a lot like pissing down your leg. It seems hot to you, but it never does to anyone else.

Now the RBNZ continues this saving of the debt fueled with artificial low interest rates and robbing those who are conservative and saved cash all the while pushing our banks closer to an OBR event with no deposit holder guarantee for anyone who has been conservative. Orr, Hawkesby and Bascard need to go.

Agreed, further watch as your kiwisaver funds are forced into buying NZ bonds over the next few years. In the name of protecting your investment from the volatile stock market. Welcome to the world of financial repression.

But hey so long as the boomers house prices keep going up 10 percent a year, who really cares.

There is a time and a place for Central bank intervention/participation in markets, but not at the expense of becoming them becoming The Market. They are the space-saver tyre in the boot of the markets.

Anyone who went through the sterling calamity that accompanied the UK leaving the ERM will remember that there was no market to be sorted out. No one quoted; no one answered the phones and no one had any idea where the level of interest rates was ( last seen at 50% for overnight cash and heading north) or Cable ( last seen headed for the bottom of the Atlantic in search of its namesake). The same happened here when Kreiger/BT/Elders hit the local markets with the first real Options play. The markets froze.

But once the pacemaker has been used, it should be put back in its box.

That's what we have failed to do on numerous occasions, most notably after 2008.

Regardless - it's all too late now. What happens from here will be both interesting and frightening to watch because we have put on the economic spare tyre when the proper one punctured; have kept running on it for ages at flat out speed, all the while KNOWING that (1) it wasn't designed to be used that way and (2) it's going to disintegrate at some stage when we should have paid the price of a replacement tyre some time ago.

I completely, totally agree. 100% correct.

The whole article is utterly disingenuous and highly misleading in presenting the situation as a dichotomy between the two false alternatives of having a bond market out of control with spiraling interest rates on one side, and the massive RBNZ's on the market pushing for zero rates and massive QE on the other side (potentially killing the bond market and causing a complete mis-pricing of risk and further inflation of assets bubbles)

There was also the common sense, cautious, conservative and longer-sighted approach of avoiding spiraling of interest rates while at the same time keeping them, and the natural working of the market, at a reasonable and meaningful level.

What have similar zero-rates policies policies achieved in Europe and Japan ? Zombified, stagnating economies with close to zero growth, scant productivity increases and a virtually meaningless bond market, all compounded by a structurally weak banking and financial system. This is the direction towards which the un-elected bureaucrats of the RBNZ are pushing our economy.

Spot on OC. The global can kicking has been going on for nearly 20 years. Continually adding to the debt fueled ponzi just delays the inevitable.

Central Banks around the world are one trick ponies. These purported experts all do basically the same thing - lower rates/QE. It is not fixing the problem and we now have zero bound interest rates in most of the developed world.

The day of reckoning is approaching. Isn't it about time we had an honest discourse about how we're going to deal with the coming bust rather than cheerleading the rise in house/asset prices and pretending its back to business as usual.

Playing with fundamental... Even reserve bank has no idea what the outcome will be except able to inflate stock and housing market.

Government too is happy that the only ecomomy in NZ - Housing is Rocking.

Adrian Orr is singing from the same song sheet as J Powell. Suppression of rates requires them to keep buying debt. They cannot just “say” they are going to keep rates low – they must create cash out of thin air and buy the debt. The affect of this is rate suppression.

By free-market forces not being allowed to work in the debt market, a monster bubble has manifested itself… and this assures one thing: a giant snap-back will occur at some point.

Debt Market Snap-Back

Market forces are market forces, no amount of rigging in any aspect of the market can go on forever. They can persist for exceptionally long periods of time, but there is always a time where asset values correct to fair value, and this will happen in the debt market.

As time goes on and Central Banks the world over (incl RBNZ) continue to rig the debt market, massive distortions occur and get exponentially worse. The main result of artificially suppressed rates is the manifestation of a stock market hyper-bubble and also a bubble in real estate prices.The day of reckoning will result in a “snap-back” of rates to fair value, resulting in a massive sell-off in the debt market. Interesting times.

Orr, Hawkesby and Bascard are all on their own re Negative Rates experiment that has never worked. J Powell has completely shot the idea down...."During an event hosted by the Peterson Institute for International Economics, Jerome Powell said the Fed will continue to use its tools to their fullest until the coronavirus crisis ends and the economic recovery is well under way.

Yet, among these those tools, he added, there is no option for pushing interest rates below zero.

The usefulness of negative rate policy triggered a debate in global central banking circles, given the examples of Bank of Japan and European Central Bank which could not reap the benefits and failed to reach the desired level of inflation."

So if it's known not to work, what motivation is there apart from preserving certain folks' wealth at the expense of others?

If we had better reporters perhaps they would ask them the question every interview and point out what a stuff up negative rates have been elsewhere so why does NZ want to experiment with them when the US Fed and Australian Reserve Bank have both rejected the idea...."RBA remains against negative interest rate despite rising unemployment. The Reserve Bank views negative interest rates as being an “extraordinary unlikely” course of action in Australia, even though it is predicting the unemployment rate rising to 10 per cent by the end of the year.Aug 7, 2020"

Now the RBNZ continues this saving of the debt fueled with artificial low interest rates and robbing those who are conservative and saved cash all the while pushing our banks closer to an OBR event with no deposit holder guarantee for anyone who has been conservative.

I think you’re forgetting who’s been paying your term deposit interest, those “losers” with debt.

You invested in a bank, why don’t we “let the market be the market” and see your deposits go missing. Wouldn’t want to socialise your losses.

Yes there will be no socializing of depositors losses. The RBNZ's Open Bank Resolution https://www.rbnz.govt.nz/regulation-and-supervision/banks/open-bank-res…. The RBNZ have made a beautiful diagram of how they will steal deposit holders money to refloat the bank. This was the status quo and since Corona Virus and QE Robertson has ruled out bringing in a deposit guarantee early.

I would argue the RBNZ and Treasury are increasing the risk of a bigger OBR event the greater they inflate the housing bubble and push for spending of the new wealth created due to houses going up. Removing LVR restrictions was completely irresponsible.

If it pops the debt fueled will be the initial losers. As OBR wont happen on day 1. Banks will tell the debt fueled to sell down assets and pay debt to increase there equity position. This will take some time perhaps 3 months. Bank is still getting repaid in full until approx 20% decrease in house prices is being achieved. Once its gets to approx 25% decrease in house prices the number in negative equity begins to grow but wont be known until the success of mortgagee auctions is known. This process will take 6 months plus to really kick in.

One of the reasons I have never gone beyond 6 months TD's since OBR came in. Since 31 March I have no TD's just on call at all banks.

The conservative may use there cash to buy property from the debt fueled at new market prices or they may ship money offshore or into foreign equities.

You mention that the conservative have invested in a bank. I argue you are forced too with the Anti money Laundering rules. The AML rules make having large amounts of cash to transact with impossible. Even buying property with no debt and cash from a bank account is a nightmare of compliance. Buying commercial real estate with no debt is extremely difficult due to AML rules. You are treated as a criminal for not being debt fueled. I would happily keep cash in safety deposit boxes but the banks have removed these. So the banks and the RBNZ and Government have made it nearly impossible to transact with large sums of cash.

However the truly conservative will persevere and be ready for an OBR event. Keeping all money on call. Spreading it across all five NZ banks. Ensuring you have no daily limits on electronic transfers out of your NZ banks. Have foreign bank accounts and foreign equity brokers with US federal deposit guarantees ready to take transfers or even transferring amounts now.....

As you cant rely on Orr and Roberston to protect you. They are only interested in increasing the house prices and protecting the debt fueled.

Is anyone shorting the NZ housing market through derivatives?

Yes. I know a few. They made their own.

Good luck with the OBR; inflation is your bigger issue.

Derivatives shorting the NZ housing market. Very interesting. I have been wondering if there were any out there and who was the counter party.

Yes I agree re inflation...but any amount x zero is zero (words of wisdom from Warren Buffet at his May 2020 annual meeting) so chasing yield is not worth it but there is a cost if you are very focused on protecting capital in the current environment being inflation.

Even with yield inflation will still be well in excess, RBNZ overlooks the medium term which can be quite significant.

There are no derivatives

Good synopsis of Labour’s tax policy

https://www.rnz.co.nz/news/on-the-inside/425908/unfair-tax-rules-not-he…

So give more power to Green by voting them though not a fan of Green but if government n RBNZ can do experimemt why not voters

What have the Green's achieved in the last 3 years to justify the vote? The most notable achievements I see are giving $12m of taxpayer money to a private school then trying to back tracking on it and Shaw's reasoning included the fact they have shut down oil and gas exploration in Taranaki.

Totally correct.

They have demonstrated more than once that they have not the slightest ideas about the basics of how an economy should be run. I still remember with horror when, a few years ago, the Green's guy responsible for the Party's economic policies could not even tell, when asked by the media, the current OCR level, let alone the current inflation level.

They are dangerous, ideologically motivated amateurs who should be kept away as far as possible from any economic lever. I agree with experimentation, but our economy just can't afford these guys.

I am not talking from a politically right-leaning view: I am not attracted by National's caveman approach to economical development based on roads and landlords.

It may be true that they have no idea how an economy should be run, but given the position we are now in and the massive debt and social welfare we are using to prop up that debt that makes them little different to National and Labour combined with our misguided Reserve Bank governors.

Eugenie Sage has done an exemplary job on waste management/minimisation. She took over a crisis when China abruptly stopped taking our rubbish - the crisis hasn't yet been abated but the changes to regulation/legislation are underway and the funding of local recycling infrastructure is in place.

..

Actually OC it all goes to a sorting centre first, a lot of recycling goes to landfill because it's contaminated. If NZ had a workable system where the recycling was processed into usable products, none of it would go to landfill. It's one of the Greens biggest fails since they've been in parliament. Now when NZ needs new industries supported and created, thanks to their extreme social policies, they won't be around to pursue those initiatives. Shame really - they had potential

No it goes in the landfill. "Changes to plastic recycling collections

As of Monday 20 July 2020, we will no longer accept plastics numbered 3, 4, 6 and 7 in the kerbside recycling collections – these need to go in your general rubbish. For more information, please see the following". https://wellington.govt.nz/services/environment-and-waste/rubbish-and-r….

In addition i have seen the recycling trucks taking yellow bags. But these are obviously going to the "sorting facility"

Agree. That's why a new curbside recycling standard is being introduced to address the issue of contamination; and why new/upgraded recycling infrastructure/facilities are under construction nationwide;

https://www.beehive.govt.nz/release/more-action-waste-%E2%80%93-governm…

And why work has begun on legislation that will mandate product stewardship;

https://www.beehive.govt.nz/release/government-regulate-environmentally…

And why the waste levy scheme has been amended;

https://www.beehive.govt.nz/release/government-steps-action-waste-funds…

Sage has done sweet FA about recycling other than try to tax the crap out of people (hence the big uptick in fly tipping). If she was serious or even remotely competent she would be pursuing amalgamation and support of the many small scattered industries using the waste stream. She'd also be driving real momentum in electronic recycling - so far bugger all gets done about that in NZ on a national scale, there's a whole industry sitting there waiting for and needing support. Sage is only in that portfolio because she's ex Forest and Bird and she hasn't got a clue

See above - if you are talking about electronics being used to automate the sorting of the different types of plastics, yep, that equipment purchase is a part of the $100+ million recycling/waste minimisation fund; e.g.,

https://www.stuff.co.nz/environment/118104297/new-faster-automated-sort…

There was an "incredible amount of innovation happening around those solutions", many of which were being supported by the Government, he said.

It matters not with the Greens!

All that matters is the article this morning on chloe swarbrick. How she loves renting expensive homes in trendy leafy suburbs. Talks about expensive cafes and coffee brands. Truly disgraceful.

She is part of the new of the new Geens. I want my cake and eat it as well but my parents generation must pay for it, hurry up and hand it over now.

haha, yeah PK.. read that article. Likes buying art and T-shirts off her trendy art nouveau mates she met at her previous job (I doubt she's had too many) at the trendy art nouveau bar. Now I see where she got the inspiration for her reefer- endum.

Nothing but if reserve bank are experimenting why not voters.

Why dont interest.co.nz reporters question RBNZ and Roberston where is the deposit holder gaurantee every time they interview them? Ask why do you rush to implement QE and negative interest rates increasing the risk of an OBR event but refuse to guarantee deposits like the US and Australia? In 2008 Crown Retail Deposit Guarantee Scheme was brought in the GFC. See below.

In 2008 Dr Michael Cullen, Finance Minister at the time of the scheme's introduction said, "The deposit guarantee is designed to give assurance to New Zealand depositors. The New Zealand banking system remains sound. We want to ensure that ordinary New Zealanders feel that their deposits are safe in the current uncertain international financial market conditions."

But this time around save the indebted with deposit holders money. Quite a shift.....

Didn't Orr emphatically answer that. They are looking only at debt as it is larger, gives more bang for 100b bucks. True believers.

Adrian Orr is a good Governor.

It is best for RBNZ to buy bonds, with the banks being an intermediary for government borrowing. I.e open market operations instead of giving money directly to Treasury/Government to spend. This lowers interest rates and I trust the private sector banks to undertake appropriate risk assessment and loan that money out accordingly.

When invoking the retail banks to lend that money out do you make any distinction between virgin borrowing and recycling rollovers of fixed mortgages whose term is due for reset ie 1 year, 2 year, 3 year, mortgages

Haven’t given that much thought to be honest

Economist Steven Hail explains here how the governments finances operate. https://www.interest.co.nz/news/106341/steven-hail. The government first creates currency through its spending and then it borrows it back. Only the government can create NZ dollar currency. Banks can only create credit with a debt liability. Bonds are in fact an anachronism that dates back to the gold standard days. Economist Bill Mitchell explains here why governments borrow.

Part one. http://bilbo.economicoutlook.net/blog/?p=45106

Part two. http://bilbo.economicoutlook.net/blog/?p=45108

By calling bonds an anachronism, you seem to be suggesting that RBNZ should just print money for Treasury and write off the debt. I don't disagree with Steven's description of how money can be viewed. But bond buying by RBNZ actually has implications. It's not just semantics. Do you agree with this?

From a previous article - By buying Government bonds, the RBNZ increases demand for these bonds, which in turn reduces their yield interest rates. Because a number of the interest rates in the economy are calculated off the yield interest rates for Government bonds, a move to reduce these rates will enable retail banks to lower their mortgage and business lending rates. Investors (including retail banks) also receive a cash injection when they sell Government bonds to the RBNZ.

Bill Mitchell gives alternatives in his article, paying a support rate on bank reserves for instance. He thinks that bonds are just corporate welfare, supporting an over inflated finance industry that adds nothing to the economy. Best to read his article.

My claim is that bond buying by RBNZ actually has implications. It is different to a purist MMT approach where RBNZ would print money and gift it to Treasury (government) instead of going through the current open market operations route. Do you agree with this? I ask because you've previously said that the monetary system already operates as MMT describes, which I disagree with.

According to MMT money is created at the point of its spending, it is simply typed into existence from a keyboard at the reserve bank when government payments are made. Taxation then later deletes currency, it is not re spent. What is not taxed away must then be our savings. Logically banks cannot create their own reserves or capital or our interest payments to them, we must have government money for these things including our savings, we cannot save up bank debt. Our current account deficits must also be funded otherwise private debt will continue to accumulate. (Sectoral Balances)

I know what MMT is, this isn't in dispute. It is easy to copy and paste a description of MMT but more difficult to articulate what you actually think government should be doing diffently and why.

They could stop the continual reference to government debt as something that has such a negative connotation i.e. a burden on future generations. MMT gives us a different perspective on what government debt represents.

Ok, they can start referring to "government deficit" as "private sector surplus". Both are technically correct. But what difference would this make? Zero. RBNZ would still be buying bonds through conventional open market operations instead of the MMT route of gifting money directly to Treasury.

With the latter route bank interest rates would be high and hinder liquidity. Would also compromise our reputation - with international bond holders in particular.

We are misled by our politicians, they are not truthful with us, perhaps they are mislead themselves. Everything that we are told about government finances carries a neo-liberal slant. We are given low expectations as to what can be done by our government that is dependent upon other peoples money. We are told that poverty and child hunger cannot be solved because the government has no money. UNICEF recently gave a damning report on NZ poverty levels. https://www.rnz.co.nz/news/national/425122/nz-ranked-near-bottom-of-uni…

Bill Mitchell also wrote this article about NZ and our budget surplus obsession whilst household debt and poverty increase. http://bilbo.economicoutlook.net/blog/?p=38819

tradlightly... I dont think that is correct. ( in regards to the current monetary system )

The Govt uses Westpac as its Bank for daily transactions.. In this way they are no different to you and I. It either spends what it earns or borrows and spends. ( ie. credit money ). Taxation does not extinguish money , under the current system.

The Treasury account with the RBNZ is a different story. Here the RBNZ creates and destroys at a keystroke.

Maybe You are alluding to how things will be under MMT , rather than how they are now. ?

Not sure why MMT makes such a big deal about the idea about money being spent before it is created... Thats just semantics... in a way.

Anyone can create credit ( which is created at the moment of spending )... its just that Bank created credit is accepted as money..... and is not extinguished until the IOU note is repaid.

Also current acct deficits are funded with either debt or the Sale of assets... ( under our current system )

The governments payments have to go through a commercial bank as that is where all of the recipients of these payments hold their accounts, in the commercial banking system. Westpac acts as an intermediary, it doesn't create the money for the government. When the government spends it creates reserves in the banking system, they cannot come from anywhere else. When the government borrows it lowers these bank reserves again and QE returns these reserves back to the banks again.

Maybe he is for the few supporting him, yet he will be remembered by his actions and the damage that his decisions will do to the NZ economy.

Banks are giving loans with 10 LVR and lower to people with jobs in risk sectors and others that have been getting government support in risk of losing their jobs, so please do not make fun of us talking about appropriate risk assessment.

Everything is socialised in society. Corporate bailouts to drug use and unhealthy living. No personal responsibility for anything unless you are a wage worker.

Martin Luther King said it best.. "Socialism for the rich and capitalism for the poor".

Is Adrian Orr instructing window guidance to the retail banks? You have to lend so many billions to fund asset inflation as part of the QE swap like Japan?

Adrian is doing a good job keeping house prices up but I think he may have gone too far. Perhaps just stabilising house prices would have been enough? I am not so sure now that it is really justifiable for the rich to be getting so much richer whilst the poor are suffering so much.

The poor probably need to get angry enough to march, disrupt and even riot in the streets before the government and Reserve Bank will consider that perhaps enough redistribution upwards is enough.

ZIRP and QE (LSAP) treat symptoms. The causes of this low or no inflation environment remain undressed.

Is there any substantial NZ government bond liquidation evidence associated with the global sovereign 10 year yield spike around 19 March 2020, while equity and many other securities markets were cratering?

For instance our collective banking system noted an increase in what some claim as an HQLA (Debt securities) illiquidity backstop from Feb 20 to Mar 20 ($48.939 billion to $52.908 billion) - evidence

Large US banks reported a similar outcome - evidence

{kind=link}

In the more extreme liquidation cases, liquidity isn’t just a concern for risk assets. There’s leverage even in the safe stuff, too. Much less, of course, but enough so that when the going gets really rough it can produce temporary dislocations and distortions even there.Link

MR. FISHER. In summary, I want to mention that, as I said earlier, most of these variations that have been suggested are very un-Bagehot-like. And what I mean by that is, twisting [or QE] entails purchasing assets that investors are fleeing toward, not assets that they are fleeing from. Link

Looks to me like we have a bunch of bankers thanking the RB for ensuring they can continue to make risk-free profit. What are the banks even for at this point? If they’re shielded from loss by the RB, why don’t we all just bank with Adrian directly at wholesale cost?

That would be an option for our savings, give us all an account at the RB. Government debt is nothing more than the private savings created from the governments deficit spending after all. As explained here. https://www.economicsjunkie.com/sectoral-balances-and-private-saving/

I'm a big fan of the idea of the RBNZ offering simple electronic accounts with a debit card only attached. Can't be overdrawn. No account fees. Suitable for young people who don't have complicated needs such as mortgages and loans. Government could even be generous and mandate RB pay 10% interest on saved balances. Not hard

Government debt is nothing more than the private savings created from the governments deficit spending after all.

The RBA claims:

Deposits and money are primarily born of credit

Measures of money grew strongly over March and April this year, reflecting growth in deposits at authorised deposit-taking institutions (ADIs; Graph D.1). Deposit and money growth are typically driven by new lending by the banking sector. Lending creates deposits as the funds made available to a borrower find their way into a deposit somewhere in the banking system, either as a deposit in the borrower’s account, or in another account when the borrower uses those funds to make a purchase.[1] Link

Bank lending creates an equal debt liability for the private sector so no net financial assets are created for our savings. We cannot store up bank debt as savings, it makes no sense. In just the same manner bank lending cannot create bank reserves.

treadlightly, whilst technically correct, you are missing a HUGE part of the puzzle. Whilst an liability is exists when credit is created, it isn't expected to be cancelled out until decades in the future. So until the debt is repaid, debt *is* net money in the system. This is where the problem of debt and the debt cycle always exists. A miscalculation between the availability of money and value of assets in the future, vs out capacity to consume and earn in the present. Current debt levels are making an assumption of very high earnings, high asset values and/or very cheap money in the future. If that proves to be correct over the next 25-30 years, sure no problem. But debt bubbles usually become a problem because the future never looks as perfect and optimistic as we hope it to be.

Money exists to facilitate trade and exchange. A token of agreed value that helps us swap the stuff we give and receive in the market. If there are too many tokens chasing too few goods or too few tokens chasing too many goods we have inflation or deflation. Both also affected massively by human psychology which does and will flip on a dime, at some point of the next 25-30 years. But money itself has no value, this is why MMT is a flawed theory, MMT makes the assumption that money is valuable but it is not, all the money in the world would be worthless without the goods and services we need. The goods and services that we produce have value, the money tokens are just there as an agreed way to value and exchange , the goods and service and store the value of those things as token, if we create some kind of surplus. Same is true of debt, which is even older than money. Anywhere that a surplus exists, there must be a corresponding deficit somewhere in the system (globally) unless we just chuck away the surplus. Sometimes prices can get that low but its rare.

Fundamentally, the money created must match the money required for functioning exchange of goods and services. Money is a tool. A token. Sometimes is can be mismanaged when too much or too little exists in the system. Debt however is much more complicated because it involves an assessment of trustworthiness, assessment of future values and very often, that assessment suffers from overly optimistic belief that markets and economies will continue on whatever trajectory they have most recently been on. Many studies in psychology and neurology have shown our hard wired flaws in assessment of risk.

We cannot save up good and services, we can only save up money, money saved leaves the economy, it is in 'storage', it is no longer purchasing goods and services. What do banks require when you go to them for a mortgage? They require that you have saved up a deposit. What a house of cards we would have if it was only banks that created money. If banks were the source of the money that we save then household debt and household savings would be of equal value but of course they are not, household debt is of a much greater value than savings. Levels of savings are more closely aligned with government debt levels which is what MMT tells us that government debt is.

treadlightly... The reality is that it is the Private Banking sector that creates most of our money, in the form of credit.

Credit is a claim on money. ( money being the money that the Central Bank creates and also Cash ).

Inside money is the term for Private Banking sector created Credit

Outside money is the term for Money created by Central Banks.. ie. Monetary Base + cash and coins ).

And yes... This system is inherently unstable...

Also... unless "savings" are stored under a mattress, they don't go into storage... Most people deposit it into banks .. and those Banks lend it to others..

But from the point of view of the bank, it has acquired the security without giving up any cash; the counterpart, in its balance-sheet, is an increase in its liabilities. There is expansion, from its point of view, on each side of its balance-sheet. But from the point of view of the rest of the economy, the bank has ‘created’ money. This is not to be denied. Hicks (1989, 58)

I find the idea that Govt deficits create private sector savings , therefore Govt deficits are good ... to be a myopic financial balance sheet view that is blind to where real wealth comes from... ie. the productive economy.

Let’s say you borrow $100 to build your dream home and the homebuilder banks at your bank. The bank ends up with a $100 asset and a $100 liability (the loan and the deposit – loans create deposits). The homebuilder will end up with $100 in retained earnings and you will end up with $100 in debt. If you net out the investment (you made $100 in residential real estate investment) then the private sector has no change in financial assets and you might presume the private sector is no better off than it was before. Remember, your $100 investment resulted in $100 in saving for the homebuilder. But are we actually no better off than we were before? Of course not. You have your dream house, the corporation has $100 in profit and the bank will presumably make a profit on its loan. We are all actually better off!

https://www.pragcap.com/yes-government-deficits-equal-private-surpluses/

Surely the key to government deficit spending is whose wallet it runs to and what they in turn do with it viz the velocity of money

Is this report correct or trying to create fear :

It is clear that central banks around the world are looking to set the banks up to fail so that the central banks can take over.

Plan all along. Destroy the banks and complete the takeover. Everyone will have central bank accounts and corporate elites will get funded by the fed etc directly.

No middle class and no small business. Just central banks control and ubi with no democracy.

But it looks like they’re desperately trying to prop up banks, if anything. If the RB raise rates, banks will be hit with a wave of foreclosures and failed businesses; if they lower rates, bank margins get squeezed, but that’s a chronic rather than acute illness. The idea of banks as victims of a NWO plot is silly; they’re in a trap they were enthusiastic about creating.

Silly?

Fed saying it will fund corporates directly? Digital accounts at the central bank for all and central bank created digital ubi payments.

Not silly but I guess time will tell..

Cyprus, Ireland, Greece...

The governments were never able to take over. The banks threatened them until they backed down. (Mix of private and offshore central.)

Current boom in asset price is manipulated by reserve bank and not based on fundamental and for the same now questions are being raised about fed action ( Hence the article and justification comes when have doubts) and the other question is how long can economy run on reserve bank support and why the fear of correction as up and down is part of economy cycle and BIGGER question can reserve bank has the option of controlling or stop printing money?

Correct as having duscussion on action of reserve bank by itself signifies that though needed but still not 100% correct the way they panicked and pressed the accelator on printing and distributuon of cash and going all out to support even the zombie companies.

Many action were doing on herd mentality as others are doing so even we do and was done on expiremental basis as even now No knows what the long term consequence will be - short term managed to inflate the stock and housing market but for how long can reserve bank intervine and not allow economy to run on fundamental.

The New Payday Filing employment statistics

"This data series will be discontinued end October 2020. We will update each series, each week on a Thursday, until the end of October 2020. At which point we will review whether the series will continue. This series is designed as a temporary product in response to requests for more timely information to support the COVID-19 response."

Note - It is published 4 weeks in arrears - They do not publish total wages outlaid or PAYE deducted. The series are due to be discontinued just after the last of the Government wages subsidies

Week ended 17 May 2020 = 2,199,000 total paid jobs

https://www.stats.govt.nz/information-releases/employment-indicators-pa…

Week ended 24 May 2020 = 2,208,160 total paid jobs

https://www.stats.govt.nz/information-releases/employment-indicators-pa…

Week ended 31 May 2020 = 2,207,950 total paid jobs

https://www.stats.govt.nz/information-releases/employment-indicators-pa…

Week ended 7 June 2020 = 2,197,170 total paid jobs

https://www.stats.govt.nz/information-releases/employment-indicators-pa…

Week ended 28 June 2020 = 2,188,510 total paid jobs

https://www.stats.govt.nz/information-releases/employment-indicators-pa…

Week ended 5 July 2020 = 2,193,530 total paid jobs

https://www.stats.govt.nz/information-releases/employment-indicators-pa…

Week ended 12 July 2020 = 2,170,640 total paid jobs (down 22,890)

https://www.stats.govt.nz/information-releases/employment-indicators-pa…

Week ended 19 July 2020 = 2,182,420 total paid jobs (up 11,780)

https://www.stats.govt.nz/information-releases/employment-indicators-pa…

Week ended 26 July 2020 = 2,191,710 total paid jobs (up 9,290)

https://www.stats.govt.nz/information-releases/employment-indicators-pa…

Week ended 2 August 2020 = 2,206,140 total paid jobs (up 14,430)

https://www.stats.govt.nz/information-releases/employment-indicators-pa…

week ended 9 August 2020 = 2,187,980 total paid jobs (down 18,160)

https://www.stats.govt.nz/information-releases/employment-indicators-pa…

Not bad so far.

Let's not forget about the LVR fiddle. That was completely unnecessary...

At this point it is CLEAR; Adrian Orr is a financial terrorist - in my opinion.

China Foreign Policy:

I think this is a good article. At least someone is trying to examine why the institutions are doing what they are doing.

I have to point out that NZ is not alone in it's actions. There is no country that I can see that let 'the market' collapse enabling 'the reset' leaving a pile of economic rubble, virtuous savers and asset bargains.

Given that most of the people running the financial system are conservative to their core and inherently neo-liberal why do you think they did what they did?

These are people that only take action when it is necessary, who don't believe in being the first to do anything or being the first to take the risk. They are bankers.

We are now in the stage of wait and see. In all the Anglo-Saxon economies and the EU there was an initial bump of fiscal spending to partially and reluctantly offset the impact of people staying home and people not spending. Now that the politicians think the crisis is averted they are all 'taking a pause' and going back to austerity lite. They are doing this all over the world, reacting to the wishes of their conservative voters.

The Reserve Banks all over the world are left holding the bag. The US Reserve is the leader. It has a mandate and the desire to issue bonds to pay for Trump's trillion dollar tax cut of 2017 and now the Covid stimulus spending. The US Reserve bank is also pushing down the value of the $US to devalue the cost of the US debt. We are in a phase of $US decline and at this point it becomes about power not morals.

If you let 'the market' deal to your country while you follow a prudent and virtuous budgeting policy then your own dollar goes sky high and your nation becomes a very expensive mistake for all it's misguided citizens. Once that country has managed to beggar itself and no longer has exports to sell for foreign currency then things collapse and foreigners come in and buy all the interest producing assets for a song. The locals at this stage generally don't have the means to compete for those assets.

Why don't we have a bank deposit guarantee? It could be because politicians believe in moral hazard and letting depositors take the risk. It could be because choices would have to be made about which financial institution would be included in any deposit guarantee scheme.

None of these issues is unresolvable. Again it is left to the RBNZ to be the responsible adult and tell banks to bolster capital reserves so that at least there is some buffer against depositors losing their savings in a 'bail in'. To me this is the result of irresponsible neo-liberal politicians saying even though we the govt are the lender of last resort let's keep everyone guessing until the last moment whether we we will step in or not.

The lesson of Bear Sterns has still not been learnt. When everything financial is crashing to the ground, there is no moral hazard, there is no market, there is no network of friendly bankers to prop up the system, there is only the govt and the Reserve Bank as lenders of last resort. If the last resort is not used in a timely fashion then all you have is a failed country with a lot of angry people in it.

The difference is .... In past crises - prior to 2000 - institutions and big and small corporates were allowed to stand or fail on their own merits. Since then lobbyists have become too influential. The large lobbyists are employed by the large corporates. The politicians are beholden to the corporates through the lobbyists. Nowadays the corporates and institutions are TOO BIG TO FAIL. When did that happen. When did you first hear that.? It was first called moral hazard. Australia is going after the FAANGS and standing up to the Chinese CCP. NZ is terrified of doing the same. The largest single industry in NZ is the property industry and you all know now it won't be touched. It is TOO BIG TO FAIL,

Also real estate industry is very powerfully and even government is aware that only economy in NZ to support at any cost is housing industry and for that reason has been proactive more towards it than any other industry.

If Government has to support for panademic, should also support many regions / towns like Te Anau that may be wiped out along with Hotels/ Motels/ Restaurant/ Cafe / Tourism / International education / students.....IF government is going out of the way with mortage deferral till March End 2021 by same logic should go out of the way to support those regions and industry that have been worst hit till March 2021 as they have done to protect housing industry by extending mortagee defferal from september to March 2021 and like Australia is doing tio protect all till March 2021.

Government does it as housing industry is well lobbied and also many including member of parliament have vested biased interest as themselves are heavily into property.

For many regions / industry governments attitude is if cannot survive - perish. Why not same for housing industry - biased vested thick skin politicans.

When this Newly inflated Mega bubble inevitably does burst and the banks are in trouble, who will they go after first? Will they go after the multiple rental owners, making them sell to recoup money or will they leave them be and go after the deposit savings of potential FHB's in an OBR event?

Oh god what a question.

I fear that its destined for the banks to go to the RBNZ and government, with the threat of financial chaos. And our dear leaders only have to do a quick survey to see that the ones willing to pay the price are the ones that cannot vote (or understand economics). I'm certain they will find a way to make the young pay.

I'm not sure it is possible for them to get away with such theft from the young without massive disruption to the fabric of our society, including moral standards and behaviour.

What would have happened to Bond.....

We definitely know what has happened to stock market and housing after reserve bank has done QE

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.