The Reserve Bank (RBNZ) doesn’t need to keep printing money to buy government debt.

Since the onset of COVID-19, it has successfully suppressed interest rates and helped financial markets operate smoothly by buying bonds via its quantitative easing or Large-Scale Asset Purchase (LSAP) programme.

But bond-buying isn’t achieving much anymore, and the RBNZ best start preparing to move out of emergency response mode.

This is the (paraphrased) message from ANZ senior strategist David Croy.

He suggests the RBNZ winds back its bond-buying every week to the point it isn’t buying anything come September.

The market is in a position to absorb the debt the Treasury is issuing, without the RBNZ being a buyer of last resort.

What’s more, things could get confusing if the RBNZ continues printing money to buy bonds, while it hikes the Official Cash Rate (OCR).

Croy argues it would be better for the RBNZ to stop the bond-buying, take a breather, and then embark on tightening monetary conditions by hiking the OCR - possibly from as early as November.

Background

Going back a step, the RBNZ’s Monetary Policy Committee in March 2020 launched its LSAP programme.

In doing so, it committed to being a very active player in the New Zealand Government Bond market to suppress interest rates to boost inflation and employment, and prevent the market from freaking out at a time it was being flooded with new government bonds to pay for the COVID-19 recovery.

The RBNZ committed to buying up to $100 billion of New Zealand Government Bonds on the secondary market (not direct from the Treasury) by June 2022.

To date, it’s bought nearly $53 billion of government bonds.

It has been winding back its weekly bond purchases to $200 million, from well over $1 billion last year.

Croy suggests the RBNZ cuts this purchase rate by $20 million a week, until it isn’t buying anything come September.

RBNZ may as well keep some powder dry

He makes a technical, but important point - by stopping the bond-buying, the RBNZ wouldn’t be “cancelling” its LSAP programme ahead of its end date.

Rather, the programme would sit there, and RBNZ could "print money" to buy bonds again, if necessary.

But because the bond market doesn’t need the LSAP programme right now, the RBNZ may as well keep some of its powder dry should the economy take a turn for the worst in the future.

“In short - there’s limited ammo left; it’s not needed at the moment, so it’s better to put it back in the bag,” Croy says.

The bond market can handle it

He believes the market wouldn’t be overwhelmed by the Treasury continuing to issue a relatively high number of bonds for a few reasons:

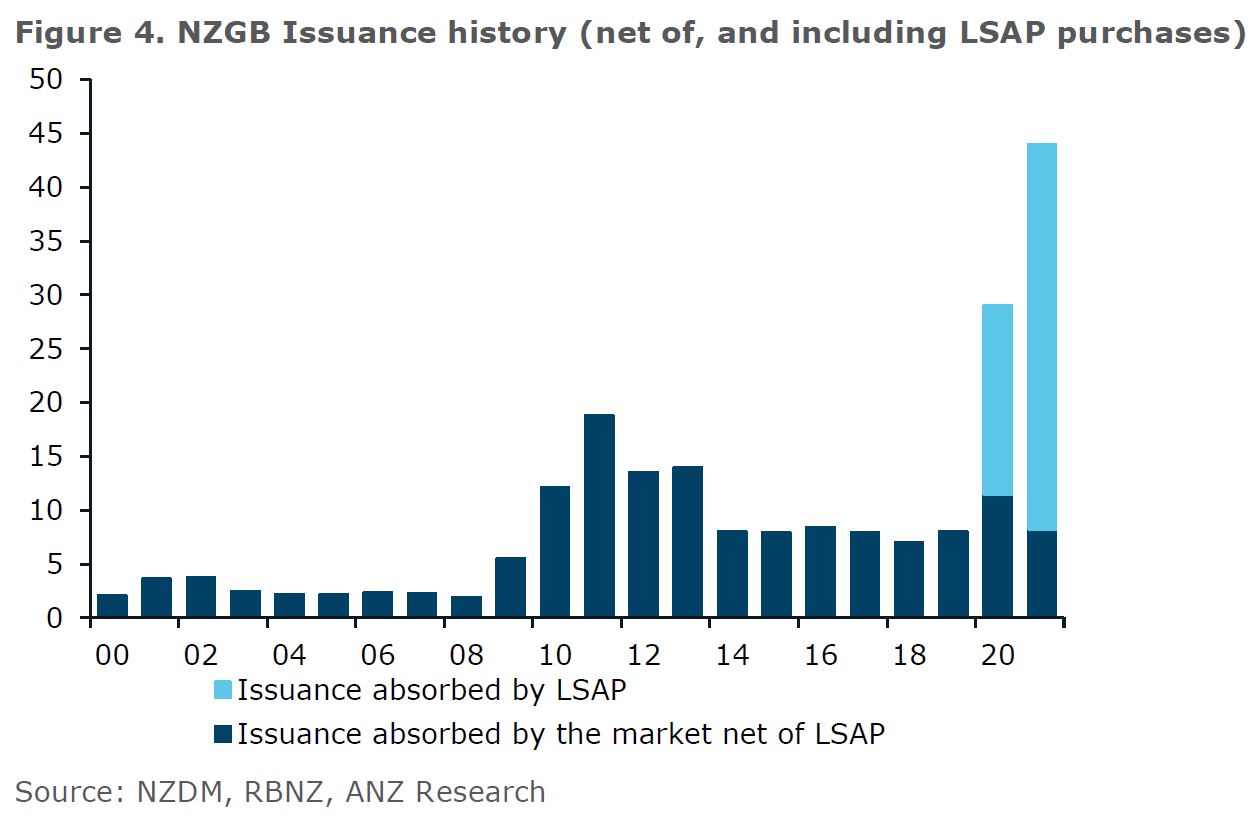

- It hasn’t actually had to absorb much debt to date, because the RBNZ has been there, buying around $53 billion of the $66 billion of bonds issued over the past 15 months (see graph below);

- The Treasury has just made a big pay out ($11.3 billion) for a matured bond;

- There is much more cash in the banking system than there was a year ago; and

- The Treasury is likely to revise down its forecast 2021/22 bond issuance programme from $30 billion, because the economy is doing better than expected.

Croy also suspects winding down bond-buying wouldn't materially increase interest rates.

He notes New Zealand Government Bond yields have “remain joined at the hip with US and Australian bond yields”, despite the RBNZ reducing the pace of its bond purchases while its overseas counterparts have largely avoided talking of tapering.

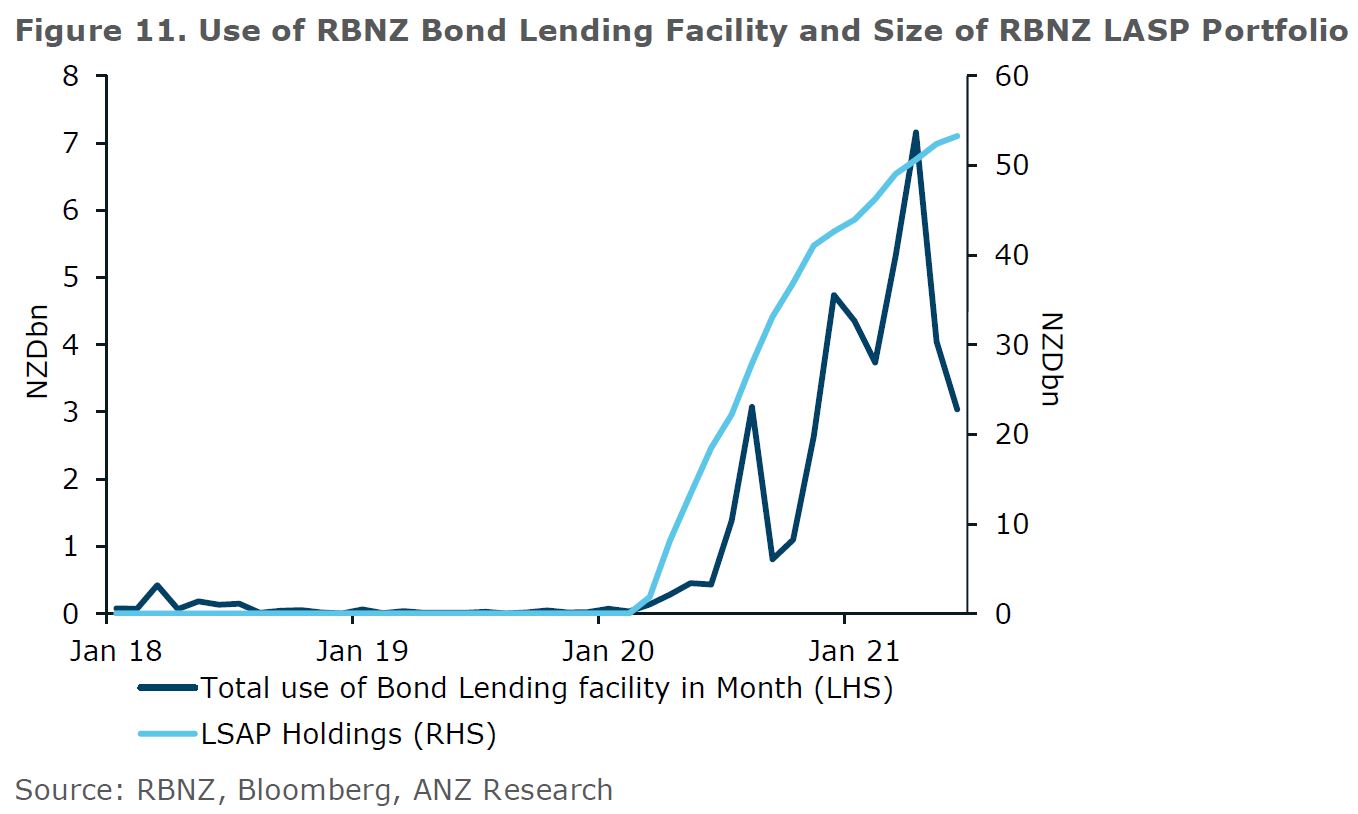

Another point Croy makes is that the uptick in banks’ use of a RBNZ bond lending facility could indicate the RBNZ is congesting the market by holding so many bonds.

The graph below shows the increased use of the facility, which banks tap into when they’re short a particular bond on any given day, because they’ve sold it, on-lent it, or don’t expect a deal to settle.

Clarity is key

Coming back to the point made earlier around the RBNZ avoiding mixed messages in the way it deploys its monetary policy tools, Croy believes it will follow the path set by the US Federal Reserve following the 2008 Global Financial Crisis.

The Fed signalled it would slow its asset purchase rate. It then issued a paper detailing the “principles” it would follow as it looked to “normalise” its balance sheet, before ceasing bond purchases and hiking its Fed funds rate.

Croy says the Fed gave markets plenty of warning around what it was doing, and expects the RBNZ to follow suit.

RBNZ will have to keep managing its large balance sheet

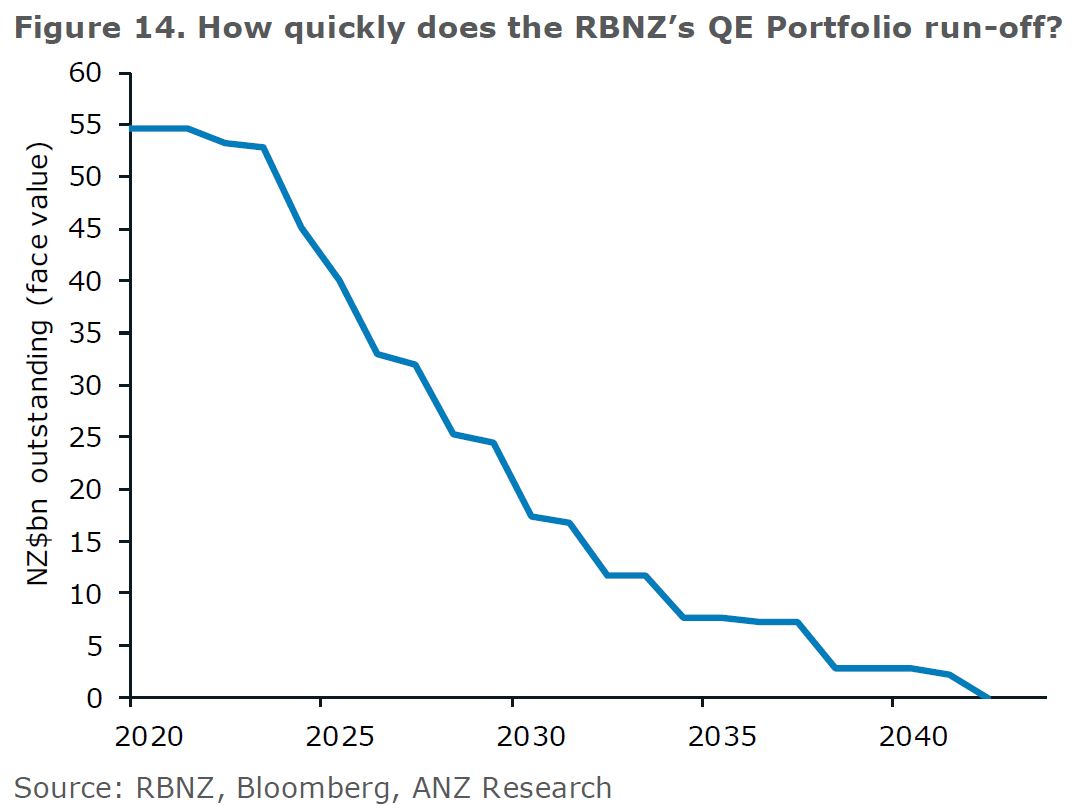

While Croy’s take-home message is that the RBNZ should wind down its weekly bond-buying fairly quickly, it’s important to note the RBNZ is likely to be an active player in the bond market for decades.

Croy acknowledges that even once the RBNZ stops “printing money” to buy bonds, it can’t necessarily just let its balance sheet shrink at the rate the bonds it owns mature.

The RBNZ might need to reinvest at least some funds from matured bonds. This is simply a feature of quantitative easing. The RBNZ now has a much larger balance sheet that it’ll need to keep managing.

The longest-dated bond it owns only matures in 2041.

47 Comments

The market is in a position to absorb the debt the Treasury is issuing, without the RBNZ being a buyer of last resort.

In doing so, it committed to being a very active player in the New Zealand Government Bond market to suppress interest rates to boost inflation and employment, and prevent the market from freaking out at a time it was being flooded with new government bonds to pay for the COVID-19 recovery.

I thought that the purpose of the reserve bank buying bonds was to force down interest rates, but these statements suggest that the reserve bank was in fact directly financing the government with printed money.

At it's very simplest it's hard to ignore the fact that the reserve Bank of New Zealand board government bonds with newly made up money.

Agree with ANZ.

Covid still presents a serious and high risk to out economy, however the economy is doing well and in the event of a further serious outbreak and shutdown of the economy there is no reason as to why QE couldn't then continue and OCR rises delayed. The increasing roll out of vaccines will reduce that risk.

While the Government and RBNZ have been widely criticised by many, Government actions have avoided the incidence of Covid, and RBNZ actions have ensured the economy has done well and employment high despite the significant foreign tourist business and employment sector being decimated.

Yes, there has been some costs to some; housing affordability for FHB (despite very high numbers), those relying on foreign tourism for business and employment and those with cash.

How have the reserve Banks actions boosted employment?

What exactly do you see as the mechanism by which this happened?

To my mind the beneficial boost in employment is the result of direct government spending more than the result of actions by the reserve bank.

Gypsy

Pretty straight forwarded as intended.

The reality is with the onset of Covid and shutting the borders and downturn in business it was estimated that unemployment would rise to 10%. That didn't happen.

RBNZ have a mandate to ensure stable employment and their actions through QE and OCR cuts has meant that unemployment has remained at around 4% (which due to a lack of inclination amongst some is considered to be "full employment").

QE and cuts in OCR led to fall in mortgage interest rates which has put more disposal income and spending into mortgage holders hands, increasing spending increasing, business and consequently employment. House inflation has also been a result and as a consequence a perceived increase in wealth and hence willingness to spend.

The alternative was to have spending tighten up with consequences for businesses and therefore employment.

Yes, Government business and employment subsidies have also directly contributed to this.

While RBNZ especially but also the Government have been criticised, their repsonse has meant New Zealand has been spared a high incidence of Covid and business and employment have been largely unscathed despite tourism being significantly affected. One only needs to look to the USA, Australia and Europe to see what could have been in terms of long and irregular periods of lockdowns, and effects on businesses and employment. Yes, that has been at some costs.

RBNZ have a mandate to ensure stable employment and their actions through QE and OCR cuts has meant that unemployment has remained at around 4%

QE and cuts in OCR led to fall in mortgage interest rates which has put more disposal income and spending into mortgage holders hands, increasing spending increasing, business and consequently employment. House inflation has also been a result and as a consequence a perceived increase in wealth and hence willingness to spend.

How would you quantify this extra spending, the direct spending by the government is definitely quantifiable, and we saw how immediate and effective it was by the publicised boom in spa pool sales.

We have plenty of evidence that businesses didn't respond to lower interest rates, as business lending fell.

I agree that the RBNZ actions have certainly goosed the housing market, are you contending it was the RBNZs intention to replace the foreign tourist industry with an extra bit of housing bubble?

I have not heard them express it like that.

Also estimated 80000 would die.

The estimators did a poor job.

If we did nothing...which fortunately we didn’t

Based on another estimate.

The low OCR made mortgages cheap and drove house prices through the roof, the QE helped hold bond prices up and medium term interest rates area down - supporting the low OCR.

Govt spending (direct fiscal injection) saved the jobs and kept consumer spending up.

Do you honestly think that business investments are affected by something as short term and minor as the prevailing interest of the day. These are long term decisions and weigh on far more important factors than the interest rates. Interest would barely register much above the "noise" level for businesses that do real stuff, create jobs and earn wealth for the country. Putting it another way, if an investment decision is so marginal that the prevailing OCR of the day is relevant, then the investment should not be made. Any directors that take any notice of the short term interest rates of the day should be fired. For property and fixed asset speculators that add nothing to the economy it is an entirely different matter. It is only these people that the easy money is really rewarding.

If the government want to encourage investment in enterprise that will meaningfully benefit the country it should be be doing far more and taking far more direct responsibility than just sitting back from an arms length position, relying on ineffective interest rate twiddling from the reserve bank.

I doubt they are - but consumption is definitely is driven by low rates. Dropping mortgage repayments puts a lot of cash in people’s pockets. conversely raising interest rates does the opposite: stalls an overheated market. I’m sure we will see that soon

It's not about business investment decisions, it's about the consumers who are the customers of those businesses.

If mortgage holders suddenly have more disposable income, they will spend more, and businesses will do better.

Likewise, if money in the bank is earning minimal interest, savers are more likely to go and spend it at a business somewhere.

saw an interesting article the other day that having low interest rates to get businesses borrowing may actually be an outdated economic theory- the reason New Zealand (and Australia for that matter) are now primarily service economies - where the majority of businesses are "service related" ie hospitality, banking, insurance, accounting are all service industries (in NZ 80% of businesses are service related).

These businesses rarely buy assets (their premises are leased and they have minimal equipment - in hospitality its limited to kitchen equipment and table and chairs) and the majority of their costs are labour driven. As a result these businesses rely more on cashflow than the use of debt to keep the business afloat.

Lowering interest rates wont result in these companies borrowing anymore debt - and with 80% of the businesses in NZ in this position - its little wonder business debt uptake in the last few years has been sluggish if not non-existant.

Unemployment is low because the borders are closed and deferred spending from 2020.

it is a moral conundrum.would a policeman take his knee of a savers neck to preserve his capital and then jump on the back of a borrower causing money to fall from his own pockets?

Interesting metaphor, but in our world the choked saver never gets the purchasing power back they lost, and the asset holders keep it all. The damage the cop has done is long term.

So a bank that buys bonds (and sells them on for a profit) wants RBNZ to stop holding the price of bonds up (and the yields down)? Surely not?

"The RBNZ might need to reinvest at least some funds from matured bonds. This is simply a feature of quantitative easing."

Why? I've never seen this satisfactorily explained apart from the feeling that markets will get mad that the central bank isn't shooting them up with heroin.

Exactly right - this article basically says "We (ANZ) hate the fact that the RBNZ are controlling the bond market and reducing our ability to make even more money from speculating on financial assets"

I hate it when people describe LSAP as 'money printing'. The order of things is very simple:

(1) Govt creates new money when it pays for things (*this is when the money is 'printed'*)

(2) When Govt sells a bond for $1m, it takes $1m money out of circulation

(3) When RBNZ (Govt) buys a $1m bond, it puts $1m money back into circulation

(2) and (3) are just swaps - bonds for cash, cash for bonds etc. A financial hokey-cokey.

Flooding the market full of cash - better?

The only 'flooding' has come from the torrent of credit money created by banks and given to mortgagees. This has inflated house prices and sent bank profits through the roof. The money that Govt has created (by spending it) has saved jobs and helped the country through a crisis.

QE has kept interest rates low, and thus made owning real estate more affordable. The RBNZ has also provided 28 billion dollars of funding direct to banks for this purpose. The RBNZ at the same time removed LVR restrictions on property. QE therefore has had a massive impact on house prices.

It has created massive asset price inflation. When interest rates rise, unless incomes rise too, asset prices have to then drop. When the tide goes out, we will see all those that were exposed. A financial crash is likely going happen at some point in the future, it is just when it will happen.

So it is 'indirectly' money printing. The technocratic arguments are quite frustrating.

Isn’t it debt printing? The money supply is only temporarily expanded.

Isn’t it debt printing? The money supply is only temporarily expanded

Technically yes. Base money refers mainly to bank reserves and to a smaller extent, currency in circulation. Commercial banks take that base money, and multiply it via lending in a fractional reserve banking system to create broad money. In the U.S., base money is $5.3 trillion, while broad money is $19.5 trillion. So broad money is about 3.7x as much as base money. In Japan, base money is ¥620 trillion, while broad money is ¥1,140 trillion, so broad money is about 1.8x as much as base money.

Why is there such a difference between the U.S. and Japan? Japanese h'holds and firms have been paying down debt and not spending / borrowing like drunken sailors.

That's what the text books say (fractional banking etc), but that is fantasy land now. You only have to cast an eye over the RBNZ balance sheet to see this - bank reserves (commercial bank settlement accounts) are 5 times higher than they were a couple of years ago (QE), and banks never check their reserve accounts before they create the cash to handover to a borrower.

And what should happen is a recession. But money supply is continuously "temporarily" expanded through lowering of interest rates.

Once a Reserve Bank commit to QE (LSAP) they're always committed to QE because debt levels out-grow the economy. The treatment for rates being set too low for too long is to push rates lower for longer, it's Hotel California Syndrome.

Exactly if the RBNZ doesn't buy our debt then who will? Its worthless paper every institutional investor knows that. We will keep printing & continue our journey down the yellow brick road

The safest financial asset in the world is now ‘worthless paper’!! Delusional stuff.

flooding the market full of cash is not flooding the people full of cash and is doing nothing for ordinary people except Asset/House owners

with 44billion in its current account -- that this government is already incapable of spending -- why would we load ourselves up with more debt

Lets stop it now !

The Reserve Bank (RBNZ) doesn’t need to keep printing money to buy government debt.

Since the onset of COVID-19, it has successfully suppressed interest rates and helped financial markets operate smoothly by buying bonds via its quantitative easing or Large-Scale Asset Purchase (LSAP) programme.

Banks never lend money, nor does the RBNZ. They are in the business of purchasing securities. When one gets a bank loan, the loan contract is a promissory note. The bank purchases that contract from the borrower. Now the bank owes the borrower money and it creates a digital record of the money it owes, which we call deposits.

Banks were and still are overwhelming buyers of government securities at tender and syndicate issuance events. The record of debt owed is credited to the crown settlement account at the RBNZ, from where it can be spent into community bank accounts.

The RBNZ does the same when it buys government bonds except the record of debt is recorded on the selling bank's account at the RBNZ, but it never leaves to circulate in the community, while the bonds are on the RBNZ ledger. And would be extinguished if the bonds were sold or redeemed.

Furthermore, the 10 year NZ government bond low yield was recorded ~ 0.5% in May 2020 and has never been back close since, it currently trades ~ 1.71%.

Not sure about you but Orr comes across to me like a drunken sailor, the guy doesn't know when to stop. It would appear that other people like bank economists are now having to point out the obvious. Will he listen ?

Emergency is over long time and this fear of withdrawal will always remain irrespective at what level the economy is performing.

Emergency action should be for emergency instead of making it new norm. Advisable to not use full ammunition specially when not needed. Also now is the time to stop imitating and following Fed - Reset.

This was recorded last year. Wonder what his thoughts will be today.

It hasn’t actually had to absorb much debt to date, because the RBNZ has been there, buying around $53 billion of the $66 billion of bonds issued over the past 15 months (see graph below);

This does not reduce the deposit liability the banks have to the government after they monetise the bonds. Contingent bank liabilities such as the crown settlement account are deducted from bank assets (bank settlement accounts) held as reserves at the RBNZ, until they are deposited into the public banking system.

Exactly - it is not hard to look at the balance sheet (https://www.rbnz.govt.nz/statistics/r1) and see the interplay between bank settlement accounts and securities.

The national debt.

We Could Pay It off Tomorrow.

"The idea that the rest of us are personally liable for some portion of the national debt is preposterous. The truth is, the entire national debt could be paid off tomorrow, and none of us would have to chip in a dime".

'The truth is, we’re fine. The debt clock simply displays a historical record of how many dollars the federal government has added to people’s pockets without subtracting (taxing) them away. Those dollars are being saved in the form of U.S. Treasuries. If you’re lucky enough to own some, congratulations! They’re part of your wealth. While others may refer to it as a debt clock, it’s really a U.S. dollar savings clock". Stephanie Kelton.

https://www.milkenreview.org/articles/the-deficit-myth

Only in the minds of MMT proponents

There is more truth and clarity in the mind of an MMT economist than that of all the delusional orthodox economists that live in a world of fantasy and groupthink.

The bond market never lies.

The US 10 year yield has been dropping the last few months.

QE helped with liquidity short term but in the long run it will tighten conditions hense why the QE will never stop. Look at Japan they invented it. The worlds population is aging and technology is taking jobs. The central banks know this and will keep the QE rolling. I expect the CPI to slow down eventually to a constant near zero print and rates to stay down.

No it hasn't. Look at the UST 10yr chart in the RH sidebar (desktop version), or here. It's only been slipping (slightly) in the past four weeks. In the past 15 months it has been rising. It is now back to where it was in Sept 2019.

History won't judge mad dog Orr kindly.

QE,will it be judged as the saviour of the economy or another unfortunate experiment.

A drug to ease the pain sorts the immediate problem; the withdrawal syndrome will be be an extra on top of the returning pain.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.