BNZ senior interest rate strategist Nick Smyth believes it would make sense for the Reserve Bank (RBNZ) to soon start selling some of the $54 billion of New Zealand Government Bonds (debt) it bought in 2020 and 2021.

This would help clear the decks, should the central bank decide to use bond-buying to lower interest rates again in a future downturn. The RBNZ might find it difficult to enter the market with a splash again, if it is already too dominant a player.

But, because the RBNZ is only allowed to sell the bonds it owns to Treasury, and Treasury doesn’t have enough cash to pay for a heap of purchases, it’ll have to issue more debt to cover the cost.

Larger bond issuances would put upward pressure on interest rates, which would align with the RBNZ’s goal of tightening monetary policy to lower inflation.

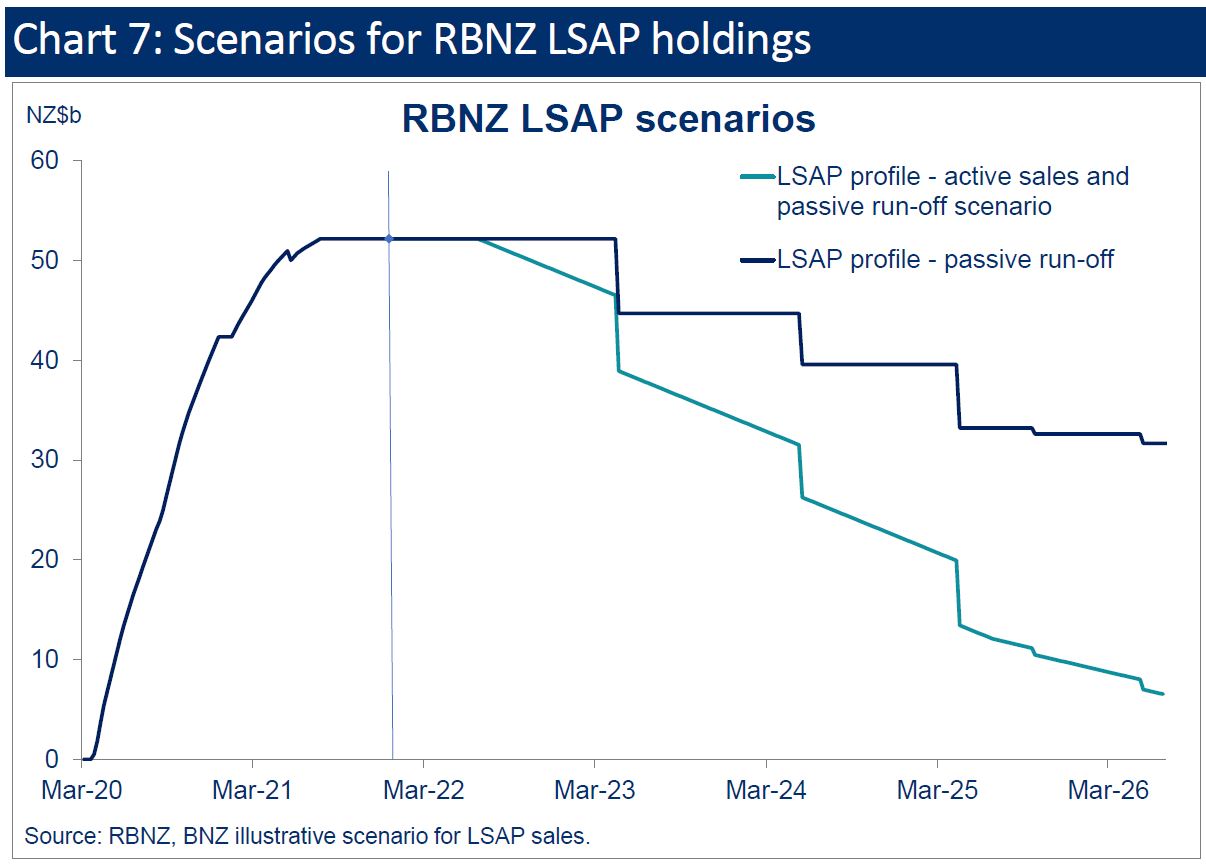

The RBNZ has said it wants to gradually shrink the size of its bond portfolio. It’s soon due to detail whether it plans to actively sell bonds or let them drop off its balance sheet at the rate they mature.

Smyth's case

Smyth, in a research paper published during the week, said he believed the RBNZ should start selling bonds to Treasury in the middle of the year.

He said the RBNZ could sell $5-10 billion a year. If it sold $7 billion in the year to June 2023, Treasury would need to increase its forecast bond issuance by the same amount.

This would bring Treasury’s forecast issuance back in line with where it was before December, when it cut its forecast issuance for the year to June 2023 to $18 billion.

Under the indemnity provided to the RBNZ by the finance minister when it launched its bond-buying programme, the RBNZ is only allowed to sell New Zealand Government Bonds back to Treasury.

While the RBNZ was required to buy the bonds on the secondary market (to stop it looking like the RBNZ was directly financing the Government), it isn’t allowed to sell them on the secondary market.

The condition exists to prevent sales made by the RBNZ causing market dysfunction. For example, there could be a problem if the RBNZ decided to sell a wad of its bonds at the same time Treasury did a big issuance.

The RBNZ is due to provide guidance on its bond portfolio early this year - possibly when it releases its next Monetary Policy Statement on February 23.

Meanwhile Treasury is next due to revise its forecast bond issuance programme at the May Budget. Hence, Smyth believed a start date of July for the bond sales made sense.

He didn’t believe Treasury flip-flopping on its forecast issuance was problematic.

Furthermore, he maintained there would be enough demand in the bond market to absorb the higher issuance, particularly if New Zealand Government Bonds qualify for inclusion in the World Government Bond Index.

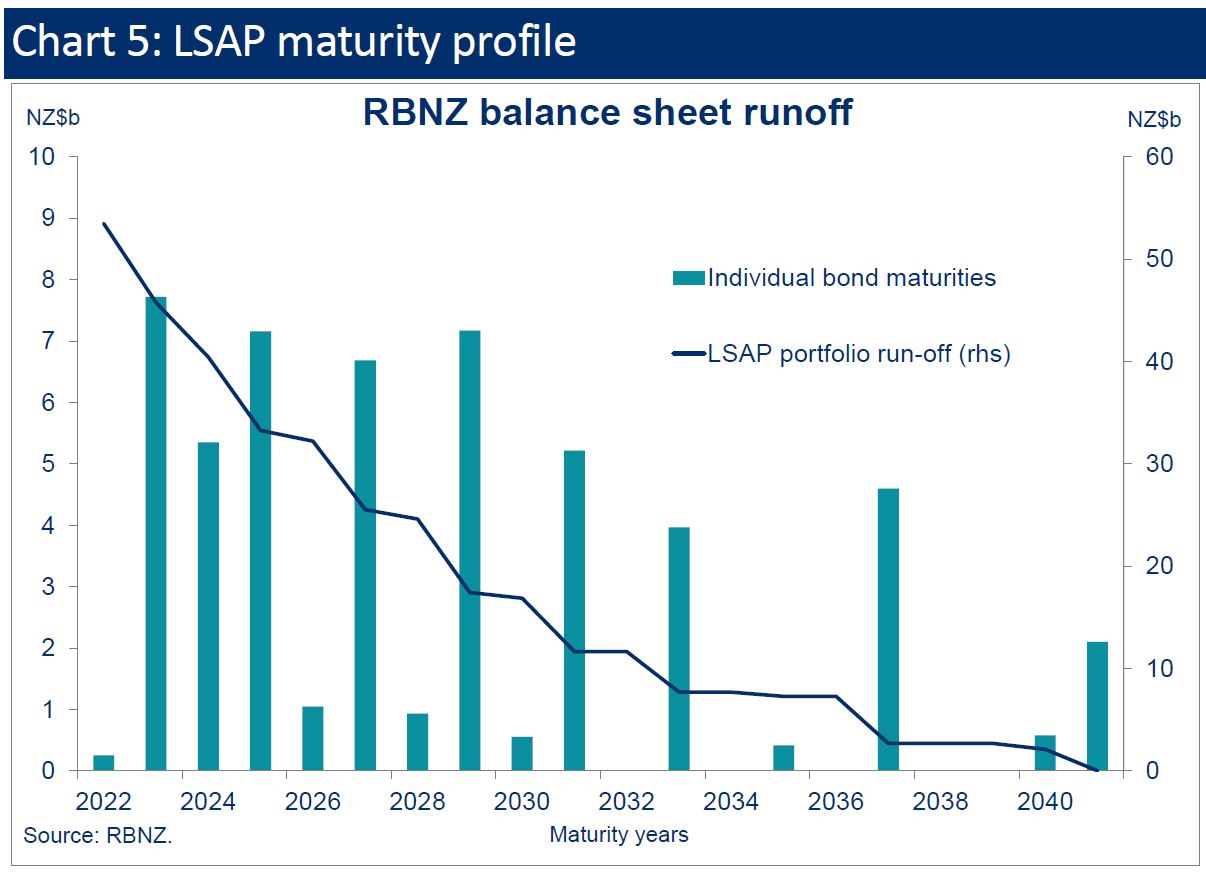

Smyth believed it would make sense for the RBNZ to sell its longer-dated bonds, as those with shorter maturities are due to roll off its balance sheet soon anyway.

OCR hikes could be slowed - maybe

As for the impact on interest rates, Smyth said RBNZ bond sales would point to a steeper New Zealand Government Bond yield curve.

Treasury issuing more bonds would also put upward pressure on longer-term yields.

Accordingly, Smyth said the RBNZ might not have to increase the Official Cash Rate (OCR) as much as it otherwise would’ve, but this “remains to be seen”.

The RBNZ has said that looking ahead, it prefers to set monetary policy using the OCR.

NZ different to the US

If the RBNZ did what Smyth suggested, it would be a world leader. The Reserve Bank of Australia and United States’ Federal Reserve, for example, are only just due to stop their bond purchases, let alone start sales.

But Smyth noted that unlike the Federal Reserve, which owns bonds with a range of maturities that will naturally drop off its balance sheet regularly, the bonds the RBNZ owns will mature in lumps.

Furthermore, the first big tranche of New Zealand Government Bonds the RBNZ owns only matures in April 2023.

If the RBNZ only let the bonds drop off its balance sheet as they matured, it would still hold over 20% of the New Zealand Government Bonds on issue by mid-2026.

The bigger a player the RBNZ is in the market, the less capacity it has to intervene again to put downward pressure on interest rates.

Smyth expected the RBNZ to give itself some flexibility, making sales contingent on the economic outlook and market function.

41 Comments

This all seems very incestuous. Like we're creating a kind of captive bond market.

Imagine of we did the same thing for the housing market. Houses may only be sold to, and bought from, a special government department who sets the price according to political goals.

I'm almost frightened to type that out, in case it actually happens. Nothing surprises me anymore.

You realise after a while that ideas like the free market and individual rights are really paper thin.

Still, we'll all play along until it stops working.

Agree.

Didn’t Kianga Ora do just that ?

free market capitalisme is dead

This may trigger a NZD sell-off.

Sharp minds will have already sold. It's been obvious for quite some time where its future value is going to lie.

If NZ Treasury buys the bonds held by the RBNZ are they considered redeemed and therefore the deposits - bank IOUs (Crown Settlement Account) associated with their initial issuance extinguished? The same issue arises with Bank Settlement Accounts at the RBNZ - when the bonds are purchased by NZ Treasury bank assets must disappear from the RBNZ's balance sheet. Hence new NZ Treasury bond issuance is just replacing floating rate cash bank assets with new coupon bearing term assets - QT? Since interest rate curves are flattening this suits government.

Audaxes,

The BBC Reality Check has examined Boris Johnson's claim and found it to be baseless. Now, in his typically weaselly manner, Johnson says that he was not talking about Starmer's personal record as DPP, just his responsibility for the organisation as a whole.

Perhaps you will now see fit to apologise for the link you put up-though i am not holding my breath.

“lower interest rates again in a future downturn …”

BNZ senior interest rate strategist Nick Smyth believes it would make sense for the Reserve Bank (RBNZ) to soon start selling some of the $54 billion of New Zealand Government Bonds (debt) it bought in 2020 and 2021.

This would help clear the decks, should the central bank decide to use bond-buying to lower interest rates again in a future downturn. The RBNZ might find it difficult to enter the market with a splash again, if it is already too dominant a player. [my emphasis]

I still love the way the Reserve Bank of New Zealand just comes right out with it:

Studies found the government bond purchases worth 10 percent of GDP have, on average, lowered 10-year government bond yields by around 50 basis points. - Link

Underwhelming, isn’t it? Pitiful, actually. Link

After all, the central bank buys whatever bonds, their price should go up. The more which gets bought, the higher the market price is nudged if not shoved therefore reducing the interest rate. And since current Economic theory equates low interest rates with stimulus – despite an equally long and unbroken historical track record showing otherwise – anyone near or around the Federal Reserve (like ECB or Bank of Japan) has been urgently seeking this validation ever since that long-ago first attempt.

It has proved only elusive.

Not for lack of trying. One such robust shot was made last March, a paper published in the prestigious Journal of Monetary Economics by the University of California’s Eric Swanson (a special thanks to Mr. Tateo for first reading through it). It was straightforwardly titled: Measuring the effects of federal reserve forward guidance and asset purchases on financial markets.

Using quantitative econometrics (what else?), Professor Swanson tries to quantify the effects of both large-scale asset purchases (LSAP) as well as forward guidance on asset markets, including others besides the one for the assets being purchased. We’ll stick to his findings on Treasuries here given our focus.

According to Swanson:

“Finally, for LSAPs, we would like the units to be in billions of dollars of purchases, which is a more difficult transformation. Nevertheless, a number of estimates in the literature suggest that a $600 billion LSAP operation in the U.S., distributed across medium- and longer-term Treasury securities, leads to a roughly 15bp decline in the 10-year Treasury yield.” Link

Even Dallas Fed’s Richard Fisher (FISHER!, for god’s sake) understood at its most basic level what the Fed was doing as it wasn’t money printing or even the holding down of bond yields:

MR. FISHER. In summary, I want to mention that, as I said earlier, most of these variations that have been suggested are very un-Bagehot-like. And what I mean by that is, twisting [or QE and yield caps] entails purchasing assets that investors are fleeing toward, not assets that they are fleeing from. [emphasis added]

Correlation, not causation.

As I have often written, the Fed’s balance sheet is actually the same things, the same sort of indication as falling yields (yes, you read that right), both adding up to negative, deflationary connotations. When the central bank’s balance sheet goes up, not only is this not the cause of rising bond prices, the QE’s, again, are a reaction to the same problem which further corroborates why and how bond yields have already sunk. Link

{kind=link}

{kind=link}

"The RBNZ might find it difficult to enter the market with a splash again, if it is already too dominant a player".

Read: the RBNZ has run out of ammunitions, and there is only so much they can do to cheat the interest rates markets for much longer. The interest rates normalization process has started, driven also by global developments, and there is very little the RBNZ can do about it - they can only postpone the inevitable, at the cost of having to tighten even more, later on, if they are so shortsighted or delusional as not to acknowledge the simple fact that the new reality of interest rates markets is structurally different to what we have seen in the last few years (or so incompetent as not to understand the long term destructive effects of a recklessly and excessively ultra-loose monetary policy maintained for way too long).

Agree 100%

Gospel Truth.

Need bold decession by all even at the cost of short term pain but will they as Politicians and Central Banksers unfortunately have very short term view for biased reason.

Not seeing to many predictions from economists on how high and when the OCR will go. Perhaps that would require actual percentages and dates so its a bit to hard to commit to. Maybe I'm not doing my reading in the right place to find it.

A cursory look at the RBNZ balance sheet shows that the table is already set for the Govt bond purchases. Govt has around $29.6bn in cash in the Crown Settlement Account (around $5bn in usual times), and Govt spending (more than it has taxed back) has boosted the balances of banks' Settlement Accounts to $44.4bn (usually around $3bn).

So... Step 1: Govt buys, say, $20bn of bonds from RBNZ. The Crown Settlement Account is marked down by $20bn and RBNZ assets are marked down by the same amount. Zero drama. No change to deficits etc.

Step 2: Banks are currently earning less than 1% on the $44.4bn of credit in their RBNZ Settlement Accounts. This is credit literally sat waiting to be used to 'purchase' bonds (it has nowhere else to go really). Treasury will therefore issue some bonds over the next couple of years and drain this credit back to usual levels. The Crown Settlement Account will swell again and Step 1 will get repeated. Zero drama again.

Bank Strategest = vested interest. Put interest rate where it should (2% over inflation) be and let the gamblers reap their reward.

RBNZ ...just do your job.

I'm sorry but I don't really understand the RBNZ needs to "sell" the debt. Cannot it not be key-stroked away?

At the cost of our credibility and creditworthiness as a country, but that's probably already gone...............

I wish I could understand all of this, but alas, most of it is beyond me. I was educated last century. Sigh.

Here is a snippet from a story I wrote in December that provides a bit of background (it is all awfully confusing):

The RBNZ bought the bonds between March 2020 and July 2021 to lower interest rates to help boost inflation and employment, and support smooth market functioning at a time the bond market was being flooded with debt issued by governments who needed cash to pay for the Covid-19 response.

When the RBNZ launched its LSAP programme, it committed to buying up to $100 billion of New Zealand Government Bonds by June 2022.

However, because the economy rebounded more quickly than expected, the RBNZ stopped the purchases early, before it started lifting the Official Cash Rate (OCR) in October.

The RBNZ hopes increasing the cost of money using the OCR, ahead of turning its attention to how to reduce the supply of money, will cool an overheating economy.

Its preference is to prioritise using the OCR, as it’s a simpler and better-known tool than changing the supply of money by being an active player in the bond market.

As for the bonds it already owns, it can either let them drop off its balance sheet when they mature, possibly reinvesting some of those proceeds. Or, it can actively start selling the bonds.

While it isn't in a hurry to do so, it would be easier for the RBNZ to use bond-buying as a means of lowering interest rates again in the future, if it wasn't already such a dominant player in the bond market.

During the 2020/21 round of bond-buying, the RBNZ agreed it wouldn’t buy more than 60% of the New Zealand Government Bonds on issue.

The RBNZ being such an active player in the bond market has a material effect on the way the market functions.

The RBNZ and Finance Minister therefore agreed at the onset of the LSAP programme that should the RBNZ wish to sell its bonds, it would have to sell them straight to Treasury.

They figured it was better for Treasury and the RBNZ to be made to coordinate with each other than for the RBNZ to try to flog off bonds to investors at the same time Treasury issues new bonds. This could be confusing and distortionary.

Between March 2020 and July 2021, the RBNZ was made to buy government bonds on the secondary market, from banks that had bought them from Treasury, so as not to directly finance government spending.

But, should the RBNZ sell the bonds, it would need to work very closely with Treasury…

Both Treasury and the RBNZ won't want their moves in the bond market to cause dysfunction or uncertainty. However, it will be interesting to see if their goals conflict in any way.

The RBNZ will be mindful of how any bond sales affect interest rates and thus its inflation and employment targets.

Treasury will be wary of ensuring New Zealand Government Bonds remain attractive to investors, and the Crown accounts are in good shape in accordance with the Public Finance Act.

While New Zealand is ahead of most other countries in unwinding stimulus, other central banks have previously been down the bond-buying path. So, we have experience to learn from. Two things are for certain:

1. It’s easier to increase the supply of money than it is to reduce it.

2. Public servants at number 1 and 2 The Terrace will continue to play critical roles shaping the market.

https://www.interest.co.nz/bonds/113690/how-treasury-and-reserve-bank-c…

Your explanations are superb and I follow it generally. But I still can't understand why "some" of the GBs bought can't be erased. I know my idea sounds awfully simplistic, but I can't really follow why it can't be done.

The BNZ strategist made zero sense to me. Treasury would only need to issue debt to fund bond purchases from the RBNZ if they intended to hold them. If the bonds were to be sold into the secondary market, then there would be no requirement for funding as the bond proceeds would be received t+2. So why transfer ownership to Treasury if they are just going to hold them, it's the RBNZ who have the better balance sheet to hold such assets.

Also, the often quoted LSAP losses are entirely misunderstood. The RBNZ held bond prices artificially low whch was a transfer of value to the DMO as issuer. Much of the MTM loss is sitting as a gain on the Crowns balance sheet.

When RBNZ buy a $200m bond on the secondary market, they credit the Settlement Account of a commercial bank with $200m (who then credit the bond seller). That extra $200m liability in the Settlement Accounts still exists if RBNZ and Treasury agreed to tear the bond up, so what's the point of tearing up bonds - it doesn't decrease Govt debt / liabilities?

It's kind of like your wife having a debt and you deciding to take over that debt. Your 'net household debt' does not change. If you decide that your wife doesn't have to pay you back after all, that's all very nice, but your net household debt does not change... there is still that debt to pay.

When RBNZ buy a $200m bond on the secondary market, they credit the Settlement Account of a commercial bank with $200m (who then credit the bond seller). That extra $200m liability in the Settlement Accounts still exists if RBNZ and Treasury agreed to tear the bond up, so what's the point of tearing up bonds - it doesn't decrease Govt debt / liabilities?

But it increases the money supply. It has to. And that is the whole point.

No, both bond sales and bond purchases (QE) simply change the form of the Crown's liabilities - from balances in RBNZ settlement accounts (earning a bit of interest) to bonds circulating in the economy (earning a bit more interest).

Govt increases the money circulating in the economy when it spends and reduces the money circulating in the economy when it taxes. The cycle go likes this - using ANZ as an example:

- Govt spends $100m on a contract: Balance on the Crown Settlement Account reduces by $100m, Crown's net worth reduces by $100m, ANZ's Settlement Account balance increases by $100m, ANZ credit the contractor with $100m. There is now $100m more money circulating in the economy

- Govt sells a $100m bond to ANZ: Balance of ANZ Settlement Account reduces by $100m, Crown Settlement Account increases by $100m, ANZ now have a $100m bond (instead of the $100m they had in their settlement account). ANZ will generally onsell that bond into the economy. The net impact is that $100m circulating in the economy is now stored in the form of a bond. Bonds are highly liquid financial assets - not much difference to cash (just safer!). Note that Crown net worth is unchanged when bonds are sold - they just have a liability in the form of a bond instead of a liability in the form of a Settlement Account deposit at RBNZ

- RBNZ buys a $100m bond from an ANZ customer (QE): RBNZ credit the ANZ Settlement Account with $100m, ANZ credit the bond seller with $100m, RBNZ take ownership of the bond (their balance sheet now shows $100m of extra liability in settlement accounts, and $100m of asset on the asset side). This basically reverses the bond sale . The net impact is that there is now $100m of cash circulating in the economy instead of $100m of bonds. Crown net worth is unchanged.

- Crown receives $100m tax from an ANZ customer: ANZ customer account is marked down by $100m, ANZ Settlement Account is marked down by $100m, Crown Settlement Account is marked up by $100m... So, Crown net worth increases by $100m, there is $100m less money circulating in the economy.

OK. So as you say, if the money supply has not been expanded, why is there any need for quantitative tightening? It is benign and just a balancing act between govt and central banks.

I am not sure that there is any need for tightening at all personally. What I would say is that investors do need Govt bonds in their portfolios. Large pension and investment funds rely on having super low-risk financial assets like Govt bonds in their portfolios to balance their risk. Once you realise that the primary purpose of Govt bonds is to provide a safe store of value for investors, the world makes a lot more sense!

That is well explaiined JF. You can see the split in balance of RBNZ bond purchases (directly from Treasury and in open market tenders) as the crown settlement account and bank settlement accounts are +$27b and $37b respectively over the year.

So central bank independence has been conveniently forgotten...

Regardless of whether the RBNZ sells Treasury bonds on the secondary market, or sells them back to Treasury, it would be a form of quantitative tightening that reverses the original quantitative easing (QE).

The only way for avoidance of quantitative tightening would be for the RB to forgive the debt and write off the asset from their books. That could happen but it would be controversial.

Under normal circumstances, the Government would have to issue new bonds to pay for the old bonds that it was buying back. The question then becomes one of whether the purchasers of the new bonds are from New Zealand or overseas.

Regardless of whether or not the RBNZ actively sells existing bonds, there will be approximately $7.5 million of bonds that Treasury will have to redeem in 2023. But $7.5 milllion might not be enough to have a clearly measurable effect on market interest rates give the current slack in the system with large amounts sitting in settlement accounts.

KeithW

The only way for avoidance of quantitative tightening would be for the RB to forgive the debt and write off the asset from their books. That could happen but it would be controversial.

Which supports what I say. But why would that be controversial?

Because it implies that debt doesn't matter.

But if debt doesn't matter, money loses an essential belief-prop. It's like keeping laws, police and courts - but forgiving punishment; what would a crime be 'worth'? And belief can evaporate rapidly.....

It would be hugely controversial because it would show that Govt is prepared to hold debt in the form of deposits at RBNZ (in settlement accounts earning next to no interest) instead of in the form of bonds that pay interest. This might reasonably lead people to question why Govt is choosing to sell interest-paying bonds to the private sector at all.

It would be controversial because it would provide strong confirmatory evidence that QE was part of a long-term funny money policy rather than a short-term response within the economic cycle.

KeithW

Well that's kind of the reality in the U.S. and Japan

Both USA nd Japan have very important differences to NZ re appropriate monetary policy. Being the global currency changes many things. And Japanese consumer behaviours are also different to NZ.

KeithW

It is amazing how hard central banks are having to work to maintain the mirage of both independence and the public perception that the Govt is 'borrowing' money from savers. Maybe the 'funny money' moniker better describes the whole world post Gold Standard, and we are now seeing something emerging that actually makes more sense?

Stop press: “Government will probably have to issue more debt than planned to help Government”

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.