By Gareth Vaughan

In a bold statement, auditing and financial advisory firm PwC says New Zealand's big five banks are "well positioned to deal with anything they are confronted by," and, with net interest margins having bounced back from global financial crisis (GFC) lows, they've built up a buffer to compete head on for business in an environment of ongoing low credit growth.

Speaking with interest.co.nz in a Double Shot interview on PwC's latest bi-annual Banking Perspectives report, PwC financial services partner Sam Shuttleworth said the major banks - ANZ NZ, ASB, BNZ, Kiwibank, and Westpac NZ - "have got their groove on." PwC's report covers the six months to March 31 this year.

"When you compare the results with the previous six months it's basically a mirror image," Shuttleworth said. "There's a bit of ups and downs but it's largely flat. So to me that indicates that the momentum of the banks is there now. They understand their risks, they've positioned themselves well, they've got through the various pains they've experienced over the last four years," Shuttleworth said.

"The banks have got their groove on, they've learnt from the lessons of the past, and they're re-positioning themselves to deal with what's in front of them."

Asked whether he was confident the big five could handle whatever's thrown in their direction over the next next 12-18 months Shuttleworth said: "Based on what we know of today, they've got the skills, the knowledge, and I guess the balance sheet in the best position it could be to deal with anything that does come down from the Northern Hemisphere."

A key reason why PwC sees the banks in such a strong position is their declining dependence on offshore - especially short-term - wholesale funding. The firm notes that during the six months to March the big five's proportion of wholesale funding fell to 39% from 42% last September, and the proportion of overseas funding fell to 34% from 36%.

A recent article on bank funding from the Reserve Bank said before the GFC short-term wholesale debt, mostly from the US commercial paper market, was the biggest source of bank funding comprising about half total funding. But from 49% of total funding in early 2009, short-term wholesale debt had dropped to 34% by April this year with banks stepping up their use of retail deposits (47% of total funding at the end of April this year) and long-term wholesale funding such as covered bonds.

Strong net interest margins give scope for 'head on' competition

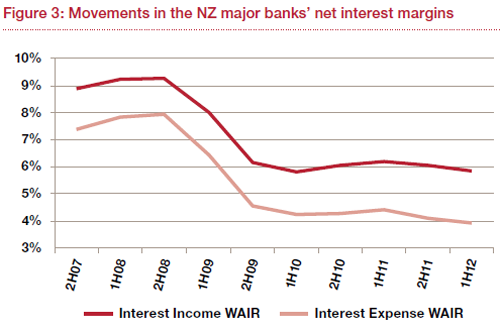

The five banks reported an average net interest margin of 2.40% for the period, up from 2.31% in the second-half of their 2011 financial years. That's well up on the 1.95% figure recorded by the Reserve Bank across all registered banks in November 2009, but is still well below some of the pre-GFC margins such as BNZ's 2.78% in the half-year to March 2003.

"The net interest margins reported by the banks are showing signs of strength and that has indicated to me that they have been very good at repricing their loans, but also maintaining their funding over the last six months," Shuttleworth said.

"Contrast that to the Australian (parent) banks for the same period and they're about 10 basis points lower. To me the margin at 2.40% means that they've got flexibility and they've got the ability to engage in a bit of competition to try and gain market share because we are off a low base of credit growth."

"The banks have got themselves a bit of a buffer there and we might see a bit of pressure on that margin as they compete head-on to bolster their residential mortgage books."

Banks have been competing hard for home loans and targeting each other's customers in a market that's growing at an annual rate of under 1%, with ANZ the big winner in the June quarter.

(The chart above and others below are taken from the PwC report. WAIR stands for weighted average interest rate).

Meanwhile, based on research by the Bank for International Settlements, the Australian parents of New Zealand's big four banks are the most profitable in the world based on pre-tax profit as a percentage of total assets. However, interest.co.nz broke out figures for the New Zealand subsidiaries - ANZ NZ, ASB, BNZ and Westpac NZ - with the results showing they're more profitable than their parents.

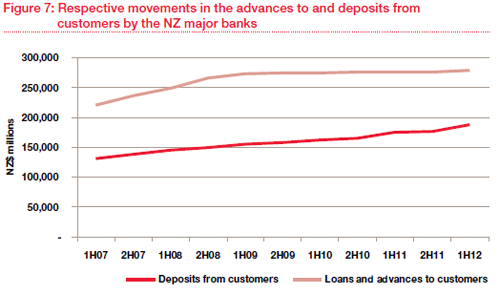

Deposit growth 6.9%, lending growth 1%

Shuttleworth said he was surprised to see deposit growth remain so strong. In the six months to March 31 the big five grew customer deposits by 6.9% or NZ$12.2 billion compared with lending growth of just NZ$2.8 billion, or 1%. The strong deposit growth has continued in the June quarter from most banks who have issued their general disclosure statements for the period thus far.

"I was really surprised to see the lift in customer deposits. I thought we may have hit a ceiling," Shuttleworth said. "I thought it (growth) was maybe going to slow down to 1 or 2% every six months but that 7% was a very sharp increase. I guess it's further illustrating the banks are looking at appropriateness of funding and making sure they've got a stable base. That is a good news story for the banks, which kind of helps them tackle anything else that might eventuate, especially what's happening in the European region."

Nonetheless he suggested the government's sharemarket floats of state owned enterprises, which are being marketed at "mum and dad" retail investors, might put some pressure on banks' deposit intakes.The latest Reserve Bank statistics show household deposits in New Zealand dollar terms up NZ$30.1 billion, or 40%, to NZ$105.78 billion at June 30 from NZ$75.68 billion in January 2008.

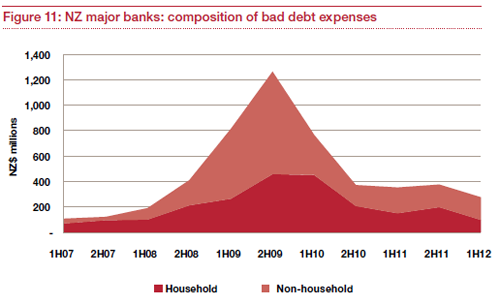

Tumbling bad debts

PwC said the big five banks' bad debt expense for the six months to March of NZ$277 million, down NZ $102 million, or 27%, is the lowest charge for a six month period since the first half of their 2008 financial year, before the full impact of the GFC.

"Household write-offs have dropped again and that's roughly about NZ$100 million for the six months. The corporate write offs, circa NZ$170 million, again they're tracking down as well. What I suspect is we'll still see a decrease in bad debt expenses, but maybe not to the same percentage drop of 27% for the next six months. Sooner or later we'll get the natural equilibrium of business as usual," said Shuttleworth.

Again this trend contrasts with Australia where the major banks have seen their bad debt expense deteriorate by 15% over the same six months.

Household sector provisioning as a proportion of the New Zealand major banks’ lending portfolios fell to 54 basis points for for the six months to March from 59 basis points in the six months to September 2011.

"Given household lending constitutes 63% of the overall lending of the major banks, the major banks will be encouraged by this trend," PwC said.

The non-household sector - business and rural loans - fell to 151 basis points from 153 basis points.

Impaired assets fell NZ$307 million over the half-year to NZ$3.418 billion and 90 day past due assets as a function of gross loans and advances are even lower than pre-GFC, dropping NZ$117 million in the half to NZ$$1.017 billion.

Less than NZ$2 billion needed to meet Basel III rules

Shuttleworth said a "back of the envelope exercise" done by PwC suggested the big five collectively need to raise about NZ$460 million of Tier 1 Capital and just under NZ$2 billion of Total Capital (including the Tier 1 Capital) to meet Basel III global capital adequacy standards, which the Reserve Bank plans to phase in between 2013 and 2018. The PwC figures exclude NZ$400 million worth of ordinary shares issued by BNZ to parent National Australia Bank in May, which has bolstered BNZ's capital position.

Shuttleworth doesn't expect any major problems for the banks in raising the capital required to meet the Basel III rules.

"We don't foresee this being a major issue because we've looked behind the capital levels and there are some qualifying instruments that are held by their parents which satisfy the Basel II rules but don't meet it under Basel III. So there might be a bit of swapping of the cards looking for these non-qualifying instruments to be redeemed with their parents to be replaced with other capital instruments that satisfy the tier one and total equity rules."

The country's biggest bank, ANZ NZ, alone may pay its parent NZ$1 billion in dividends this year.

PwC is the auditor for ASB, Kiwibank and Westpac NZ, three of the five banks covered by its Banking Perspectives report.

This article was first published in our email for paid subscribers this morning. See here for more details and to subscribe.

4 Comments

A bold statement.....lets remember it....

regards

In your article you refer to pwc as an 'auditing and financial advisory firm' Study after study has stated that these two functions need to be separated. But we do not seem to have the political will to do it. We know that it is not sensible for these two functions to be under one roof but we let a very small number of very large firms dominate the market

In the article you state that PwC is the auditor for ASB, Kiwibank and Westpac NZ, three of the five banks. Does this position as media commentator/promotor and auditor not seem a little conflicted. Would it not be better for audits to have more independence. say broaden the supply of providors of audit services and then have then appointed to such entities as banks and public companies on a rotational basis. That way the auditors would not be conflicted nor have the taint of conflict of interest on them

http://www.telegraph.co.uk/finance/9473360/PwC-faces-investigation-over…

A recent interesting article with many comments about the issues and challenges facing the auditing industry. It is indeed a difficult area and one where it may be better for the companies, investors and the auditors themselves if we did seriously look at changing how the audit system works in countries such as ours.

1. Are there enough firms conducting the audits of public companies?

2. Are the audit firms independent enough of their clients.

3.In reality who should be engaging the auditors- the management of the firm, the board, shareholders or some regulatory authority?

4. Are the auditing firms that handle the vast majority of public company audits simply too large and therefore too dominant?

Would it help provide a more robust audit if there were more providors, and if auditors were chosen by ballot rather than being appointed essentialy by the people they are going to audit? It does seem a little strange to me to continue on the way we do now and expect a better result somehow. But there seems little political will to tackle the situation.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.