By Roger J Kerr

The interest rate environment at the start of 2018 is certainly different to how it has been over recent years.

The global financial and investment markets have already voted with their feet in anticipating that inflation will increase in most western economies this year and that money printing in Europe is finally ending.

The result is material increases in US long-term interest rates over recent weeks from 2.30% to 2.66% as the super low yields in Europe no longer holds US yields down.

Outside of global geo-political shocks or risk events (resulting in safe haven buying of bonds), it is difficult to see who the big buyers of US Treasury bonds will be to return the yields to lower levels.

As US inflation and short-term interest rates increase through this year expect to see US long-term yields pushing even higher to 3.00%.

The implications for our medium and longer-term swap interest rates are obvious.

The rise in the oil price over recent months has also been a contributing factors to the higher US interest rate yields.

Shale oil production in the US provides a natural cap to continuing oil price increases and it appears that the oil market has sold prices too high, too quick.

I would not expect to see oil prices any higher - and a pull back to below US$60/b in Brent may be one variable that slows down the increase in long-term interest rates.

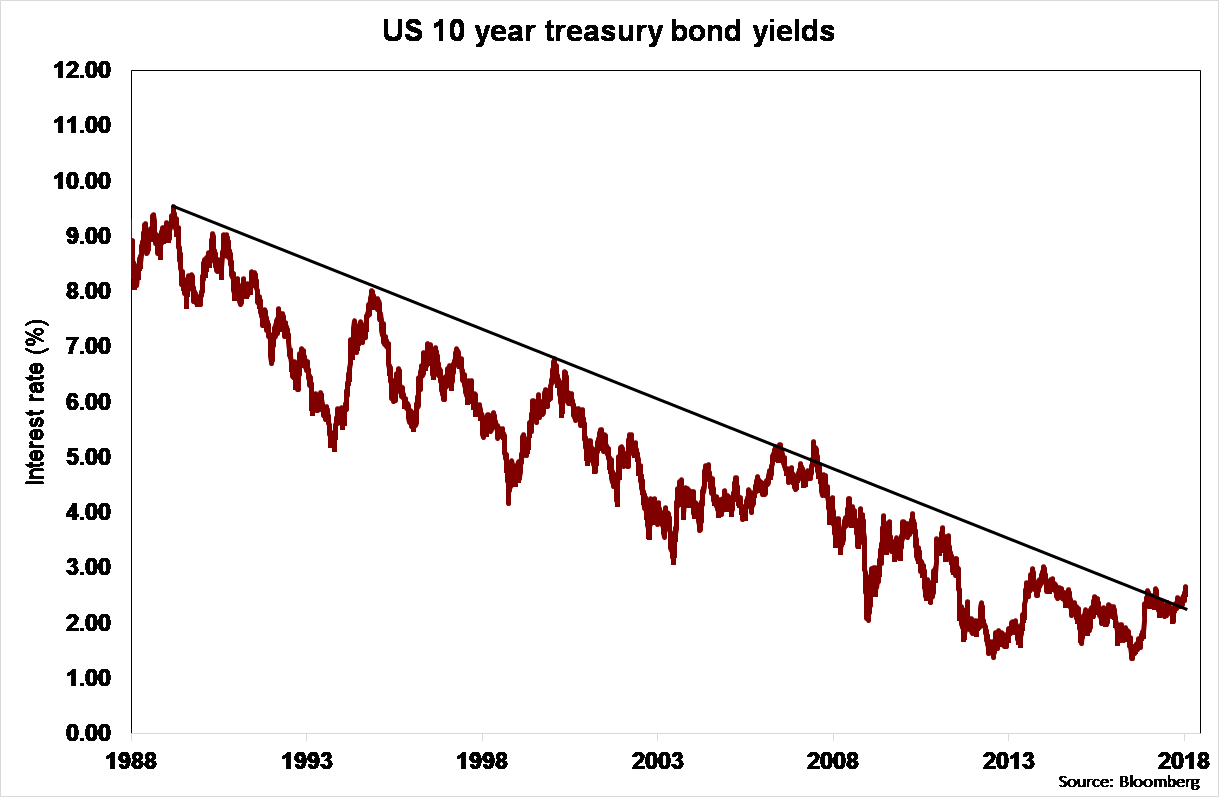

The chart below plots the US Treasury Bond “bull market” (yields lower, bond prices higher) that has run since the yields were above 9.00% in 1988.

The Fed Chairman in the mid 1980’s, Paul Volcker (those with grey hair such as myself will be old enough to remember him!) was very successful in taming the inflation beast that started the decline in interest rates.

The bond market threatened to move yields above the downtrend line in 2008, only to be gazumped by the GFC.

Today the downtrend line is again under threat as the world economy finally moves on from the super loose monetary conditions that were required after the GFC.

Daily swap rates

Select chart tabs

Roger J Kerr contracts to PwC in the treasury advisory area. He specialises in fixed interest securities and is a commentator on economics and markets. More commentary and useful information on fixed interest investing can be found at rogeradvice.com

3 Comments

I along with savers and baby boomers hope he is right ................ but anyone with a mortgage should be hoping he is wrong .

I dont see inflation or interest rates as a real threat

The Bond and debt markets are , however.

ETF.com seems to think along the same lines:

Analysts have been predicting it in almost every year since the financial crisis―the rise of long-term bond yields. But each year they've been off the mark, with 2017 being no exception. Despite three Fed rate hikes last year (and four in the past 13 months), the U.S. 10-year Treasury yield actually declined, inching down from 2.44% at the start of 2017 to 2.41% on Dec. 29.

In 2018, that won't happen―not unless the yield curve inverts (which it very well might). It's simple math. If the Fed hikes rates another 0.75% in 2018 as it's currently projected to do, the two-year Treasury yield, which tracks the federal funds rate closely, would likely jump to 2.6% or more.

Either the 10-year yield would have to also climb, or there would be a 10-year/two-year yield curve inversion. Investors fear an inverted yield curve, because one has preceded every recession of the past 40 years, according to the St. Louis Fed.

All this means investors can't expect the same ho-hum bond market they've grown accustomed to. Fixed income might finally start to get interesting in 2018.

Source: http://www.etf.com/sections/blog/big-market-predictions-2018

Most bonds are offering not much more than term deposit rates, even on an initial offering. I do not consider these rates worthwhile at the moment.. If predictions are right these bonds are going to be worth less in 6-12 months time if you have to cash up.

Property investors, who have relied on the tax free capital gain in the past will take a big hit if interest rates rise. Property investors who have bought in the last 4 years will be getting a net return less than a term deposit rate.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.