Kiwibank's economists see a fairly strong chance that the Official Cash Rate will go as low as 0.75% next year, while they're predicting that the Kiwi dollar, "our beautiful bird", is about to be "broken".

In a Kiwibank 'Our Take' publication, chief economist Jarrod Kerr says he's confident interest rates will fall further "and remain at or below historic lows for a very, very long time". The Kiwibank economists are forecasting two OCR cuts this year, starting in May, which would take the OCR down to 1.25% from its current 1.75%. But then there may be more.

"We’d put a 40% chance of another 50bp cut in the OCR to 0.75% in 2020, if conditions worsen. Beyond there, the RBNZ could cut to 50bps, and would entertain the use of QE, currency intervention, and firing up Government investment.

"The RBNZ’s QE could buy Govt bonds with the understanding the Govt ramps up fiscal investment. And the RB can easily print and sell the currency. But we’re still quite some way away from entertaining QE.

"The point here is, we have plenty of ammunition if needed," Kerr says.

On the Kiwi currency, Kerr says it will do what we need it to do, when we need it most. If not, the RBNZ will intervene.

"We forecast a volatile descent for the bird this year. The Kiwi should drop into the low US60s by year end. RBNZ rate cuts will accelerate the Kiwi’s decline.

"At US68c today, the risk is asymmetrically lower, in our opinion. Threats of recession offshore, could see the bird drop into the US50s."

In explaining the current economic backdrop, Kerr says there are three bug bears frustrating the outlook for Kiwi growth.

Lack of confidence

"The first, is the lack of confidence. Firms remain wary of the outlook. A lack of business confidence may disrupt hiring and investment decisions.

"The second, is the Australian property market. The housing market is tumbling (mainly in Sydney, Melbourne and Perth). The sharp decline in Australian house prices is thought to represent a yellow canary down the coalmine for Kiwi housing. We disagree.

"The third, is the rise of populism and protectionism. We wait with baited breath on the outcome of US-China trade negotiations and Brexit. Both events spawned by a rise in populism."

Kerr says global growth is "grinding lower", and political risk, including Brexit and US-China trade, has sapped confidence.

"A deteriorating global outlook can quickly impact New Zealand. We don’t have to look too far for evidence. Kiwi Businesses are worried about their own outlook for activity, and profitability. The economic woes offshore are weighing on Kiwi confidence. And a lack of confidence can quickly lead to a lack of growth. The latest QSBO survey showed a marked decline in confidence.

"So the RBNZ are highly likely to step in. We expect a 25bp rate cut in May, followed by another 25bp cut in (June or) August. The markets are still exposed to a quick move."

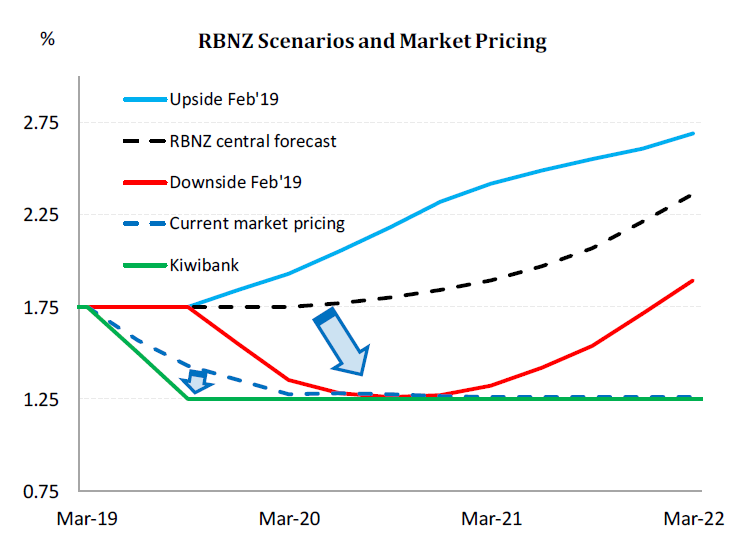

The chart highlights the upside, downside and central scenarios set by the RBNZ just 6 weeks ago.

Kerr says It seems we’re headed down the downside (red). The Kiwibank cash rate forecast (green) and market pricing (lighter shade of pale blue) have moved to match the downside (red) scenario.

"There’s still plenty of room to move more. Interest rates markets are about hedging risk. And once the RBNZ starts cutting, the risk is automatically titled towards the bank doing more. Indeed, we’re calling for 50bps worth of rate cuts to 1.25%. Our economy is still reasonably strong. But, if international developments worsen, the RBNZ will do more.

"We place a high 40% probability of follow-through rate cuts in 2020. Again, 50bps may be required, taking the cash rate to 0.75%. The point here is, the market will price more than the RBNZ deliver, until the cycle turns."

"Current market pricing has a slow decline to 1.25% by mid-2020. We see the risk of a rate cut in May, followed by a rate cut in August, possibly June. [RBNZ Governor] Adrian Orr has clearly elevated the importance of OCR announcements with last week’s change in stance. So we could be at 1.25% by mid-2019 (not 2020). Beyond the middle of this year, the market will have to price in the risk of another rate cut or two."

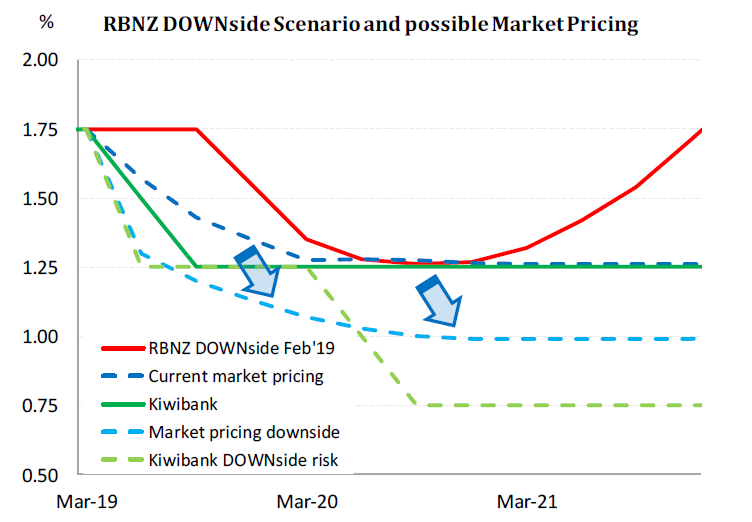

Kerr says the chart below highlights the current RBNZ downside scenario, current market pricing, Kiwibank’s central scenario (1.25%) and Kiwibank’s downside scenario (0.75%).

"Market pricing should move to the light blue line between the Kiwibank scenarios. The 2-year swap rate should fall to a 1.30-1.50% range. And that will lower 2-year fixed mortgage rates. The Kiwi dollar should fall too," Kerr says.

"Our beautiful little bird is about to be broken. The Kiwi is likely to enter a downward spiral in coming weeks or months," he says.

Up until recently, the Kiwi has been flying high. The strength of our terms of trade (strong export prices relative to soft import prices) has supported the currency.

"We’ve seen the Kiwi hit a high of 0.6970 in December, and a few retests of the high in January, February and a push to 0.6939 in March. Our flightless bird often finds herself at lofty heights. We think it’s time for a timely descent to more reasonable levels. The RBNZ provided the first airpocket with the March OCR statement, leading to a 1c drop on the day. After a slight updraft, the bird was weighed down by the QSBO survey yesterday.

Kiwi fall will lift our economy

"It will come as no surprise that a lower Kiwi currency will provide a much-needed lift to our small, open economy. The problem with currencies, is they’re a relative price. Unlike magnificent interest rates, that can all fall together, currencies are a different beast altogether. Currencies can’t all fall together. Today, we have a US Fed on hold, and talking about ending QT. So the USD is not going to be as strong as (everyone else outside the US) hoped. The UK has Brexit to contend with. The EU has the EU to contend with. And the Aussies have a housing correction to contend with.

"In order to stand out, just for a moment, we need to look relatively worse than a bad bunch to get a currency decline. Adrian [Orr] understands this. In bad times Japan will repatriate, and the Swiss have a nice hiding place."

Kerr says if we cut our interest rates before Australia the NZ-Australia currency crossrate should fall.

"If we cut twice and signal anything can happen from here, well, all of a sudden, the USD, the Euro, the Yen, the Swiss Franc, and possibly even the Pound (ok maybe a step to far), look more attractive - at least for a little while.

"After the volatility subsides, the 50bp reduction in our interest rate advantage over much of the developed world should hold the Kiwi dollar in a lower trading range. And the 50bp reduction in the OCR takes us that much further beneath the global benchmark for interest rates, US Treasury yields.

'The flying Kiwi descends'

"Let’s say that happens. Let’s say the RBNZ cuts 50bps. Let’s say the RBNZ leaves it’s commentary open-ended, and allows the market to price in the risk of more cuts (no harm in doing so). Then the flying Kiwi descends, and should end the year close to 60c."

Kerr notes that in currency terms, against the "Aussie battler", the Kiwi was "dominant – like a rampaging All Black pack trampling over a weakened Wallaby".

"We’d love to see NZDAUD parity. But such a strong NZD/AUD hurts our manufactured exports.

"A strong NZD/AUD is great if you’re wanting to buy an Australian canary yellow cricket jersey, loose fitting for underarm bowling, with a complimentary strip of sandpaper. But generally, we prefer a weaker Kiwi/Aussie cross. Because it helps our Kiwi expats in Australia import the black jerseys."

48 Comments

Is it time to load up on big ticket purchases from overseas then? or is that what firms and households have already done last year?

Perhaps purchase US dollars, and back again to NZD later on...

Out of curiosity, are there any private i.e. non-bank money changers who change currency at more attractive rates than the banks? Kiwi banks really gouge you when changing currencies - and I am talking major currencies here like USD / GBP / EUR and not those currencies from smaller countries on which you expect a much wider spread between the buy and sell prices.

When I was an expat in Asia, local money changers offered exchange rates with a tiny spread so you could change money any time and the cost in doing so was absolutely negligible. Are there any such money changers anywhere in NZ?

PaulO. Years ago we used HiFX. We were initially nervous giving our money to a non bank. Over time we built up transactions to property settlement type deals with no problems. However from memory they only changed currency for genuine reasons. They wouldn't/didn't do speculative transactions. But they saved us thousands$ in conversions costs.

Check out TransferWise, EDIT for NZD->USD the fees are 0.38% + 2.51 NZD. You get the exact exchange rate to four decimal places. Is there anywhere else where you get a better deal than that?

Yes. Safest bet is to buy some US dollars. Gold may go up (or down) but if you have a balance of other currencies you will be well positioned.

Hopefully I can get my NZ funds over to the US and in low cost index funds before the rate cuts weaken the currency much further.

No, I won't be investing in "property".

Not sure you'd want to be buying too many US shares at this point in the cycle...seen the PE/CAPE ratios of US stocks?

True, really high. Even Buffett is finding it difficult to find US stocks to buy right now, but there are a few (mainly in the financial sector, that he has still bought recently) with P/Es from 10-12 that could be held long term. Other than that, it's looking expensive. The NZ market too, having risen fully 300% in 10 years.

Are you playing the bond markets Voiceofreason? In terms of the expected drop in interest rates?

Interesting indeed. If you take a quick and dirty shortcut by assuming the natural rate is best guessed by the 2 year government bond, currently at 1.41%, then the RBNZ is already behind. The current rate of OCR at 1.75% now looks contractionary. Judging by the new governor's very dovish tones it should already be at 1%. That should give the new committee lots to frown about and discuss most seriously.

One might be tempted to sack a good half of them and just set the OCR at the two year bond rate, unless there is a war or other national emergency.

https://www.interest.co.nz/charts/interest-rates/government-bond-rates

And with inflation still in the 1.5-2% range, guess what this does to effective (after-inflation, after-tax) TD returns.

Plus inflation has just gotten a wages cost-push on April Fool's day, coupled with a weaker dollar for imported inputs like fuel which means price rises across the board......

Hey ho.

Agreed, minimum wage hikes just adds to NZ's inflationary pressures.

Surely even the most naive politicians understand raising minimum wages to ultimately $21/hr is a zero sum game. Which makes me think, aside from votes, is there an ulterior motive here?

Buying votes through virtue signaling, that would be my guess to the motive. Or maybe they are getting too much credit and are really just a bunch of incompetent idiots.

I wish I understood whats actually going on

I agree. I cant help but feel like we are missing a few pieces to the puzzle

The world is slowing. That is what the government bond yield declining means. The bond markets figure it out months before the central bank bureaucrats see it in the data and respond. They are paid to be serious and responsible, whereas the bond market is paid to be right.

As bond yields decline in Europe, the big money goes elsewhere, Aus and NZ are seen as fairly reputable places, better than most.

Roger,

As James Carville said in 1992; "But now I want to come back as the bond market,then you can intimidate everybody". Plus ca change......

Aus and NZ are seen as fairly reputable places, better than most.

so why NZ pulls the rates down artificially??

Maybe it's a long drawn out OBR by stealth?

Will make my bitcoin even more valuable in NZD terms

You've got to sell them first.

Some plonker in DPRK will buy it

Somone put a buy of 10,000 BTC (Bitcoin)...

Market shot up 25%

Roger is right in general terms but the space for rate cuts to re stimulate from a recession historically - at least since the 60s have been between 3 & 6 % reduction. No stable capitalist country has that room and the level of debt and disruptive events past present & future globally means this next recession/depression will be brutally ugly. QE an outside chance white knight, a war, a Jubilee, saved by Aliens all possibilities. Understand why the Elites are kicking the can, hope I have a year or so to sort out my own finances. At such rates how many pension funds will be in deep do do - just asking for a friend!

When Don Brash was Reserve Bank Governor he anguished over cutting the rate by 25 basis points, X weeks later nothing happened so he cut again by 25 basis points still wringing his hands and nothing happened so he cut another 25 basis point y weeks later. I think something happened then. Moral of the story. Don't frutle around with minor bites. Knock the problem on the head, that is if you think there's a problem in the first place. I concur with Boatman.

why are we hell bent to become poor by devaluing our own currency?

While we have a terms of trade deficit we will continue to keep getting poorer. We should be devaluing our currency until our terms of trade balances

And devaluing our currency does not make us poor, it makes us richer. The only way NZ makes money is by selling stuff overseas, with a lower XR it is easy to sell more. Even if we don't sell more, we get more NZD for what we currently sell. It is only your flat screen TV and petrol that are more expensive, and that seems a reasonable sacrifice to ensure we are only spending what we earn (as a country)

Not just flat screen TVs - everything that's imported.

Money manipulation doesn't make us richer in the end.

Would you agree that if we have more money coming into the country than going out we will be richer (as a country)?

Well, that is never going to happen with so much foreign ownership in just about everything here now.

You know that is just not true, right? The NZ national accounts clearly show that domestic ownership of our economic assets is at a cycle high - and that may be an all-time high - the reliable records for this only go back a couple of decades.

So where do you go if you actually have substantial cash savings? Not sure about USD. When SHTF, JPY is always a good bet. GOLD ETF looks safe, but you don't know if JPM, Vampire Squid, etc will suppress the gold price. Silver ETF (EPTMAG) is a possible safe haven. The price has already been suppeessed to the point where it can't really go any lower (one would think).

Property or shares of course

Don Brash was one, if not the worst RB governor we ever had, his misguided actions left a crater in the economic base of this country that has been filled with poverty eversince. As for the weak NZD it never lasts long nor is it beneficial because we need imports to produce our exports so the inflated cost of those soon push up the dollar again and we lose the low currency advantage. The low interest rates might see some long overdue capital investment in our industrial base, which might help improve productivity if we can find the management talent to go with it....

Later on under Bollard we had interest rates up over 8% supposedly to cool the economy, particularly the housing market. That was too much,too late. The GFC did the actual work. Seems to me that cheap, cheap finance may stimulate business growth, but more likely, it can encourage imprudent borrowing and wayward spending. Don’t think our good,sound, prudent and efficient farms and businesses are staggering under the weight of finance anyway. Unfortunately this government has introduced too much uncertainty by way of mixed messages, too much consultation on one hand, too little on the other. Forward planning is difficult enough, but when the water under your boat goes muddy, best practice, haul in the sails.

Looks like Jon Key was right, the NZD is heading to $0.50 USD its fair value...

Time to buy Gold/BTC as the only asset class's not printable by governments.

or maybe just load up on debt and wait for inflation to eat it away.

Interesting outlook, thanks for the article. Might be a good time to stack up some US dollars or US dollar assets in that case.

As for this: "The sharp decline in Australian house prices is thought to represent a yellow canary down the coalmine for Kiwi housing. We disagree." What's the explanation for "we disagree", apart from perhaps: fully 88% of all Kiwibank's loans are mortgages, so we have a massive interest in house prices not tumbling like in Australia.

We agree to disagree

In the source publication ('Our View' by Kiwibank Economics) they have a link to a video where Jarrod explains this statement. Watch it.

TLDR: Australia has too many houses (over supply), more cautious lenders (hesitant banks) and no more foreign money pumping up housing. The main difference here in NZ is that we have a severe shortage of housing which will keep prices inflated.

Be interesting to see what happens to mortgage rates if OCR goes down 1%. Can, will banks pass it on. I guess depends on how much money savers are saving in our banks and overseas bank borrowing costs

Regardless of what the mainstream media are reporting about our economy, the RBNZ is spotlighting a house of cards.

Buying USD is not the solution. Kicking out the current socialistic Government is the need of the hour.

That's a non sequitur. The debt-fueled bubble we are now seeing the fruits of was carefully nurtured by the previous governments.

Just seems like central banks are now nervous that more people are becoming reluctant to take on ever larger debt to live outside their means, thus the call is for "Cut! Cut! Cut! This only works if the next person comes along with more spending."

These forecasts are ludicrous!

We would have to be in serious recession to get down to 0.50 otherwise how will we deal with GFC 2.0

Cutting so our dollar = 60c to the USD means a 15% rise in fuel costs and other imports.

So imports go up and the cost to transport them goes up, meaning inflation will rise easily over the RBNZ target range.

People will have less money and consumption suffers and people start losing jobs.

Given the RBNZ has a mandate of stability, employment and target ranges, I cant see big cuts like this unless things get absoluetly dire.

Hopefully next time the KB economics team can tone down the dopey metaphors a bit. Talk about insulting the reader's intelligence.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.