By Gareth Vaughan

As the Australian Government lines up its Productivity Commission to probe banking competition, should New Zealand's do the same?

Australian Treasurer Scott Morrison recently said his government was ready to act on a Financial System Inquiry recommendation that bank competition be investigated. According to The Australian Financial Review, the Australian Productivity Commission is likely to be asked to consider whether the Australian Prudential Regulation Authority (APRA) gives sufficient consideration to competition issues. This comes with Australian Securities and Investments Commission (ASIC) chairman Greg Medcraft recently describing the banking sector as an oligopoly.

The Australian oligopoly consists of the ANZ Banking Group, Commonwealth Bank of Australia, National Australia Bank and the Westpac Banking Corporation. Here in New Zealand their subsidiaries - ANZ NZ, ASB, BNZ and Westpac NZ - dominate.

In a research note Deutsche Bank's Sydney-based banking analysts Andrew Triggs and Anthony Hoo point out a statistic commonly cited to demonstrate the oligopoly's dominant marketshare is the four's slice of the residential mortgage market. Using APRA's measure of the system it's 83%, and under the Reserve Bank of Australia's statistics including non-banks, it's 77%.

Based on Reserve Bank of New Zealand mortgage figures and the big four NZ banks' December general disclosure statements, the big four here have 90.2% of the home loan market.

How about a Productivity Commission probe of NZ bank competition?

Back in 2015 I suggested the Productivity Commission ought to probe banking competition in NZ. I cited big banks' dominance of KiwiSaver, high fees, high credit card interest rates and world leading profitability.

I also noted there is competition from the likes of Kiwibank, TSB, the Co-operative Bank, SBS, Heartland Bank, HSBC, Rabobank and other banks including three of China's big four, plus building societies, credit unions, finance company survivors and peer-to-peer lenders. Despite this competition, and the relative ease these days of switching banks, the big four have thus far been very good at holding marketshare.

My article was met with an underwhelming response from interest.co.nz readers. It attracted just one comment and was not among our better read stories. Does this mean bank customers are happy with their banks? That they take it as a given the big four's dominance should be probed? Or was it simply because I failed to include 'Auckland house prices' in my headline? I don't know.

But if the Australian review of banking competition gets underway in this NZ election year, it'll be interesting to see if there are any calls on this side of the ditch to follow suit.

Interestingly during Chinese Premier Li Keqiang's recent visit, Prime Minister Bill English welcomed the rise of Chinese bank lending in NZ from the local offshoots of the Chinese government controlled banks ICBC, China Construction Bank and Bank of China. English noted increasing competition for the dominant Australian-owned banks.

“We welcome some competition,” English said.

“We’ve got a very concentrated banking sector - probably more than most other developed countries - and it’s good that the conditions in New Zealand are such that smaller banks, including our local New Zealand-owned banks, are able to grow,” English said.

'A sole focus on marketshare would be misplaced'

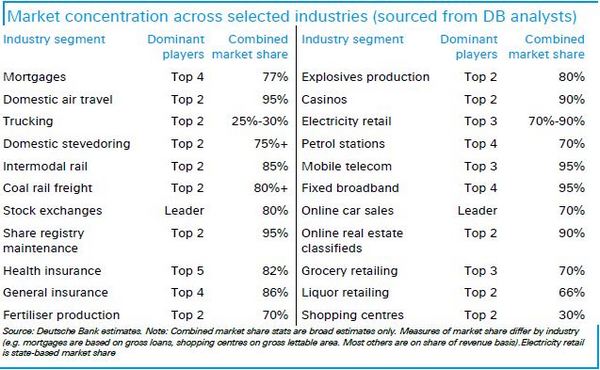

Back to Deutsche Bank's Triggs and Hoo. They point out the type of mortgage marketshare enjoyed by Australia's banking oligopoly is not unique in an Australian context. (And nor, of course, is it in NZ where even greater market concentration is not uncommon such as in general insurance, supermarkets and building materials).

Say Triggs and Hoo; "Most industries in Australia tend to be highly concentrated. As such we would argue that policies expressly aimed at reducing major bank marketshare would be misguided and could potentially introduce greater risk into the financial system. Are there factors supporting structurally high banking sector concentration?"

Although acknowledging competition should always be encouraged, the Deutsche Bank analysts argue there are factors suggesting concentration will remain structurally high. These are;

i) A concentrated market makes prudential regulation easier;

ii) Big banks tend to have more extensive branch networks for customers; and

iii) Big banks with high return on equity and better risk management supports financial system stability.

"Arguably, greater digitisation in banking reduces the second argument, however we think concentration is likely to remain high. That’s not to say that the Government shouldn’t try to improve competition in the industry, e.g. by reducing barriers to switching between banks, however we argue a sole focus on the marketshare of the big four banks would be misplaced," Triggs and Hoo argue.

The chart below comes from Deutsche Bank.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

12 Comments

Tell me more about those Auckland house prices....

By the nature of the special position of banks in payments system, banks are incentivised to coordinate and move lock step one with the other. For instance, we see all major banks have economists who ostensibly discuss the economic outlook, but no doubt use this means to signal one to the other as to what to do next: loosen credit or tighten credit, lend to investors, or not etc.

I agree about the need for a review of competition in NZ banks, but unsure of what the possibilities for improvement are, even if the banks are found to be oligopolistic?

NZ is open to more banking competition but is not a particularly alluring business prospect because of a tiny GDP and small population. Who would want to compete for a tiny share of a tiny pie? Isn't this the overall cause for the lack of competition in most NZ sectors?

And yet here they all are:

Kiwibank, TSB, the Co-operative Bank, SBS, Heartland Bank, HSBC, Rabobank and other banks including three of China's big four, plus building societies, credit unions, finance company survivors and peer-to-peer lenders. Plus the big 4 Aussie banks..

The question in my mind is; 'why'. What do they know that we don't!!

Compared to other OECD countries, that's a tiny, tiny number of banks.

Plenty of banks in NZ to choose from,the only problem is that they all offer the same thing.

ANZ is always rated lst on customer experience etc but nobody ever leaves them and that goes for the other big banks as well.

There doesn't seem to be a point of difference amongst banks in NZ.

Are ANZ ranked first? Last time I looked they and Westpac jointly had the lowest satisfaction scores unfortunately.

Agreed about there being no point, it's not like a startup can go out and get a banking licence. That's why banking is so attractive, there are very high barriers to entry.

Actually there was a real point of difference between the Big Four australian banks and Kiwibank up until the end of February where our government only allowed a bailout to Kiwibank customers in the event of a systematic bank failure. Unfortunately this guarantee has now just expired, but as far as the Credit Ratings go, Kiwibank still holds a strong position because in the unlikely event that it suffers a fianancial collapse, it is one of the only New Zealand banks that the government would be likely to bail out of trouble, unlike the other big banks which won't be bailed out because they are Australian owned. So in that context, I keep term deposits with a local bank and keep everything else to a minimum with that other lot. The OBR also known as the Open Bank Resolution is detailed on the RBNZ website and is a telling piece of advice, should your bank hit the wall and find it's assets frozen overnight.

I am pleased to see this article. For decades NZers have been "over it" from high fees and exorbitant credit card fees and mostly feel helpless. I switched from Westpac to Cooperative Bank and love their service and the fact it's NZ owned. Perhaps if ever the OBR is used the NZ owned banks may be safer as their asset ratios are higher to their loans.

It's political sleight-of-hand

I might be right - I might be wrong - but IMO the Productivity Commission enquiry into banking is a sleight-of-hand gesture

With the scandals that have plagued the big 4 banks over the past 2 years there have been 2 Senate Equiries that have led to demands for a Royal Commission into the culture and behaviour of the banking system

The Liberal National Party have been absolutely desperately ruthlessly opposed to holding a Royal Commission and in my opinion (again) the calls by ASIC and ACCC Medcraft are paid-for-elites stooges doing the Coalition bidding which is being used to mount a Productivity Commission enquiry into competition when the called for Royal Commission would examine the fraud committed within the banking system

Interesting that the Fraud, the cover-ups and the Senate enquiries have hardly been touched here in NZ

Anyone who thinks the same events are not happening here in NZ are dreaming

PS: This little scrap has been going on for about 3-4 years

The sub-prime mortgage fraud that has been going on in Australia is starting to surface now. So far we have only seen the tip of the iceberg. I'm not convinced that the Australian Banks are that sound when they are desperately trying to attract local depositers to keep up with their customerrs insatiable appetite for borrowing funds to buy Real Estate. Something is about to give and rising interest rates in the US will most likely be the trigger for a sudden collapse of house prices in Oz, because the banks are now going cap in hand to the US banks for further funding.

Sorry Gareth, but I have to say by and large I am happy with the way things are.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.