Summary of key points: -

- Kiwi dollar temporarily de-couples from AUD/USD correlation

- Pressure builds on RBNZ to hike interest rates

- Sources of current inflation cannot be influenced by interest rate changes

- Downward correction in the Kiwi dollar still has further to run

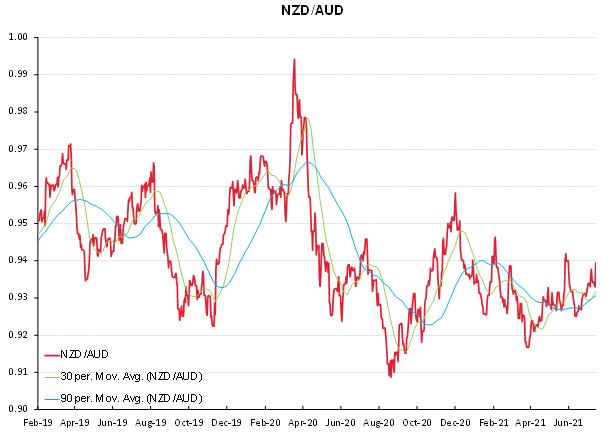

Kiwi dollar temporarily de-couples from AUD/USD correlation

After several months of US economic events/outcomes and US dollar movements dominating the NZD/USD exchange rate direction, domestic inflation and potential interest rate changes here took over as the main focus of the financial markets over this past week.

The end result after all the machinations, speculations and paralysis by analysis on local inflation and interest rates, was that the Kiwi dollar ended the week at 0.7000 against the USD, very close to the value it commenced the week.

However, the apparent stability and lack of response to monetary policy changes as inflation ramps up, belies some significant developments on where the NZ dollar is now valued. Over recent years the NZD/USD rate has generally maintained a consistent five cent gap below the AUD/USD rate, resulting in the narrow 0.9200 to 0.9400 trading range in the NZD/AUD cross rate. In remaining at 0.7000 after last week’s events, the Kiwi dollar today is now only four cents below the AUD/USD rate at 0.7400. The RBNZ monetary policy review statement last Wednesday and the higher-than-expected inflation numbers on Friday prevented the NZD from following the AUD lower against the USD, resulting in a dramatic spike up in the NZD/AUD cross-rate from the 0.9300 area to 0.9460. Had the RBNZ monetary statement been more neutral in tone and the inflation outcome closer to prior forecasts, the NZD/USD would be trading closer to 0.6900 (tracking the weaker AUD against a stronger USD on global FX markets).

The historical pattern of NZD/AUD movements over recent years is that the sudden spikes upwards or plunges lower never last too long.

Currency speculators move in to profit from the misalignment always correcting itself i.e. they bet that the five cents gap between the NZD/USD and AUD/USD rates will rapidly return. Therefore, the current four cent gap in the two exchange rates is unlikely to be sustainable.

Local AUD importers should be immediately increasing their hedging percentages to policy maximums and exporters in AUD’s should be using existing hedges at lower levels and not converting or hedging at current cross-rates above 0.9400.

Pressure builds on RBNZ to hike interest rates

Whilst there was widespread “shock, horror and panic” responses from the local financial media and bank economists to last week’s monetary policy and inflation events, at the end of the day after due reflection not a lot has really changed. The markets were surprised that the RBNZ announced an abrupt ending to the LSAP programme (they expected a progressive phase out), however the RBNZ’s weekly bond buying had already reduced significantly as the banks were awash with cash they were not lending out into the economy.

The RBNZ did signal that the balance of risks with inflation and the economy had shifted and therefore (like other central banks) it was time to commence the process of unwinding the emergency Covid related monetary stimulus implemented 12 months ago. There should not have been any real surprise at that messaging. There are still sufficient caveats, conditions and out-clauses in the RBNZ statement wording to allow them to delay that unwinding if Covid risks to the economy re-emerge.

The local interest rate markets are now pricing-in an 80% probability that the RBNBZ will start increasing the OCR interest rate next month. Bank economists are adamant that the economy is currently “overheating” and that the RBNZ must act immediately to tighten monetary conditions with successive interest rate hikes.

Investors, borrowers and those with FX exposures should be somewhat circumspect and perhaps a little cynical about the motivations behind these calls from excitable bank economists. Their claims that the economy is overheating looks about as accurate as their forecasts 12 months ago of the economy plummeting into the abyss and their forecasts/pricing six months ago that we were heading to negative interest rates as deflation was a higher risk than inflation!

Whilst some parts of the economy have certainly been stronger than expected over the last six months (housing, retail and construction), the main productive sectors are facing severe challenges and constraints (as we have been highlighting in this column) with product, labour and shipping shortages. Productive output in our major manufacturing and export industries is not going to be 5% up on a year ago due to these constraints. If the RBNZ officials and bank economists were a bit closer to the coalface of the economy in regional New Zealand there would be a realisation that the overall economy is far from overheating.

In any case, it would appear to be a very brave (or ill-advised) central bank that tightens monetary policy whilst their population is only 11.5% fully vaccinated against Covid. A community outbreak here similar to what Sydney has just experienced would have us in lockdown again and the RBNZ having to reverse any decisions to tighten policy. Governor Adrian Orr needs to resist being panicked into premature tightening action by banks who only have an interest in creating volatility in interest rates for their own ends.

Sources of current inflation cannot be influenced by interest rate changes

The RBNZ appear to be wavering on their previous viewpoint that current inflation increases are largely temporary (oil, freight, commodities etc) and they should “look through” such inflation increases and only tighten monetary policy when more permanent inflationary forces are evident (e.g. wage increases). The Reserve Bank of Australia is adopting this stance and are sticking to it, despite considerable pressure on them to shift their stance. Governor Orr would be well advised to follow the lead of the RBA and the Fed in how they are clearly setting pre-conditions and milestones for normalising monetary policy settings.

In 2009/2010 when Adrian Orr was running the NZ Super Fund, he instructed the buying of much cheaper equities when the world was selling. A brave stance at the time, that turned out to be correct and very successful. Once again, he needs to stand up against the short-termism and bullying from the local banks on the need for immediate interest rate hikes and chart his own course. For these reasons, this commentator’s view is that the RBNZ will not increase the OCR in August and that decision will be negative for the Kiwi dollar (which has now priced-in such increases) at the time. The four-cent gap to the AUD will return to five cents as the Kiwi dollar catches up to the weaker Aussie against the USD.

Dissecting the reasons behind why our inflation rate is now above the 3.00% maximum limit and what the RBNZ should do about it requires an understanding of the root causes of the price increases. The component parts of the Consumer Price Index need to be split into two parts, prices than can be influenced by dampening consumer demand with interest rate hikes, and prices that are supply-side driven and completely independent and not influence by the level of interest rates. Current increases in tradable inflation are all supply-side driven (oil, freight, commodities). Non-tradable inflation has been running close to 3.00% for many years, and as stated previously, the continuous reductions in technology/communications prices have disguised such increases in the overall CPI numbers. Electricity prices are up due to low lake levels from climatic conditions. Gas prices are up due to Government policy changes. Health, education, local body rates and building costs are all up due to public sector provision and the absence of market competition. It does not seem to the writer that dampening demand with mortgage rate increases will make a scrap of difference to price setting behaviour or pricing determinants in these sectors of the economy.

The RBNZ would be better off directing its inflation control energies to the real sources of non-tradable inflation i.e. the Government’s out of control fiscal policy spending (funded by increasing debt) and non-competitive parts of the economy. The response of the Minister of Finance that the higher inflation was a natural consequence as it evidenced strong economic growth. The growth is only in retail and housing and that is all debt financed. For a Labour Finance Minister to be almost championing a large inflation increase must be galling for the average household who are struggling to make ends meet each week with recent increases in petrol, electricity and rent.

Downward correction in the Kiwi dollar still has further to run

Irrespective of whether New Zealand leads the world with interest rate increases over coming months, or not, the NZD/USD exchange rate will continue to be dominated by the USD side of the exchange rate equation. The US dollar remains on its strengthening path against the Euro and further gains from $1.1800 to the $1.1600 area will come from stronger US jobs and other economic data over coming weeks/months. The NZD/USD correction down from 0.7400 still has a few more cents to go before the USD starts to go the other way later this year and into next year.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

9 Comments

Isn't the apparent improvement in the US economy due to much the same things we have namely out of control government spending and reckless policy?

" For a Labour Finance Minister to be almost championing a large inflation increase must be galling for the average household who are struggling to make ends meet each week with recent increases in petrol, electricity and rent."

BURN!

Interesting counter view here. Interest rates can't control the types of inflation we're seeing? A downward correction in the NZD would lead to imports becoming more expensive. They're already expensive enough.

ECON101: the demand curve is elastic and the supply curve is inelastic, in the short-term supply curve is almost perfectly inelastic locally, so if the demand curve shifts to right, the price will increase dramatically.

Interest rates are going to have to rise or else petrol will be $3 a Liter by Christmas and the people will riot.

I dont think governor orr feels bullied or in a panic from the banks,I think he does realise if he doesnt act then he will join ruth richardson on the nz economy wall of shame if the property market crashes and burns.

Roger J Kerr, One does not need to to be an expert or economist to know that Mr Orr will take time to raise interest rate and definitely not next month.

It is in his best personal interest to follow fed and if any goof up will not be alone and can easily blame the environment and as only economy in NZ is housing economy, it is in his interest for the ponzi to continue. It has become too BIG to try to control as in doing may pop the hyper streched bubble and will have no where to hide. His best option to do nothing and kill his time in office as retirement near and has done well for himself and his family with asset prices touching the roof.

I do not agree, he may as well move at least 0.25% as the banks have already moved more than that anyway. Of course he may decide to throw his toys as a signal to the banks to tow the line and stop ignoring him and hold but who cares the banks are already moving. Last time I checked, everyone was repaying the banks not Orr.

The present status gives the major banks a bit more room to provide pre Christmas "Specials"

Hello everyone... I have a rather critical view on the performance of our reserve bank over the last 18 months. Who carries the can for the predictions that seem to be at least 100% wrong in most cases.

1) March 2020 a forecast of a 20% housing fall resulting in printing 64 billion to facilitate near zero interest rates and removal of LVR restrictions

-Actual Housing rises 29%

2) inflation was predicted for the June quarter 1.6%

-Actual 3.3%

3) March 2020. Unemployment to be 10%

- actual... well it is 4.7% now and never got anywhere near 10%

Then we get all the excuses, ,

'We couldn't foresee that kiwis would rush home' Really when the government was broadcasting loud and wide ' Kiwis come home now while you still can.'

Print 64 billion and we have inflation on a 2 month reporting cycle, we can see it going up in countries with a one month reporting cycle,,, and we still can't predict anymore accurately than.1.6 versus 3.3%

And then housing... we have shouted to the world to come home,, made money free and removed LVRs... really how could it do anything else than bubble up.

Sorry but the reserve bank is in the business of tweaking policy for the future based on accurate predictions. Yes... that is right, the job description is 'accurate predictions'. If you cant do the job .... carry the can... instead of getting rich off the tax payer while delivering incompetence.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.