Economists at ANZ, the country's biggest bank, are now picking the Reserve Bank (RBNZ) will cut the Official Cash Rate (OCR) by 50 basis points next April to -0.25%.

In a report ANZ economists Sharon Zollner and David Croy say New Zealand is still experiencing the early stages of the economic impacts from the COVID-19 epidemic.

"We are now forecasting the RBNZ to cut the OCR by 50 basis points to -0.25% in April 2021. Beyond that, further easing is possible, but there are constraints on the OCR going below -0.75%," Zollner and Croy say.

"The RBNZ has ruled out changing the OCR before March 2021, but expressed a preference for a package of a lower OCR and a bank ‘funding for lending’ programme, should they conclude that further stimulus is required at that point. We think they will. We see a further increase in the large-scale asset purchase (LSAP) programme in November as likely, perhaps to $120 billion. The programme in its current form will have largely done its dash by that point."

Previously ANZ had expected the OCR to remain at 0.25% for the foreseeable future.

ASB economists also said they were formally changing their OCR forecast, and now expect the RBNZ to cut the OCR to -0.50% in early 2021. They see it staying there until the COVID-19 storm passes, potentially in late 2022, and no OCR return above zero until 2024.

The RBNZ last week increased its LSAP, or quantitative easing, programme to $100 billion from $60 billion and left the OCR at 0.25%, where it has been since March when the RBNZ pledged to keep it there for 12 months. The RBNZ has asked banks to be technically and legally ready to handle a negative OCR by the end of the year.

Zollner and Croy say the lockdown starting in late March caused a huge dent in economic activity, but was followed by a vigorous bounce-back as pent-up demand and a collective sigh of relief saw spending rebound sharply.

"The Government’s balance sheet appropriately took the lion’s share of the hit, with enormously expensive wage subsidies and other business support measures meaning the overall scarring to the business sector from the first lockdown was looking less severe than many feared," the ANZ economists say.

"As we write we are battling a second outbreak, but it appears to be limited to one cluster – albeit a big one – and optimism is rising that we will be successful in containing it relatively quickly and eliminating COVID-19 from our shores once again. Both business and consumer confidence will have been dented by the popping of any illusion that we could be 100% secure in our defences, but a rapid re-elimination may at least boost confidence that we can avoid the fate of Melbourne or the US, and the attendant severe economic damage that comes from uncontrolled spread of the virus."

But, they say, two other factors are only starting to make themselves felt. These are the missing international tourists and students, and the dire global economic outlook.

"The flow-on into retail and hospitality makes the hole bigger; the inability of kiwis to travel overseas reduces it. But on net, New Zealand with a closed border is an economy that is around 5% smaller. Because of the extreme seasonality of tourism, the blow will fall most heavily from October to March. Specialised labour shortages will also dampen output to some extent," Zollner and Croy say.

"Global growth is looking dreadful. While people have to eat, they don’t necessarily have to fork out a bit extra for New Zealand’s premium, high-quality produce. Food supply disruptions globally are providing price support, but also logistical headaches. On the whole, New Zealand’s commodity prices are holding up pretty well, but downside risks are evident, and non-commodity exporters are finding the going very tough. In addition, the robust NZ dollar is doing our exporters no favours."

'Into the twilight zone we go'

Zollner and Croy say they are now reviewing their Gross Domestic Product forecasts following Auckland's move to COVID-19 Alert Level 3, and the rest of the country moving to Level 2 from Level 1.

"The basic theme will remain the same: that the more persistent economic pain will start to be felt in summer. There is a significant risk that despite the significant fiscal and monetary stimulus already delivered, both inflation and employment will look set to undershoot the RBNZ’s targets for a prolonged period, and the RBNZ is very unlikely to stand idly by in that instance."

Zollner and Croy say they are not fans of negative interest rates, holding deep reservations about the long-term financial and societal implications of prolonged extremely low interest rates. Furthermore they point out the difficulty of exiting unconventional monetary policy has been demonstrated overseas during the past decade.

"But we’re not fans of deep recessions either. The RBNZ has clear inflation and employment mandates, and unless instructed otherwise, will feel duty-bound to do what they can to deliver on those mandates over the medium term. Long-term risks of unconventional policy are so blurry that of course the natural tendency is to focus on the nearer-term, more easily identifiable and quantifiable risks. Time will tell, though we may have to wait for the economic history textbooks written thirty years from now for the full story. For now, the path forward has been laid out clearly. Into the twilight zone we go," the ANZ economists say.

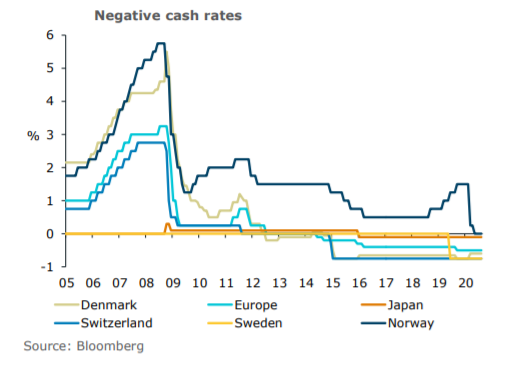

In terms of their view of constrains on taking the OCR below -0.75%, Zollner and Croy argue that at some point, a lower OCR would encourage cash hoarding and break down the transmission of monetary policy.

"This point is known as the 'physical lower bound' and it is thought to be around -0.75% or slightly lower. No countries have attempted to take their cash rates lower than this."

ASB sees negative OCR until 2024

ASB's economists say they have "pencilled in" a "large one-off OCR cut" of 75 basis points in April 2021. They had also previously expected the OCR to remain at 0.25%.

"The OCR would remain at -0.50% until the economic outlook had sufficiently brightened so as to warrant OCR hikes. This is assumed to be until at least late 2022, with the RBNZ erring on the side of caution to make sure the recovery is well established before slowly raising the OCR. We do not expect the OCR to move above 0% until 2024," ASB's economists say.

"The extent the OCR could fall and how long it would remain there would depend on the economic outlook, the effectiveness of other policy options (particularly the LSAP programme), and the ability of banks to continue to attract funding from depositors. Our observation is that across the globe, retail deposit rates don’t tend to fall below zero when wholesale rates are negative. A limit we currently identify for the OCR was around -1%, as this was the level that would likely keep deposit rates positive."

"Even at -1%, however, the OCR will need mates, with the amount interest rate stimulus to pull the economy out of its slump. We are hopeful that the FLP [Funding for Lending] and LSAP will provide further support needed, but much of the onus of policy support will fall on fiscal policy, with fiscal settings remaining highly supportive over the next few years," the ASB economists say.

Whether a negative OCR will work is the $64,000 question, they add.

"We have remained guarded on whether the benefits of a negative OCR outweigh the costs, given the international central banking community appears to be split. Our concern was that negative interest rates can interfere with the functioning of banking systems reliant on deposit funding and impair the ability of some banks to supply credit – the opposite of what monetary easing aims to do."

A key factor, ASB argues, will be the rollout of an FLP, which the RBNZ says it would link to a lower OCR. They expect an FLP would offer banks stable, low cost and long-term funding by borrowing directly from the RBNZ.

"A poorly designed FLP would significantly diminish the potency of a negative OCR. It is also unclear how easy it will be for an economy to extricate itself from a negative policy interest rate environment. The experience in Europe does not inspire a lot of confidence," ASB says.

74 Comments

Fully expect to get Mortgage Rates sub 2% within the next 6 odd months.

What this will do to asset prices e.g. Shares and Housing - well simple answer, if you are going to get 0% or close to 0 at the bank for your cash, literally people will be pushed into those particular markets and I expect House prices to continue to surge.

Crazy that given the circumstances we are facing, but if anyone is holding off on purchasing a house hoping for a fall in property prices, well the whole market is effectively against you. Personally recall the 2007 financial crisis and expected house prices to crash - instead they doubled in how many years?

Brave man to bet against that not happening again!

People will be pushed into all assets classes. Just look at current house prices in NZ and at the current price of the Air New Zealand stock, or even more incredibly at the current stock price of Hertz, to see how ridiculous such prices have become.

Housing is just one such asset class, and most probably the most inflated bubble of them all.

It is just a question of deciding in what bubble investor will put their money (the stock market bubble ? the bond market bubble ? the gold bubble?).

Question is: when will these bubbles burst ? Or will central banks and governments be able to keep them indefinitely from bursting ? Who knows. When interest rates go up again it is going to be quite interesting to see which one of such asset classes will collapse first.

Maybe interest rates will just not go up again in the foreseeable future, even when inflation kicks in.

The dilemma is: should investors park their money with the banks, and lose their investments through inflation, or should they bet that all these asset bubbles will continue indefinitely ?

In either case there is a substantial risk: investing in housing or in any other asset class is far from risk-free. It is very dangerous to assume the opposite. I am investing in many asset classes and leaving very little as bank deposits, but at least I am fully aware of the risks I am taking.

Hmmm. I pulled cash out of shares and bonds recently in anticipation of a dip in the residential property market in October (and a corresponding correction in the sharemarket). The plan was to buy a reasonably-priced rental or two at a 70% LVR. Not panning out as I planned so... Do I:

(a) Hold my nerve and stick with Plan A?

(b) Reduce our current DE ratio and pay more tax?

(b) Leave the property market to FHB's and returnees, and get back into tech and healthcare shares, with a big bank or two thrown in?

(c) Buy vintage watches, gold and silver or one of the other miracle cures? Or

(d) Buy a bigger boat and spend summer in the sounds?

No to BTC as I really don't understand it (Ive tried...but there you are). The boat appeals right now, especially if we can disappear for a month before election day.

Buy houses, shares, gold, silver, watches, hertz, cats, boats, air nz. Just don't hold anything the government can tax or inflate away.

Well Rhumline, you might have shot yourself in the foot getting out of the sharemarket, but if I were you I'd go with option (d) but register as a tourism business. Healthtech shares are a bit fully priced right now.. unless you got PEB @ the early stage (11c), maybe some SaaS companies but tread wisely and carefully (VHT is a dog right now. VGL and GTK are just treading water, ERD much the same) That nice 45ftr as a fishing charter venture down the Sounds would be pretty pleasant.

Option D.

Personally our strategy is as per the next poster... buy stuff, assets and toys the govt can't inflate away but also importantly have some liquidity so as to be able to buy time to enjoy those toys before the end of days. Yolo.

So you pulled out of shares and bonds. What is your investment strategy, and timeline? Why did you think there would be a dip in the residential property market? Have you been reading too much spin?

Possibly reading too many of the comments on this website, to be sure. I'm a relative novice at the share game but it does appear that some of the fundamentals are at breaking point (ref the discussion on P/E ratios here). Shovelling more money into the game doesn't necessarily make sense from a longer term hold (my timeline is five years) point of view unless it can generate income along the way.

The case for a dip in property prices has been tipped up a bit by ever-diminishing interest rates, but I don't think we've seen the full impact of job losses and world movement restrictions yet (possibly also investor appetite in view of the new regs). As I see it, the market is currently characterised by too little stock and a bow wave of demand from FHB's, retirees and some returnees. As the inventory grows (if the inventory grows) we should see a decline in some market segments - to a point where my benchmark net yield of 5% is achievable.

My strategy in recent years has been based on about 75% of assets generating an income and some capital growth, the balance growth-focused. Bit pedestrian I know,

Gold is not in a bubble, it’s only just passed its previous 2011 peak.

And the problem is that wages haven't been growing to match these asset price rises. So people will end up being priced out of houses, because when eventually when interest rates return to normality, many people will not be able to service their mortgages. Otherwise it could cause hyper inflation on certain things usch as housing and building, but not other things, such as imports like electronics and cars. Otherwise it will need wages to increase significantly. By reducing interest rates to such low levels, is like kicking a can down the road. Leave it to someone else to solve in the future.

I’d confidently bet against anything like the post 2008 boom happening.

Prices will be supported by these measures, and may even rise moderately.

And the price of NZD ?

Not at all sure. Maybe only a little weaker than now.

What is your track record to provide such advice Fritz?

What is yours?

And it’s not advice. It’s opinion.

Strong, to quite strong. How long does your opinion have to be wrong before you change it?

What is your prediction Te Kooti?

In the tug of war between the Covid impact and RBNZ/Govt. stimulation, the latter is currently winning the war on asset prices. Aud/NZD is >1.10 and wholesale rates are on the cusp of turning negative. If the RBNZ are prepared to accept house prices rising as a price to pay in supporting the economy, then they could accelerate higher.

Let's be clear though, we are not getting richer as a nation.

Interesting, thanks.

Just for the record, I still don't have a friggin clue how this will unfold. Too many potential factors and uncertainties. I'm positioned for wealth protection and just treading water for a couple of years, aside from continuing to spend butt tonnes on a reno.

Neither do I, but we are currently on the path to moderate currency debasement.

That is pretty clear.

Sometimes referred to as an external devaluation, standard playbook for a small open economy with relatively high private debt.

Debt monetisation

Are we any different to small countries around the globe. I would say we are as our economy has a better base than most as our products are food based as opposed to Switzerland which is bank/cash based which dosent bode well in the Covid era.

Note how our currency hasn't actually hit "banana republic status". Every economy is in the stuup so it's all relative. I very much doubt we're going to become the Zimbabwe of the South Pacific so maybe a little less "chicken little" and a bit more "tortoise" would be relevant

As you clearly haven't seen it, I have already said before 10-15% house price drop may not happen now. I revised it to 5-10%. I will stick to that for now. I think there will still be a fair bit of economic carnage to come. But really, which knows?

I have actually been quite honest in admitting my errors, unlike some here who think they are all knowing oracles...and will never admit they got things wrong, or that they might be wrong...

....yeah, NZ is different... It'll go up forever.

Let's charge people to save money and pay them to take out mortgages. Let's have stagnant wages and high unemployment with mortgages that consume 120% of family income. We can borrow to cover the gap. Tax anyone that earns anything at 95%. We should all invest heavily in an airline that doesn't run any flights.

We'll call it the Coked-up Rockstar Economy.

I can't agree more. This is the sheer lunacy of what has been happening.

And Orr & Co. are creating serious structural, long term economic damage that is even more unforgivable considering that the policies that they are promoting have clearly and utterly failed in Europe and Japan. Europe and Japan are now stuck in a deep hole they can't possibly get out of, and the funny thing is that Orr is busy digging our hole, ignoring such precedents - it all reminds me of Kind Cnut and the tide

And people used to look askance at Greece for living beyond its means. Now we're all patting ourselves on our backs as prudent and astute for living beyond our means.

"Don't worry guys, low interest rates are just temporary."

- all the economists since 2010

I wonder, then what? Stay there forever? Or keep going down...?

Took a while for the bank economists to reach this conclusion.

Duh!

If -2.5% is good, we should go to negative 10% and really boost the economy

Why is everyone so terrified of a recession? It's a natural and needed part of economic cycles.

Like the lock downs we've had 70 years of quite low hardship and now we're faced with some our resilience is found completely wanting.

We're all terrified because in the past it has been a correction. An opportunity to clear out some dead wood.

This time it's all dead wood. It's all crap and bubbles built on almost free money. There's a real danger of the ponzi scheme being exposed.

Because someone needs to think of the ma and pa investors, even if a few generations have to be sacrificed to enrich them. No one is prepared to stand on their own two feet and take responsibility for their own risk taking.

How high will inflation go as a result?

Not much higher at all. They need to do this more extreme stuff to nudge it higher.

Depends how you measure infaltion of course.. with the broken ruler they call CPI.. yeah, you're right.

"but there are constraints on the OCR going below -0.75%"

An explanation would be helpful.

The continued existence of cash.

Not enough cash in circulation to make much difference

May relate to the fact that banks submitting government debt for purchase by the RBNZ under the LSAP programme (QE ) receive payment in the form of a government balance sheet liability paying OCR. Will banks sustain incremental losses as the QE programme expands with negative interest rates?

This whole prognosis of expanding the RBNZ LSAP (QE) programme and instituting negative OCR defeats the claimed necessity of low interest rates to "stimulate", because banks will pass losses on to customers in the form of higher interest rate lending.

Well, there isn't that much cash now. But banks can't impose significant negative rates on depositors in an environment in which cash withdrawal is possible. And if they can't pass those rates onto their depositors then the whole margin model is out the window.

Banks' balance sheets are in the range of $620 billion, currency in circulation ~$8.0 billion, banks' vaults have $0.833 billion available for further distribution.

Audaaxes - There is an appropriate sign......

Below that rate, banks will have no margins, or in any case they will not be able to lower their retail rates any further.

As depositors and other funds providers will simply not accept negative returns, banks can't offer mortgages below a rate that is equal at least to the average fund costs (let's assume for a moment that this is 0%), plus a minimum margin that takes into account their admin costs, loan risk etc..

They have investigated how low they could get in Europe, and actually, I am surprised that the -0.75% has been seen as a constraint: from what I recall, the European Central Bank has determined some time ago that such absolute minimum is around -0.5%, below which the only effect is not to lower retail rates, but simply to subject the banks to further pressure on their margins, and paradoxically to force them to be even more cautious and risk-averse.

The only central bank in the world that has reached -0.75% is the Swiss one, but this is due to extreme, extraordinary circumstances that are very, very different to the NZ scenario (the severe disruption caused by a potentially overwhelming appreciation of the Swiss frank).

The technical term for the minimum rate is called by the EU Central Bank as the "reversal rate". Extract from a speech by a Member of the Executive Board of the ECB: "At the reversal rate, bank profitability will fall, reducing capital generation via retained earnings, which is an important source of capital accumulation, and thereby eventually restricting lending. The decline in present and future net interest margin reduces the forward-looking measure of bank capital, hence the risk-bearing capacity of the bank, and its supply of credit.".

Retail deposit rates in Europe are very slightly negative only in very few exceptions, and they are between 0% and 1% in the majority of cases: I actually recently established new term deposits with German and UK banks for rates not much lower than the current rates available in NZ.

To me, Orr and his interest rates attempts appear more and more like King Canute and the tide.

I've added ANZ's explanation for this to the story.

I hope Adrian Orr has a long term plan lol

He has, it's follow japan down the rabbit hole

https://alhambrapartners.com/2020/08/17/it-was-bad-in-the-other-sense-s…

Which is failing right now - You Need NIRP But Because NIRP You Then Need To Lessen NIRP; Or, Just Trust US, This Stuff Just Works

Orr says we may need a negative OCR next year and now the banks are forecasting this will happen. The economy maybe 5% off but the banks must be in a worse state if this is the route to salvation. Lower interest rates will not lead to inflation as measured by CPI, but they will keep asset prices up there. Hopefully the next government will see the folly of this path as experience overseas has shown. Fix the OCR at 0.25% while covid problems remain. The government can fund at this low level and savers still get a few crumbs.

Issue people credit cards and let them go shopping. At 9.95% (Kiwibank credit card)and pay it for the rest of their life. Always ways to make money. They made it so easy to apply for credit cards online now.

Yes

we cant unleverage a Ponzi

we can only leverage further

The net result is inflation in asset classes ... but deflation of purchasing power & wages

At some point it will snap

Banks have the best interest of the general public. :)

ING/ANZ Frozen Funds ?

I think I'm finally starting to understand Bitcoin...

I would love to learn how to start using crypto but have no idea where to begin

to do what?

The "funny money fiat" issue is NOTHING to do with transactions/ease/fees/stores of wealth/govt control etc etc

Its to with LEVERAGE in order to maximise the extraction & flogging of resources

This flogging provides jobs / incomes / consumption

Once a resource is flogged, you cant magically unflog it back by reconfiguring the financial side of the ledger

The ponzi is locked and loaded

Allow me to fill in the gap in your comment (or just say so if I have missed the mark entirely) -

Our banker friends and reserve bank governor seem to not have any idea what they are doing, apart from fiddling with a lever that no longer does anything apart from move a wee dial on the dashboard. In the short term they agree it has the effect of... appearing to do something, maybe. In the long term they agree they don't know what the lever does.

Meanwhile in bitcoin land we at least have some market governed by supply and demand, and the laws of pump and dump. Not every big bitcoin superstar can pump and dump at the same time, and there is no impotent lever, so it puts a limit on the frustration of being a player. So perhaps this is indeed a better place to hang our $

Its made a whole bunch of druggies from back in the University days rich is all I know about it.

As negative interest rate taken in place, we walk into an unknown territory. There are still lots of unknown factors about negative interest rate. Will it boost our economy? Maybe yes or maybe no. What we've known is that, once we get to that stage, we'd better get out of recession fast. If not, we might stuck in that for a long time. And you don't know when is the next crisis going to hit us. And when it hits again, what should we do? keep lowing our negative interest rate? to what point?

BW, you've been predicting a liquidity crisis and deflation for quite some time, certainly well over a year. I don't disagree with you that this likely the end outcome but I'd like your opinion on WHEN you think this will happen, especially as it's very clear the RB & the Government will do everything to avoid disaster / prolong the party?

Thanks

I don't know what is the case for a negative OCR or in fact negative interest rates.

What is that going to achieve ? Who will it benefit ? The poor and struggling or the rich and the banks ?

The monetary theorist controlling things in the central banks and commercial banks are really crazy, if they want to undermine the very system of borrowing, saving, economic growth, etc.

This seems to be an expired medicine being given to a progressively deteriorating patient.

Time for a new Vaccine, folks.

Prediction for 1 year mortgage rates in February 2021?

1.5% ?

It will mainly benefit the rich, home owners and the banks.

It will possibly offer some secondary benefits to the wider economy if it provides mortgage holders with more disposable income.

Negative rates, protect the banks and the stupidly leveraged.....wow. This runs against all the interests of all Kiwis who operate financial prudence, especially those that have saved to retire, and all those old people vote.

sorry to say but all "Savings" are a mirage ... being just a debt call on the future

In order to see any future, we must distort the Ponzi , otherwise it falls over sooner

The savings (system wide) were never there, it was all just faked by 40 years of (unjustified) leverage

It remains to be seen how banks can operate for long with negative interest rates

So how do you vote out a Governor of an independent RBNZ?

What am I to do? Do I pay down some of my mortgage when it comes up soon for refinance or keep my retirement managed funds intact as a 'balanced' fund?

Pay down your mortgage but keep the facility in place.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.