The first Official Cash Rate (OCR) hike in seven years is expected to have a particularly large cooling effect on the economy.

ANZ chief economist and Sharon Zollner and Triple T Consulting managing director Sean Keane expect the economy to be more sensitive to an OCR hike - which markets are pricing in for November - than a cut.

Accordingly, Keane believes the Reserve Bank (RBNZ) won’t need to do a lot (make too many hikes) to meet its inflation and employment targets.

Zollner expects it to lift the OCR in steady steps from 0.25% to 1.75% by February 2023.

The last time the OCR was increased was in 2014, when four 25-basis point increases took it to 3.50%.

First hike the sharpest

In general terms, Zollner said the first hike is always the sharpest, just as the first cut is the deepest.

She said there was a risk financial markets could take a 25-basis point OCR hike and run with it, tightening monetary conditions more than the RBNZ might be comfortable with.

Keane noted that after seven years of money becoming cheaper, there is some uncertainty around how people will respond to having to get their heads around money becoming more expensive.

However, there are some specifics in the current environment that mean the RBNZ will get traction when it hikes interest rates.

Bulk of mortgage holders will be affected soon

Firstly, it’s hard to look past the big increase in mortgage debt that has accompanied years of interest rate cuts.

The value of bank mortgage debt has increased by 11% over the past year to $311 billion, meaning New Zealand’s mortgage debt is now worth almost the same as the entire economy, or annual gross domestic product ($325 billion).

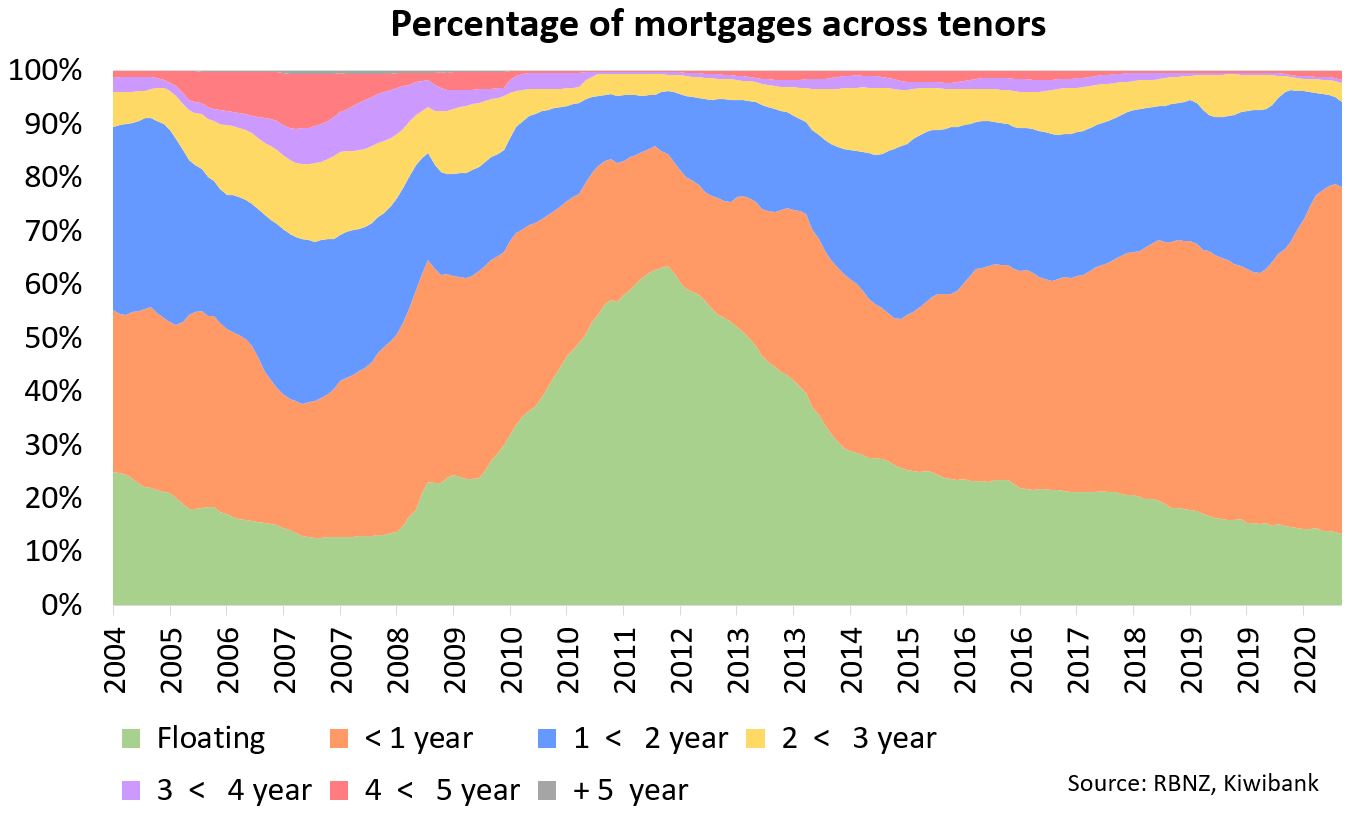

As interest.co.nz reported in May, the bulk of this debt is due to rollover within the next year, so the effect of higher rates will be felt by a number of people fairly soon.

According to Kiwibank chief economist Jarrod Kerr, 60% of mortgages are either floating or up for refixing in the next three to six months. Meanwhile 80% of the country’s mortgage book will refix in the next six to 12 months.

“That’s an enormous amount of fixing flow into a tightening cycle,” Kerr said.

Zollner also made the point that while mortgage rates may only go up by couple of percentage points, the increase is proportionally larger in a low interest rate environment.

For example, a mortgage rate hike from 2% to 4% is a 100% increase, while a rise from 6% to 8% is only a 33% increase.

Interest rate hikes to coincide with tax hikes

Keane noted that on top of people getting their heads around money becoming more expensive, the government’s tax changes will soon start biting.

These include the new top income rate of 39% (which took effect in April), the removal of interest deductibility (which is being phased in over four years) and the extension of the bright-line test from five to 10 years.

Keane believed the combination of these policy changes will keep the RBNZ’s tightening cycle short.

Indeed, with house prices up around 30% over the year, Zollner said the RBNZ would need to feel its way genteelly when tightening monetary policy.

However, she said the later it starts, the more it will need to scramble to deal with an over-heated economy.

She said the economy no longer needs higher demand. Rather, it needs more resilience

RBNZ research done pre-Covid reaches different conclusion

With the RBNZ due to publish a Monetary Policy Review next Wednesday, it didn’t comment on whether it believed the economy would be more sensitive to an OCR hike than a cut in the current environment.

However, research it did in 2019 (before it started using “unconventional” tools like quantitative easing) concluded the impact OCR changes had had on consumer inflation and economic growth had been stable since the 2008 Global Financial Crisis.

‘Indebted demand’ theory

Keane had a different view, arguing that economic responses to central bank policy adjustments have changed in recent years.

He pointed to the theory of indebted demand, explaining that as borrowing becomes cheaper, people take out more debt.

The cost of servicing that debt lowers spending, consumption and thus economic growth, prompting central banks to lower interest rates again. So, the stimulus/debt cycle repeats.

Eventually, all the monetary and fiscal stimulus halts the downward spiral, and central banks can start hiking rates again.

However, Keane said because every 25-basis point OCR hike will affect a larger pool of existing debt, hikes will bite, and the RBNZ won’t need to lift the OCR by very much to achieve its inflation and employment objectives.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

118 Comments

"Bulk of mortgage holders will be affected soon"

I agree. There is need for both mortgage holders and potential FHB to factor this in over for the next few years and beyond. A 1% increase on a substantial mortgage is significant. Surprisingly whenever this is raised in the comments section there is a number who counter post. It would seem that the current short term rates are lulling many into a false sense of security . . . these are more like the last of the summer wine . There is need to be prudent and look to reducing debt and questioning need for large discretionary spending. I don't think that rises in interest rates will result in a flood of mortgagee sales, however it is likely household budgets will be significantly affected. While the banks apply a stress test when lending, that is your breaking point and there will be pain prior to that level being reached.

If only we'd been prudent and not put FHBs in a position where they have to take on terrifying levels of debt in the first place to own a house.

Funny how that never comes into it.

Still, can just cut back on discretionary spending that they don't make because wages haven't kept up with costs, I guess. I just need to cut 600 coffees out of my day and it will be fine.

No just the two coffees a day and make your own lunch instead. Make your existing car last and its not like your going to be going on that overseas holiday you insist on having every year anytime soon anyway. People will cope, they just need to pull their heads in for a few years.

No just the two coffees a day and make your own lunch instead. Make your existing car last and its not like your going to be going on that overseas holiday you insist on having every year anytime soon anyway. People will cope, they just need to pull their heads in for a few years.

But this is not how the NZ economy works. It needs people out spending like drunken sailors and living on the edge financially. Without that, the whole shebang (including the bubble) is at risk.

Exactly. The retail economy relies on frivolous spending + the tax it creates. House of cards

Not necessarily 'frivolous' but yes, the NZ economy relies on consumer spending. If people stopped buying coffees, ate home-grown turnip soup and gave up utes to drive around the suburbs, then the economy will go into sharp decline.

dp

Those who have got themselves donkey-deep in debt will pay a price, inevitably, in the advent of a significant rise in mortgage interest rates.

But the all-to-conspicuous housing shortage in NZ will continue to underpin enthusiasm for house purchasing - both by owner-occupiers and investors.

The propects for the housing market remain particularly positive - and certainly so in the longer term. NZ remains a good bet for the future.

TTP

You do realise that NZers are by and large are donkey-deep in debt? And that enthusiasm can only last when buyers are willing and able to take on debt to continue the on the current trajectory?

There are oodles of people who are cashed-up - anxiously waiting to find a suitable property.

TTP

What are they waiting for? I thought you said that property is a good bet so why would the sideline cash wait?

I guess I'm one of those. I'm waiting so I can get a slightly better picture of where house prices are heading over the next few months. No hurry as I'm probably earning more in an international managed fund atm than if I rushed and bought something. Property will always be a good bet as it's leveraged - and even in the current climate and with all the rules if you pick something that's cashflow positive you'll do well long term.

LOL I'm sure cutting back on coffees and making your own lunch will magically give you that $60000 extra you needed to keep up with last year's price increase. Assuming 20% deposit. Just to keep up!

Well I get free coffee, I don't buy lunch, or even eat it, I don't take overseas holidays (was a decade between my last one and the one before that) and I drove my last car until it hit 340,000km and would still be driving it if someone hadn't wiped it out in a crash that wasn't my fault.

But come on, tell me how many free coffees and non-existent lunches I have to cut back on to mitigate a 30% increase in house prices, and then tell me why people think buying a first home when housing was drastically more affordable makes them Warren ****ing Buffet and qualified to give financial advice that no wants or is asking for.

..i think he was being facetious.

I've heard too many people saying similar things unironically, it's getting more and more difficult to tell satire from ignorance.

the govt is solely responsible for the 30% increase in house prices, they may clown around pretending the need more advice but the truth is the got exactly what the wanted.

Economy is now in hyperdrive so tightening needs to happen.

They acted too hard and too fast when covid hit instead of trying to limit the damage, now they are in a position where they need to move away from the "emergency" settings but find that the economy is hooked to the emergency settings like meth addicts.

Soon or latter needs to go into detox, the longer you wait the harder it will be

If house prices increase 20 percent over 2021 that is equivalent to another 26 percent increase on 2019 prices after a 30ish percent rise in 2020. Confirms the saying, of best time to buy a home is today

I think the saying is more like Pity da fool - Mr T

What we actually need to do is move on from the ridiculous addiction to property. What a waste of life.

Then stop commenting

And if they drop 40 percent in 2023 is today the best time?

Hahahahaha.... read the above comment, very appropriate for yourself BL. You were labeled Broke Landers for that exact reason.

Sadly I have friends who scrimped and saved for years, still missed out on a home and now are just like "$%k it I'll just buy my [insert vice] " as a way of comforting themselves. :-(

Because some people are offering crazy amounts to secure a house. Those who miss out are often just offering a more sane price.

Exactly, work a second part time job, there is plenty of work if you are prepared to put the effort in.

Why not just work 2 full time jobs. And eat canned food every night.

Ah yes, "just work two jobs"... I'm sure my partner and my 2 month old daughter will be delighted to never see me again.

Congratulations! Seeing her grow and reach those milestones will be some of the best memories in your life. Enjoy.

For goodness sake; do you want to live just to work rather than work so that you can live. Truly, I feel sorry for the under 50 year-olds these days; you are trapped big time!

GV

Get over it and start living in the real world.

Back in the 1980s saw our mortgage rates rise from under 10% to over 20% - that is reality and one adapts.

When one's rent goes up (and it will) one adapts, when one is faced with a signifcant car bill one adapts . . .

When the cost of buying or renting a home becomes unsustainable one adapts (and leaves across the ditch)

What was the average household income to mortgage ratio in the '80s? 3x? Or >10x as many FHB's in AKL are finding in 2021? This "back in my day" perspective reflects a different paradigm.

Also, what was the ratio of average wage to average household income in the 80's?

If it was fairly close to 1:1 then plenty of families in the 80s were not paying $5 - $6 per hour per child in pre-school so both parents can toddle off to work to service a mortgage.

Let the old people compare Apples and Oranges, it makes them feel good about themselves.

100% agree. Those who don't understand compounding interest will be forever paying it, those who do will eventually reap rewards. Blown away by the number of folk who have mortgages, or are renting yet travel overseas, buy consumer crap including new cars. Jesus, if you have a mortgage ask yourself every day "how will I service this loan if I am unemployed, or rates rise?" Do everything to get the mortgage down....2nd job, live like a pauper. When I suggested this sometime back I took heat as the respondents felt 'people needed to enjoy their lives and not be a slave to the bank.' Get over it. Times have changed.

People have swallowed the modern day fairy tale that debt is their friend.

Look at the tv advertising especially for some of the second tier personal lenders. It's all fun and good times. Take that trip, buy that car.

Rebel Wilson advertising on tv yet another buy now pay later scheme…. The debt fuelled financial system must be continued at all costs. On a separate point was listening to George Gammon this morning who mentioned the increase in household savings since March 2020. Only problem is that it is concentrated into the age 65+ age group who are not known for their high spending levels. This was USA data, not sure if we have a demographic breakdown for NZ?

Not sure when things changed from saving for something to borrowing to get it.

More a process than a defining moment in time. A process of marketing, mass media, wages falling behind inflation and bubbles, fomo and several other contributing factors.

Cheetahlegs

Agreed.

Nzdan a millennium posts that he bought three years ago is paying down his mortgage as much as possible and is looking at having it paid within 9 years.

With average house price to income ratios sitting in double digits this doesn't seem releastic unless someone is on a very high income.

I'm starting to suspect that avocado toast isnt the problem.

Yes, not realistic for many. What I did was up sticks to Masterton, bought at the bottom of the market from a distressed accidental landlord for a discount. House is a 5 minute walk from the train station, and I commute into Wellington for work each day.

You are P8's poster boy for getting into the housing market, whatever it takes.

"Do everything to get the mortgage down....2nd job, live like a pauper." Work weekends, don't have kids, don't eat out, don't go to concerts, forget travel to visit family.....just work and work and then once the mortgage is paid off when you are 70 you just lie down and die - job done!

Income goes up, debt declines by repayment. Very slow erosion by inflation. If you are paying a mortgage at 70 you have failed.

Personal experience is the lowest form of evidence in medicine but here we go: I crucified myself from late 20s (single beer on Friday night, crap clothes) through to 41 when I became freehold. Now 14 years l'm looking for part-time work with retirement funds set. The 2nd job was the key. The extra payments off principal changed the ball game. Try spending some time on moneychimp.com and playing around with interest rates, extra repayments. Seriously, the learnings can change your life :-).

How many kids do you have Cheetah?

This is the crucial issue. If you are a 41 year old man, there is still plenty of time to have kids, if you have a younger partner. If you are a woman who does this until you are 41, it's likely too late.

If you leave it until 41 to have kids, you're going to be 62 at their 21st. You likely only have another ten years in you before death becomes an average/numbers game. There is a high chance you would not live to see your own grandkids being born. So yes, it's possible, but given Kiwis and their tendency to drop dead in their 50s from heart disease, it's a terrifying idea of acceptable normality.

I've placed a 100 year business plan on my latest project. Will be in the family for the next 3 gens, so its not about capital gain or cost, its about developing and improving an asset and revenue stream

"Those who don't understand compounding interest will be forever paying it, those who do will eventually reap rewards"

And if interest rates are negative?

Interest rates (typically term deposits) don't equate to interest earned e.g. share dividens, income from commercial property. Last Fri the S&P500 reached a record high. Good spreads across ETFs help offset the low bank/Gov bonds. It's not hard. The information is out there, easily accessible. Unfortunately the biggest impediment to people acting is self-inertia.

The upside with low interest rates is borrowing is cheap. Capital investment in businesses....buy another property...borrow to buy shares (not a recommendation but an option).

Printer8: Get a clue. Houses are many times more relative to incomes than they previously were. No one is interested in your tales about walking six miles barefeet in the snow uphill in both directions to school anymore. Your experiences are not relevant and your anecdotes don't displace actual, measured statistical data. Buying a home is harder than it was. Get over it.

GV and 8014

Yes most definitely . . . you really do need to start living in the real world.

Yes it is tough but stop with the "poor us, poor us its too tough, its too tough".

In the past year 60,000 FHB now own their own homes . . . the highest level since RBNZ started publishing data in 2014.

Four sons, all millennials, no help from bank of mum and dad, all have their own home. One (single) at 33 owns a rental also, another who until last year had five rentals until he sold four to buy a multi-million dollar mortgage free home better than mine. All four average guys, yes all university degrees, but in usual/average salaried jobs.

Interesting that he sold 4 rentals last year, I thought house price is going to double in another 5 years. Why buy a multi-million dollar mortgage free home now when he can buy two in 5 years? ;) I have to admit he is smart though. I think every smart person would ask why is he selling now? ;)

coh

For a few reasons

- For him and family to enjoy a more comfortable home

- Did not see then rate of increase as sustainable so took his gains when ahead (although one property subject to brightline)

- Looked at buying a business which didn’t eventuate

- despite popular belief, considerable work in rentals.

As for properties doubling every 8 years, well that is a simplistic throw away line which isn’t necessarily so - after recent increases (although similar to 2004-7) expect flattish market over the medium to longer term. The property party of very significant increases (albeit some) is over for now.

Printer: I can tell you I very much live in the real world, thanks. You can feel free to pretend there are no downsides to investors hoarding multiple investment properties in a market with limited supply, cheap credit and wages that don't keep up with inflation just because your kids have creamed it, but perhaps it's worth keeping mind that one 'average' salary won't get you finance on an owner-occupied home and in many cases, neither will two.

GV

That is a sad comment.

Get over it; it is quite proper to buy investment properties.

If you want to play the absurd morality card, then there are numerous homeless needing much needed housing but you don’t seem to consider the need for rental accommodation. Very selective morality on your part.

Rather than blame shifting you need to ask yourself what you need to do as others are achieving homeownership. If that is shifting to Australia or the provinces then so be it - you won’t be the first. Emigration in the past - other than the last year of gains - has been around 40,000pa. ( . . . and by the way during the late seventies and early eighties due to economic conditions emigration was considerably higher but you won’t want to acknowledge that)

Cheers

"Rather than blame shifting you need to ask yourself what you need to do as others are achieving homeownership"

God, not this again. The problem with your attitude is the assumption that the housing crisis is an individual problem that can be solved by individual actors behaving (or not behaving) in a particular way. This just isn't the case. The housing crisis has causes - namely decades of policy that had the forseeable effect of limiting simply, increasing demand for housing as an investment, and pushing up deposit thresholds.

But this debate about who had it harder is just a red herring. The real question is: how hard do we want it to be? Is it really a good thing for the country as a whole that house prices are at this level? It's hard to see how anyone could say yes to the last question.

While I agree residential property investment is a logical response to policy settings, I can see a time (if it's not here already in many circles) where owning multiple investment properties isn't something to brag about over the BBQ, but rather a shameful secret. Hopefully.

Unlikely, they internally justify it as providing shelter for the less fortunate and think they are doing them a favour.

I think the changes in interest deductability, 10 year brightline and tenant security of tenure changes they made will start discouraging landlording for speculative reasons (short(ish) term capital gains), but if the govt really wanted to see the instant effects they should have exempted house sales from the 5yr brightline test until some date in the not to distant future (end of 2022?). Right now there a bunch of landlords out there with tens of thousands in potential brightline tax liability that makes it worth holding onto the rental for a few more years till they are past the 5year mark, and they are instead going to raise rents as much as they can to ameliorate the impact of the interest deductability changes till they can sell, or until they get back to positive cashflow.

There is nothing wrong to buy investment properties. But we have to admit here, hoarding and speculating houses is not a moral thing to do, especially when we have housing shortage at the moment. Same as hoarding and speculating toilet paper or even food when the crisis comes. People do make choices, sometime people do throw their moral away. I think when people do that, they just need to admit it. It's not a good act, that's why governments regulate the market to prevent these actions happening.

“....is not a moral thing to do.” By whose judgement? Frankly I envy anyone who has been a long term owner of residential property and regret selling my 2 rentals. Media and selected commentators would demonise landlords, I’d rather they direct the hate to gangs, long term beneficiaries and drug dealers. Each to their own. Where’s Yvil, he has a pragmatic view.

Oh course it is, shelter is one of the most basic human needs. How would you feel if the private sector had captured the water market and only provided enough water to survive if you handed over 30 or 40% of your income. The reality is, short of sleeping on the street, no one has the option of refusing to consume shelter if the price is too high. In previous ages you’d self build on some unoccupied land on the edge of the village, but these days the cult of free market economics means far too many people are trying to screw over their fellow countrymen all in the name of “getting ahead”.

The govt plans to restructure water management will end in a dog's breakfast and you paying iwi under te tiriti o whytungi... you will be filling in the swimming pool if this goes ahead

" I’d rather they direct the hate to gangs, long term beneficiaries and drug dealers."

Let me know when they're creaming tax-free gains and outbidding FHBs at auctions and then maybe, but you're picking a pretty low bar to defend yourself there.

One of the side effects is increasing crime and family violence as the have-nots become ever increasing disenfranchised - welcome to SA mk2

"Yes it is tough but stop with the "poor us, poor us its too tough, its too tough".

Wild how this is your response after bringing up the predictable talking point of mortgages in the 1980s. Perhaps you could take some of your own advice on that one.

It's a heartwarming story. I particularly enjoyed the twist with the landlordism.

Now let's see how they fare fresh out of university in 2021. Don't forget to also pay down the student loans because mummy and daddy didn't fund that either.

GV: the deposit is the issue, the servicing costs are about the same as a percentage of household income. This is pretty constant, mortgage servicing will be about 35-40% of household gross income most of the time.

Simple enough to see for yourself if you open the interest.co.nz mortgage calculator and key in two scenarios

Scenario 1: a 1980s household, mortgage 2x household income at 18% interest, mortgage servicing ends up at 36% of gross income

Scenario 2: a 2018/2019 household 8x household income at 2.5%, servicing costs are 38% of gross income.

Right now we are probably a bit outside that, but thats going to be short lived as incomes catch up* with house prices (which are already slowing, and may even fall slightly)

* Jacinda is going to to put the public servant pay freeze into defrost mode soon.. Nurses strike + overloaded hospitals under a labour govt in a pandemic, I give it less than a month before they get a carve out, then its a question of who is next, teachers?

Pragmatist: That's at current ATL interest rates. They won't last forever, unless the real estate lobby and Printer8 can successfully convince the government they've managed to Gordian Knot the entire economy around house prices and their continued rise. So while the deposit is the head-ache now, it's a 30 year bet that you'll constantly be ahead of the Printer8 ball. Two full-time incomes with no career issues, redundancies, kids, illnesses, retracing in the value of the underlying asset, etc.

The higher prices go now when credit is cheap, the more people are exposed to risk when it eventually goes the other way.

Not a 30y bet if you buy before you retire, income goes up, debt doesn't. Renters get sick and made redundant too, life has risks, but I don't see how renting makes any of those any better, it's still a bill that's got to paid every week.

Not a 30y bet if you buy before you retire, income goes up, debt doesn't. Renters get sick and made redundant too, life has risks, but I don't see how renting makes any of those any better, it's still a bill that's got to paid every week.

Most will have allowed themselves some headroom. Certainly their lender will have.

Yes, except for those that lied to the lender to secure the mortgage they otherwise wouldn't have been able to get. There may be a few households that suddenly need to find that boarder they told the bank they had lined up for the spare room when they refix at a higher rate. But this will mostly be recent FHBs, not a huge number of them in that position hopefully.

Printer8 - An increase in the OCR is coming but it pays to remember any mortgage taken out for a number of years has had to pass the 5.5% - 6.5% acid test to get a mortgage at 2 -3 % so there is a substantial buffer there.

Also not all houses have a mortgage or a mortgage of significants.

The OCR would have to rise 3 - 5 % to have a major effect.

In the past the OCR has had to go very high to kill off inflation, in the last decade and more the RB has had trouble getting inflation, we have a window of inflation coming that is Covid related that will pass through when supply chains/shipping resumes back to normal 18 months ??

The reserve bank and Government have demonstrated that all stops are/have/will be used to keep the economy from failing.

Recession's seem to be a thing of the past, unlike the recessions we had in the 70's/80's/90's !

Shoreman

The bank’s 6% stress test is a bank initiative about banks protecting their interest . . . not in the borrower’s interest especially ensuring borrowers continuing quality of life.

I agree that the 6% stress test means that one can survive increases of 2 or 3% . . . but note use of “survive”. That does not mean maintaining same standard of disposal spending on pretty mundane things (eating out, kids birthday presents etc).

Yes, I expect most will “survive” but by being prudent earlier rather than later will mean that tightening will be need less severe.

Yes, I agree RBNZ are likely to take little steps with OCR increases (and may counter that with extension of likes of FLP) as they will not want to cripple the housing market for the same reason they have allowed it to increase.

a warning shot of 0.25% definitely would have a shock effect,like the ABs losing a test match but the property market frenzy is not always rational so dont see it slowing down unless he fires a volley.

AB shocks are of lesser impact now as sadly they are of greater frequency. People have no choice other than to get used to trends but not quite so easy when they hit them in the pocket though. Sufficient comment on here to identify that everyday household items and services are already starting to pinch. Some of those with hefty mortgages might well not be able to stretch much further.

A high inflation rate has a much larger negative effect on the economy.

Inflation in propety prices is a far greater sytemic and social danger than your flat white going up a dollar to pay a Barista a living wage.

Quite a fallacy from the government letting businesses import hundreds of thousands of low-skilled workers in a short span to ensure the likes of our flat whites remain cheap but ending up inflating property prices instead.

The basis of belief in OCR increase, is somehow based on the idea that NZ is experiencing an economic recovery. This is next to impossible, given other nations are not. NZ is not independent from the global pool.

Oddly enough as it seems, the NZ economy is not based around housing. The OCR isn't about housing.

Banks economists are pushing the Govt agenda, as the banks don't want to get offside with them. Govt wants housing to cool off, but are in reality unable to lift rates. It's not the rates that's caused the problem, it's the banks willingness to lend. If this was curtailed well and truly, then housing prices would get the cold water treatment. Even financially qualified seasoned investors would bide their time, wait a year or two to reenter and start snapping up bargains. This is what happened during the GFC.

Meanwhile bank economists appear stultified, even challenged in their thinking. Are they lying or uneducated? Probably not. Their job is to advance the agenda of their employers, and little beyond that.

. It's not the rates that's caused the problem, it's the banks willingness to lend.

Yes, but bank lending is the vehicle by which monetary expansion really works, particularly in the Anglosphere. Ex-BoE governor Mervyn King said as much but people didn't pay any attention. The idea of base money and broad money is quite important. All the QE tricks are irrelevant if the sheeple don't play their part. This is why Japan's QE experience is something of a 'failure'. Japanese firms and h'holds have been paying down debt as opposed to taking it on. NZ seems to be in a sweet spot in that the sheeple will bid up high prices without blinking and a 'no worries mate' laissez faire attitude to it all. It's all about behavior and the ruling elite have no idea what they would do if this changed. Until then, the bank economists' narratives will hold and their jobs will be safe. Look to protect yourself against extreme money printing in the meantime. Despite what people believe, that might not be in land or property.

Given the size of their mortgage books , the banks will make every attempt to lock in anyone into longer term and more expensive rates, with the full knowledge that the RBNZ will find itself in a position ,again, where it has made a policy error and reverses course .Of course the banks will pocket the change as they are benevolent creatures.

I thought much of the bank mortgage lending was calculated against a much higher interest rate scenario.

It is, but figures can be fudged, and a large swathe of consumers are addicted to the Next Big Thing. All new Ranger out in 2022!

Yes, the banks will be fine. The rest of the economy won't as there will be less disposable income to flow around.

It is, the reality of the situation is there wont be many people losing their homes if the OCR goes back to 1% but discretionary spend will definitely drop, which is exactly what you want when the economy is overheated, which it is.

Certainly as rates rise the share market and residential rental may slow up as other less riskier investment returns improve.

The interest rate discussions at the moment are fascinating. However, all that matters today is that FOOTBALL IS COMING HOME!!!

No wonder you're bored. You need to get out more. ;-)

Italy are a superior team to England and I expect Italy to win.

However, just like predicting house prices, predicting football is fraught...

The veritable Mike Hosking (who is financially on a much better wicket than the sheeple):

Because if it's not like that, I just can't work out how it is we survive without re-joining the world. As much as the dazed, bewildered, and scared might like the cocoon, we are going broke paying for it.

I was astonished at those personal borrowing numbers yesterday from Centrix. We are still borrowing to buy flash cars despite the fact interest rates are allegedly on their way up this year. Is anyone awake?

A lot of what we have right now is a false reality, a debt primed dream land, where the world is locked out, printed money is being flushed around the economy, and we think we are doing well.

Wise words....but of course hindsight is a great thing.

But is this the same Mike who championed mr key and his Rockstar management of the economy? You know .. the bloke that imported zillions of unskilled and often elderly people and forgot to put any infrastructure in place for them? Knighted himself and then scarpered before it all blew up.

Sure. The Hosk goes where the wind blows. Entirely inconsistent one day to the next. That's his job. To push emotional triggers and buttons. That gets the audience for the advertisers.

But his words here are tangible.

I thought it was simpler than that - National good, Labour bad.

How overwhelmingly stupid is it to rely on turning the OCR up and down to effect change on a system as complex as the modern economy? It's like attempting brain surgery using a spoon.

We need to focus on the actual problem we are trying to solve. Are we trying to force people off benefits and into unrewarding and precarious work? Then cut benefits and lay on some free transport and sleeping sheds on the farms. Are we trying to cool the housing market? Then announce the introduction of a mandatory rental WOF in 2023 and a scheme for the compulsory purchase of non-decent private rentals (for social housing). Or are we trying to give low-paid workers a bit more power in the labour market so that we get some wage growth and improved job security at the bottom-end - then say so!

Agreed. There's a kind of wilful collective stupidity in insisting that tiny adjustments to interest rates are the be-all and end-all of economic management. We've inherited a fairly bizarre set of rules but they're rarely questioned. We have a weird insistence on being hands-off in certain areas when direct intervention would be helpful (housing) but no problem being interventionist in others.

Massive massive massive jawboning going on.

That's all it is. If RBNZ increases the OCR and economic activity crumbles they will reverse the decision. There is a time lag though the first one or two increases won't hit until everyone on 1 year fixed rate re-fixes. So it could easily be a year before there are signs of trouble.

As pointed out in the comment below 2.4% isn't going to be a disaster. Which for many this is true. For those that keep spending and accumulating debt any increase in payments will become a budget blowout. I have read an article in the past month where a mortgage was obtained and they defaulted on the first payment. You can't expect everyone to be responsible.

LOL. Central banks are starting to come across like ineffective parents... "Go to your room NOW or I sell the Playstation... I'm not joking, I *mean it* this time..!"

Journalists: ooh snap Johnnies gonna lose his playstation

Bank economists: How good is Johnnie gonna have to be to get his playstation back?

Banks: PlayStations! Special price!

Johnnie: BUYS MORE GAMES F U MOM.

So the 1yr fixed goes from 2.19% to 2.4%?!

Not really going to cause significant hardship.

Exactly on 500k mortgage $20 a week, just have one less beer a week...only big impact be on those that borrowed seven fiqures or more..but that will be a small majority.

...that's a pricey beer, even at a fancy pub...

That not point.

House price follow interest rates.

They go up, house go down.

House go down, overleveraged sell.

House go down further.

And on it go.....down

Lanlord.com not tell me dat.

Bugga

Unfortunately things are never as tidy as this.

I expect a couple of hikes, then cuts to a negative OCR within the next 3 years following an economic shock.

This is a plausible scenario. It all depends on how responsive RBNZ is to the suffering.

Whenever OCR is raised, market is bound to react for short term but will soon settle down and will than try to push pressure / throw tantrums on rbnz to not raise again, soon and will be successful.

Despite all talks, rates will not rise before next year and from than on will take another year or two and 0.25% rise though symbolic will not change much besides sentiment for short term as even after .25% rise, interest rate will be very low to have any major impact but yes, if they follow soon by 0.25% after first rise, will be effective but doubt if Orr will have the guts to do it as thinking is based on short term gain long term pain.

Whilst Zollner is correct about the proportionality of a 2% interest rate increase at the 2% and 6% level she is somewhat devious in failing to point out that the actual cost is the same. Human reaction is always the driver of events and it is uncertain what the reaction to any rate rise will be, I speculate that it will be more negative due to past history of lowering rates so if the RBNZ understands human reaction they will raise rates in very small increments to judge reaction. However past history of the RBNZ and the FED shows their understanding is deficient so it is quite possible they will plough on raise rates and then be surprised at the adverse reation.

Just read Tony Alexander’s repot out today.

Indications are that it is still a sellers market . . . translated that is upward pressure on prices.

So yes, action seems likely needed to cool the market.

(Yeah, easy to slag him off but he has regular surveys of mortgage brokers, valuers, and yes, REA which he processes quickly to give what I consider the most current view of the state of the market. Don’t suggest one slavishly follow him, but worth taking into consideration his findings especially to confirm one’s observations and other sources of information.)

Housing is in crisis mode, yet this government has the first draft of the proposed new RMA postponed until 2022??? Why????Draft legislation set to replace the Resource Management Act (RMA) has been labelled “revolutionary” and praised for putting a greater emphasis on the environment and the principles of Te Tiriti o Waitangi.

But there are concerns that any efficiencies that were hoped to be gained from the repeal and replacement of the RMA may be lost due to the bold nature of the changes and the complexities of incorporating new legislation with existing and upcoming bills and frameworks.

A review of the RMA, launched by the Government last term, recommended three new laws to replace the RMA; the National and Build Environments Act (NBA), the Strategic Planning Act (SPA), and the Climate Change Adaptation Act (CAA).

There are about 3-4 contributors who have spent the last 18m - 2 years continually valorising FHB taking on more and more debt. No doubt they will feel no compunction whatever now the inevitable toll is to be rung on these unfortunates

watch them pile in Mike. That's hate speech, your gonna get hammered.

There are about 3-4 contributors who have spent the last 18m - 2 years continually valorising FHB taking on more and more debt. No doubt they will feel no compunction whatever now the inevitable toll is to be rung on these unfortunates

The way house prices have moved, only those taking on a mortgage in the last 2 months are at high risk. Anyone who got into the market 6 months ago are thanking their lucky stars right now. Unless the interest rates start to rise very quickly, then everyone including those that bought yesterday are sitting pretty. There is always risk but lets face it, there are those on here that still wouldn't buy a house if prices fell 50% tomorrow so those are the people you don't want to be taking advice from.

The NZ govt will be printing more and more over the next 10 years just like US.

Backed into a corner of debt.

End of long term debt cycle.

Rises? In the long term interest rates in New Zealand only go one way and that ain't up.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.