Questions are being raised over what the Reserve Bank’s (RBNZ) hawkish tilt means for the bulk of mortgages that are due to rollover within the next year.

The RBNZ, in its Monetary Policy Statement released on Wednesday, surprised financial markets by pencilling in a series of Official Cash Rate (OCR) hikes from the latter half of 2022.

RBNZ Governor Adrian Orr acknowledged that because so much of the country’s economic growth has come off the back of higher debt and asset prices, the economy is very sensitive to interest rate changes.

Accordingly, he expected the RBNZ to get “reasonable bang for buck” with any shift in monetary policy.

“That’s why we keep putting that warning out: Think about long-term average interest rates, not what you’re currently being offered,” Orr said.

'An enormous amount of fixing flow into a tightening cycle'

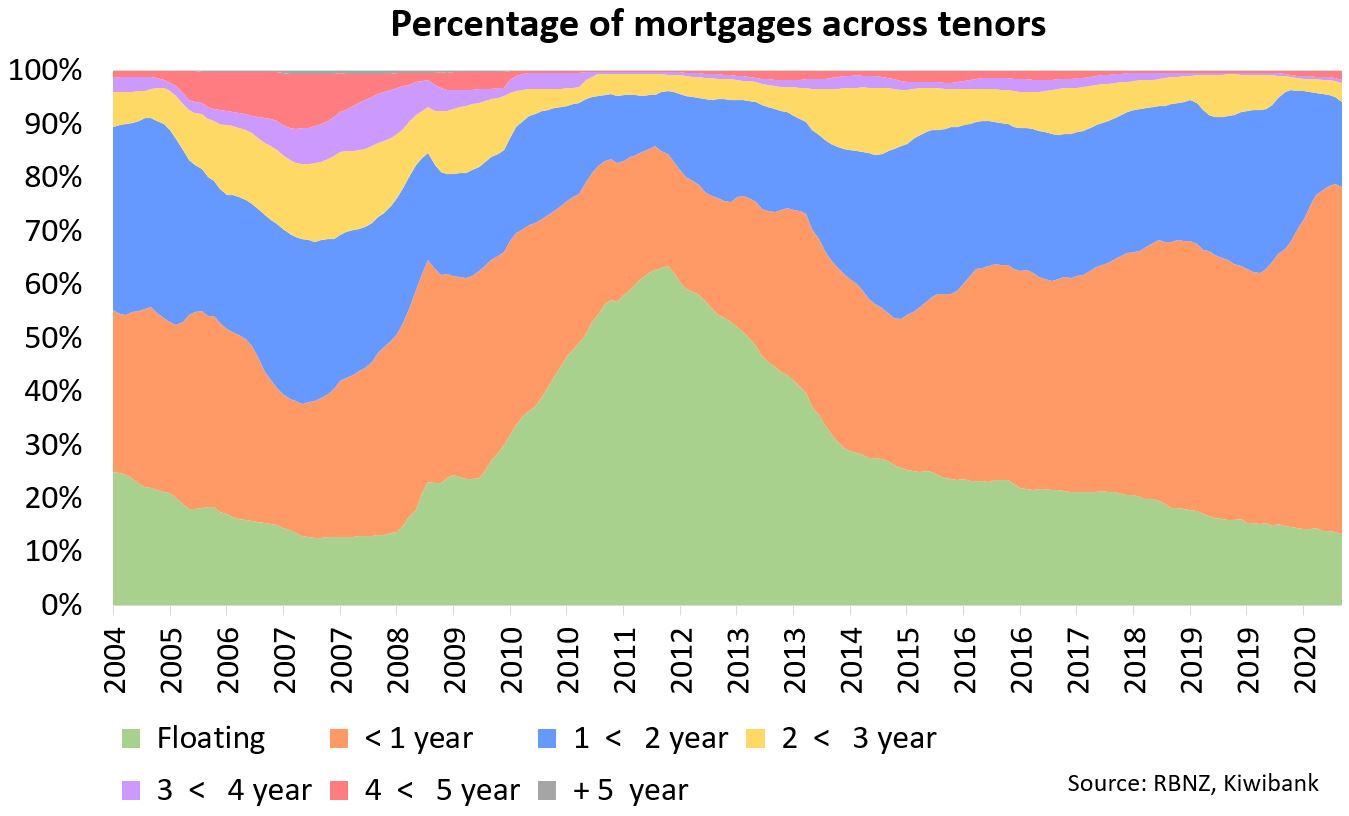

Kiwibank chief economist Jarrod Kerr made the point New Zealanders are also particularly exposed to interest rate changes, because 60% of mortgages are either floating or up for refixing in the next three to six months. Meanwhile, a whopping 80% of mortgages are up for refixing within the next six to 12 months.

“That’s an enormous amount of fixing flow into a tightening cycle,” Kerr said, noting the country’s aggregate mortgage book is as short as it comes at the moment.

If enough people fix their mortgages at slightly longer terms, Kerr believed this could push wholesale interest rates up even further.

Kerr noted three to five-year mortgage rates have already started to rise, but not as much as the movement in wholesale interest rates.

“This suggests banks may start passing on higher wholesale interest rates to mortgage rates in coming weeks,” he said.

“We’re not trying to scare the horses here. I’m simply stating that last time we were in position like this, it happened.”

The “last time” Kerr is referring to is 2012. He said a change of tone by the RBNZ prompted billions of dollars of mortgages on floating rates to fix in a matter of days. This pushed swap rates up.

Kerr said the shift might happen over a matter of months this time, as households sitting on short-dated mortgage rates look at the messaging from the RBNZ and look to fix for longer than one or two years.

The assumption at the heart of Kerr’s view is of course that mortgage holders believe there will be enough heat in the economy for the RBNZ to justify raising interest rates next year - likely ahead of its international peers.

But what if inflation doesn't rise enough to warrant an OCR hike next year?

However, Orr himself recognised there was still a lot of water to go under the bridge.

There are uncertainties around how much pressure skills shortages will put on wage growth, how much the Government’s tax changes and RBNZ’s reinstatement of loan-to-value ratios will cool the housing market and thus the economy more generally, and the extent to which inflationary pressures from supply chain disruptions and high oil prices are temporary.

OCR hikes for 2022 remain a projection, not forward guidance.

What’s more, OCR hikes in 2014 were reversed fairly quickly in 2015, as it turned out the economy still needed more fuel as inflation threats dissolved. The OCR has only tracked downward since then.

Fixed mortgage rates

Select chart tabs

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

82 Comments

No reserve bank will be able to hike the interest rate in next few years and even if they do, it will be symbolic as low rates ( May be not the lowest) but low rates are in for number of years to come.

Whenever interest rate hike will be announced, markets are bound to throw tantrums and reacts adversely, which will restrict further interest hike , if not reversal like you mentioned in 2015.

Low interest is the new norm, how earlier it use to be 10% to 20% than 5% to 10% and now will be between 2% to 5% maximum ( Most probably will be between 2% to 4%).

Reserve banks by choice for short term gain have pushed themselves in a situation where will be blackmailed to not raise rates. No exit policy will work.

May be reset that everyone is talking about will be in reserve bank and how they operate.

Keeping interest rates low, effectively lower than real inflation, is a way to inflate debts away. A gradual unwinding.

That's assuming wage inflation occurs. If we get stagflation we'll be in trouble.

And given our productivity is not improving its hard to see why wages will grow. If we can close off immigration more permanently then maybe but otherwise what are the drivers for wages? I'd like to say kindness but reality and labour virtue signalling are not good bed-fellows.

Markets will throw tantrums either way, though interest rate stress or inflation stress. I'd rather not be the one left holding the debt when they do. People with no debt stand to benefit from wage inflation more than those with debt who will also see their interest rates rise and asset values decline.

If there's wage inflation then there's no need for asset prices to deflate. So holders of debt are the winners as those debts reduce relative to income.

interest rates up = cash flows down = asset value down, pretty basic really. You assume that wage inflation will happen at a high enough rate to offset the impact of inflation & interest rates rising on cash flow. Which I highly doubt (but would gladly accept!).

Those without debt don't need to worry about the interest rates rising, but still get the benefit of the wages increasing.

Again, RBNZ has no completely control with interest rate movement. They do make decisions. But how economy performs along with global economy performance determine how rate goes. What they've been doing in the past doesn't mean what they will be doing the same in future. People who make quick adaptation to changes will be in winning position.

Talking the talk, just not walking the walk. Similar to Jacinda & Co.

Long suffering countrymen and women, come to Australia and escape the slumlords clutches. Australia wants to give you a fair go and a chance at a decent life. You only live once, don't let your youth be spent just making Orrs rich friends richer. https://www.google.com/amp/s/amp.tvnz.co.nz/news/story/JTJGY29udGVudCUy…

In NZ a gang can shut a public, tax payer funded school down for days for a tangi and the MOE approves. Wouldnt happen in Aussie. Are gangs another useful idiot being used to drive honest hardworking kiwis away?

Co being Collins? Not impressed with either.

So let me get this straight: Banks lent all this money out like drunken sailors...did they not expect that interest rates would go up at some stage? Why the angst? Could someone explain to me what in the blazes is going on, surely these people with control of billions of dollars can see past the hand in front of their face? We are lead to believe that these are very, very smart people. Now we've got John Key saying frankly extraordinary things such as: 'the one thing saving some mortgage holders were record-low interest rates, and if they rose to combat inflation recent buyers may struggle to afford repayments'. What the heck is going on?

The graphs and carded rates tell the story of what the banks really think. The angst is just part of their plan to support their forecasts. They can use the media to scaremonger the damage that interest rates raises could do, and our RBNZ will respond with only the tiniest jumps towards non-emergency rate levels.

JK works for ANZ. Of course he will make statements that are in the best interests of his pay masters.

Why anyone listens to JK is beyond me...

Why anyone ever listened to JK is beyond me...

He was one of the greatest All Blacks of all time IMO. Great winger.

Yeah I remember JK doing a cat walk wearing the world cup jersey, looked more like he was a Hooker though not winger. Can't forget that amazing missed hand shake with Richie Mccaw at the world cup too. They were the good days...

The way how we measure inflation has flaws. This means the data we see on regular bases possibly could not reflect the true inflation. When it lags, that's when they make inaccurate forecast and wrong decisions.

The way inflation number is calculated .....?

It includes and excludes what can be controlled and manipulated by reserve banks to suit their narrative.

Wow. Almost all debt is rolling within 24 months. RBNZ stuck between an avalanche of inflation and speculator bubble. What to do... continue to sacrifice everyone or let the risky speculators find the new normal.

Orr is about to be world famous in NZ, as famous as the 87 crash.

Its the RBNZ's game of musical chairs where the speculators get assigned their own thrones and everyone else has to fight over the dwindling flimsy plastic yard chairs. The RBNZ would never harm speculators.

Averageman, Mr Orr came out with warning of interest rate rise, is only to calm down and avoid taking any action on speculative demand / ponzi.

When the time comes, he will have thousand reasons, not to raise.

Yes. Or that everyone will have forgotten what he said in 2021. It will be all a bit last year!

Happy Friday.

Seems to me that the RB is, predictably, trying to 'cool off' the housing market with warnings -- and warnings only, because they really don't want to raise rates in reality. I don't think the banks expect rates to rise; but it's in their interests to encourage people to fix while inflation fears are around.

The Reserve Bank has somewhat got us stuck in this cycle of low growth/inflation/rates and high debt. Markets have responded by relentlessly bidding up assets.

To be fair there has been a lot of mission creep for Reserve Banks also. Governments have largely abdicated responsibilities in terms of economic development so, to some extent, Reserve Banks have been trying to push on a piece of string by lowering rates.

More like, trying to fan the FOMO embers back into flames

he is trying to Spook the market so buyers are not loading up on debt and keep the prices from rising.

Rising interest rates will bring the fragile economy to an abrupt halt

Very insightful John, I agree that is exactly what is happening. No CB is tightening due to a supply side inflation shock.

Currently supply side inflation but the very nature of open economy means feedback to demand side will happen

Well forward rates have been in backwardation (right word?) for years, essentially the bet everyone has take is that interest rates will keep declining. To be fair for about three decades that's been one way bet in the medium to long term.

Stupidity is employing Thieves and Idiots to set the Amounts over and beyond the Norm. Especially when they have "Over Valued" the Norm in their own favour.

Real Money and Real Eastate and anyone who has a hand in the pockets of the people these days is a Total Failure...waiting to happen.

Dipping and double dipping is a crime out of all proportions. And this is the biggest Ponze so far.

https://www.msn.com/en-nz/money/personalfinance/certainly-be-a-burden-f…

https://www.msn.com/en-nz/money/personalfinance/certainly-be-a-burden-f…

An economic crisis will hit before rate goes back up to 5%, then they will lower the rates again...

COVID didn’t do much damage rather let the economy skipped a real recession and the world is heading straight into “recovery” mode...

I get tired of the incessant hypothetical speculation that banks are going to raise rates. I've heard this same narrative since 2008. Any rise is short lived and followed by lower rates. To even consider they have that option is to be supremely naive and taking their word at face value is giving them credibility they sorely lack. Don't do it. Question everything.

Agree 100% but than even journalist and media have family to support and need a topic to discuss instead of asking hard questions.

They should disclaim that.

Hi Jenee here, to do some serious journalism, but I gotta pay the mortgage and want to be invited back so I won't totally call BS on this latest word salad, follow me down an inane path of central banker crystal ball gazing sold as expertise to deflect from the 'cant do anything but cut decisively without consultation' one trick pony with no backup act except stalling long enough in the hope dementia gets you before the reality hits. Cheers.

Interest rates a distraction me thinks. Any rise will be minimal. The real threats are rises in associated ownership costs and a stalling economy.

Throw in covid arriving (we haven't actually had it yet), China possibly de-friending us and this winter might well be a doooozy.

Happy friday :)

Rewind on here and elsewhere and see anyone mentioning inflation and rising interest rates?

Apart from myself I mean, and anyone else automatically labelled DGM, rather than reality merchant

Inflation and rising interest rates is a given and does not make you a DGM. It's picking house prices are about to fall by 50% to 70% in the next 12 months that makes one a DGM.

That sounds like the opposite of doom and gloom.

Said the vulture to the dying buffalo.

Less buffalo, more Hyenas

And haven’t the vultures had their fill already when investor LVRs were removed last year...

Still hasn't actually happened fella. If interest rates increase in any meaningful way, I'll eat my hat.

Full-time investor here. I locked in 3/4 of my debt at 2.99 / 5 yrs a month before Labour's new tax. When it goes I think it will go sharply and quickly.

If that isn't happening offshore, it won't happen here in NZ.

OO here. Locked in my mortgage on a 4 year 3.09% and adjusted the payments further to bring it below 10 year amortized. It presented the best value as a % discount on the standard rates. Currently on track to have the house paid off in under 15 years, having bought in 2017.

A friend who is a developer posted this list of May's announced price increases.

Effective May:

• Steel and Tube Holdings - 2-16%

• Ecko Fastening Systems – 2.75-9.85%

• Mitek - 5.2%

• Rosenfeld Kidson and Co - 33%

• Permapine - 5-7%

• Eurocell Wood Products Ltd - 3-4%

• CHH Woodproducts – 8-10%

• PSP - 5%

• Clearlite Bathrooms - 4-6%

Effective June:

• Steel and Tube Holdings - 4-16%

• Riverlea Group - 4.17-8%

• Windsor Brass - 5.51%

• Sika NZ - 3.2%

• MSL - 8-14%

• Paslode New Zealand - 4%

• Rosvall Sawmill - 5%

• Southern Pine Products - 6-11%

• Niagara - 5-8%

• CHH LVL - 5-15%

• Max Birt Sawmills - 4-8%

• CHH Woodproducts - 5-10%

• Red Stag Timber - 5-7%

• ITI Timspec - 4-10%

• Winstone Wallboards - 2.9%

• Roofing Industries – 2-25%

• Bowers Brothers Concrete – 4-5%

Seems the estimates of a real world inflation rate being about 10-12% are about spot on based on those averages. Good list.

Good. That will for sure inflate the house prices.

Any of those in the basket of goods used to measure CPI? Nope. No inflation will be measured or admitted to.

It was clear from the get go, that Labour's ad hoc housing policies would create additional shortages.

We issued a 1 July notice for price increase which was not category specific. We're experiencing variability across all the product groups, and assessing the costs as shipments arrive.

All consumer goods will head north. Freight across the tasman has doubled, dg's are very hard to move at all, ex China freight is 2 to 3x what it was... there is no way your average sme can eat these rises...

These lists are becoming common in the building industry. Cost of new builds continues to rise as a consequence, with no end in sight

Home owners and property investors should CHILL, not to worry of rise in interest rate, as Robertson and Orr are more worried than any individual borrower as it is ther reputation / policies, which is at stake, if people start defaulting in mortage payment as that will indicate their failure. To prevent exposing their fault / wrong decession will keep on pumping more to support and promote house price, hoping that it does not burst during their term.

Reserve bank role : "The Reserve Bank is committed to ensuring smooth market functioning - Reserve Bank of New Zealand"

And for smooth market functioning, the only way possible, now ( also they know and are confident) is to support and promote the housing growth at all cost as in any ponzi, it is either up, Up, UP or it crumbles...no role of stabilizing - nature of ponzi is such -Check histotry.

Should also ask them, what is their defination of Temporary in terms of inflation as am confident that they will keep on increasing the period to suit them.

Also, what if it is not temporary as all their policies are based on assumption that rise in inflation will be short term.

Can. Kick. Road.

Orr could always lower the rates further then be true to his word and increase them again next year. He didn't exactly say they had to be higher than what they are now, did he?

If or when NZ has another lockdown between now and then, I wouldn' t be surprised if that happens. Victoria is a good wakeup call for NZ.

How will all of the investors who did equity withdrawals to leverage up and buy more and more property be impacted by rising interest rates? Will they loose everything if they can not repay on one of their loans? Because they are all leveraged to the max using paper wealth, that isn't real until the property is sold. If prices fall as rates rise, they might not be able to realise that equity, with debt attached that still needs to be repaid. So investors will rush together to sell to stay above water, but at a time when there is also low demand. This could very easily turn into an aggressive downwards spiral in prices, as animal spirits take over. The RBNZ know this, I think that's what's making Orr go grey.

Orr would come up with some other scam to keep the ponzi going and the rich richer. Maybe the RBNZ could find another way to harvest money from the young, perhaps kidneys?

Specuvestors who leveraged up, could loose everything. Ya role the dice and take your chances. There will be some. Those with vulture funds are at the ready and waiting for commercial reality to occur.

Just need all that social housing to come online and it's curtains... - oh wait - lots of campervans floating around somewhere

What's conveniently forgotten is that all loan applicants were stress tested before loan disbursement.

Alarm not warranted, nothing is more cruel than false hope.

The banks also assume 0 inflation on household expenses

Which is probably fine really, because banks know that 99% of households will go to extreme lengths to avoid a mortgagee sale.

Really what causes people to lose their house is if they lose their income - either through illness or accident, or just having bad luck with their employer. Interest rates going up from 2% to 4% when the loans were all stress tested at 6% is not really an issue for the mortgage and bank, it's a problem for the wider economy as discretionary spending dries up.

But what about investors? I'm not convinced that they will go to the same lengths as traditional homeowners to avoid default. They are about to see their income change through tax, interest rates and inflation.

Supposedly they provide a much needed service to society, so they will never see their income disappear. The added benefit is that any inflationary changes can just be "passed on to the tenant".

You are correct and the dominoes will fall as the reduced discretionary spend produces more job losses, less tax take and likely deflation of those sectors remaining to reduce prices or suffer the same fate. Deflation of course makes debt more expensive to service and repay so Govt & RBNZ will face a Tsunami of biblical proportions if significant deflation arrives and we have the least competent at the head of both to deal with the results.

Yes, but many mortgage holders in the short-run cannot readily respond in kind to increasing costs (mortgage and other)... wage/salary increases tend to be inelastic

Was that before or after the ranger/pool/boat ? Tried to buy a boat recently ? Up to 2 years wait with some Marques...

Inflation above rate of wage increase

Plus mortgage rising taking more income

So reverse of cuts in costs all owners been handed last 6 years

And Finance minister forecasting 3-4% GDP growth

Ha

Some of us can add

In theory consumer inflation would not occur under those conditions; prices don’t tend to go up when people have less disposable income to spend. Although most of our inflation is probably imported these days so it is possible.

I wonder if we will see equity release mortgages for younger people.

Majority of current inflation is caused by Govt local & National plus their monopoly subsidiaries - Rates/Power/Fuel/Taxes(Levy's) and largesse to beneficiaries who refuse to work. Interesting to see the reaction by Wallytonians to a 16% rate rise!

I just re-fixed for 5 years. Get in quick.

Maybe. It wouldn’t be the first time there has been talk of inflation and people have fixed long and now regret it. I fixed for 2 years at 3.4% just before Covid as I was thinking inflation would be coming, has cost me about 5k compared to just fixing for 1 year. The future is very hard to pick; for example it is quite likely Covid won’t really be a problem in most countries by the end of the year, so the current inflation may disappear altogether. Who knows, I sure don’t.

Then you'll have five years to regret it. Not getting at you though.

IMO if they didn't want the reduction in interest rates to cause this insane house price inflation, they should have put universal restrictions on the lending solely for residential house lending. My understanding is that a lot of this printed money instead should have been lent to businesses, and not home borrowers. But my understanding is that businesses aren't borrowing and banks have all this money to lend out

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.