By the Westpac NZ economists*

Inflation has been very low for the past two years but is set to rise gradually from here, boosted by technical factors in the near term and a strong economy over the medium term.

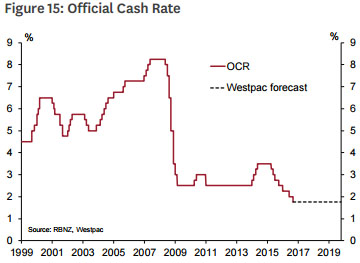

We expect the Official Cash Rate to remain on hold for a substantial length of time, but market interest rates are likely to be pressured higher by other forces.

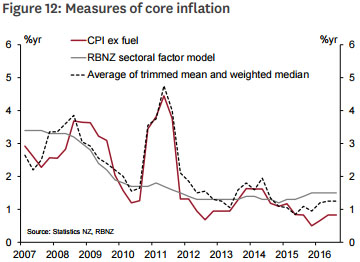

The inflation story in New Zealand is approaching a milestone of sorts. For the last two years, annual inflation has been below the Reserve Bank’s 1-3% target range. The shortfall was exacerbated by some temporary factors. One was a steep fall in world oil prices, stretched out over two years; another was a pair of cuts to the ACC levy component of car registrations. Both of these factors cropped up at a time when ‘core’ inflation was also softening according to a range of measures.

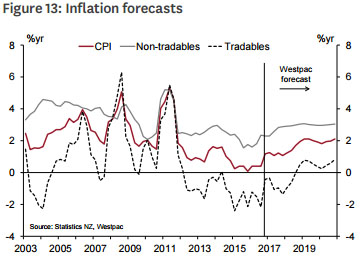

We can now be more confident that inflation will be back within the target range at the end of this year, even if only marginally. Some of the temporary depressing factors will start to drop out of the annual inflation rate soon. In the December quarter, last year’s sharp fall in fuel prices looks set to be replaced by a modest increase. And from the September quarter next year, the ACC levy cuts will no longer have an influence.

Importantly, core inflation appears to have bottomed out, and has picked up a little in the last few quarters. The September quarter figures showed a lift in prices for many tradable goods, a sign that retailers were able to pass on last year’s sharp fall in the New Zealand dollar, albeit with a long lag.

That said, we expect only a gradual rise in the rate of inflation over the next couple of years. One of the biggest headwinds will be the resurgence of the New Zealand dollar over recent months. Exchange rate movements tend to take the best part of a year to flow through to retail prices, due to factors such as importers’ currency hedging. The latest upturn in the NZ dollar has yet to be reflected in the CPI, and is likely to suppress import price inflation for a while longer.

In contrast, the conditions for a sustained pickup in non-tradables inflation seem to be in place. With strong GDP growth expected to continue through 2017, the economy is now catching up to what we estimate to be its non-inflationary potential. The unemployment rate has fallen below 5%, and more than half of firms report that supply-side factors, rather than demand, are their biggest constraint on growth. Nominal wage growth has yet to show a meaningful pickup, but this tends to be one of the last shoes to drop in an economic upturn.

The housing-related components of the CPI account for a significant part of the inflation outlook. The building industry is the one part of the economy that is clearly running into severe capacity constraints, and prices for newly-built homes have risen 6.3% in the last year. In contrast, rental inflation has been relatively subdued. Rents are on the rise in Auckland, where the shortage of dwellings is most glaring. But they are now falling outright in Canterbury, where the ‘scarcity premium’ is coming out of rents as the housing stock is steadily restored. Since the nationwide balance still points to a shortage of housing for years to come, we expect the upward pressure on housingrelated costs to continue.

Altogether, we expect a slow return to the 2% midpoint of the inflation target over the next few years, with a lingering risk of dipping below the target range again. As long as this remains a genuine risk, the RBNZ is likely to favour a long stretch of loose monetary policy settings.

As we anticipated, the RBNZ reduced the cash rate again in November to a new low of 1.75%. But with domestic conditions improving, and a diminishing threat of inflation expectations becoming unanchored, the RBNZ has indicated only a small probability that further easing will be required. Instead, the OCR is projected to remain low for a considerable time.

That doesn’t mean we can expect a period of stability in market interest rates, however. For one thing, markets tend to favour action over inaction, and with the focus moving away from OCR cuts, traders are instead turning their attention to hikes. The market is currently pricing more than a 50% chance that the OCR will be raised again by the end of next year. We regard this timing as far too early. On our forecasts, inflation will still be barely within the lower edge of the 1-3% target range by that time. Indeed, we expect that the RBNZ’s communications over the coming year will emphasise that monetary policy will need to remain accommodative for a long time.

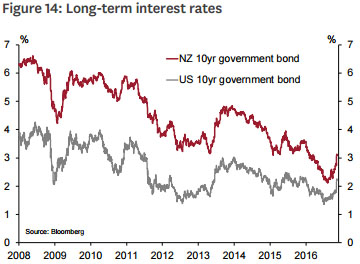

However, we expect that this jawboning of interest rates will be only partly successful. There are other forces pushing interest rates higher that are beyond the scope of the RBNZ. The first is that global interest rates appear to have broken free from their multi-year decline and are rising again. This movement began well before the US election, but has clearly accelerated since then as the market has anticipated a sharp rise in government borrowing and infrastructure spending. New Zealand interest rates have been swept up in this move, despite the lack of any similar change in the domestic outlook.

Another factor is that banks’ funding costs are evolving independently of the OCR. For several years after the financial crisis, growth in deposits was sufficient to meet banks’ funding needs. But in recent months, deposit growth has slowed markedly, at the same time that credit growth has accelerated. In principle, banks can meet this funding shortfall through offshore wholesale markets, but there are limits to how far they can go down this path – partly due to tightening international regulatory requirements, and partly due to cost. If the constraints on funding persist, this will likely manifest as some combination of higher interest rates and tighter lending standards.

Consequently, we anticipate a moderate rise in mortgage rates over the next year, even with the OCR on hold. That will mark a change from the last couple of years, where falling mortgage rates contributed to rapid house price gains. And this will have implications for both monetary and macroprudential policies. Previously, our forecasts incorporated another round of lending restrictions – most likely debt-to-income ratio limits – at some point next year. But we now suspect that higher interest rates will do much of the work in cooling house price growth, removing the need for further lending limits.

There is one other substantial change to our interest rate forecasts. We noted in the previous Economic Overview that a slowing economy would warrant further OCR cuts into 2018 and 2019. However, with our economic forecasts now evolving towards stronger growth for longer, we have decided to remove those additional cuts from the forecast. We still anticipate a slower pace of growth towards the end of the decade, as the Canterbury quake rebuild winds down and the construction pulse elsewhere peaks. And without that additional easing, our forecasts suggest that inflation is more likely to linger in the lower half of the inflation target. But that in itself would probably not be enough to spur the RBNZ back into action.

Financial market forecasts (end of quarter)

| CPI inflation |

OCR | 90-day bill |

2 year swap |

5 year swap |

|

| % | % | % | % | % | |

| Dec-2016 | 1.2 | 1.75 | 2.10 | 2.30 | 2.70 |

| Mar-2017 | 1.3 | 1.75 | 2.10 | 2.40 | 2.80 |

| Jun-2017 | 1.1 | 1.75 | 2.10 | 2.50 | 2.90 |

| Sep-2017 | 1.2 | 1.75 | 2.10 | 2.50 | 3.00 |

| Dec-2017 | 1.1 | 1.75 | 2.10 | 2.50 | 3.00 |

| Mar-2018 | 1.2 | 1.75 | 2.10 | 2.50 | 3.00 |

| Jun-2018 | 1.4 | 1.75 | 2.10 | 2.50 | 3.00 |

| Sep-2018 | 1.7 | 1.75 | 2.10 | 2.50 | 3.00 |

| Dec-2018 | 2.0 | 1.75 | 2.10 | 2.40 | 2.90 |

| Mar-2019 | 2.1 | 1.75 | 2.10 | 2.30 | 2.80 |

This article was prepared by the full Westpac New Zealand economics team. Michael Gordon is the acting chief economist at Westpac New Zealand. This is the fourth chapter of their recent publication "November 2016 Economic Overview", and is here with permission. The first chapter is here, the second chapter here, and the third chapter is here.. The final will be re-posted here, tomorrow.

12 Comments

Sounds good Mr Westpac and supports your move to increase rates/margins on your customers. However given the anticipated global move to low growth spurred by "deflation" in many cases, but you are not supposed to even mention that. Let alone the move by States to ring fence there back yards and protect there own industry it is hard to see any light at the end of the tunnel for sustainable interest rate increases.

Long term interest rates are rising, and will continue to do so.

We have hit the bottom of this cycle.

No we haven't. The bottom of the cycle doesn't happen until all the bad debt is wiped out (most of it) and the currency reset. The trend remains firmly down.

With debt levels so high, won't climbing interest rates will lead us into recession?

The joys of ZIRP, people have taken on too much debt and now must pay.

Trap sprung.

The interest rate rises are so insignificant at the moment it doesn't affect anyone.

Most people are still,on fixed at over 5 per cent and rates are under 5 per cent for the 3 year rates so once they come off their fixed rates they will be paying less anyway.

Rates aren't heading up much over the next 5 years as the U.S. can't afford to so the Banks are trying to scare people into fixing with them now.

interest raising is now the trend, I hope people have prepared for it,

trump will install 2 hawks into the FED to rebalance against the doves

WESTPAC, National Australia Bank online and other banks are planning to raise fixed and variable home loan rates by up to 60 basis points

http://www.news.com.au/finance/business/banking/westpac-increases-intere...

The US will have a tough time raising rates. There's the small problem of $20,000,000,000,000 of debt to service. Trump will have a tough time making America great again.

you cant make America great again without an easy viable plentiful energy supply - So its simply not possible.

Flatliners,saw the movie,it ended badly.dont bet the farm on those forecasts.

As I say the so called hiking at the moment is insignificant and won't be hurting anyone who is currently fixed.

The world can not afford to have high rates again and that certainly includes the United States.

Interest rates in England, Asia etc. are still very low and it would not be in their interests financially to have much higher rates.

Not too sure why many on here are wishing them to be much higher as it will affect everyone dramatically, and that includes the ones who don't own property.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.