By Gareth Vaughan

Six-and-a-half years ago the sky seemed to be the limit.

In mid-2014, with the Financial Markets Authority (FMA) poised to hit the "go" button on the local licensed peer-to-peer (P2P) lending sector, it was being suggested that P2P lending could be to banking what Walmart was to retailing, or Ryan Air was to airlines.

P2P lending licences granted by the FMA would enable successful applicants, as intermediaries, to run websites matching borrowers with lenders and charge fees for doing so. This would be a new form of consumer and small business borrowing, and a new fixed-income investment option for savers.

As Elaine Campbell, then the FMA's head of compliance monitoring told me in April 2014: "It's a bit like an online dating service. Essentially what they are doing is introducing people wanting to lend money to people wanting to borrow money."

This lightly regulated marriage of technology and money lending appeared to have the potential to rattle the cages of New Zealand's remaining finance companies, plus our credit unions, building societies and ultimately even the banks. P2P lending was already making waves overseas in countries such as China the UK and US.

I certainly saw potential in P2P lending writing the following paragraph in June 2014:

"Peer-to-peer, or P2P, has the potential to cut a swathe through the world of small, consumer lending focused finance companies... But it goes much further than that. P2P has the potential to be to banks' consumer and SME lending what Trade Me is to the world of second hand sales and newspaper classified advertising. It also has the potential to have a significant impact on banks' deposit gathering."

However Thursday's release of the FMA's annual statistical report on the P2P and equity crowdfunding sectors, covering the year to June 2020, shows the sector is a very, very, very long way away from fulfilling its potential.

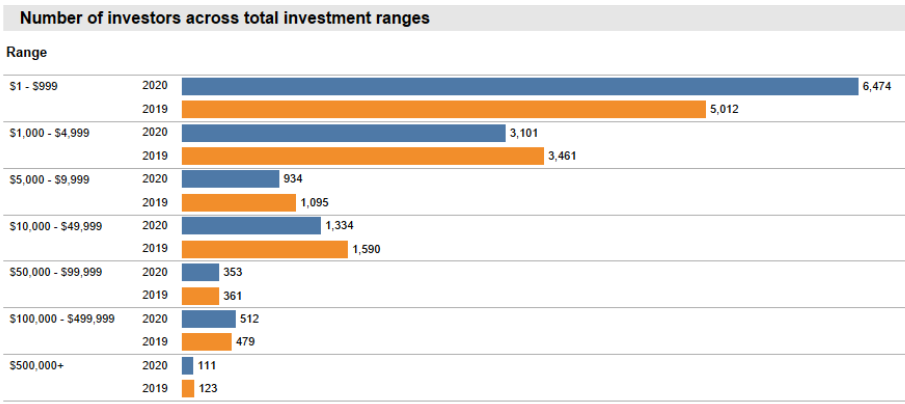

Here are some of the key annual statistics. The total value of outstanding loans across the seven licensed P2P lenders reached $624.3 million. Compared to Reserve Bank data on total lending outstanding across the consumer, housing, business and agriculture sectors of $481.806 billion at June last year, that's miniscule.

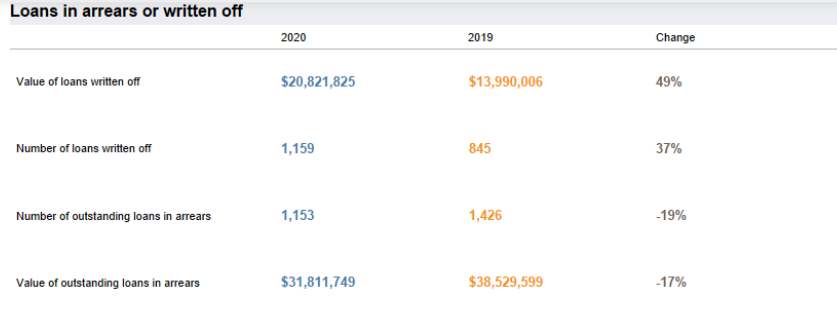

The FMA statistics also show 22,840 outstanding P2P loans, 34,290 registered investors, albeit just 12,819 investors had open investments even against the backdrop of very low bank deposit rates. There was $12 million worth of secondary market trades, just four borrowers had reached the $2 million maximum borrowing amount, total registered borrowers stood at 418,495, the number of loans taken out by by repeat borrowers was just 1512, and the number of outstanding loans to small businesses was just 375 valued at $163.4 million.

Harmoney, which accounted for $387.3 million, or more than half the total outstanding P2P loans, withdrew from accepting retail lenders last April. That means the biggest player quit the market. Albeit Harmoney was sourcing the bulk of its loans from TSB, Heartland Bank and institutional, or professional, investors anyway.

Of course P2P lending is still a relatively recent phenomenon in New Zealand. At some point in the future it could still grow to meaningful scale. Maybe there's a dynamic newcomer around the corner. Or perhaps it's just a slow burn and real scale may take years or even decades. But for now it has underwhelmed. It just doesn't appear to have attracted the attention of enough New Zealanders.

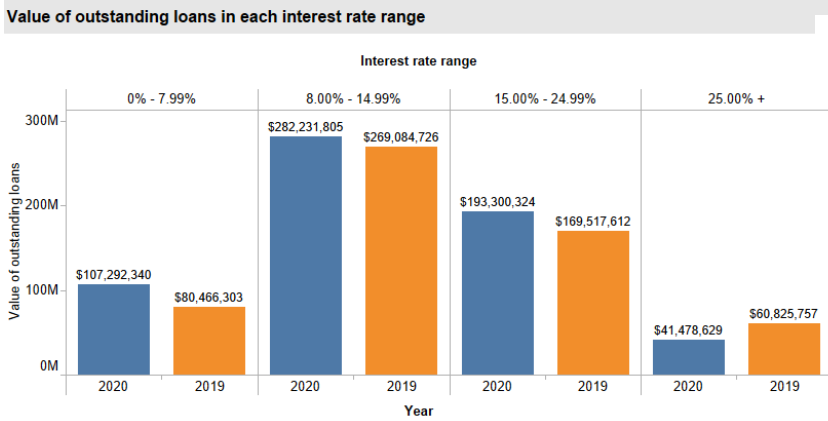

In a world where a bank raising its five-year term deposit rate 75 basis points to 1.75% is headline news, you'd think the P2P interest rates on offer might attract more investors, or savers. About 76% of money loaned through P2P platforms was earning between 8% and 25% in the June year. Perhaps New Zealanders' obsession with property investment is preventing P2P growth, or our inherent conservatism. Or maybe most of us are just happy with our traditional lenders and feel safe with our money in the bank.

And heck, if P2P lending was growing fast we'd be calling it a bubble and worrying about what might happen if it pops.

Now that the high profile Harmoney, following its unsuccessful battle with the Commerce Commission and founder Neil Roberts' suggestion there's no viable P2P lending model in NZ, has left the sector, P2P may fly below the radar for a while.

Certainly if Harmoney's business model always appeared to be a sprint towards a share market listing, something fulfilled recently, some remaining operators such as Squirrel Money and Lending Crowd, certainly appear to have a business model that has more in common with a marathon. And that is probably a good thing.

In response to Roberts' questioning whether there's a viable business model, blaming regulation, Squirrel Money founder John Bolton told me in 2019 that running a P2P business in NZ is doing the "hard yards" because it's a low margin business. Here's more of what Bolton said:

"It’s a tough market to profitably grow in and to get rapid growth," says Bolton.

"The challenge is that finance companies make big margins on their rates with borrowing [interest] rates around 20% and funding rates around 5%. That compensates for lower fees but also allows them to aggressively advertise. They’re also operating in a part of the market that is not rate sensitive. They simply want the money. It’s a higher risk segment and that is reflected in arrears and default rates, but it is also very profitable provided you have low funding costs," Bolton says.

In contrast P2P is a lower margin business.

"We are on average paying out about 7% to 8% to investors and charging borrowers around 12.50%. [So] 3% to 4% margin makes the model difficult, especially when it comes to having to spend money to acquire customers. To get higher margins requires investors earning less, and that’s when the attraction of P2P investors drops off," Bolton says.

"Harmoney is effectively becoming an online lender leveraging the same model as finance companies to extract lower funding costs through securitisation and high borrower rates giving a big spread. It has a similar target market to finance companies. This will be a very profitable business model for them as it is for finance companies."

Back in 2014 P2P lending was the hot new thing in financial services. Seven years later the heat is certainly long, long gone. With Harmoney no longer welcoming retail investors, the sector's likely to have a lower media profile, at least for a while. That might not be a bad thing, letting it grow slowly. Nonetheless the lack of scale and SME lending in the P2P sector nearly seven years from its birth is disappointing. Whether this will significantly change, only time will tell.

*The tables and charts below come from the FMA.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

26 Comments

It is doomed to fail now!!

Banks are currently awash with customer deposits. Mum's and dad's have decided to personally deposit billions into the banks. Because banks are awash with customer deposits which is then used to lend out.

So when was the last time you woke up with a LOWER balance in your account because your bank loaned it out? Never I'd say.

Deposits aren't your money. You account balance is a reflection of debt the bank owes you.

Wrong Zack

Dave Chaston has said on this site banks take deposits which is used to lend out on mortgages. And banks are awash with customer deposits at the moment. Which means the economy is strong because banks don't create money all money is existing.

Wrong PonziKiwi

David Chaston over simplified an article and was too ambiguous with his phasing - ONCE !! Then a bunch of savants/dilettante commenters jumped on!

Most people on interest.co.nz, especially the authors like DAVID understand money is created through bank lending (debt). It's the first thing new comers remind them of when they get here.

interest.co.nz has produced [as you know?] great content on MMT. Let it go PonziKiwi, you're like a-dog-with-a-bone on this one. David is like a wee Yoda, he's kool man, chill.

Zack

Dave does not support the credit creation theory. He supports the money multiplier pushed by academics and Don brash. He has said banks don't create money but the banking system does. This is wrong and he needs to be corrected.

Retail Banks are part of the banking system. Though it is true money (aka debt) is created/enters the system when loans are made. It is also true that 'Funding for Lending' is provided by the likes of the RBNZ. That's not to say Retail Banks ring the RBNZ every time they make a loan (aka create debt).

Banks are asked to hold reserves.. so one could impute (aka 'make up') a factious fractional-reserve-ratio.. but I don't think David has EVER used the term 'money multiplier'.

There are no reserve requirements in nz..

They are required to hold some funds for "financial stability reasons", BUT really it could be irrelevant:

If banks make a bunch of bad loans they could just loan ME 100 Billion on the agreement I buy their bonds with it, therefore recapitalizing themselves. If the annul-bond-yield I receive is more than the annul-payment on my 100 Billion debt, everybody is happy? lol

OR

If Million Dollar Houses in Auckland were suddenly only selling for $350,000 - property investors might choose to go bankrupt rather than paying off 1 Million for a house(s) now only worth $350,000. Retail Banks would then be on the hook for the 1 Million Dollar loans but only have $350,000 dollar houses. SIMPLE, the RBNZ could buy the junk loans ($350,000 houses) AT FACE VALUE (for 1 Million Dollars/Outstanding Amounts).

NOTE:

The above examples wouldn't directly put money into the domestic economy, therefore they would NOT directly cause inflation. HOWEVER, Retail Banks would again have healthy balance sheets and be able to lend - therefore reinflating-house-prices and causing inflation in general. Obviously if banks get to this point they have failed and probably shouldn't be bailed out to destroy the country's economy a second time.

Also in my first example, creating money out of debt - I probably wouldn't be a credible borrower for 100 Billion in debt.

Zack

Prof Richard Werner proved individual banks create money. Both Brash and Chaston said they don't but the banking system does. Werner in a speech said that argument is the Fractional reserve theory which is a myth. Until society and the media are aware of how it works absolutely nothing will change.

https://www.interest.co.nz/business/90794/rbnz-analysis-suggests-banks-…

Zack here is the link scroll down to dave Chaston comment and explain to me what he means and I'll let it go... Cheers.

@ PonziKiwi

When the Retail Banks make new mortgage loans, aren't they drawing [low uptake so far] from the RNBZ's Funding for Lending? Therefore incurring the debt obligation of the mortgage loan and the prescribed interest-rate (Cash Rate) to the RBNZ. Isn't that really the RBNZ lending? Only the Retail Banks have been imbued with the RBNZ's Power of Money (debt) Creation?

Retail Banks are the liquidity gateway to the domestic economy. They can keep creating money (debt) with their imbued power, until they can't. Banks still have to pay back the money (debt) you borrow. If someone loans $1000 and with interest pays back $1010 dollars - the bank doesn't make $1010, It makes $10 (tops). The money supply has been increased by $1000 until it's paid back, then the money supply is reduced by $1000.

Obviously Retail Banks get some funding from foreign markets.

Thanks Zack

I'll let it go... I just wanted someone to spell it out. So in effect werner is incorrect.

If I'm wrong please, please tell me. I'm not sure about things like over-drafts and their relation with central bank lending, etc.

Also more debt is being created than money when loans are made. Therefore the Banking System is a game of musical chairs, or needs lots for money velocity/inflation. Bankruptcies are good for clearing out bad loans/debt. Unfortunately the 'too-big-to-fail" mindset, constant government bailouts and cronyism is rife. Inflation is theft too, just another tax on the people.

The whole system is a bit odd, especially interest only loans and people using unrealized equity.

If all fiat debt was paid in full, theoretically their would be no fiat money.

Werner is correct that banks create money

Werner is correct that banks loan money into existence

David is correct that the banking system creates money

Now, lol Don Brash was WRONG

Also Retail Banks in the likes of Japan and Germany may operate differently to NZ Banks.

Werner would benefit from using terms like Retail Banks. Many commentators unfortunately group central/retail banks together as; "The Banks". I think Werner wrote a book about the Yen and Japanese Banking, I've watched the documentary version - Princes of the Yen (it's on YouTube). Werner noted the BOJ (Bank of Japan) once had leading quotas that retail banks HAD TO REACH. The BOJ was like, Bro, I don't care nobody wants to borrow - you still have to lend~!! lol

Wow you da man Zack..

Banks, often together, use their size to corner markets and create bubbles.. banks profit along with government and retail investors - anyone riding it up really.

Bubbles can be made in energy-markets, soy futures, silver-&-gold, whole stock markets even. Rural Banks could theoretically create regionalized farmland bubbles. Government often turn a blind eye to these bubbles if they feel voters are benefiting. But really it's a misallocation of capital.

NZ banks seem to like blowing housing bubbles. I'm not sure why NZ banks have kept inflating house prices, just lazy and myopic perhaps - they should have moved on and blown bubbles elsewhere in the economy - not just ONE giant bubble of expanding social disfunction lol. :)

Bubbles are picked/created by those whom have access to cheap funding (often banks). If (in NZ for example) you have equity in property, you can access cheap money and invest it in The Housing Bubble. If you don't have access to cheap money and require housing [silver, energy, farmland, whatever bubble] you're on the losing side of The Bubble.

Whoever gets the cheap money first.. well they get to buy the various assets before prices-go-up/bubble-sets-in/inflation. It's a Biflationary/Cantillon

Bubble effect really.

Ideally targeted [small to medium? lol] bubbles could create new industries by acting as an incentive/stimulus.

That's not how it works. The Bank of England and the Bundesbank both have articles on their websites explaining how commercial banks create new money when they issue loans.

Professor Richard Werner conducted an experiment to prove this. Details here: https://www.sciencedirect.com/science/article/pii/S1057521914001070

Also, another article from the BIS stating the same: https://www.bis.org/review/r180118c.htm

https://www.forbes.com/sites/francescoppola/2019/09/17/if-you-dont-unde…

Gold Kiwi

Correct werner is correct. Werner promoted the credit creation theory which he proved.

Chaston does not believe this theory..

It was the ird that killed it for me.

Their inaction to address the blended return of written off loans resulted in an unworkable situation for me.

But the ird plan has worked and the problem has gone away as the industry has folded.

This is exactly it. You can only write off the bad debts if you were a company for the purposes of the lending. Essentially the bad debts are such a drag on profitability (with IRD cashing in on money you have lost and is not recoverable) there is no point putting money into it.

Unless tax laws or IRD opinion changes then P2P lending is dead in NZ.

That's how I understand the current situation. Unless IRD apply a more sensible approach P2P will remain a flop:

https://www2.deloitte.com/nz/en/pages/tax-alerts/articles/peering-into-…

You could say that about all sorts of industries though, regulation and tax bias act to preserve the status quo.

I don't ever see P2P lending being a threat to traditional lenders such as banks and even finance companies.

The reality is that with the ability to leverage of the equity in one's home (not only for investment property) at interest rates of around 2 to 3% means that any borrower seeking P2P will not have asset equity, nor be considered a sound risk by traditional lenders meaning that are exceptionally high risk.

OK for those lenders prepared to take that risk but it is only ever likely to be considered as a gamble, and money that they must be prepared to lose.

For the majority with money to lend are by nature prudent to have that money in the first place and largely probably older and more conservative and risk aversion . . . and even then many of these will still remember the GFC experiences with finance companies.

So P2P will never seriously threaten or displace banks and even the brick and mortar finance companies.

I think P2P lenders should change its focus more onto their mortgage lending businesses to improve its prospects. There're lots of FHB in the market requiring liquidity as well as investors looking to expand their portfolios- a huge but lightly tapped market. Secured lending would also improve it's risk rate by categorial change and that will justify their current profit margin to all stakeholders.

The growth in buy now pay later schemes has probably moved into a bit of this space on the borrower side?

It is just another scheme to help people to fail. Offering money for small items without having to save. Interest over a life time paying for basics is staggering. Anyone tempted by this type of lending will never get far.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.