By David Hargreaves

Detailed analysis by the Reserve Bank suggests that banks would struggle to close the recent gap between what they take in through deposits and what they lend just by hiking the interest rates on deposits.

The analysis goes on to conclude that if they are not to become over-reliant on overseas borrowing, banks may need to pull back on lending (which some have been doing) or use some other "combination of approaches" to bring deposit growth back into line with credit growth.

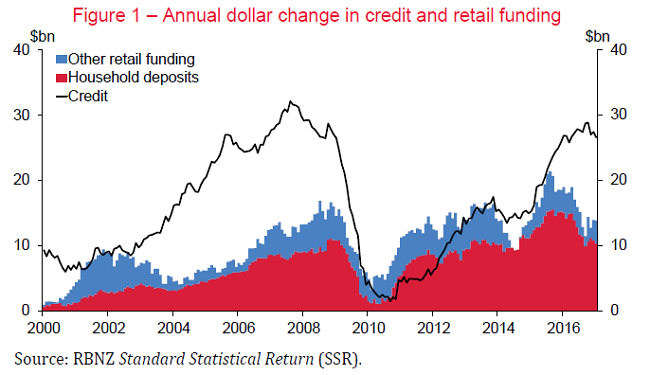

In the past year or more a gap has developed (though it has shown signs of decreasing more recently) between the banks's deposits and lending - with credit growth having been particularly strong.

Banks were increasingly borrowing offshore to fill the gap in their funding, but the RBNZ had certainly suggested earlier this year that some of the banks were getting close to the limits of what they could do in this regard.

The funding gap saw mortgage rates edging up late last year and into this year, while some deposit rates also firmed as banks sought to attract more deposits in. Some banks talked openly of 'credit rationing'.

In response to these recent developments, the RBNZ has produced an 'analytical note' by Jed Armstrong and Nicholas Mulligan, titled: Diving in the deep end of domestic deposits, which aims to answer the question of whether banks can close the funding gap simply by hiking deposit rates.

The answer is, essentially no - or not sufficiently.

Armstrong and Mulligan say over the first half of 2016 there appeared to have been a change in household preference that resulted in households wanting to hold less money in deposits.

"This may be related to the increase in consumption and residential investment," they said.

"At the same time, demand for deposits from banks was modest. During this period, banks were largely funding the deposit deficit with market funding, given the easy availability and low cost of offshore funding.

"Since then (that is, through the second half of 2016), banks have increased their demand for deposits in an effort to close the funding gap. For example, this change in bank behaviour may reflect that banks were reaching internal limits on the proportion of funding which they obtain from offshore markets. It may also indicate an increase in competition for deposits across the system."

Since mid-2015, annual banking system credit growth has averaged 7.6% and materially outstripped deposit growth, Armstrong and Mulligan say.

"At the end of 2016, annual credit growth exceeded annual retail deposit growth by $13.5 billion."

They say this is not the first time a gap between credit and deposit growth has been observed. From late 2002 through to the end of 2009 credit growth exceeded deposit growth by a significant margin.

"However, considering post-GFC reforms of bank funding profiles, changes in bank appetite for offshore exposures, and the discipline of credit rating agencies, it seems unlikely that banks will ever again be as reliant on external funding. Therefore, in the current environment, banks may need to restrict credit to grow more in line with deposit growth or increase deposit growth to support credit growth."

Armstrong and Mulligan say their modelling suggests banks can increase the rate of household deposit growth by increasing deposit interest rates, but they go on to suggest that the impact of this alone would not be enough.

"Our models suggest that a 1 percentage point increase in the six-month household deposit rate would increase household deposits by around 1% after four quarters, and by 1.3% in the long-run.

"However, total retail deposits would grow by less, as the growth in household deposits appears to come partly at the expense of lower growth in other retail deposits. Deposits are also more expensive if raised quickly, rather than over a longer time horizon.

"Overall, banks would only be able to marginally reduce the recent gap between credit and deposits by increasing deposit rates by 1 percentage point. Therefore, if banks wish to maintain robust funding profiles by not becoming too reliant on offshore wholesale funding, they may need moderate credit growth or use a combination of approaches to bring deposit growth in line with credit growth."

18 Comments

I've banged on about this suggestion before. I suggest that the government could remove the tax deductibility for the inflation portion of the interest on loans and similarly make the inflation proportion interest on loans tax deductible.

That would be an Investment Bankers delight! Anything that's a new set of rules will be exploited.....

Goodness me David, isn't this discussed before?

Banks don't lend money from deposits, they create money out of nothing.

They are not the intermediary between savers and borrowers.

I suggest you watch the below discussion with Prof. Werner, it's absolutely worth your time.

https://www.youtube.com/watch?v=EC0G7pY4wRE

And remember the articles in the NZ Herald by Bryan Gould and Don Brash?

It amazes me Brash didn't know, or perhaps he wanted to keep the confusion going, remembering Henry Ford's quote:

It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning.

Here the articles in question:

https://thestandard.org.nz/gould-explains-how-money-works-to-brash/

The banking system creates money, individual banks themselves don't. See this. It is a result of their lending activity. It is strictly regulated. And it works in reverse; if loans aren't made, the system will remove money.

Banks are very dependent on deposit flows, and more generally on the liability side of their balanace sheet.

Think about it. If they could individually just conjure up money as you suggest, there would be no bank failures, and no need for regulation. Nor would there be any need for capital. They would be forever safe. But that is not the case. In fact excessive leverage (too many liabilities to depositors and other lenders) is dangerous.

Which is why they need deposit money to lend. They worry about funding (liabilities), as they should.

The article you reference has a 10% reserve requirement, but I thought the banks only had to have 25% weighting on household mortgages as they are deemed so very safe. Maybe that is in Australia and we don't do rash things like that here. However 25% of 10% works out to 2.5% reserve requirement. Am I missing something?

You are not missing anything. The referenced article assumes New Zealand operates a fractional reserve money multiplier facility similar to the US, which by the way has been moribund for decades.There is no evidence of vault cash or borrowed reserves of the magnitude potentially required (10%) registered on any published RBNZ ledger.

RBNZ S10 declares a minuscule bank wide $667 million cash and notes asset ledger to theoretically reserve $421,287 million loans and advances - 0.1583%.

But I must point out you are noting bank regulatory capital leverage via RWA, which is maintained against assets for financial "stability" purposes. Banks moved on and no longer leverage cash using a fixed 10% retention level/multiplier to create liabilities. That function has been superseded by the model Peri kindly linked - read more

David, you often reference this 2008 note RBNZ, but it is based on a fractional reserve perspective: - there are now numerous recent papers which better describe the money creation potential of banks (such as from

Deutsche Bundesbank April 2017: “ The role of banks, non-banks and the central bank in the money creation process, and

Bank of England, Monetary Analysis Directorate "Money creation in the modern economy")

These papers show the potential for money creation to be much less benign than the RBNZ portrays.

Thank you David for explaining so well what is sadly a very common misconception.

As Mark Twain said " It ain't what we know but what we know that ain't so "

You may wish to consider the words of a former RBNZ economist before you embarrass your self further.

Mitchell has it in for mainstream academic economics. Quite probably there is something in what he says about that. Between the sort of internal incentives (“groupthink”) that shape any discipline, and the inevitable simplifications that teaching and textbooks require, it seems highly likely there is room for improvement. If textbooks are, for example, really still teaching the money multiplier as the dominant approach to money, so much the worse for them. But as I pointed out to him, that was his problem (as an academic working among academics): I wasn’t aware of any floating exchange rate central banks that worked on any basis other than that, for the banking system as a whole, credit and deposits are created simultaneously. He quoted the Bank of England to that effect: I matched him with the Reserve Bank of New Zealand. Read more

Nope, banks create money, it is a known mechanic. Banks can issue a loan because it creates a deposit when it is issued. The BOE confirmed this is the process by which 98% of money is created.

When I issue a loan it becomes a deposit in the borrowers account. That doesn't mean that i dont need a deposit, I do, but initially that deposit is met the loaned money. After that money gets spent then i need to borrow money from another bank that received those funds or, over night from the reserve.

Mining gold, labouring and many other enterprises create credit - not just the banking system.

If the GFC is over, why do we need the RBNZ to determine the cash rate to stimulate spending (not necessarily growth)

If the banks can get low cost cash overseas, end user rates may lower, if banks are up to the eyeballs in borrowings themselves and cannot meet the cash reserve criteria talked about, then rates may increase - that is the market in play. That is self balancing and good.

People must remember cash is a commodity. The RBNZ does not regulate the currency, or other price points and should not dictate interest rates. The result of low rates is savers cash flows into assets for protection.

Only need to be able to count to figure that out.

Those exodusing out of Auckland to the provinces only need a relatively small deposit,

https://www.tvnz.co.nz/shows/moving-out-with-tamati

More articles everyday on economic refugees exiting Auckland

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11942708

I read that article. Interesting story about living in Sandringham. The writer seems to think that Sandringham has always been little India. Sandringham was my home town when I was a boy and was a very typical Kiwi place with a fish & chip shop, a toy shop, chemist, ASB, Post Office, second hand shop and a dairy or two. Fish & Chips cost 30 cents and they were really good.

I was intrigued that she wrote this:

When a Monteiths bar opened in Sandringham, I was incredulous. Its predictable modern architecture felt out of place in the jumble of Indian restaurants and spice shops, its name - a throwback to a commander in the Indian army - insensitive to say the least.

Like it was a crime that a Montieths bar opened in Sandringham, something quintessentially Kiwi. Shaking my head, I did a bit of digging around and found that a Stewart Monteith took over the Phoenix Brewery in the South Island in 1868 and his son William carried on the family tradition in 1920.There was a William Monteith a British soldier who rose to the rank of major-general while in India in 1841 but as far as I can tell never had anything to do with Monteith's Brewery. He died, half a world away, before Stewart Monteith even started the brewery. Just because a fairly minor player in India shared the same name as Stewart Monteith's son it is somehow an affront to people of Indian heritage living in Sandringham for there to be a Montieth's bar there?

The writer is an import - only been here a couple years - and already telling you what you should or should not be doing (to your place)

Defensive Zach

You cannot possibly compare your childhood in Sandringham to the young writers experience today

Sandringham was a suburb of working class cottages predominantly which now require an arm & a leg to purchase a tiny box.

The writer should not remain in NZ but seek higher remuneration and better climate in Australia like most aspirational young kiwis do who don’t move to Europe or Nth America

It was pretty sad reading her heart jump driving over the Auckland harbour bridge She needs to move to somewhere bigger than Auckland and definitely not Dunedin

Life’s short & it’s sad to be trapped in one country

I don’t see why NZ banks AKA AU bank subsidiaries try a little harder to attract depositors funds from savers in other countries if they require more real deposits there are millions of people up here earning less than 0.5%

or no interest at all who would like to earn more interest on their savings but cannot. Perhaps directly offering

bank accounts to foreign savers but I suppose they’ll be laws to prevent capital flight.

It truly is pathetic what savers earn in Nth American banks & fees are ridiculous

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.