By Bernard Hickey

What would happen if the world judged New Zealand Inc was unable to service its debts?

Who would put us into receivership and what would it look like?

Unfortunately, these are not idle questions any more. Our net foreign debt is as high as Greece's and Ireland's, both of whom have just suffered the indignity of being 'bailed out' by the international powers-that-be after effectively being judged bankrupt as nations. In their cases the International Monetary Fund and the European Union dictated massive cuts in public spending and new taxes. Their downfalls were preceded by credit rating downgrades.

Standard and Poor's put New Zealand's AA+ credit rating on negative outlook a few weeks ago. As recently as March last year Ireland had a credit rating that was one notch better than New Zealand's. The former Celtic Tiger also once had public debt levels similar to ours relative to GDP, but now has a rating four notches below our rating.

New Zealand's growth rate has been the slowest in the OECD in the last 40 years and shows no signs of improving any time soon. Our government is borrowing up to NZ$300 million a week and is running a structural deficit running at about 4% of GDP.

The government has just announced a slump in revenues leading to a cash deficit of NZ$15.7 billion or 7.7% of GDP this year. It has also just increased its borrowing programme by NZ$10.5 billion over the next 3 years. That is almost all foreign borrowing. See more here.

In fact, it's somewhat strange that we haven't already been hauled over the coals by our creditors and the markets.

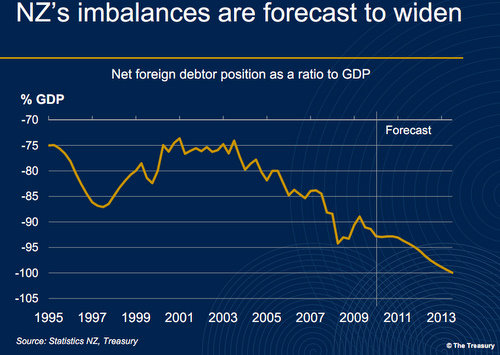

Our net foreign debt is set to widen past the 100% of GDP danger point in the next four years, Treasury has forecast, although the government believes stronger commodity prices will help reduce that widening in coming years.

Our net foreign debt is in the Greek/Irish/Portugese/Spanish zone.

Understanding why we've gotten off so lightly helps explain what any bankruptcy might look like.

New Zealand's foreign debt problem is a household debt problem, rather than a government debt problem, like it was in Greece and Ireland. Actually, our foreign debt problem is a corporate or bank debt problem because the debt is owed via households through the big four Australian-owned banks.

'Let them win the Bledisloe'

This is the key point.

New Zealand's economic future is in the hands of the Australian banks and the Australian Government if we ever have trouble servicing those debts. The pivotal point in any future crisis will be the reaction of the four CEOs of those banks and the Australian government behind them.

In fact, we've been here before.

Back in October 2008 when the financial world was going to hell in a handbasket the Australian government stood behind those Australian banks by offering a retail deposit guarantee and a wholesale deposit guarantee. We immediately offered the same, although our guarantees have since been withdrawn faster than the Australian guarantee.

That pivotal decision was a pre-emptive one taken without much consulation with the New Zealand and it was disguised as a backstop for the banks in Australia.

The untold story is that those banks, their shareholders -- and the Australian government indirectly -- bailed out the New Zealand arms of the big four banks in late 2008 and early 2009. They were helped by some emergency loans from the Reserve Bank of New Zealand, but without around NZ$5 billion of fresh capital sent across the Tasman at short notice they would have struggled. See more here in this June interview with NAB (and former BNZ CEO) CEO Cameron Clyne from 7 mins on in Part II) .

The 4 New Zealand arms of the four Australian banks weren't able to raise funds in their own right on international markets for many weeks. They relied on their parents for support.

At that time New Zealand couldn't be blamed for the freeze on international capital markets.

But what happens when or if we are targeted for something we've done or haven't done?

Can we simply expect the Australians to back us again? Is the Australian backstop something we can rely on? Should we just lie back and trust that they'll always be there?

What might happen if they aren't or want something more in return? What if they are in trouble themselves in the even of a Chinese slump or an Australian property crash.

Have they already asked for their pound of flesh?

The key trigger points

It's worth, therefore, wondering what might trigger another one of these pivotal moments and what we should do to reduce our risks.

Luckily for us, our government debt is relatively low at the moment, although it is growing fast. For Ireland and Greece, a sharp rise in Government bond yields was the symptom and trigger for their crises.

Bond markets essentially judged Ireland and Greece's public finances as unsustainable. The first canary in the mine was a rise in credit default swap spreads versus benchmarks, and then a rise in the bond yields themselves.

These rates set the basis for all interest rates, including the ones New Zealand's banks have to pay when servicing their corporate debts. If New Zealand were to be downgraded and our government bond yields were to diverge too much from Australian rates then it becomes painful for the banks.

As longer term interest rates rise, that puts more pressure on the economy and therefore on government finances. It becomes a vicious spiral.

Luckily, for New Zealand (and unlike Greece and Ireland), we have a flexible currency. In theory, a downgrade in our credit rating would force the New Zealand dollar lower, which would boost our export earnings and the economy more generally.

A debt spiral

But what if the economy doesn't improve much, particularly the domestic sector, which has been dependent on rising house prices and increased foreign borrowing in the past. Or America, Europe and Japan continue printing money aggressively to devalue their currencies, leaving ours high and dry?

What if the deleveraging that surprised everyone this year continued into next year, and the year after that? GST revenues, which the government is now relying on more heavily, would lag. Corporate profits would be weak.

Luckily for us (and unluckily for Ireland), the New Zealand government has not bailed out its largest banks and blown out public debt to fill a financial black hole opened up by a property collapse.

There has been some limited socialisation of financial losses, led by more than NZ$2 billion worth of payouts to holders of debentures in guaranteed finance companies. Unlike in Australia, the bulk of the guarantees of deposits have now rolled off, although there is still a significant amount of guaranteed wholesale bank bonds. There is the non-trivial matter too of losses on leaky buildings, some of which may be borne by the government. See more here.

The real concern for the Australian banks starts when New Zealand customers start defaulting on their hefty household and farming debts, particularly if land and property values continue to fall.

The banks have had a sneak preview through the vineyard industry and parts of the dairy industry.

What if the CEOs of those big four banks believe that New Zealand's government is headed in the wrong direction and is keeping interest rates higher than is possible by running big deficits.

What pressure could they exert?

Covered bonds

One element of bank lobbying we have already seen is from those banks who wanted to be allowed to issue covered bonds overseas.

The Reserve Bank has been "very progressive" in supporting this push into covered bonds, which effectively push New Zealand depositers down the queue in the event of any problems and which were banned in Australia, at least until this week.

Back in 2005 the Reserve Bank had to fight a rear-guard action to keep control of regulation of the banks here in New Zealand. Then Australian Treasurer Peter Costello argued New Zealand had already ceded control over its banks when it sold them.

Governor Alan Bollard and his backers within the bank and Treasury successfully fought off that push.

Would they be able to fend off another set of demands when New Zealand is in a weaker position?

We should prepare

The best way to avoid this sort of risk is to have a much stronger economy and budget position. That means a much faster move to budget surplus. That is the fastest way to increase national savings and avoid building up more debts we may struggle to service.

We also need to use any prudential tools we have to stop the Australian banks borrowing more offshore. Are massive new issues of covered bonds a good idea? Particularly when they are being used to increase investment in property, rather than repaying short term borrowing.

The early signs are that these new foreign borrowings are being deployed into the housing market, helped along by the income tax cuts that are worsening the budget deficit.

Your views?

56 Comments

Bernard: The best way to avoid this sort of risk is to have a much stronger economy and budget position.

But we will never have that with John Key at the helm. Big governments can not make the economy stronger. We can argue a small government can have a positive influence, but a government like NZ that takes up 50% of GDP sucks the life out of everything. But the Nats are firmly committed to the socialist model that has bankrupted every country that has ever tried it.

Unfortunately we are to far advanced for that to happen, i.e. we have too many people dependent on the government. With 1.7 workers per beneficiary, there won't be a change ever.

That's the sad truth.

Even sadder are the Nat supporters that would scream if Helen had ever delivered a budget like this. But in one year John Key has delivered a deficit that is worse than Helen in 9 years. And Labour's answer is the same as always: spend even more.

Mining? Can't do that, our precious snails and ferns can't have that. Building? We need to suspend our laws to get anything build in this country.

So nothing will happen, until the big downfall. And it will be even quicker than Ireland.

Another blinkered-horse comment.

These whinniers don't think much, eh?

This isn't about Aunty Helen, John Key, or any glib two-worders (tax cuts, economic growth, going forward, step change).

It's about exponential growth just hit the ceiling.

Multiplying people and multiplying their per-capita consumption was a temporary thing, but all borrowing was done on the basis that growth would inflate it away.

Sadly, on the downside, the reverse must be true. Chase the goal-posts by all means, but they will retreat from you at exponentially-increasing speed.

The common fault is to think the temporary paradigm that has existed for a few lifetimes, was a permanent state of affairs.

Sure, reduce debt. The best way I know is not to purchase anything. I defy you to maintain a growth regime while doing so, though.

I think the thing is, when people see problems with deficits they immediately look to those managing the show. Surely in recent times when countries have gone bankrupt it has been due to financial mis-management by those in power?

Not many people are looking at the fundamentals, which now due to global peak oil (and hence peak everything derived directly and indirectly from it) are causing the cost in real term of everything to increase. This is a fundamental game-changer. I believe the whole picture is quite complex, but while people are believing the current mess the global economy is in can be blamed on the few in power, then I think they're missing the bigger picture. The bigger picture being that from here on in there's going to be less to go around. Combine that with a glowing population and it's clear our standard of living has on the whole just one way to go; down.

No one has yet made anything like a robust case for how or why potential mining revenue would offset the costs, let alone turn a profit for anyone other than the few at the top.

And building? How does more construction help us? Borrowing too much to take on huge mortgages for grossly overpriced property was one of the root causes of our current predicament.

Make some tough decisions: reduce or axe benefits across the board, including - especially - the middle-class and top dog corporate welfare rorts which have been bleeding the country dry.

Force people to save money if necessary, while offering attractive incentives to save. ("whine, banker bitches, whine!")

Make it extremely difficult for 'consumers' to live the borrow 'n' spend lifestyle. Cultivate and inculcate an attitude of frugality and good sense.

Or we can just keep borrowing so that NZ's wealthiest and a bunch of dribbling PIs can continue to live the extravagant lifestyle to which they feel entitled.

Malarkey, you might be right on mining/construction, but I'm just using these as examples that we can't even find out. The government has to suspend our laws to get something build in Christchurch, that shows you how big our problems are.

I fully agree on axing all benefits for middle class and especially for businesses. No more bank guarantees ever, and no more implicit taxpayer guarantees for any business, and get rid of the SEOs, as they have that implicit business guarantee and the big boys at the top are having the good life at this implicit taxpayer guarantee.

I can even agree on the consume lifestyle, but we really don't need any more government involvement. But a simple rule you can't charge more than 7% interest would take care of a lot of the problems.

But it won't happen.

During Labour the country was slowly regulated to death and all increase in our productivity (which was rising during the 90s) was halted. With National we're borrowing ourselves to death.

Not much choices left.

lets be sure of the facts....(im open to corrections here).....

The middle class are for better or worse the ones already handling the biggest tax burden and least services.....WFF etc doesnt (mostly) apply above $70k....up to that amount is really working class territory.....IMHO....I'd consider "middle class" as ppl by and large earning over 70K....if you want to consider salary/income as the measure....In fact Im not so sure NZ has much of a middle class these days....(I'd like to see the income distributions for NZ actually, compared with other countries)

Top dog rorts....I can certinaly agree with that.....but that is self-perpetuating. Personally the share market / system is now corrupt to the point its damaging us. The share holders are the big institutional investors who vote the CEOs big pay packets and big bonuses as long as they pay out big dividends and teh share prices rise.....

"Borrow n spend" There are some interesting examples Texas for instance where they limit by regulation say the max a householder can borrow is 80% and they had no huge property bubble. Steve Keen points out that the OZ Govn first time buyer scheme actually pushes up / leverages the price of a house up, and then that money passed onto the next buyer see's the same leverage again....the opposite effect of Texas's limits and oh look we have a huge OZ bubble...

The downside of "Borrow n spend" is that our economy is now set heavily in favour of retail and service jobs, and the infrastructure, businesses all work in or are aiming at retail. These need to be re-directed into different sectors you cant do that overnight....and it wont be easy to do that.

PIs, well there is a clear and positive case for professional landlords.....the problem is the mad speculation from PAYEs and self-employed rorting the system....the Nats changes start to correct that....but again you cant change that overnight....

In terms of borrowing, well in my case I have litle debt, (but then I dont have a huge income either) so I dont fear a housing collapse wiping 60% off my house value its no biggee its un-realisable anyway IMHO.

regards

Dont let reality, truth, real world successes get in the way of your fantasy...

There is big and there is BIG....a libertarian's defination of 'big' I suspect is anything over 2 ppl and a dog....(you set the dog on anyone who looks like they might want to work together for mutual support).

Govn often offers a better service and a lower cost, eg Public Health service....its 1/2 the cost of a private service when measured against GDP, ppl covered 100 v 75% and longer live expectancy....

Also when you look at periods of Labour/Democratic Govns its apparent that these periods are times of relative well being of a Nation...and the harder right (or left) a Govn the worse off we are.

In terms of socialist model, again there is "socialist" and SOCIALIST.....typical Libertarian viewpoint.....anything that is left of the extreamist borderline anarchy line is Socialist....

For instance Sweden has a pretty socialist Govn model and its working pretty well, certianly better than any equivelent right wing model.....of which say the USA is a great example of a disaster area.

The sad truth is we have let the super rich and banks cripple our World economy, there is good cause to agree with GS's title "blood sucking vampire squid". This is what you dont get.....Govn's are the least of your worry......the taxes the super-rich and the banks put in real businesses and workers far outstrips the damge you perceive Govn tax does....

Snails and ferns.....Nzers can clearly make the choice about the quality of NZ environment....how many ppl have marched in protest? How many libertarians are there? Probably at 10:1 ratio against libertarians....

and what do you do when that coal is mined out? what you are suggesting is a delay treating the symptom instead of the cause....

The cause isnt big Govn its big banks and greed...

regards

Nice piece, Bernard. And sadly well summed up by BdB.

Good article BH. I hope this is going in the Herald also, and/or getting some air time on the MSM.

That 2008 chart is interesting - it would appear that the total net foreign asset position of the entire world was negative. Given that all debts are owed to someone, this can only happen if unerlying asset values have been massively written down - which is of course exactly what happened in the GFC.

But that then raises the question - how much can we believe any of this data? Which countries have written down their asset values correctly and which are extending and pretending? This is the crux of the problem for bond investors - NZ doesn't look great, but it doesn't have a whole lot of physical foreign assets to write down, so its probably not lying about its numbers. Can we say that with any confidence about any of the other countries on that list?

Bernard,

The issues around the risks posed by foreign bank-ownership are worth airing, but there are a couple of logical inconsistencies you need to work through before spreading this article around too widely.

1) "what if ...America, Europe and Japan continue printing money aggressively to devalue their currencies, leaving ours high and dry?"

Well then we won't be bankrupt. A high currency and sovereign default may happen sequentially, but it is inconceivable they will happen simultaneously.

2) What if the deleveraging that surprised everyone this year continued into next year, and the year after that?

Then private debt will drop approx twice as fast as public debt would if the money was spent and taxed. You want more money in the economy? Well then, you need to grow export income, not provoke domestic churn.

3) The best way to avoid this sort of risk is to have a much stronger economy and budget position.

No. A strong economy and a balanced budget are very good things, but the BEST way to avoid the risks posed by a foreign owned banking sector (who carry out their profit-loss accounitng in Au$) is to reduce their influence and market share. This requires support for kiwibank to poach customers (rather than originate new loans) and probably tariffs and taxation on the mega banks (a la the UK). Giving Southland, TSB and maybe Heartland (if they prove worthy) a leg-up would probably be a good idea too.

Chris B

Fair questions.

1. "what if ...America, Europe and Japan continue printing money aggressively to devalue their currencies, leaving ours high and dry."

The problem for us is our currency may be high enough for long enough to kill our non-commodity exporters. You're right a currency spike and a bankruptcy. They would happen one after another, particularly given the long lag times between building an exporting business/or killing it and restarting.

2. You're right about growing export income. Tough to do though when the government is running big deficits and keeping the currency high.

3. Good points on market share and encouraging local banks.

The problem at the moment is that the major local owned bank is one of the biggest offenders in terms of borrowing overseas to pump money into the housing market.

cheers

Bernard

Bernard, regarding your point 3:

This is obviously Kiwi Bank, so why is not the Reserve Bank or the Government be able to make sure they don't blow the property bubble even more, because they want to "grow"?

It is really insanity to offer 95% home loans! And this in a falling market! This is risk taking at the highest degree!

Have we nothing learnt from the recent disasters all over the world?

See Steve Keen on point 3.

regards

The Folly of Competitive Currency Devaluations

By Doug Casey

During our just-concluded Casey’s Gold & Resource Summit, Doug Casey spoke out about the folly that central bankers commit when they set out to deliberately weaken their currencies in the hope of gaining an advantage for their export goods and, therefore, for their economy. I dropped Doug a note asking him to quickly recap his thoughts in favor of a strong, versus weak, currency – his response follows…

A strong currency only hurts exports over the short run. Nobody seems to remember that the German mark was at .25, and the Japanese yen at 300 before the Nixon devaluation of 1971. The mark afterwards quintupled, and the yen has almost quadrupled since then.

A strong currency reduces the cost of imports, helping to keep prices in check. If the price of your currency doubles, the price of imported oil, machinery, technology, and everything else is cut in half.

Strong currencies attract foreign capital and encourage domestic savings. Businesses prefer to invest in a place where values tend to rise with the currency.

A strong currency encourages producers to be as efficient as possible. When domestic costs rise with the currency, producers run a tighter ship and substitute technology for labor. That is the path to progress. Using cheap workers instead of technology is a poor alternative.

Conversely, devaluing the currency simply makes everyone poorer. Most people keep their savings in the national currency, so are directly impoverished by devaluation. The only people helped (and only over the short term) are the relatively few companies that export.

In point of fact, governments have no business fixing the prices of currencies. It creates distortions, just like fixing the price of anything does. The idea of devaluing the currency to make things better is at least as stupid as the idea of printing money to stimulate the economy. And they have the same economic premises.

Why do we always suffer from NZ dollar weakening to help our country?

Completely agree here... a devaluation, competitive or not is a cut in living standards... so I can never figure out why we have all these people bleating on about demanding a cut in living standards... how and why is that a good thing??

The difference is someone taking a cut in living standard say 10% v being un-employed which cuts your living standard 90% to poverty.

De-valuation makes our exports cheaper abroad which means employment is protected, in effect we export un-employment elsewhere....what makes our country rich is earning foreign currency.

Thats why its a good thing.

regards

In other words, devaluing one's currency is a sneaky way for the government to remove money (value) from your bank account without actually going into the bank and robbing it.

Then IMHO the guy is an idiot...

He's only looking at one side of a coin....and extremes....and I think he has things back to front....

Much of imports are consumerism, this is generally bad, it makes importing and selling goods rather than manufacturing easier/cheaper...ppl get jobs in the importing and selling sectors rather than manufacturing....more bad news.

Imports, generally as the cost of imports rise sellers have to cut their margins as ppl will only pay so much for a good....if imports drop the selelrs often dont pass on the savings....

A manufacturer should be as efficient as possible anyway, the currency rising makes life harder and they can go out of business, job losses, exprt earnings losses, certainly a fairly strong currency isnt a bad thing, a weak currency would I suspect allow the manufacturers an easy time....so I suppose this is relative, ie depending on your neutral or starting point....

"producers run a tighter ship and substitute technology for labor. That is the path to progress. Using cheap workers instead of technology is a poor alternative." Generally I do agree with this though....but its a specific case of importing technlogy. In NZ's context our labour has always in Global terms been cheap, and because of our small and rigged import market technology very expensive and I see it every day in what I do.

Take a real world example....in IT

We were looking at a monitoring technology from a US vendor this allows us to monitor our virtual IT infrstructure automatically saving the labour of doing monitoring for faults and report writing manually.... If I was in America I could buy the software for $10000 US, buying it here in Oceana means I dont get that 50%+ discount I have to pay full price....plus the addons means that cost is over $30k NZD instead of $15K NZD.....now by the time I put a solution together Im looking at $50 to 75K NZD in the first year plus a 25% annual maintenance fee or I could employ a graduate at $35k a year give some basic trianing to watch things manually....

Now if we were paying the US price the tech becomes a no brainer....

Savings in local currency....if its a NZ grown carrot it still costs say $1.....it only makes them poorer if buying imported goods....

"The only people helped (and only over the short term) are the relatively few companies that export."

This is the whole point, the idea is to grow the number and size of exporting countires these make us richer....yes its only a short term help and if everyone de-values there is no gain......but take a look at the UK its doing just that and its helping it recover over the short term which is the point.

"Why do we always suffer from NZ dollar weakening to help our country?"

because our economy is set up wrong....if it was setup to make us as a Nation richer and not some individuals a weak(ening) economy would be benefit us....

and again when you take an extreme simplified example to justify why you do something then its no longer real world and relevent.....

NZ does not fix our currency directly, it does however have to influence it by policy so it advantages us.....

regards

Thanks for that Steven.

I am sure it is perfectly understood in economic circles. i wonder if you could explain it further. considering that .....

Our major imports are

crude oil

and gadgets - chinese made clothing, tvs etc

(I would imagine that the $NZ cost for importing oil is much greater than the gadgets)

our major exports are

soft commodities ie dairy, farm products.

If our dollar was stronger, then we would be paying less for energy - a good thing and would reduce the cost of manufacturing gadgets to export.

Farmers would get less NZ$ in exchange for weak overseas currencies. But it wouldn't matter because they would need less $NZ to buy what they needed including energy. That would mean they could develop their farms for less costs.

Or maybe our economy has already become too financialised already and the fact is .....

Of course we import savings from overseas and export 'interest' income. But isn't that just because of previous mismanagement of the welfare state?

I think that it is the financial imports and exports that could be the clincher in the import export equation.

Extra:

Doesn't your example of one price for us vs them in regards to US software indicate a

1 strong currency that has stronger purchasing power for US nationally and a weaker currency (in foreigners hands) for international trade?

Is that like double jeopardy when it comes to stronger currencies?

Maybe it is all too criminal for even the boldest of NZers to match.

Maybe we should be happy to ride a strong dollar when the opportunity arises - and pay down debt buy back assets

Just as we are 'very' happy' to weather the weaker currency to export and earn.

Excellent article Bernard.

What we need is for NZ'ers to realise the consequences of bankruptcy and to start putting pressure on the Govt to start serious reform.

Bernard,

this is a pointless and stupid article. its only purpose is to drive traffic to your website and nothing more... At least I understand your business model... shame no one else does.

Bernard, good on you mate for saying it you see it ,

Horace , you need to understand that one of journo's functions is to to provoke thought and influence public opinion .

Bernard is simply painitng a " What if......" scenario , which needs to be discussed .

To carry on the way we are and just accept our fate without strong opinion and public discourse on issues is dangerous .

We are Kiwis..... not lemmings.

As the Dutchmand De Boer so rightly pointed out , if we have 1,7 workers for every 1 beneficiary we are already in seriuos trouble.

John Key needs to be bold , he knows what do do and even if he becomes unpopular in his next term , he must do the right thing for New Zealand .

We need to be more aggressive in the face of other countries devaluing their currencies, and do the same if need be .We need to stare down the Anti-mining lobby

The Govt can stimulate employment through infrastruture development and get those on the benefit into work .We can run a deficit if it is in the development arena.

For example , we need a better road system , because congestion is costing the economy and it would be money well spent .

We can develop mining , fishing and food manufacturing .

We can relativley quickly become a centre for managing international funds . Auckland is a great palce for fund managers to live and work .

We can develop our capital markets , we can become a hub of innovation in medicine , research and technology.

The list is endless , and forget catching up with the Aussies , we can become the Swiss of the Asia -Pacific, and become the envy of those flycatchers .

We actually need a better rail system. Rail is head and shoulders more efficient than road networks. Peak Oil will quickly reduce the cost effectiveness of road transport. Rail is key.

If we are going to mine, then the benefits to the country as a whole need to outweigh the costs. And providing a few jobs on the west coast is not really a benefit to the whole country.

Fishing, sure thing. Again, by NZ companies in a sustainable manner. This means actually funding research into fish stocks by an independent body.

NZ inc simply needs to be far far more self interested.

The Sarah Palin solution in Alaska, to your notion that "mining on the West Coast doesn't benefit all New Zealanders"?

Royalties for oil and minerals get paid DIRECTLY to citizens. What's "not beneficial" about that?

Nobody who advocates Rail instead of cars and roads, has ever come back to explain to me what is wrong with Alain Bertaud's landmark study of urban form in the former USSR, "The Costs of Utopia". Omnipotent planners told everybody where to live - in apartment blocks - and how to travel - by train. Was it more efficient than a typical free market city? HAH. Did the USSR "bury the West" economically and productively, as Lenin promised? The answer to both questions, is the same.

Read the study; and if you can come back to me and tell me why it is wrong, you will be the first.

Mining, fine, but not if we sell of our one time family jewels as Australia is doing with just the gangue (rock) removed. If we are mining, for instance, iron sands, we should combine this with our top grade coking coal and sell off, at the very least, ingots of top quality steel. Better still we sell machine tools and maybe even the machines themselves. No one thought we could compete with Holywood. Well we did. Lets not sell ourselves short.

Mining, fine, but not if we sell of our one time family jewels as Australia is doing with just the gangue (rock) removed. If we are mining, for instance, iron sands, we should combine this with our top grade coking coal and sell off, at the very least, ingots of top quality steel. Better still we sell machine tools and maybe even the machines themselves. No one thought we could compete with Holywood. Well we did. Lets not sell ourselves short.

Absolutely William, mind you we've been saying this for years with things like logs. Close down the saw mills, P&P plants, put the workers on the dole and export the raw logs. Brilliant!

That's globalisation for you. Otherwise known as slitting your own throat.

Yep, and what might we have done to keep the saw mills and pulp and paper factories going? We weren't prepared for what was required to do that.

NZ - a leading example of economic Darwinism.

Thinking that an economy can live on credit, not resources, is THE big lie common to both Wall Street AND most politicians and the people who vote them in.

Cue Powerdownkiwi here: "but the resources have run out..." yeah, that's why we're all arguing about leaving them in the ground, because they've run out.

I think that this article misses the issue of addressing the systemic issues of the current banking system. I was going to explain with an example but it got to long winded so if I can highlight that in the current system.

Bank shareholders are owners who invest in a bank to make money. The bank they invest in employs people who are qualified to make the commercial decision as to which people and businesses it lends out it's money out to.

Depositors in a bank are not owners of the bank, they are putting money in the bank generally as a safe store of value.

The New Zealand public or taxpayers do not own the bank or receive benefit other than through taxes to the business.

So if a bank makes bad loans and becomes insolvent - all be it from no fault of any one person, should the loss be paid for by the bank owners, the depositors or the taxpayers.

I put it to your readers Bernard that the only problem with todays banking system and debt is that it is expected by the bank owners that they are able to socialize any major loss to the tax payers (as seen in Ireland).

This expectation gives bankers the license to do al-sorts of irresponsible lending to maximize return in good times with-out the need to worry about the risks to their shareholders.

In the mean time the public has to live with the consequences of the bankers decisions, decisions which effect us all..

As many commentators have said, the solution is for us, as individuals, to save more money. The saved money replaces funds borrowed from overseas. KiwiSaver should be that mechanism but isn't because it is a terrible investment. The only reason it is worthwhile for the individual Kiwi is because of the government hand outs associated with it. In case you haven't noticed, this is our own tax money which is being given back to us. Today on the news (Dec 15/10) it was announced that KiwiSaver expenses are one of the reason the government has to borrow so much money overseas. Stop all the subsidies, including the employer contribution, which is a cruel fiction and make KiwiSaver worthwhile and much of the problem will disappear.

http://mtkass.blogspot.com/2007/07/kiwisaver-good-for-new-zealand.html

William

Nice try William...but ending the gravy train would deprive pollies of an easy route to the pig trough!

Both main parties are passed experts at running this path...the minor parties learn by example and catch up fast....point to one who refuses to join in!

The only solution is in the hands of Mr Market and the ratings agencies. The sooner they swing the axe the better for the rest of us who saved and didn't splurge with credit.

interestingly NZ has opted for a consolidation of the financial services sector - ie wipe out the finance sector, and credit unions (who are losing market share) , such that we have really only four major players now. Australia on the other hand are reforming and want competition. They are looking at removing barriers of entry, watering down the market dominance held by the encumbants. Once again Australia have it right.

Excellent Articule Bh

"What would happen if the world judged New Zealand Inc was unable to service its debts?"

Is this the lead up to part 2?

Its fine writting up an articule like that, for those who know what a bond is and havew at least a basic understanding....What is really missing is an articule "What would happen if the world judged New Zealand Inc was unable to service its debts?"

Something that Joe Public, the checkout operator, the labourer, Pensioner waiting for a op, the Solo parent can relate to....personally effect.

Commentors are good at explaining x number of people get benifits, Y % year Z % of the wages....but fail miserbly explaining to the majority of Joe Public who do earn, recieve benfits, super etc and are not part of the top 10% of the national wage package.

If someone else dictated action, it would look a lot like what happened in Ireland. A slashing of government payrolls and salaries. Lower benefits and pensions. Lower investment in infrastructure. Asset sales. The usual IMF prescription.

cheers

Bernard

I know that, you know that, but tell the NZ joe public that and its .."never been there, dont they throw bimbs at each othe or something"

Im talking taking real examples out of the NZ population..what it WILL mean to THEM on a rewal personal level.

If we want/ need Kiwis to cut back, save what ever, we NEED to tell them, "that bypass you have been waiting for...sorry all by passes are off the table."...and its not just going to be the by pass, it will be many other things we take for granted.

"A slashing of government payrolls and salaries. Lower benefits and pensions. Lower investment in infrastructure. Asset sales. The usual IMF prescription"

Got any road works in the street? go out say hi to the crew working say that to them and ask if they have any concept in real terms as to what you are talking about...And that is what people in NZ bee to have explained.. "

An 'old' one by Brian Easton (seems like six months ago!)

"The cautious but proud independence which has characterised New Zealand’s international and political relations in the last fifty odd patronless years will continue. There is not a half-baked alternative to this. In my view the only alternative is to become a state of the Federation of Australian States. My fear is that if we adopt the inept economic policies which advocates of monetary union and the 2025 Taskforce policies propose, we may end up begging for Australian state status. We can do better than that."

Good article Bernard, thanks.

Bernard - to repeat the praise of others, good article.

Indeed:

"New Zealand's foreign debt problem is a household debt problem, rather than a government debt problem, like it was in Greece and Ireland. Actually, our foreign debt problem is a corporate or bank debt problem because the debt is owed via households through the big four Australian-owned banks. "

Indeed:

"We also need to use any prudential tools we have to stop the Australian banks borrowing more offshore. Are massive new issues of covered bonds a good idea? Particularly when they are being used to increase investment in property, rather than repaying short term borrowing."

However, when you say "We also need to use any prudential tools ...," I'd rather that were stated "RBNZ should be required to use any prudential tools .....," and a particular ratio that doesn't get enough exposure in debate is probably the simplest and easiest to intuitively understand, the 'Loan to Value Ratio' (LVR).

Bother lenders and borrowers would benefit from specified and varied LVRs per asset class and purchase type - would they not?

Cheers, Les.

Seeing as we spend something like $25B dollars a year on private motor cars (roads, maintenance, car cost, accident costs, congestion costs, health costs) and have one of highest amounts of road per capita in the world it might be a good idea to reduce our dependence on cars. We only spend half that on health or education.

Of course this would require increasing the density of our cities - not adding to suburban sprawlavitch - which would require changing RMA focus away from protecting what exists to protecting the environment.

Imagine 20% less cars = $5B dollars extra a year in the pockets of government and people, just like that.

Urban limits to increase density have already driven up property prices to the point that the first home buyer is "outta here". And "bubble debt" has been estimated at around $30 billion already. That is for NOTHING. It could have bought a LOT of Toyota Priuses.

Furthermore, because land prices get driven up all over the metro area, guess what happens to households making location choices? Suddenly, the cost of the home is 80% to 95% of the equation where you trade off location and travel expenses, instead of 40% to 50%. THAT is why you now see all that dense development 30 kms from the CBD, while only a few super rich people can now afford to live NEAR the CBD, in increasingly pleasant walkable neighbourhoods. The urban planners all pat themselves on the back and say that multi-million dollar Condo prices are "proof" of "demand" for "sustainable" urban form. Meanwhile, tens of thousands of Joe and Jane couples are paying prices for homes 30 km away, that WOULD have bought them homes 10 km away BEFORE the conceited urban planners monkeyed with the curve.

I'm with Berend deBoer and the other rational people who see what an honest and courageous article this is.

As for the socialists and the resource alarmists, DUH. I think these people are typical of what the politics of envy does to people's minds; I suspect they really want the whole world to resemble the USSR circa 1930, rather than daily be frustrated by the presence of successful and well off people all round them.

NZ's resources could support 50 million people for centuries. If NZ WAS part of the Communist bloc, it probably WOULD have this many ChiComs here. And we would find out what "strip mining" REALLY was.

I just read "The Rational Optimist" by Matt Ridley. He ends his book by saying that the one thing he is pessimistic about, is the scope there is today for a BAD idea to sweep the whole world rather than just one nation. I think that bad idea is what his book is about - environmentalism and conservation and "peak oil" and global warming and all that stuff that is based on lies anyway. Matt Ridley reckons he remains optimistic about the power of the human spirit somewhere to survive and keep on innovating and exchanging ideas and creating wealth, in spite of bad politics.

I reckon he is wrong, in so far as it would be tragically possible today to "globalise" a Green version of Bolshevism and eventually turn the whole world into North Korea. The new Dark Ages would make the medieval Catholic Church look progressive. But if only Ridley's common-sense, rational book got distributed and read enough......IF ONLY schoolteachers did that instead of showing Al Gore Doom movies.Philbest... you make the mistake of characterising resource depletion as a socialist left - right issue.

If this is so The International Energy Agency, Lloyds of London, the US and German military, the UK Energy secretary, Sir Richard Branson and a UK Energy business task force (to name a few) are all socialists....

as they all say that global oil production has, or is to shortly peak, and warn of a supply shock with very high prices and shortages by 2012- 2015

links to reports from these bodies and many other credible sources here

the crucial political question is how will government mitigate these shocks. Neither major party is willing to acknowledge the problem let alone produce policies

Larry Williams ( Newstalk ZB ) putting it to Bill English that National are carrying on Labour's bloated government budget , that Labour increased the government spend by 50 % , we're so deeply in debt ................. Well , Bill says , if we have a mandate after the next election we'll look at it all . .......

......... the clock on NZ Inc's debt time bomb is ticking ..........

Exactly when you cut your revenue but don't or can't cut your spending, how is that any better than the government before, that increased spending when the money was there to do it?

Just wondering how long it will be before they will be forced to back down and increase taxes again.

Personally I don’t think it is anything to do with whose doing what or isn’t do what to whom. Whatever you do in life there has to be controls whether that be self or external discipline. To say that the market knows best, that we need small government and not big government and to somehow not recognise that there is something in between is, I believe, really a bit silly. No country will ever survive unless it has the right economic policy that provides for all its people. Until we have a government that recognises this we will go further and further down hill. There has to be controls, and, I believe, those controls have to be financial and which protect New Zealand and New Zealanders. A Government has to govern and at times it has to put the brakes on and at times it can let the economy expand. To let the Reserve Bank do that by virtue of the OCR beggers believe. The ridiculous free market global system we have had for the last 30 years just does not work. The people in New Zealand do matter and any Government has to have policies that provide for all its people. To say that the poor somehow bring it on themselves is just so 19th Century. To compare ourselves to other countries all the time is so stupid. We have a wonderful country that did and can still work.

Most comments here including Bernhard’s describe the state of the disease, but not what is actually triggering the disease. The real question is and I say that again:

How can a nation, which provides an excellent education system investing Billions for young people lose such a high number of potential members ready for the workforce to overseas countries ?

Please, read and understand this article in context to my many others.

Please read and understand , once and for all , in context , it is spelt " Bernard " , not " Bernhard . "

No ... " H " ......... !

We invest billions into the edhucation shystem , and sthill shome cannut sphell .

Gheeeez , Wahlter , you're a shocker , old buddy . ............hha hha de hha !!!!!

If Walter wants to give Bernhard and aitch it's not a problem Bummy Gear...so how much snow are you expecting where you are next weekend...just ice in the drinks I spose. Hey that would make a great fashion label...have it for xmas.

ICHTHYOPHTHALMITE - more "H" Roger. I can't spell begause I did not have NZeducation.

Sorry - Bernard - one of my best Swisskiwi- friend is Bernhard - all - 95% G- Swiss are Bernhard.

Seriously Walter , 95 % of G-Swiss are called Bernard ! Including the frauleins ? Martina Hingis was lucky .

Hha hha !

Recipe for progress.....is there one......yes, but first we need a govt that has the guts to lead and not play games dressing up in Helen Clarks skirts.......

so much for 3.5% growth, and significantly dropping unemployment in 2011

with govt stimulus drying up, and private sector investment dead....

blah blah blah

Come on Matt....you never believed that crap............the only real growth that will take place is in the size of the debt mountain and it will be a bloody sight more than 3.5%. 6 more months to the budget....six......a world falling apart....an economy going down the dunny and that lot intend taking 6 months to make their minds up.....thank goodness it's not a crisis.

From a reader via email.

Bernard,

A very nice piece re NZ and our headline figure vulnerability, particularly when in black and white our numbers are very PIIGS'esque.

It dovetailed very well with Gaynor's recent piece wherein he compared NZ to Iceland.

My only point is that I think everyone is over estimating the position that Australia is in. Its property market remains the most inflated in the world, on nigh any multiple or basis. Therefore by definition, the loan books of the Australian banks remain fragile. I think the trigger point will come from Australia down, as opposed to NZ up (and the question as to whether the OZ banks will rescue NZ, which then of course would be rendered redundant).

I appreciate that everyone says, "yes, but Australia has commodities". However if you break that down, and what it means, it doesn't mean that a country can ignore an over valued asset base (read bubble). Sure, it means that profits are trickled throughout Australia by virtue of employment and of course the tax take etc. (from the commodities companies), however in no way is that enough to underpin a country's whole property market. For example Spain has some similarly globally competitive, and profitable companies e.g. Repsol and Telefonica to name but two.

Many companies have successfully leveraged their Iberian roots to expand into Latin and South America, e.g. Santander, Telefonica. Yet I note that none of this is used to explain why Spain shouldn't be attacked because of the fundamental problem of a country with an inflated property market (and therein Bank loan books and the possibility of the Country rescuing the Banking system, causing more fiscal deficits, an untenable Sovereign debt position etc.). Yet the commodities rationale is always trotted out for Australia. I think it bears further investigation re its veracity.

Therefore when NZ is examined in isolation, of course I am concerned. However I think the trigger will come from an attack on Australia (where if nothing else there is more liquidity re instruments for the Hedge Funds to exit their positions or give away ridiculous bid - offer spreads).

Rgds,

Damon

Damon, I have some counterpoints I see.

Australia would be a trigger for NZ certainly so what is the trigger for Australia?

China and or the property market?

So what s the trigger for China, well I dont see any high risk there they have direct control over there economy and people yet all the market mechnisims if the choose. Their consumption requirements are enourmous so commodities volumes are safe, prices well thats different but a good average price.

The Property market is tight in Sydney thats the reason for prices the way they are. There is that much demand and no change in the supply demand balance really to come. Immigration is still a 180,000 a year. Its a popular destination to purchase a home or investment property for Chinese and Asians of chinese heritage and indians. They are cashed up a lot of them.

I

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.