By David Hargreaves

It is time to call a spade a spade, or in fact, an Auckland housing problem an Auckland housing problem.

New Zealand doesn't have a housing problem. Auckland does. So, why should the entire NZ housing market be treated for a condition that only exists in Auckland?

You don't generally try to fix a cut on your finger by wrapping your entire body in bandages. No, you treat the directly affected area.

Auckland has a perceived problem of a shortage of housing. So, fair enough, this problem is being directly targeted. The Government and the Auckland Council are working hard at resolving the supply shortage through such initiatives as the Auckland Housing Accord.

But it is not all about supply - much as some would like to simplistically say it is.

We know that advice the Government has received from the Ministry of Business, Innovation & Employment suggests even with the current housing supply initiatives "...demand is forecast to exceed supply in Auckland for at least the next decade", according to officials.

So, the immediate problem that needs tackling is demand, yes, that's right, DEMAND - till the supply can catch up.

But that's where I reckon the trouble is. While the supply problem is being tackled on an Auckland-basis, the demand issue is being tacked through nationally-focused initiatives, such as the Reserve Bank's 'speed limits' on high loan to value ratio lending introduced in 2013 and with more measures likely on the horizon.

The applied logic seems to be that if you constrain demand for housing in the whole country then this will have an impact on Auckland. And presumably it will...eventually. But it is a sledge-hammer to crack a walnut, isn't it? The blunt instrument approach. Auckland may eventually be tamed. But what happens across the rest of the country - where you are squeezing a demand problem that doesn't exist? Unintended consequences, and all that.

It would actually just be plain unfair if people in regional NZ, or you can broaden that and say non-Auckland NZ, saw house values (which are in general much lower than Auckland's anyway) pushed down because of nationally-focused initiatives that are really trying to fix an Auckland problem and are hammering the rest of the country in a kind of incidental way.

There have been public calls for the Auckland housing demand problem to be tackled in an Auckland-specific way. There were certainly calls for regional targeting at the time the RBNZ introduced the LVRs measure - which is of course nationwide..

At that time the RBNZ said the use of targeted restrictions was not being contemplated. "Geographic targeting would be administratively complex, and would require difficult decisions to be made defining ‘problem’ areas," it said.

The RBNZ has subsequently maintained its opposition to geographic targeting and is planning to nationally focus its intended recategorising of property investors, a move that might well lead sooner rather than later to specific macro-prudential measures being brought against those investors.

I've already said I think the net has been spread too far with these property investor proposals, given that they will affect people with as few as two properties.

But until now I've been prepared to hold fire on the whole question of Auckland-specific targeting because I genuinely believed that the rising house market trend would start to spread outside of Auckland. If that were to be the case then targeting one market in the country would not make much sense.

However, two specific things I've heard in the past week have helped to change my mind. These two things suggest to me that the problem is all about Auckland and it will remain all about Auckland.

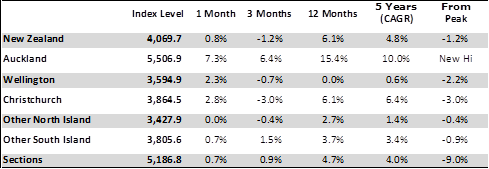

First piece of relevant information helping me to make my mind up was the latest Real Estate Institute figures for the month of February. These showed house prices in Auckland up strongly, but elsewhere generally flat.

The best guide to what is happening within the REINZ figures is provided by the institute's "stratified housing price index", which adjusts for some of the variations in the mix that can affect the median price and produces an overall measure of house price inflation.

As can be seen from the table below, prices in New Zealand have actually fallen in the past three months - but risen 6.4% in Auckland. In the past year the Auckland prices have shot up 15.4% versus just 6.1% for the country as a whole - and remember the New Zealand figure does include the Auckland impact as well and is therefore inflated by that.

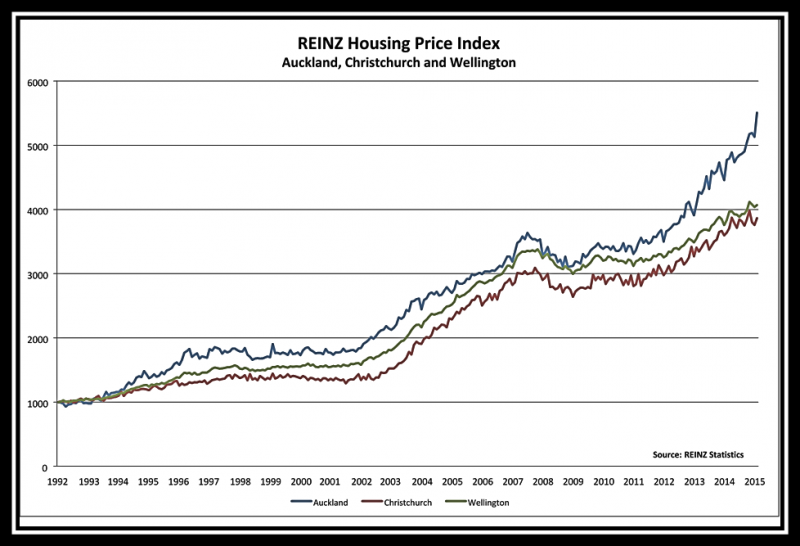

So, really we can see that Auckland is roaring along and the rest of the country merely simmering at best. The growing gulf between Auckland and the rest is well depicted by the graph below, also from REINZ, which shows the increasing disparity between Auckland, Christchurch and Wellington.

The RBNZ, concerned about financial stability problems that could be caused by any boom and bust cycle, has said it wanted to wait to see how the February-March housing sales statistics panned out before deciding definitively on more specific action on the housing market.

The latest REINZ figures therefore surely demonstrate that there is an overheating housing market problem. But they just as equally assert that the problem is purely with Auckland. The spread into the regions of house price rises in the manner we saw in the early-to-mid-2000s is so far tellingly absent.

The other piece of information that clicked into place for me last week came out of the mouth of RBNZ Governor Graeme Wheeler.

In response to media questions about the level of new buying by housing investors - which cited the information released by the RBNZ showing this running at around 30% - Wheeler came out with figures suggesting that the level of buying by investors is in fact running higher than these figures suggest - at about 40% in Auckland and 35% in the rest of the country.

Curious

We at interest.co.nz were a bit curious about this and asked the RBNZ for some clarification. We were told that Wheeler had been "quoting data about the share of investors in house purchases, which shows that investor purchases currently make up around 35% of residential sales by number, with Auckland currently sitting at 40% by number.

"The data is calculated from sales data that we source from CoreLogic, using algorithms and micro-level sales data to identify multiple property owners and then using that as a proxy for 'investors'. Because the result depends on the algorithm being used to create a proxy for investors, this data is indicative only and we caution against spurious accuracy."

So, that's not all particularly clear. But what it does tell you is that the RBNZ thinks property investors are proportionately buying more houses in Auckland than they are the rest of the country.

Yes, that's right, despite the fact that the Auckland prices are soaring, investors are more attracted to that market than elsewhere. And you can only presume this is because, well, the investors pick that Auckland prices will continue to soar relative to the rest of the country.

Now, of course investors want the best rates of return available, which is why they see Auckland as the best place to be at the moment. To take heat out of the Auckland housing demand equation then, presumably the desired course of action is to make Auckland comparatively less attractive for investors.

But is that what nationwide penalties/restrictions placed on property investors would actually do?

Isn't it actually possible that any macro-prudential measures that are targeted across the whole country - therefore carrying some cost on investment anywhere - might actually encourage investors to target their spending even more in Auckland. They might they look for higher returns to offset the potential penalties applied for them just being investors, anywhere. "Okay, if it will cost me more money to be an investor, I'll invest in Auckland where the returns are higher."

Isn't that outcome at least possible? Couldn't a nationwide clamp on property investment actually drive more investors into the Auckland market?

Dampen Auckland investment

So, regardless of whether the RBNZ and/or Government think it would be administratively tough to implement directly-targeted measures that would dampen property investment in Auckland (and I stress I'm talking about homes bought for investment as opposed to ones being bought to live in), I think it really must be considered.

And one obvious way to do it would be by making the banks hold more capital against mortgages advanced on Auckland investment properties (though I would still have a higher threshold than those with just two properties - I would still favour the original four or five threshold).

Making the banks hold more capital against some Auckland investment mortgages would have the likely impact of driving up the cost of those mortgages - and it might make the banks more reluctant to lend to Auckland property investors. The result theoretically should be some dampening of demand.

Now, the banks would say it would be far too difficult to organise Auckland targeting in such a manner. The property investors would say it would be too difficult. Sometimes you just have to bite the bullet.

It wouldn't be as easy as a blanket serious of measures thrown across the whole country. But I think it could work, while a countrywide measure, I think, could have bad unintended consequences for places not called Auckland.

And if Auckland were to be specifically targeted, just maybe this would then encourage some property investors to invest more in other centres, which I think would be a very virtuous outcome. You could target Auckland - help Auckland - and help the country as a whole.

Of course any measure targeting investors through the banks won't tackle the situation around cashed-up investors who don't need to borrow. We still need to see more useful information about how many of these investors there really are out there. Anecdotally it is a significant issue, but we need more than anecdotes. Once there is more information, perhaps there are measures that could be levelled in that direction too.

It's fair

What I'm suggesting might seem inherently unfair, which is why it would surely meet with strong opposition. But I think the Auckland housing demand problem right at this moment needs to be tackled at source (IE not indirectly through the rest of the country) by measures that will directly take the steam out of the housing-for-investment market in our largest city.

Auckland investors might see it as unfair. But I don't think young Auckland people who want to buy a house to live in but can't get one because they keep getting outbid by investors would see it as unfair.

And who knows, ultimately some investors might be saved from themselves. When somebody as experienced in the Auckland scene as mortgage broker John Bolton starts describing a market where "prices are heading well above fundamentals and increasingly it’s a speculative play" then you know we are getting into the very sort of risky environment that the RBNZ is so keen to avoid.

18 Comments

Make banks value property at 3 year moving average value.

So buying an over priced auckland property at 800k for example, banks take 3 year average value to be say 700k, and so happy to lend 80% of 700 = 560k. Effectively a 30% deposit required to buy this sort of property that has had recent price rises.

In non-price rising areas, the 800k property today, has a 3 year average value of, 800k still, so banks happy to lend 640k on properties of this sort.

So targeting only properties that have had recent price rises. And leading to increased financial stability as recent bubble prices are not taken as the sole means of property valuation.

The problem with this is that it will stabilise prices around the current level. I.e if prices fall then you can borrow more to bid them back up. Current house prices are in a massive bubble and persisting this price will cripple the country in the long-term.

Yeah forgot about instances of falling prices.. Take the lower of current value or 3 year moving average value.

We also have a massive debt problem, debt that cannot be paid back from the countries earnings.

Remove the tax deduction against personal income. This would then favour properties that are not cashflow positive which is anything purchased in Auckland in the last few years without sigificant equity. The rest of the country has much better yields so won't be affected as much. This also catches people who stretch their equity too thin to leverage up to buy more investments.

Keep tax deductions for property investment companies as they will have to pay capital gains on disposal (they are companies set up to invest in properties therefore must be investors and liable for capital gains).

Where does "Auckland" start and finish?

Does it include Manukau, Rodney, Waitakere, Norh Shore, Papkura, & Franklin?

Which street is the last street where Auckland ends and the rest begin?

You're right these are some details to iron out and would create some strange activity on the boarders of Auckland. But this should never be used as an excuse not to go down the Auckland targeted restrictions road. Boy if it ever was wouldn't that be a case of the smallest of minority ( IE the few houses that exist on the boarders of Auckland ) dictating to the overwhelming majority, IE the rest of New Zealand.

Main employment areas bigdaddy, thats specific enough, even for smart blogger like yourself :)

I think the uncertainty of Wheeler's suggestion of new measures is a problem. Unless there is some sort of shock to the financial system we assume house prices in Auckland will continue to rise for the next couple of years. Property price inflation around the rest of the country is less certain. If new measures are implemented and this flattens Auckland house prices we can handle this. Heck, we all know it will come at some stage! If new measures are introduced and this has a negative impact on property prices / investment in the regions this is highly undesirable. So, the effect for the time being is keep investing in Auckland.

Give us some certainty and we can invest outside of Auckland. I think a lot of investors would like to do this right now but are holding out to see what exactly is implemented by the RB.

Given the Chinese buyers story in yesterdays top10, why not find and reasonable measure of foreign house buyers. I still find little wrong with the Auctralian 'new homes only' approach.

40% bought by investors - how many investors in this country?

Thats right David, in this circumstance - Auckland.

Thier needs to be fair policy implimented around a property to invest in and property to live in.

A house to live in is closer to basic human need and better reflects our egaliterian socioties principles.

People / families need the option to own an affordable (being ratio to income), reasonable home (not a shoe box apartment) and not be forced into being a life time tennant; almost reverting back to historic Aristocratic class, inslaving people from not so fortunate/wealthy up bringing to pay for the investors and future genreations privledged lifestyles.

These home buyers are people who provide services to our communites (teachers, retail, hospitaltiy, consultants etc.) are simply looking for a home close to work, their up against wealthy professional property investors with sophisticated strategies (some not even living in NZ!)

Handicapping first home buyers with LVR is unfair, unballanced and creates an advantage to the investors, in turn those who have more than enough need to have their greed curbed/targeted and investments re-directed in a positive way for all, through strategies mentioned.

That being said we still need rentals, so there has to be a balance in order for our economy to grow in the right way.

Cheers

Scoring points here for admitting the bleedin' obvious. Those who hide behind skewed or deliberately deficient data and claim to see no problem have ridden this horse to its knees.

Points: Chinese money is not borrowed here so lending curbs will be useless, but you cannot separate this from any other nationality bringing in funds.

Owning more than the one property where you reside is investment.

Much of the auckland market is just churn, musical chairs for the narrow minded jafa's, who will get stuck at the top of the pypramid?, who cares?, no-one outside Auckland does.

People outside Auckland should care.. when the Auckland ponzi scheme finally falls over, the repercussions will be national, 25% of the countries' population is in Auckland, none of the political parties will ignore that many voters and let them suffer what is coming to them, the politicians will be bailing them out with your money. Or if it gets bad enough, the banks will be skimming a bit off the top of your accounts with the OBR.

Limit interest only lending. If a buyers cashflow or equity position is insufficient to repay over and 30 year term it is over leveraged. Would immedntiley limit the most risky investor behaviour

If house price inflation in Auckland was due to a genuine shortage of houses, why then have house prices in every OECD country risen by a smmilar amount? It is too much of a coincidence that suddenly there is a shortage in all these cities.

House prices have risen because other countries (notably America) have flooded the world with cheap money which has gone into assets and not productive investments.

When prices rise, every man and his dog want a bit of the action and buy rental properties, thus exacerbating the situation and pushing prices even higher. It is similar to a pyramid game. Eventually the market will correct, hurting many people.

The Government is negligent in not addressing the demand side of the equation.They are leaving the Reserve Bank to make the unpopular decisions.

If investment properties were not so attractive, tax wise, then house prices would at least stabilise to some extent. I went to a property seminal a few weeks ago out of curiosity.The main theme over and over again was"let the taxman pay for your rental house".

The main reason National do not want to control house price inflation is solely because there are now so many National backers who own multilple rental houses.

it is international buyers with cheap international $$ (Euro, yen, US) going into a perceived 'high yielding' currency country, with fundamentals that make currency appreciation (NZD) more likely than currency depreciation. They buy Auckland as its the biggest safest way to do this. If they had more local knowledge of fundamentals in other areas besides Auckland then they'd be just as happy pumping there $ into these markets too.... Problem is they have too much $$ for many of these smaller markets, so just as Buffett can't buy under valued small caps (as he'd have to find a million small cap companies each year to make it work without buying the company out altogther), foreigners pump it into auckland. As a NZ'er with local knowledge theres no excuse to be so lazy. Prehaps if you think NZ and the NZD is still cheap at present against the major currencies (USD, yen) then by all means, the current state of affairs may continue. I think we are definately at or close to a turning point though.

Who wants to live in inner Auckland anyway. Its an overpriced dump. We just moved out of the central city to Rodney. Back to Kiwi living. So good. We could even afford to buy a place with a full 1/4 acre. Heaven.

I don't have a problem with house prices in the rest of the country being flat. Why is that a bad thing? Why would you want to increase the cost of housing in the rest of the country? A 20% is pretty sensible, the bad old days of 5% are pretty risky, and good riddance to them.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.