By Christian Hawkesby*

Over the weekend, central bankers from around the world met at Jackson Hole in Wyoming to discuss unconventional monetary policy and lessons for the future. Closer to home, the RBNZ has itself moved closer to unchartered territory, cutting the OCR to an all-time low of 2.00% in August, projecting further reductions, and publishing two scenarios that would push the OCR to around 1.00%.

It is not our central view that the RBNZ will be forced to follow the same path taken overseas. Indeed, the Governor set out in his speech last week that the RBNZ would prefer not to have to cut interest rates aggressively. However, with the OCR already at all-time lows, as part of considering a range of plausible outcomes, it seems timely to consider what unconventional monetary policy might look like in New Zealand.

The main unconventional tools employed overseas have been:

- Negative interest rates

- Quantitative easing

This paper addresses these tools and other new horizons.

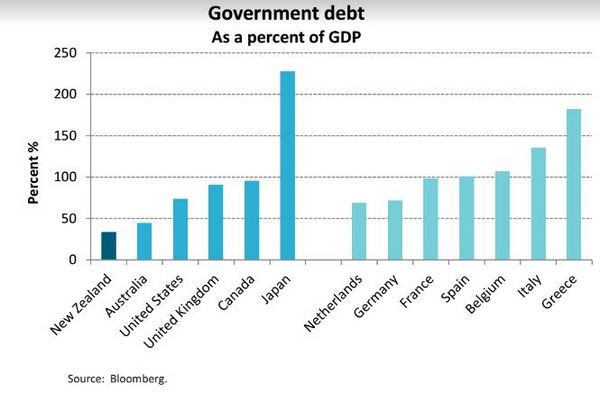

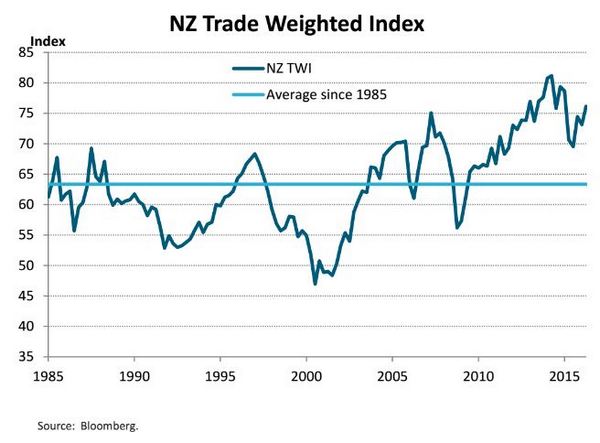

A key conclusion is that, relative to other countries, New Zealand has the benefit of greater room to manoeuvre. In particular, by starting with an elevated exchange rate, there is more scope for an easing in policy to come through a depreciation in the NZ dollar. Similarly, by starting with a low level of Government debt to GDP, there is more ability for supportive fiscal policy to be deployed hand-in-hand with supportive monetary policy.

Interest rates

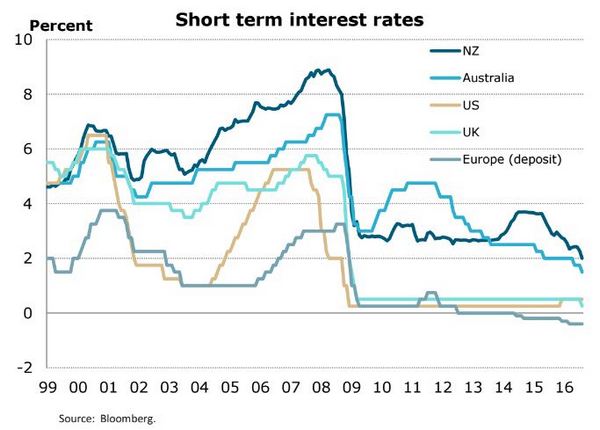

The RBNZ has not yet officially ruled out cutting the OCR below 0%, to negative levels.

Back in 2009 when the GFC was at its height, the US Federal Reserve and Bank of England initially cut and paused policy rates at 0.25% and 0.50% respectively. At the time, it was thought that cutting interest rates any further would potentially cause more harm than good. In particular, it could have the unintended consequence of hurting the profitability of banks and building societies, unable to pass on negative interest rates to depositors.

That conventional wisdom was challenged in 2014, when official interest rates in Europe and then Japan were cut to negative levels. This initially came as a surprise to markets.

However, it reflects that these regions have faced acute deflationary pressures and the lowest potential growth rates. That said, there is a physical limit to how low interest rates can be cut. At some point depositors become incentivised to remove their cash from the banking system when the cost of storage, security and insurance is less than the negative interest rates charged by banks on deposits.

More recently, there has been increasing focus on the adverse consequences of negative interest rates, including on the harm to savers, as well as the perverse incentives and distortions it can create within the financial system.

In response to the surprise Brexit referendum result, the Bank of England cut overnight interest rates from 0.50% to 0.25%, but has signalled that it is likely to finish cutting interest rates just short of 0%, which the market has taken to be around 0.10%.

Quantitative easing

Much like the question of where to stop cutting interest rates, the assets purchased in Quantitative Easing (QE) schemes have also differed for each central bank. While they shared the same objective of increasing the monetary base and bringing down longer-term interest rates, the application of QE has often depended on many local considerations.

- US Fed: The US Federal Reserve initially began QE in November 2008, buying mortgage-backed-securities (MBS). This reflected that these assets were a large, liquid part of the US financial system. It also provided official support to a market that had been under pressure from the US housing market crash. In later phases of QE – QE1, QE2, and QE3 – the US Fed added US Treasuries to be a major component alongside MBS purchases.

- BoE: The Bank of England (BoE) initially began QE in March 2009. Despite being provided scope to buy corporate assets (corporate bonds, loans, asset-backed securities), the vast majority of assets purchased by the BoE were UK government bonds. This reflected a preference for the central bank not to take credit risk, and instead focus squarely on lowering long-term interest rates and “crowding in” other investors into the corporate bond and the equity market.

- ECB: The European Central Bank (ECB) initially began QE in May 2009 by purchasing covered bonds, a form of debt issued by banks and securitised (or “covered”) by pools of mortgage assets. Much like the motivation in the United States, the covered bond market in Europe represented a large, liquid part of the European market for the ECB to easily access.

In addition, the ECB was initially keen to avoid purchasing government bonds as part of a QE programme, to avoid even the impression that the ECB was financing national governments. In January 2015, in response to growing deflationary pressures, the ECB changed tack and announced a new expanded asset purchase program, including the debt of national governments, agencies and European institutions.

New horizons: Helicopter money

As the ECB, BoE, and BoJ (Bank of Japan) have scaled up their QE programmes through 2015 and 2016, commentators have increasingly asked what more can be done by policymakers, moving beyond the unconventional tools used so far.

While QE involves expanding the money supply through the banking system, the next step would be expanding the money supply direct to households.

The phrase “Helicopter Money” was coined by Nobel Prize-winning economist Milton Friedman in 1969, and was popularised more recently by Ben Bernanke (“Helicopter Ben”) in his 2002 speech on preventing the threat of deflation.

In these days of electronic banking, what this amounts to is getting money directly into the bank accounts of households, and encouraging them to spend their windfall. In practice, the easiest and most practical way for governments to do this is through a tax cut that is financed by the central bank – so-called “Monetary Financing”.

While Quantitative Easing involves the central bank buying government bonds off another investor in the secondary market, Monetary Financing involves the central bank buying directly from the government in the primary market. As a result, both the money supply and the government deficit increases hand in hand.

Importantly, this form of Helicopter Money requires a new co-ordination between monetary and fiscal policy. This requires a real change of thinking from policymakers. In the immediate aftermath of the GFC from 2009 to 2012, ‘fiscal austerity’ was a key catchphrase in the US and Europe, encouraging tighter, not looser, fiscal policy.

In more recent years, the conversation has moved on, with many commentators calling for more active, stimulatory fiscal policies to take the load off overburdened central bankers. That said, many countries, especially in Europe, are already constrained by high government debt, limiting the room for manoeuvre. Over the weekend in Jackson Hole, Janet Yellen once again reiterated that “as always, it would be important to ensure that any fiscal policy changes did not compromise long-run fiscal sustainability”.

What does this all mean for New Zealand?

It is not our central view that the RBNZ will need to apply unconventional monetary policy. However, with the OCR already at all-time lows, it seems timely to consider this tail risk as part of considering a range of plausible outcomes.

In this scenario, we suspect that the RBNZ would stop cutting the OCR somewhere between 0.25% and 0.10%, judging that negative interest rates are potentially more troublesome than they are worth.

If the RBNZ were to undertake a QE program, New Zealand Government bonds would be the obvious assets to purchase. With $75bn bonds outstanding, there is no other NZ dollar market with the same scale, liquidity, or credit quality. This is the simplest approach.

If the RBNZ were having to loosen monetary policy aggressively in response to sharp deterioration in the housing market, it is also likely that mortgage-backed-securities (MBS) would play a role in an asset purchase program. While the MBS market is not currently a large, liquid part of the local financial market, banks would be in a position to quickly structure these securities specifically to sell to the RBNZ. In effect, the banks would be liquidising their balance sheets, exchanging mortgage assets for reserve balances at the RBNZ.

There may also be a practical reason for the RBNZ buying MBS as part of a QE program. The RBNZ would need to be careful that their NZ Government bond purchases weren’t so large that they removed so many bonds that it harmed secondary market liquidity. In that case, the sheer scale of banks’ mortgage assets could become an alternative source of assets to purchase as part of a QE program. (By way of comparison, household debt to GDP is around 160% of GDP, compared to Government debt to GDP of around 30%).

As a small open economy, the RBNZ has an additional tool in its armoury: the NZ dollar exchange rate. If the RBNZ were to ease policy more aggressively than its trading partners (through a lower OCR and/or QE programme), there is plenty of scope for the NZ dollar to fall from its current elevated level. In practice, this could be where the economy receives the most stimulus and immediate impulse to lift inflationary pressures.

An asset purchase program from the RBNZ could be even more potent if accompanied by an expansion in government spending, with monetary and fiscal policy working in tandem. With one of the lowest levels of Government debt to GDP in the developed world, New Zealand has the luxury of having real room to manoeuvre with fiscal policy. Implementing this approach would require a significant change in mind-set or circumstances. At the moment, the NZ Government is still focused on reducing (not increasing) Government debt to GDP.

However, the government has shown flexibility in the past in times of crisis, like the Canterbury earthquakes, to let the fiscal stabilisers (higher benefit payments and lower tax income) kick in to support the economy.

In other words, while the New Zealand Government appears hesitant to pre-emptively loosen the fiscal purse strings, if a recession causes the RBNZ to embark on unconventional monetary policy, it is likely that those same circumstances would also result in more supportive fiscal policy.

--------------------------

*Christian Hawkesby, is executive director and head of fixed interest at Harbour Asset Management.

25 Comments

In this scenario, we suspect that the RBNZ would stop cutting the OCR somewhere between 0.25% and 0.10%, judging that negative interest rates are potentially more troublesome than they are worth.

Fed Vice Chairman:

FISCHER: Well, clearly there are different responses to negative rates. If you’re a saver, they’re very difficult to deal with and to accept, although typically they go along with quite decent equity prices. But we consider all that and we have to make trade-offs in economics all the time and the idea is the lower the interest rate the better it is for investors. Read more

'They' recon people have too much money.. and it's about time to get this savings of 'em.. 'They' always find new ways.. like taxing pension finds, etc.

Give that man a job. Great opinion piece and easy to digest. Oh wait he's got a job. Maybe he could write here more often.

President of Property

Excellent article and a decent departure from the usual tone of opinion pieces published here.

Well done!

What happens when The Fed Vice Chair changes his mind and says something like

FISCHER say 2020: Well, clearly there are different responses to higher Interest rates. If you’re a saver, they’re very good to deal with and to accept, although typically they go along with dramatic falls in overpriced equity prices, due to our previous policy blunder of negative interest rates. But we consider all that and we have to make trade-offs in economics all the time and the idea is the hiher the interest rate the better it is for investors.

Disaster waiting to happen.

Synopsis:

"It is not our central view that the RBNZ will be forced to follow the same path taken overseas".

"The RBNZ has not yet officially ruled out cutting the OCR below 0%, to negative levels".

"It is not our central view that the RBNZ will need to apply unconventional monetary policy. However, with the OCR already at all-time lows, it seems timely to consider this tail risk as part of considering a range of plausible outcomes".

"In other words, while the New Zealand Government appears hesitant to pre-emptively loosen the fiscal purse strings, if a recession causes the RBNZ to embark on unconventional monetary policy, it is likely that those same circumstances would also result in more supportive fiscal policy".

Meanwhile, private wealth has increased at 18% per year rate worldwide, doubling their capital every 4 years, since the GFR in 2008. Talk about raiding the till on the way out... All that government debt is being bought by private groups right under our noses; the tax payer will foot the bill!

"Talk about raiding the till on the way out"

Yes. The problem we have is that policies are only pumping asset values which doesnt actually generate real wealth across the board, so the effect on commodity prices is muted. ie No matter how rich Bill Gates gets, he will only drink so much milk. So the policies which ultimately aim to lift commodities to viable levels doesnt work - the effect becomes a transfer of wealth (claims) to already wealthy.

The problem the supposed rich have is that the system is geared up to run on full capacity, it cant function just for them.

We have had eight years of this rubbish and seem to be going backward. They need to think carefully about what they are trying to achieve and pursue that in a highly focused way. Just throwing money willy nilly into the economies just seems to be producing undesired side effects like asset bubbles and extra cautious spending behaviour. I think what they are trying to achieve is to encourage business investment in new business and productive assets, higher wages supported by increased productivity and volumes of production. If that or something like it is what they want, then they need to target support for that behaviour far more closely. The cynic in me wonders if channelling cash to the wealthy is partially bend it all. Even if it isn't that is what they are doing.

Correct. Ultimately what they are trying to do is keep producers viable - especially Oil producers - by lifting demand and the Oil price to a viable level. But asset inflation is only having a weak effect on demand for commodities - and they are running out of tools.

I don't understand this statement:

"As a result, both the money supply and the government deficit increases hand in hand."

Surely, with true helicopter money, the money is simply "printed" into existence - no need for government borrowing. Personally, I think the government should get on with helicopter money now and spend it on infrastructure. This will both be inflationary and also likely crash our dollar - but those are both good things in this environment. The inflationary element can be controlled by controlling the quantity of money injected. Many people are unaware that our original state houses were funded by money printing - worked just fine.

This appears like a viable option in isolation, but collectively it wont work. This is basically what China has done, build massive capacity for ... the brighter future .. capacity that isnt needed because the future cant pay and wont pay. This is only throwing more IOU's on the credit card.

Debt/money/wealth is only a claim on future energy surpluses - its the future energy surplus thats missing.

could also start a house building program and stop house inflation

avatar,

Good point. It does seem conventional for Central Bank printed money to be "loaned" to their government, as though one day it will be or should be paid back. So it sits on the Fed's and the BOE's and the BOJ's books as debt- hence the Japanese government debt appearing to be the largest in the world, at the same time as the BOJ has bought up trillions and trillions of not only their own debt, but they are easily the largest shareholder in every public company in Japan, as well as a good number on Wall Street.

There would arguably be a deficit, which is different to debt.

I agree with your solution, and have done for a number of years. Rebalance the economy towards productive enterprise and away from property speculation, by funding infrastructure, not only then getting infrastructure, but also lowering the exchange rate that anyone sensible agrees is too high.

Nevertheless it's good to see these opinions getting more mainstream with this article.

LOL ... tell it like it is. Unconventional Monetary Policy is basically an acronym for fairyland.

The central bankers know that they have run out of tools ; everyone is bankrupt - the future can no longer pay and they know this. No amount of financial manipulation can bring back cheap to produce energy (and real growth). We are now like wily coyote, running full speed in thin air. The only thing stopping us from falling is collective faith that we cant possibly fall. When zero and negative returns are everywhere permanently (a la Japan), faith will disappear.

And, unfortunately NZ is not an island, everyone is in it together.

This whole paragraph IMHO shows their woolly thinking; "Back in 2009 when the GFC was at its height, the US Federal Reserve and Bank of England initially cut and paused policy rates at 0.25% and 0.50% respectively. At the time, it was thought that cutting interest rates any further would potentially cause more harm than good. In particular, it could have the unintended consequence of hurting the profitability of banks and building societies, unable to pass on negative interest rates to depositors." as I understand negative interest rates, their purpose is for Government's to use them to direct stimulus in an economy. To date they seem to have been used with a shotgun approach, no direction, no specification, therefore no real results. Of course they'll be a problem for depositors, they'll cause a run on banks as people pull their money out rapidly and likely cause a bank to collapse. Negative interest rates are for Government's and Central banks to pay commercial banks to get money into an economy to stimulate growth. Thus it must be spent in ways that does things like create jobs, increase actual consumption, increase trade (including exports) and so on. Undirected it will just get spent on houses and land which does none of the above, unless it is new development, but will still be limited in any overall and long term benefit to the economy. The question is will Governments or Central bankers have the clues to do this?

another part of this equation is the question of what the commercial banks are doing with depositors funds - loaning them to property investors at 3 - 5 % interest rates, or investing in real business ventures that will generate real benefits to the economy at what 10 - 15%? So who is the real problem here?

The function of the RBNZ at the low OCR is just to pump wealth to the rich or new rich. It's a good time to work in finance, construction industry or own property/shares. If you are outside of those the RBNZ is giving you the middle finger and thinks you should live in a car.

If RBNZ considers ZIRP or NIRP it will be time to rethink the function of our central bank and the ability of banks to create money. These are failed policies internationally and the Fed is trying to escape the liquidity trap by slowly increasing their OCR.

Leave the BoJ to destroy their entire economy, there's no reason for the rest of the world to follow their self destruction.

It does seem strange that the world follows Milton Friedman's approach to the letter except when it comes to helicopter money. It's like there are people screaming "don't give money to poor people!" Even though that would create the most stimulus. It's as if there are people fighting the trickle down effect.

The problem with all this QE and so forth is that it is all based upon flawed economics.

It works on the principal that in order for the money supply to increase debt has to increase. Debt must equal deposits.

So to achieve an increase in money supply someone has to borrow, and that someone is the government.

So in order to increase the money supply the government gets into debt and ultimately the interest payments become unsustainable.

On the other hand “Helicopter Money” is frowned upon. So what is it?

How about this?

The government makes big tax reductions, particularly to lower incomes. These tax cuts are funded by the government printing its own money at zero interest rates.

When the economy heats up the government increases the taxes and destroys the extra revenue collected. All square

So stop mucking about and admit it is this stupid economic system that is broken.

"An asset purchase program from the RBNZ could be even more potent if accompanied by an expansion in government spending, with monetary and fiscal policy working in tandem. With one of the lowest levels of Government debt to GDP in the developed world, New Zealand has the luxury of having real room to manoeuvre with fiscal policy. Implementing this approach would require a significant change in mind-set or circumstances. At the moment, the NZ Government is still focused on reducing (not increasing) Government debt to GDP."

Highlights the feeble effort so far to do anything material to reduce the exchange rate and create inflation.

Central Banks are either being co-opted to keep the economies afloat with QE or being pushed aside with ineffective monetary policies. The GFC was brought on the world by bankers who were not regulated properly by, among others, the Central Banks and later the recovery strategy was handed over to the very same bankers who were in the Finance Ministries, thanks to the Revolving Door syndrome. Net effect, Banks have been and are being supported with no limits, it seems.

The American model has won over the conservative British model of Central Banking. Now everything is up in the air. And every one is afraid of the eventual landing...Sleep well.

Excuse my ignorance; if all the governments have huge debts, who lends them the money?

In abstract terms it is the future ... we continual to borrow further into the future assuming an ability to keep service a growing debt mountain...

In practice it is pension schemes and private investors

Why can't we print money and buy back the countries assets? eg steel mill, fishing quota, power generators, telecommunications, forestry, triboard mill etc etc.

Isn't that what the States have done is print money?

By controlling the power to print money, the Central Banks/Governments in effect control the lives of citizens, present and future. It is the worst form of Dictatorship, but we haven't realised it yet.

The drawback to NZ printing money is

- imports (especially Oil) become more expensive as our currency weakens, meaning we get to spend less on stuff

- our foreign debt (essentially US$ based) becomes harder to service as our currency weakens

The US has the advantage of being the world currency, courtesy of

- the Petrodollar (effectively a deal that Saudi will only sell Oil in US$ in return for military support, so all Oil is US$ traded. Energy is the economy.

- military presence (implied force) - they dont spend gazillions on military for nothing ...

The net result is that the US gets to consume a massive disproportionate share of the world resources

Wow! good answer, that makes sense and explains a lot.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.