Today's Top 10 comes from interest.co.nz's Gareth Vaughan and David Chaston.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

See all previous Top 10s here.

Due to my (Gareth's) oversight at organising a guest Top 10 contributor this week we were left with a hole to fill at short notice. We at interest.co.nz love a good chart and we know many of our readers do too. Thus the idea of a Top 10 of charts, or chart porn as we sometimes joke, was born. So here goes.

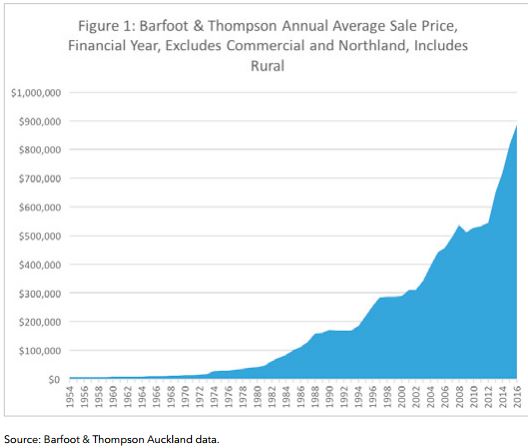

1) Where better to start than with Auckland house prices? Our first chart comes courtesy of the Auckland University of Technology's John Tookey. It's included in his new report entitled, The mess we're in: Auckland's housing bubble from a construction sector perspective. It's a chart of Barfoot & Thompson's annual average Auckland house sales price, dating back to the mid-1950s. Quite a spike over the past few years...

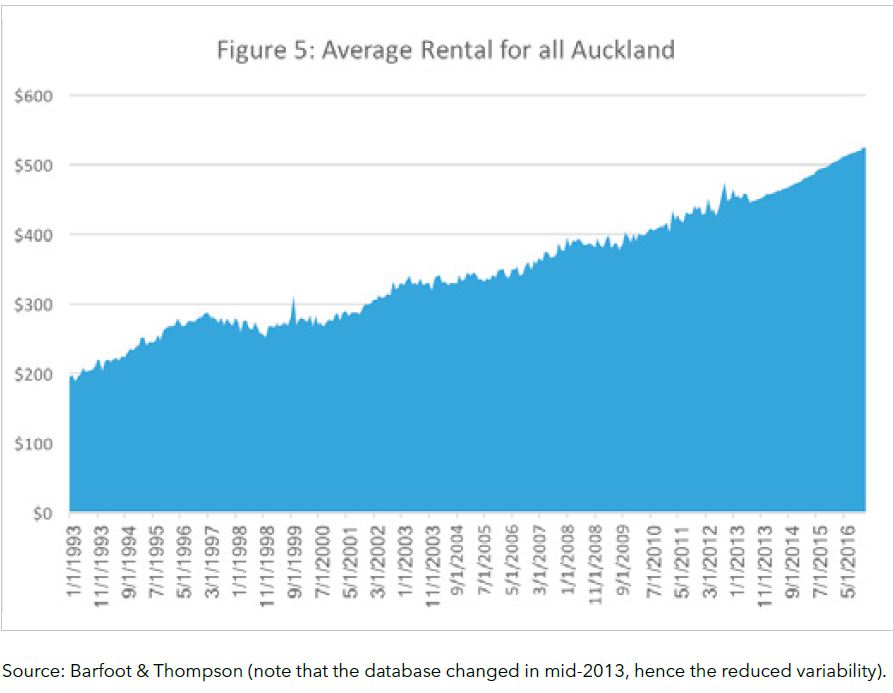

2) The second chart also comes from Tookey and B&T. This one's the average Auckland rental. It doesn't go back nearly as far as the house price chart, but nonetheless still paints quite a different picture.

Below are some of the conclusions drawn in Tookey's report.

The fact is that, on housing, we are in a mess. A huge mess. The bubble is inflating further and, as a society, we are – for entirely rational reasons – continuing the behaviours that created it. To quote Albert Einstein: “We cannot solve our problems with the same thinking we used when we created them”. The solution to this mess is inevitably governmental policy that compels market behaviour. We cannot leave matters to the free market and then continue to be stunned by the inconvenient fact that the market acts in its own best interests. Developers, builders, house buyers and the public all act for their own best interests. These stakeholders will not act as charities, pro bono publico. To think otherwise is naïve in the extreme.

He suggests the use of both carrots and sticks to combat the problems.

A meaningful response to the housing bubble will have two things at hand: sticks and carrots. Starting with the sticks, there are various ways to take pressure out of the market by disincentivising property speculation and the buy-to-let model for additional property acquisition. Typical methods adopted by governments around the world include a capital gains tax that could be incremented according to the number of properties held. However we need to focus on the broader solution of delivering large numbers of properties outside of the normal market delivery rate. In other words, we need to get ahead of existing demand, which is currently attenuated by the drip-feeding of properties into the market to maintain values.

And he floats an interesting idea to incentivise residential property investors to sell up.

A more sophisticated alternative to the sticks approach is to hold a carrot in the other hand – that is, to adopt incentives that encourage buy-to-let landlords to sell their properties in the short term, while at the same time disincentivising them from buying back for the same purpose. The ideal effect would be to ‘vire’ properties from the rental property sector to the owner occupancy sector – that is, to transfer them from one account to another. One strategy would be to use tax law and capital gains protection (assuming the prior introduction of a capital gains tax) as an incentive to sell rental properties into the owner-occupier sector. For example, allowing one-off investment of capital gain on rental property sale to enter tax free into a KiwiSaver account. This would have the effect of freeing up more property and capitalising the NZX for future investment in the economy.

(And here's Tookey in one of our Double Shot video interviews with Greg Ninness from last year).

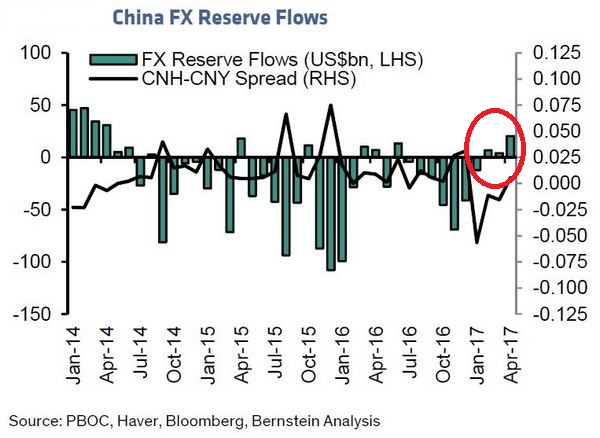

3) Sticking with the Auckland housing market theme, this chart comes from a research report by Hong Kong-based ex-pat Kiwi and Bernstein equity strategist Michael Parker and his colleague Kelman Li. It shows how successful Chinese authorities have been over recent months in turning around capital flight. The red circle was added by me. As interest.co.nz's Greg Ninness has reported including here, there has been a notable drop off in ethnic Chinese buyers at Auckland property auctions over recent months.

Obviously other factors are at play too. Notably the 40% deposit requirement for residential property investors introduced by the Reserve Bank last year. But with the latest monthly Real Estate Institute of New Zealand figures showing the Auckland median price down $50,500, or 5.6%, to $854,500 in April from March's record high of $905,000, and the North Shore median down a whopping $115,000, surely the slowdown of money coming in from China is a, or potentially the, key driver.

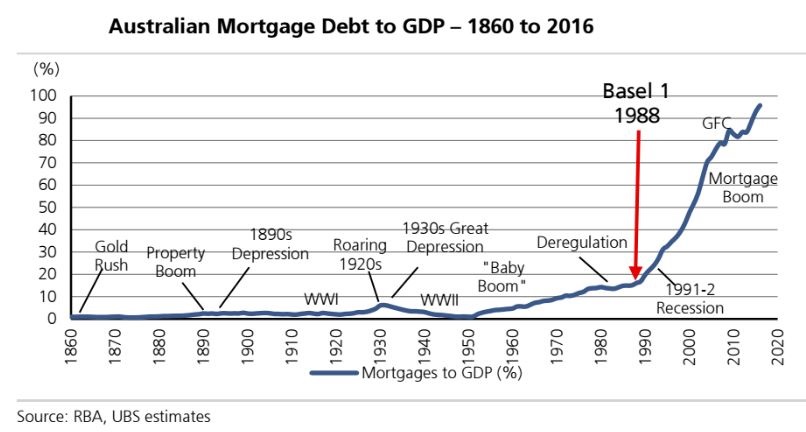

4) The controversial Basel banking regulations. This chart, from UBS, is timely given the Reserve Bank is embarking on a wide ranging review of banks' capital adequacy requirements. We're now into the third iteration of Basel. The UBS chart demonstrates how the Australian mortgage boom took off after Basel I was introduced. Undoubtedly there were other factors at play too. But the way the Basel standards incentivise banks to lend against residential property has been a key one.

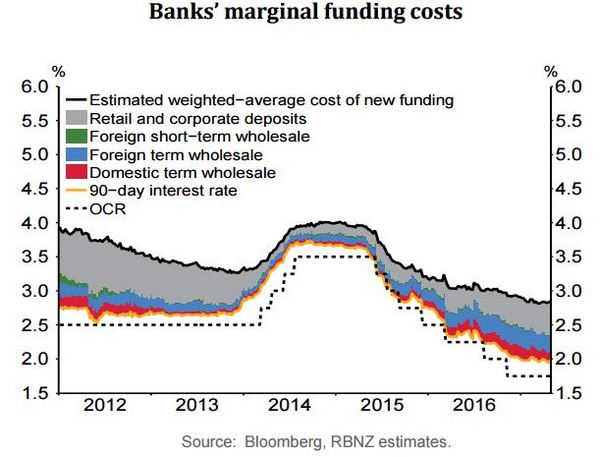

5) Bank funding costs. Bank executives are constantly telling us their funding costs are rising and are "decoupled" from the Official Cash Rate. This chart, from the Reserve Bank's latest Monetary Policy Statement (MPS), shows funding costs have been falling over the past few years. As I reported last month, figures from KPMG's latest quarterly Financial Institutions Performance Survey show bank funding costs down 30% in two years.

However, all four major New Zealand banks have reported chunky falls in their net interest margins in their latest financial results. The drops, year-on-year, range from 10 basis points to 22 basis points. The net interest margins reported range from 1.96% to 2.30%, which remain strong by international standards.

Interestingly, the pressure is coming from deposit rates, which might be news to some long term savers given how low their interest rates have been for so long. If you are When you are bargaining with banks over your deposit rates, keep in mind that they really need deposits. Both to help them meet the Reserve Bank's Core Funding Ratio, and in the case of our Aussie owned banks, to also meet the Australian Prudential Regulation Authority's Net Stable Funding Ratio.

Here's the Reserve Bank from the MPS on funding costs;

The decline in global bond yields in recent months has flowed through to wholesale interest rates in New Zealand. While wholesale funding conditions have eased since the February Statement, domestic deposit rates continue to put upward pressure on banks’ marginal funding costs.

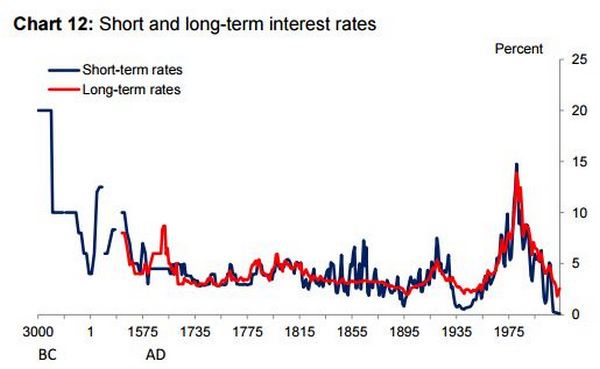

6) Admittedly this chart comes from a speech given by Bank of England chief economist Andrew Haldane in February 2015. So it's not exactly freshly minted. I've used it at least once before, and it has appeared in various publications around the world. But it's worth one more look. Haldane and his team tracked interest rates back 5,000 years to demonstrate just how low they've been in a historical context over recent years.

Here's Haldane from that speech.

Chart 12 plots a measure of short and long-term interest rates back to 3000 BC. Though the data are patchy, they suggest interest rates fell secularly in the run-up to the Industrial Revolution, from double-digits to around 3%. Alternative interest rates, such as the rate of return on physical assets such as land, show a similar pattern.

One interpretation of these trends is that they reflect society’s evolving time preferences. In the run-up to the Industrial Revolution, society became more willing to wait than in the past. That, in turn, enabled saving, investment and ultimately growth. Patience was a virtue. But if society’s time preferences were indeed shifting, that still begs the question why?

Here, we can enlist some outside help. Experimental research over the past 50 years, by psychologists and neurologists, has taught us a great deal both about the determinants of patience and how it affects behaviour. This can perhaps provide insights into some of the historical drivers of a more patient, and hence higher growth, society.

One important driver of patience is income and wealth. The lower income, the more impatient is human decision-making. Why? Because surviving on limited means absorbs huge amounts of cognitive energy. It causes a neurological focus on the near-term. This myopic thinking has been found in everything from under-saving for retirement to over-borrowing from pay-day lenders. In developing countries, it may help explain poverty traps.

Now I hand over to David Chaston.

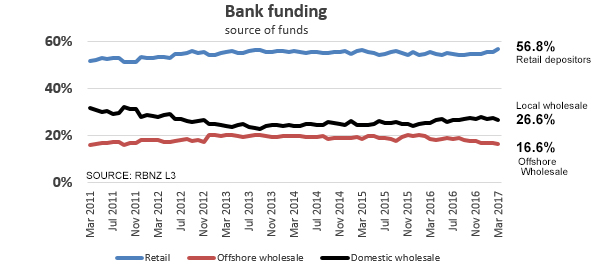

7) How our banks fund their loan books.

Our banks have way too little equity. Bank shareholders get their high returns because they use other's money to operate their businesses. I often point out to bankers that they would never tolerate lending to a business with a balance sheet like theirs. But let's look past that issue for a moment.

This chart is about where they get "other people's money". This chart is of term funding, and does not include the on-call/overnight portion. (Less than 0.5% of at-call funding is from offshore sources.)

This is instructive for those who engage in cheap bank-bashing. And I suspect the above facts will be a surprise to them.

Essentially, 83.4% of committed bank funds is sourced locally. And that proportion is rising.

The proportion being funded from offshore sources is just 16.6% and that is the lowest level since March 2011 when this RBNZ data started.

And the funding by local term deposits is at its highest level ever at 56.8%, at least since this data series started. It is true that banks need that offshore source, but they are making good progress weaning themselves off it.

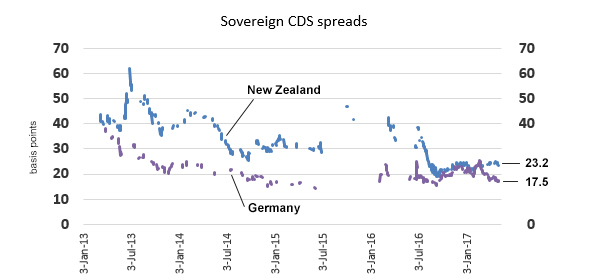

8) How offshore investors regard NZ's sovereign bond risk.

Investors buy bonds that have maturities five, 10, 20, 30 years in the future or even longer. As the risk of default grows over longer periods, they can insure against that risk by buying a credit default swap (CDS) contract. These types of derivative contracts have become a huge business (because the bond market is itself huge). They do allow the rest of us to track investor confidence in both corporate and sovereign bonds.

And as you can see here, these investors have fallen in love with our sovereign debt, ranking it with some major benchmark economies, and as better than many large ones. The improvement has been substantial over the past few years and has no doubt saved the NZ Treasury substantial amounts in interest costs.

We are comparing New Zealand to Germany here primarily because Germany is among the lowest around. The Swiss may be lower but we don't have their data. But here are the current CDS spreads for the usual suspects we compare ourselves to: The USA is 22.2, the UK is 28, Australia is 26, Sweden is 20, France is 29 (although before the election it got up to almost 70), China is 80, and Japan is 25. Norway is the best at 15.

We are batting in a heavy-hitter lineup and performing very creditably in the risk-perception stakes.

At the other end of the scale, countries we don't usually compare ourselves to include Venezuela at 3,170, South Africa at 190, and South Korea at 57.

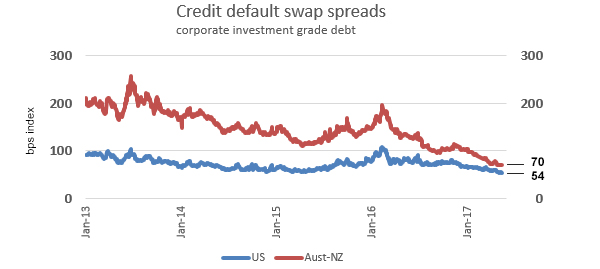

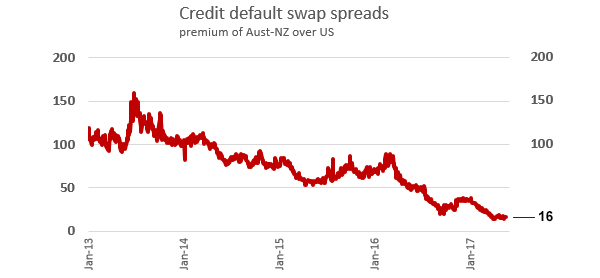

9) So let's look at corporate (investment grade) debt CDS spreads as well.

We don't have ready (free) access to New Zealand corporate debt CDS spreads. The best we can track is the "Australasian" index released daily by Markit. The investment grade index covers both bank debt and other debt, mainly from Aussie miners and resource companies. But the bank debt portion is a sizeable weight in this index. The reduction of risk assigned by these market forces is also impressive. And the improvement over equivalent American investment grade corporate debt is substantial.

The next chart tracks that difference. It has never been as low.

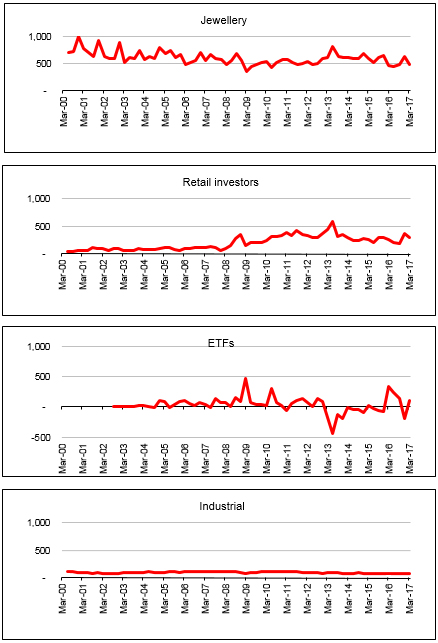

10) Gold.

Like most people following "the markets" we include our daily tracking of gold. But I sometimes wonder why. The gold price reacts to risk issues in a very minor way these days. And the fundamental demand underpinnings seem to be going nowhere. Here is the latest data from the World Gold Council, the industry body charged with spruiking the commodity class. They are up against it as these longer term charts reveal.

If it wasn't for the poor old [gullible ?] retail "investors", I suspect the bottom would drop out of this market. The global jewellery demand has been steadily falling, the big hedge funds have lost interest after loosing a bucket load on false calls, and there is virtually no industrial demand.

35 Comments

The first chart clearly shows that from 1954 to 74 our nation had far more productive things to do with our investment capital than it appears today. If we are to become more productive and raise our standard of living we must return to those times where we were much wiser.

Well, we did have a better balance of land tax and income tax to encourage housing to be about homes rather than investment, breaking up those earlier land banks including those held by foreign speculators. Not to mention government builds and other measures to help Kiwis get a home.

Was it really that we had more productive things to do or that we weren't obsessed with monetary wealth and possessions? Did we lead simpler lives where family, friendships and community were more important? Did we appreciate what we had? Was there more equality of incomes?

What caused the massive jumps from the 70's onwards? The removal of the gold standard which kept a limit on money/credit supply? Baby boomers entering the property market? The introduction of neoliberal economics? Increasing globalisation and corporate rule?

How much more productive can we get? Globally we are awash with products, with stuff. How much more do we need to produce? Where are we raising our standard of living to? What is our definition of standard of living? It appears that for those who haven't been able to own property, who work for salary and wages (including many self employed), their quality of living is not getting better.

Yes, we do need to become much wiser.

Thank you Meh, one of the best comments I have seen on this site. Totally agree with you. In the 70s and even 80s housing was not an issue...still cold and damp however but everyone had a affordable roof over their head. Wages were good, Uni was free....what happened?

frazz - today's youth could also have "free" education if their parents were happy to pay a 66% tax rate as it was back then for my father and others - I didnt actually go to Uni so I guess he landed up paying for someone else - personally I'm a fan of users pays and undertanding the true cost

The first chart shows almost nothing. If house prices doubled in the sixties it would barely show up in the chart. Showing growth in this way is almost always misleading and meaningless

Well here is how I read this info:

The first chart shows clearly that there have been 4 price boom periods (cycles) between 1974 and 2016 ( the 4 segment of price rises) the first two took longer to complete than the last two .... It also shows that prices GO UP in every cycle ... No crashes or busts of huge magnitudes ( more than short term 10-15%max)

However, in each cycle house prices ended up to approximately 1.8 times where they started at the beginning of its starting point .... the numbers are bigger but the multiplier is almost the same in all the 4 cycles.

Each time the average reached a peak, prices flattened or slightly went down for a consolidation period of 2 to 4 years and took off again ... regardless of productivity, Government , and world economic influences .... so historically long term prices prove to have almost the same behavior with a blunt average annual rise of 3 - 7% pa over the last 40 years (maybe someone can give a better number if they have the true curve numbers)... Now, that could just be the very inherent characteristics of the economic and financial systems in place since 1974 including changing immigration policies and global effects ... So history suggests that the end results will continue to be the same as long as we pursue the same fundamentals and economic and banking / lending , supply and demand systems ( apart from tweaks here or there) ...

On the other hand, rental prices have been going up in a steady manner ironing out the wrinkles in the house prices (investments) almost with the average rate of inflation pa.

Why do we blame property investors for buying and holding properties long term ?

How is changing ownership of A rental property from an investor to a FHB going to solve the housing price problem?? --- Carrots, sticks, or even shot guns will not change the current supply shortage problem ... need to increase stock not punish others who learned how to capitalise on the "phenomena" in Curve 1 !!

I am certain that you will find close similarity in the curves of all major cities in the world.

The end of Canada's housing boom features in The Econonist. Canada's debt to disposable income eerily similar to NZ.

http://www.economist.com/news/americas/21722249-american-protectionism-…

Home Capital Group (their high risk lender) had been handing out NINJA loans to the extent that they were 60% of new mortgages. That's a lot of mortgage fraud by mortgage brokers. They've received a bailout with Canada's pension money to counter the bank run.

One of the other problems is that even without mortgage fraud they've been lending on deposits as small as 1.5% which is completely insane. Unless home owners have some skin the game they can just walk away like in the US subprime crash.

No one seems to be investigating potential mortgage fraud and dodgy mortgage brokers were only pick up when they joined another group of mortgage brokers. Without policing who knows what toxic debt is sitting out there. Couple that with a uptick in desperation to sell in Auckland and we could have an event happen here. There's only so much hot air you can use to sustain a bubble.

This chart is about where they get "other people's money". This chart is of term funding, and does not include the on-call/overnight portion. (Less than 0.5% of at-call funding is from offshore sources.)

Where is this money repository located prior to being recorded on the nation's collective digital bank balance sheet liability ledger, excluding ~$6.0 billion circulating notes and coins?

The money is located in cheques that the big four banks pass to each other to keep up with the debt servicing payments. Of course they have to borrow to pay.

Cheques are just claim on money.

It's my way of comparing the financial system to cheque kiting.

@ 2

Tookey's Comments

"However we need to focus on the broader solution of delivering large numbers of properties outside of the normal market delivery rate" - This makes sense

Then

"The ideal effect would be to ‘vire’ properties from the rental property sector to the owner occupancy sector" - Surely this is simply shuffling the pack and doesn't contribute to overall supply

My thoughts too. Great analysis and rubbish conclusions about what to do. Basically, we should copy all the failed ideas of others rather than get serious and face the real problem head on.

This only holds if you subscribe to the view that we are, in fact, short of homes for the population. I do not, I see a lack of context in the homelessness statements various agencies are making. Many, many homes are left vacant now on purpose, a rental sold to an occupier is neutral. Many folk crying homeless in a specific zone are there due to poor decisions or could easily live elsewhwere, some are no longer tenants due to their disrespect of their prior abode. With the demise of unnatural capital gains we will find out the truth.

10. If it wasn't for the poor old [gullible ?] retail "investors",

These poor gullible people will still have wealth after the next GFC, OBR or Demonetisation event.

They will probably say the same about the poor gullible bank depositors,share holders and debt slaves...

In the words of JP Morgan "Gold is money everything else is credit"

Steve Keens comments on the state of the Aussie economy: http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=118…

"The housing bubble makes the politicians look good because A, people are feeling wealthier, and B ...

people are borrowing money to spend," he said.

"Then the government runs a balanced budget and looks like it really knows what it's doing"

"It hasn't got a f***ing clue frankly, because what's actually happening is the reason it's making that money is credit is expanding," he said.

"It's the old classic story, you're criticising a party because someone's laced the punchbowl. You try to take the punchbowl away from the party you're a very unpopular person but you need to because what's actually happening is people are getting intoxicated with credit"

... so long as interest rates can remain at rock bottom levels forever , nothing can possibly go wrong ...

But , I do feel a tadge snubbed once again by the Aussies ... Steve Keen didn't include New Zealand in his list of debt zombie economies .... bugger ! ... and we've tried so bloody hard too ...

The long term chart was plain to me, interest rates have returned to their long term normal after a couple of exceptional decades in the 70's and 80's. While they could, they may not ever go back to that, this could be where they stay.....

"In the past year alone, the Fed bought $387 billion of mortgage bonds just to maintain its holdings. Getting out of the bond-buying business as the economy strengthens could help lift 30-year mortgage rates past 6 percent within three years, according to Moody’s Analytics Inc."

https://www.bloomberg.com/news/articles/2017-02-06/the-mortgage-bond-wh…

I noticed that too. It appears that long term normal is around the 5% range so if looking at OCR or govt. bonds there is still an increase to come.

Questions though - what amounts were households borrowing in comparison to incomes? Were borrowings short term or 20-30 year mortgages? When did fractional reserve banking kick in? What were households borrowing for? It appears that outside of interest rates, this time it's different...

Note that it didn't need the existence of Central/Reserve Banks to manipulate interest rates for such a long period of time.

https://www.amazon.co.uk/dp/184792445X/ref=pe_3187911_189395841_TE_3p_d…

By Steve Keen on 19 May 2017

Format: Kindle Edition Verified Purchase

First an admission: Yanis and I have been friends since we met in 1991, when I was doing my PhD at the University of New South Wales and he was a Senior Lecturer at the University of Sydney. This hasn't influence my review however: if I hadn't enjoyed the book, I would simply not have written one.

Having read it, I am confident that it will go down as one of the great political biographies of the 21st century. It is a work that people will turn to when they try to understand what on earth happened during our time: a riveting, compelling history of a critical act in the self-inflicted decay of European civilisation.

Whew ! What a relief to see that only 17% of our Bank funding is from offshore .

So the risks to our currency and Banking system of sudden outflows would ( hopefully ) be muted

That must also give the Reserve Bank some comfort .

To be fair , we New Zealanders are really still in a sweet spot all round , and with the exception of house prices in Auckland we have little to complain about .

Good top 10 btw

Have a good weekend

{kind=link}

Seems like a good bet.

#4 The Basel settings have been wrong from day 1. These settings could have been adjusted so that western economies don't centre around housing and instead productivity but no. During the GFC there were enough problems with the interaction of the regulations and the credit rating agencies. The concept of the credit rating agencies is completely flawed and perhaps their exclusion would make more sense unless they were properly regulated.

#10 I don't view gold as an investment as such only a store of value. Perhaps just have a small amount of cash and gold to fund fleeing whatever country you are in at the time. A financial bug out bag if you will. I've seen people that have their entire retirement fund in gold, and it's the most stupid thing I've ever seen.

Anyone else viewing this on a Microsoft surface and it being stuck on mobile view, instead of desktop view? Is there a way to force the website to desktop view?

I've had the problem too. I have taken to logging off the site and re-entering. Seems to clear it.

New listings in Auckland today - 83 so far. Only 17 are for sale by auction.

I would say that is a pretty low ratio compared to recent times.

Wow I'm still staggered by this snippet of information in your article Gareth; "North Shore median down a whopping $115,000, surely the slowdown of money coming in from China is a, or potentially the, key driver".

Umm.. Could we have a bit more information on this? From what time period was this very significant price drop? And are their areas on the East Cost that are experiencing similar drops (Since both North Shore and parts of the East Cost were very popular with Overseas Investors)?

For bank funding, what does "domestic wholesale funding" mean?

Great graphs by the way.

With over 10% fall in North Shore house prices its now time more than ever before to do NOTHING .

Just sit on your hands because the market has a dreadfully long way to go down before there is value for buyers

Fasten your seatbelts and just sit on your hands , or hold on for the the rollercoaster ride

"If it wasn't for the poor old [gullible ?] retail "investors", I suspect the bottom would drop out of this [gold] market." Really? The fact so many of the world's biggest economies (and the IMF) keep a portion of their reserves in gold probably tells you something about its role as insurance against a sea of fiat money. It provides the same insurance for those "gullible" retail investors you refer to. I suspect the truly gullible are those who believe there's no need for such insurance because the central banks have everything under control.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.