Italian dictator Benito Mussolini at least made the trains run on time, according to legend. But other sources say the nation’s railway system remained horrible under his rule (see here, here, and here).

The same may be true of modern Europe’s (and Canada and Australia and…) vaunted social welfare programs. Certainly, they have helped many people, but they haven’t eliminated poverty, nor let everyone retire in comfort. Could they simply have shifted spending forward, leaving future generations with the bill? Today, we’ll explore that question as part of my continuing Train Wreck series.

Last week, I looked at US public pension funds, many of which are woefully underfunded and will likely never pay workers the promised benefits—at least without dumping a huge and unwelcome bill on taxpayers. And taxpayers are generally voters, so it’s doubtful they will pay that bill. (Even the Swiss, as we will see below, voted against a mild reform to pay for their pension system.)

Non-US readers might have felt a little satisfaction at that. There go those crazy Americans again, spending wildly beyond their means. You are partly correct; we aren’t exactly the thriftiest people on Earth. However, your country may be more like the US than you think.

This letter is chapter 7 in my Train Wreck series. If you’re just joining us, here are links to prior installments.

- Credit-Driven Train Crash

- Train Crash Preview

- High Yield Train Wreck

- The Italian Trigger

- Debt clock ticking

- The Pension Train Has No Seat Belts

The Money Isn’t There

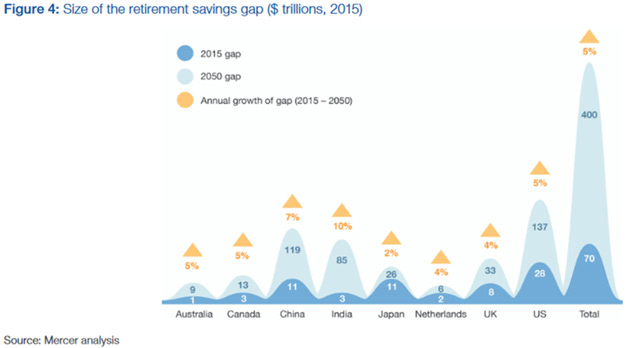

Last year, a World Economic Forum study looked at six developed countries (the US, UK, Netherlands, Japan, Australia, and Canada) and two emerging markets (China and India) and found a $400 trillion retirement savings shortfall by 2050. That’s how much more is needed to ensure everyone of retirement age will receive 70% of their working income, including government, employer, and personal savings—but mostly government.

This staggering number—more than the entire planet’s annual GDP—doesn’t even include most of Europe. Yet unless those countries somehow find the cash, they will break the promises they’ve made to today’s workers.

$400 trillion sounds like a lot of money. It is. But the eight countries in that total represent around 60% of global GDP (my back-of-the-napkin calculation), so you could say that we should add another $250 trillion to get the total global retirement gap. Your mileage may vary by country and demographics.

And for many countries, like the US, that doesn’t include healthcare and other obligations. The final letter of this series will start adding everything up. I actually haven’t done that calculation yet, but we may scare one quadrillion dollars, with a “Q.” That’s with a global economy that is less than $80 trillion today.

Remember what I’ve said in this series so far: Promises like these are debt, whether they show as such on the balance sheet or not. Breaking them is equivalent to debt default. The creditors (workers) will certainly perceive it that way, at least.

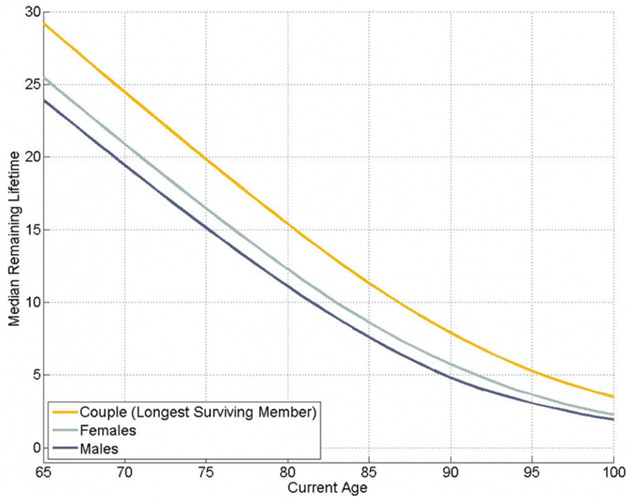

As I’ve also noted, increasing life expectancies are driving this problem. Reaching age 100 is already less remarkable than it used to be. That trend will continue. The good news is we will also be in better health at those advanced ages than people are now. Could 80 be the new 50? We’d better hope so, because the math is bleak if people stop working at age 65–70, which is precisely what the Wall Street Journal wrote this week on their front page. And we see it in the lack of workers available out in the real world.

That said, I think we will see a great deal of national variation in these trends. Some countries have robust government-provided retirement plans, others depend more on employer and individual contributions. In the big picture, though, the money simply isn’t there. Nor will it magically appear just when it’s needed.

WEF reached the same conclusion I did long ago: This idea of spending decades in leisure before your final decline is unfeasible and is quickly reaching its limits. Most of us will work well past 65, whether we want to or not.

What about the millions presently in retirement, or nearly so? That’s a big problem, particularly for the US public-sector workers I wrote about last week. We should also note that we’re all public-sector workers in a way, since we must pay into Social Security and can only hope Washington eventually gives us something back.

And this is going to get worse as the new anti-aging technologies spread. Some are here now. Here is the current life expectancy chart, via Wade Pfau writing at Forbes.

Source: Wade Pfau

When the anti-aging tech kicks in, we will need to shift those curves to the right ten years (at least!!!!). And then I think age reversal will show up by the early 2030s and be ubiquitous by the 2040s.

That’s great news for those who want to live longer, younger, and healthier, but it will force radical changes in our retirement and work. Meanwhile, automation will be killing millions of jobs.

Now, let’s look at a few individual countries.

Safety Valve Stuck

We’ll start with our closest European ally, the United Kingdom. The WEF study shows the UK with a $4 trillion retirement savings shortfall as of 2015, projected to rise 4% a year and reach $33 trillion by 2050. In a country whose total GDP is around $2.6 trillion, the shortfall is already bigger than the entire economy and, with even modest inflation, will get worse.

Further, this was calculated before the UK decided to leave the European Union. That major economic realignment could certainly change the outlook. Whether for better or worse, I don’t know yet. The answer depends on which of my friends I ask and what side of the Remain or Leave fence they are on.

A 2015 OECD study said developed-country workers could on average expect governmental programs to replace 63% of their working-age income. Not so bad. But in the UK, that figure is only 38%, the lowest of all OECD countries. This means UK workers must either save more personally or severely cut spending when they retire.

UK employer-based savings plans aren’t on especially sound footing, either. According to the government’s Pension Protection Fund, some 72.2% of the country’s private-sector defined benefit plans are in deficit, and the shortfalls total £257.9 billion. Government liabilities for pensions went from well-funded in 2007 to a £384 billion (~$500 billion) shortfall ten years later and no doubt grew further since. Again, that is a rather large amount for a less than $3 trillion economy.

To this point, UK retirees have had a kind of safety valve: the ability to retire in EU countries with lower living costs. That option may disappear after Brexit.A report last year from the International Longevity Centre suggested younger workers in the UK need to save 18% of their annual earnings in order to have an “adequate” retirement income, which it defines as less than today’s retirees enjoy. That’s just fantasy. No such thing will happen, so the UK is heading toward a retirement implosion that could be at least as chaotic as in the US.

Having Cake

Americans often have a romanticized stereotype of Switzerland. It is certainly one of my favorite countries. We think it’s the land of fiscal discipline and rugged independence. To some degree it is, but Switzerland has its share of problems, too. The national pension plan has been running deficits as the population grows older.

Last summer, Swiss voters rejected a pension reform plan that would have strengthened the system by raising the women’s retirement age from 64 to 65 and raising taxes and required worker contributions. These mild changes still went down in flames as 52.7% of voters said no.

Voters around the globe usually want to have their cake and eat it, too. We demand generous benefits but don’t like the price. The Swiss, despite their reputation, appear not so different. Consider this from the Financial Times.

Alain Berset, interior minister, said the No vote was “not easy to interpret” but was “not so far from a majority” and work would begin soon on revised reform proposals.

Bern had sought to spread the burden of changes to the pension system, said Daniel Kalt, chief economist for UBS in Switzerland. “But it’s difficult to find a compromise to which everyone can say Yes.” The pressure for reform was “not yet high enough,” he argued. “Awareness that something has to be done will now increase.”

That describes most of the world’s attitude. Both politicians and voters ignore the long-term problems they know are coming and think no further ahead than the next election. That quote, “Awareness that something has to be done will now increase,” may be literally true, but there’s a big gap between awareness and motivation—in Switzerland and everywhere else.

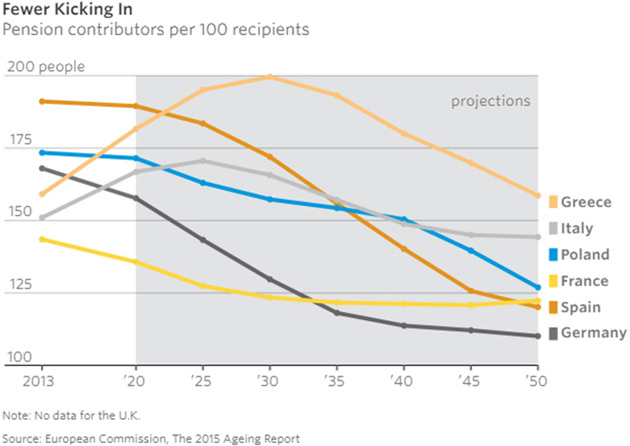

Now, the irony is that even with their problems, the UK and Switzerland are better off than much of Europe. They actually have mandatory pre-funding with private management and modest public safety nets, along with Denmark, the Netherlands, Sweden, Poland, and Hungary.

(Sidebar: Low or negative rates in all those countries make it almost impossible for their private pension funds to come anywhere close to meeting their mandates without large annual contributions for those companies or insurance sponsors, which reduce earnings. And many are required by law to invest in government bonds with either negligible or negative returns.)

Conversely, France, Belgium, Germany, Austria, and Spain are all Pay-As-You-Go countries (PAYG), with nothing saved in the public coffers for future pension obligations. Pension benefits come out of the general budget each year. The crisis is quite predictable because the number of retirees is growing while the number of workers paying into the general budget falls. Further, falling fertility in these countries makes the demographic realities even more difficult.

Debase as Necessary

Spain bounced back from recent crises more vigorously than some of its Mediterranean peers like Greece. That’s also true of its national pension plan, which actually had a surplus until recently. Unfortunately, the government “borrowed” some of that surplus for other purposes and it will soon become a sizable deficit.

The irony here is that, just like the US, Spain’s program is called Social Security, but like our version, is neither social nor secure. Both governments have raided supposedly sacrosanct retirement schemes, and both use those savings for whatever the political winds favor.

Spain has 1.1 million more pensioners than just 10 years ago, and as the Baby Boom generation retires, it will have even more. Unemployment as high as 25% among younger workers doesn’t help, either.

Of the two, the US is in “better” shape, mainly because we control our own currency and can debase it as necessary to keep the government afloat. US Social Security checks will always clear even if they don’t buy as much. Spain doesn’t have that advantage if it stays tied to the euro currency. That’s one reason the eurozone could eventually spin apart.

In at least some of those pay-as-you-go countries, public pension plans allow early retirement at age 60 or below. The contribution rate by workers is generally less than 25%.

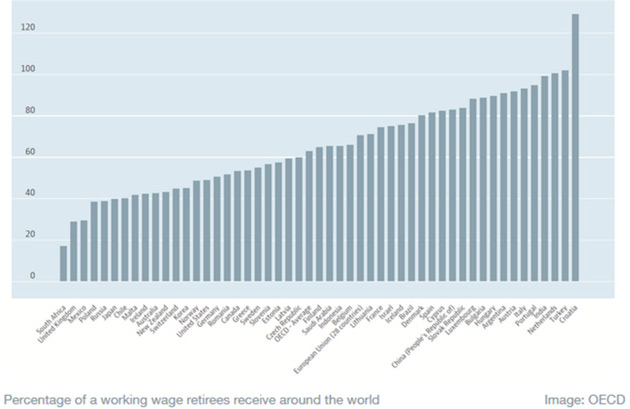

Worse, some governments pay retirees more than they made while actually working. This OECD chart shows pension benefits as a percentage of working wages. It is more than 100% in Croatia, Turkey, and the Netherlands, and above 90% in Italy and Portugal.

Source: OECD Pensions at a Glance 2017

I am sorry, but there is simply no way this can continue. These governments have legislated rainbows and unicorns. They will not deliver such benefits, unless it is because wages and benefit payments crash to unimaginably low levels.

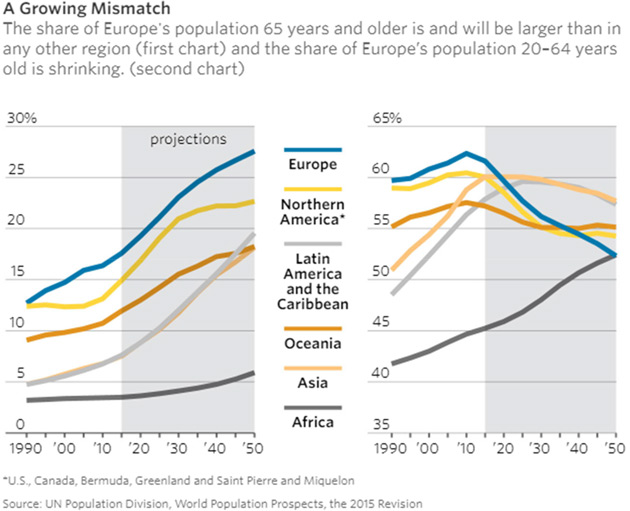

A rather bleak Wall Street Journal special report focused on the formidable demographic challenges. Europe’s population of pensioners, already the largest in the world, continues to grow. Looking at Europeans 65 or older who aren’t working, there are 42 for every 100 workers. This will rise to 65 per 100 by 2060, the European Union’s data agency says. By comparison, the US has 24 non-working people 65 or over per 100 workers, says the Bureau of Labor Statistics, which doesn’t have a projection for 2060.Unlike most European financial stories, this isn’t a north-south problem. Austria and Slovenia face difficult demographic challenges right along with Greece. This WSJ chart compares the share of Europe’s population 65 years and older to other regions, and then the share of population of workers between 20 and 64. These are ugly statistics.

Across Europe, the birthrate has fallen 40% since the 1960s to around 1.5 children per woman, according to the United Nations. In that time, average life expectancies have risen from around 69 to roughly 80 years.

In Poland, birthrates are even lower, and there the demographic disconnect is compounded by emigration. Taking advantage of the EU’s freedom of movement, many working-age Polish youth leave for other countries in search of higher pay. A paper published by the Polish central bank forecasts that by 2030, a quarter of Polish women and a fifth of Polish men will be 70 or older.

Everything I read about the pay-as-you-go countries in Europe suggests that they are in a far worse position than the United States. Plus, their economies are stagnant, and the tax burden is already near 50% of GDP.

Moreover, many private pensions are in seriously deep kimchee, too. Low and negative interest rates have devastated the ability to grow assets. Combined with public pension liabilities, the total cost of meeting the income and healthcare needs of retirees as a percentage of GDP is going to dramatically increase across Europe.

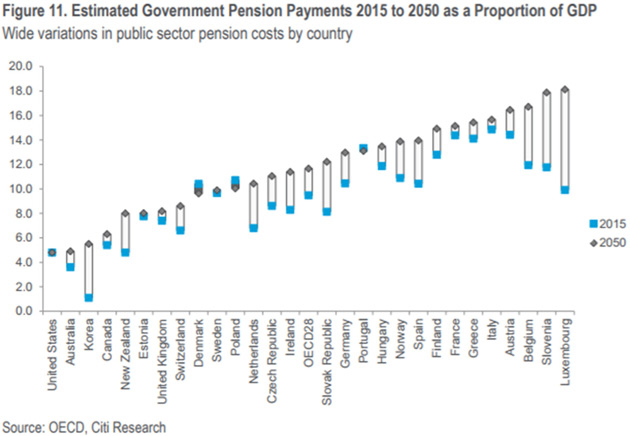

Think about that for a moment. I am not talking about as a percentage of tax revenues. I am talking about as a percentage of GDP that in Belgium will be 18% in about 30 years. Which would be 40–50% of total tax revenues. That doesn’t leave much for other budgetary items. Greece, Italy, Spain? Not far behind…

Source: Citi GPS

Some research makes the above numbers seem optimistic. Most European economies are already massively in debt and have high tax rates. And those in the eurozone can’t print their own currency.

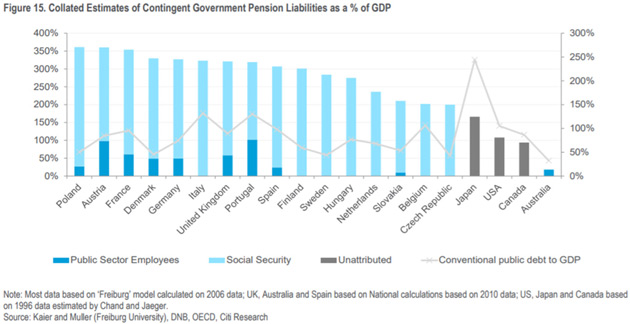

French President Emmanuel Macron and a few others seem to be laying the foundations for the mutualization of all eurozone debt, which I assume will end up on the ECB balance sheet. However, that still doesn’t deal with the unfunded liabilities. Do they just run up more debt? It seems like the plan is to kick the can down the road a little bit further, which Europe is becoming good at.In this next chart, the line going through each of the countries shows their pension debt as a percentage of GDP. Italy is already over 150%. And this is an older chart. A newer chart would just be uglier.

Source: Citi GPS

This problem is far bigger than even the most disciplined, future-focused governments and businesses can easily handle. It is not limited to any one country or continent. The problem exists everywhere, differing only in severity and details.

Magical Thinking

Look what we’re trying to do in both the US and Europe. We think a growing number of people can spend 35–40 years working and saving, then stop working and go on for another 20-30-40 years at the same comfort level, all while fewer workers pay into the system each year. I’m sorry, but that is magical thinking at its worst. It is not what the earliest retirement schemes envisioned at all. They tried to provide for the relatively small number of elderly people who were unable to work. Life expectancies were such that most workers would not reach that point, or at least live only a few years between retirement and death.

The simple fact is that the extended family, which was the source of support for those who were lucky enough to reach old age, has disappeared. As life expectancy has increased and the size of families shrunk since 1950, government has become the paternal/maternal caretaker of those who have reached the magical age 65.

As I’ve pointed out in past letters, when Franklin Roosevelt created Social Security for people over 65, life expectancy was roughly around 56. US retirement age would now be around 82 if the retirement age had kept up with life expectancy. Try and sell that to voters.

Worse, generations of politicians have convinced the public that not only is this possible, it is guaranteed. Many believe it themselves. They aren’t lying so much as just ignoring reality. But it does get them votes. They often outbid each other in political races to be the most generous. That’s not just at the federal level. It is more often seen at the local level promising ever more generous public services while filling all the potholes, too. They’ve made promises they can’t possibly keep, but the public arranges their lives assuming the impossible will happen. It won’t.

How do we get out of this? We’re all going to make a big adjustment. If the longevity breakthroughs I expect happen soon (as in the next 10–15 years), we may be able to do it with less pain, but it is still going to require large and significant lifestyle changes. Retirement will be shorter but better, because we’ll be healthier.

That’s the best case, and I think we have a fair chance of seeing it, but not without a lot of adjustment first. How we get through that process is the most important question.I’m not optimistic because compromise is becoming a lost art. Politics in both the US and much of Europe is an echo chamber where we mostly talk to ourselves and those who are like-minded. We ignore the other side, treating them as socially unacceptable lepers. We have lost the ability to disagree amicably and rationally. Not so long ago, Ronald Reagan and Tip O’Neill could sit down and work on Social Security. Bill Clinton and Newt Gingrich could sit down and not only modify welfare but balance the budget. Those days are gone.

When some librarians think the children’s books by Dr. Seuss are racist and therefore unacceptable for a public library, the quality of civil discourse is spiraling rapidly downward.

I do not like that, Sam I am.

I struggled with this letter a little bit, as there is so much else I wanted to talk about. So many countries that have their own nuances that could fill a book, but my partners are trying to get me to write shorter letters, not longer.

The truth is, retirement is going to be a problem everywhere. I left a longer piece on the cutting room floor about why extended lifespans are not going to be a problem, which I know many readers find hard to accept. But this is just one letter of seven (so far) of what will likely be at least a ten-part series. There are so many aspects to the debt crisis. I know we talked about pension problems in terms of 2050, but we will have to resolve these issues long before then.

From a long-term perspective, this may be good news. The crisis will force us to face reality. It will be painful, but we know about it in advance. That means we can plan for it, and I really have a passion for helping people get through The Great Reset. We are all in this together.

------------------------------------------

*This is an article from Thoughts from the Frontline, John Mauldin's free weekly investment and economic newsletter. This article first appeared here and is used by interest.co.nz with permission.

- Credit-Driven Train Crash (May 11)

- Train Crash Preview (May 18)

- High Yield Train Wreck (May 25)

- The Italian Trigger (June 1)

- Debt Clock Ticking (June 8)

- The Pension Train Has No Seat Belts (June 15)

27 Comments

Once again, an article from this source that contains no information or analysis relevant to the New Zealand position.

Other than the future of NZ export earnings might be tied to the health of some of these economies? Or that NZ savings are invested/exposed to some of these countries?

Croatia looks an awesome country to retire in.

Once again no source or information from you as to why this general article does not apply to NZ. Not even why NZ's position is significantly different to the rest of the world, or say specifically Canada for instance.

Don't know why you are picking out Canada as a comparator - this article is largely about European economies.

Insofar as the article does contain any information about Canada and New Zealand, it suggests that they are in a broadly similar position. That is, that their public pension costs are relatively low as a percentage of GDP, and that they are expected to remain so in the foreseeable future, well below the levels currently being experienced (let alone the levels expected in future) in many European countries.

New Zealand's approach to pensions - basically a universal flat-rate public pension, supplemented on an encouraged but voluntary approach by private arrangements - is very different to what they have in many other OECD economies. That is why New Zealand's present and projected public pension affordability is better than most of theirs.

It really highlights the shortsightedness of governments and the necessity of bipartisan approaches to rectify these type of issue.

Referendums will always get voted down by those that are retired or closing in on retirement so changes to legislate either higher retirement ages or more contributions and lower payment expectations is the only thing that can be done and if a government is always worried that making these changes will lose them power, the bipartisan approach is the only way ...... but Im not very hopeful.

If you think past the superficial information it does more than highlight the shortsightedness of Governments, it highlights their greed. In NZs case our politicians have first and foremost, ensured that they will not only be alright, but will actually be high on the hog, feeding from the trough at the expense of the tax payer. All this while they try to figure out how to short change the taxpayer in their retirement because it cannot be afforded. No political colour is exempt from this. They are all the same.

I wonder if there was legislation that tied politicians retirement benefits to those of the average worker, if they would then be a little more prudent about Government spending?

While there are so many negative views about immigration on this website, there is actually a massive benefit that we won't have anywhere near the ageing demographic problems of other countries. In 20 or 30 years time we may look back at the previous government as heroes.

When the declining birth rate is a result of peak energy per person, and peak resources per person it tells you those events are in our past. Following the rest of the world into overpopulation is no answer.

Migrants get old too - and if you want to keep the same ratio of working age people for each retiree, you need to continually increase the number of migrants.

As it is, NZ will be facing another demographic bulge 30 or so years down the track from the large numbers of migrants we have bought in over the last 7 years.

The retirement age needs to increase in NZ. And if that euthanasia business catches on, it could prove very economical from a healthcare and assisted living perspective.

In the last 20 years we have had about 40,000 to 50,000 permanent residents per year so say over the last 25 years we have had 1million immigrants (including me) and their average age would probably be between 30 to 40 on arrival. So simple maths NZ has imported a million people who will qualify for Superannuation in about 30 years. I have received super for 4 years now. OK mine is only a top up of my UK pension but (a) many immigrants are from countries with no national pension and (b) even the UK has now moved to pensions at 67 so that is two full years of NZ super.

If the immigrants have greatly added to NZ productivity and paid well above average income tax then they may be a benefit otherwise they are a net cost to NZ. The only exception would be recruiting immigrants with shorter than average life spans but unfortunately the INZ health test for applicants makes that unlikely.

Please lets put this argument to bed once and for all.

So we have a commitment to superannuation that is growing as a portion of GDP. Then we have the cost of energy growing as a portion of GDP. GDP is in a declining trend across the world, and interest rates are following closely. I call this a divergence between reality and paper wealth (claims on the future) that is growing exponentially.

The question is at what portion of GDP do these commitments come unstuck? There are all sorts of ways they could become manifest, and in some ways they already have. Kick the can down the road could also be pass the buck to the next generation.

Yes - discretionary income is being squeezed in the middle.

So demand for non essentials eventually dries up

Please show the data which support the statistical claim that "the divergence is growing exponentially".

I do not know what is the cost of energy as a portion of GDP or how it is tracking in the case of New Zealand. But the article above gives that information for the cost of superannuation in New Zealand. It shows that that cost is expected to peak at about 8%, which is far below what most other OECD economies are paying already.

Which suggests that New Zealand already has policy settings which mean we are far less likely to hit the portion of GDP where these commitments come unstuck than do many comparable economies.

Right here:

https://www.tullettprebon.com/.../1%20-%2021.01.2013%20perfect%20storm%…..

Read it. Twice.

NZ hangs on the coattails of the Americam Empire. So next try reading Chomsky's 'Hegemony or Survival". And add Jason Hickel's 'Divide'. Then read Will Catton's 'Overshoot'. And if you get that, his 'Bottleneck'. Then Kunstler's 'Long Emergency'. Then the Donella-et-al Limits to Growth - and the 30 and 40-year updates.

Then visit: www.steadystate.org

Which points out the nonsense that is GDP, and en route, the nonsense that is thinking NZ is inured. Or of comparing NZ to the 'OECD', which when I see it mentioned, always makes me assume the writer/sayer is purposely spinning. And as energy underwrites all work (less than 1% being human labour) it is what underwrites all money. So as the supply quantitively and qualitively fails (an exponential graph it WILL be) the value of 'investments' must fails with it. There simply won't be enough future work done, even as we triage decaying infrastructure, resource draw-down, overloaded sink capacities and overpopulation. Yes, even here.

Or, of course, you could keep on hiding behind a comforting belief/mantra that somehow bank-held digits are real while the planet isn't. It's the common choice :)

No PDK I am not going to go away and read half a dozen books in search of the answer to a simple question of data. I asked what proportion of New Zealand's GDP is currently spent on energy costs, and how that figure is tracking over time, not for yet another tedious restatement of your partial and economically illiterate worldview.

I did follow your link, but since that resulted only in "The resource you are looking for might have been removed, had its name changed, or is temporarily unavailable", I'm not yet convinced.

I figured you wouldn't.

And right there is the invalidation of your 'economically illiterate' comment.

Don't worry, that puts you on par with the Editor of the Listener.

Ms de Meanour

then id try these links.

https://surplusenergyeconomics.wordpress.com/

https://surplusenergyeconomics.files.wordpress.com/2018/06/129-stats-an…

"A critical point here is that, once on the upwards slope of the parabola, the rise in ECoE is exponential. According to SEEDS, global ECoE has risen from 3.5% in 1998 to 5.4% in 2008 and 8.0% now, and is projected to reach 10% by 2028"

Not NZ data (as yet) but then the issue isnt about NZ energy trend in isolation - it would make as little sense as trying to understand our debt /wealth in isolation.

There is also no simple answer to your apparently simple question

"Because the world economy is a closed system, ECoE is not directly analogous to ‘cost’ in the usual financial sense. Rather, it is an economic rent.."

You have to delve a bit deeper to really understand how the energy trend is fundamental.

Few comments. I see things differently.

1. Longevity increasing is a sign of success as a species, not failure. It is a sign of prosperity, advances in technology, public health and medicine and of humanity's progress. Sometimes I think writers of articles such as these should just start advocating a return to chain smoking to kill people off earlier. Living longer is actually good problem to have. (Perhaps the metabolic disease epidemic will come to their rescue and kill enough people off to make the financial maths work for the doom-mongers - they should be promoting Coke consumption vociferously).

2. The problem isn't whether the government has enough cash in the future to fund citizens' retirements. You can't eat bits of paper or zeros in your online bank account. The government, as Alan Greenspan once famously pointed out, cannot run out of money. It is whether our economy can produce enough real goods and services with fewer workers so that my one child can produce enough to sustain her two aged parents as well as herself.

3. Think about what would happen if en masse as a planet governments all started to run much bigger surpluses by taxing our current incomes even more and cutting our consumption by that amount to pay for the future retirement 'crisis'. Sure, we might save money in our national accounts. But it is unlikely that that would translate into massive investment in productive technologies and sustain full employment and incomes and create those real goods and services more efficiently in the future. No. It would kill off demand. Profits would fall. Investment would falter even more that it has in the last 10 years. Unemployment would grow higher, incomes would crash and savings ultimately would also fall. The paradox of thrift. Yes one person saving for retirement is good as long as their income doesn't fall. But if we all go crazy at once with the thrift, we are stuffed. Mainstreamers believe that increased saving by government and the private sector translates into increased productive investment (by say lowering interest rates in theory). Alas, animal spirits are more important - usually raised only by the prospect of increased sales.

4. Surely the best way to create an economy that can deal with a higher dependency ratio in the future is to ensure strong demand so that investment in productive technology becomes more profitable, so that young people can find jobs and that productivity can rise. Otherwise we just increase the dependency ratio today (unemployment benefits/welfare/) in order to somehow deal with it tomorrow. We also run down our infrastructure making us less productive in the future. It is self-defeating.

5. The best chance my child has of having a decent life when I am old is if she gets a good education, is fit and healthy and can find a good job in a thriving economy where goods and services can be produced by her much more efficiently than today. I can't see that economy being created by even more government parsimony and the resulting contraction in demand.

Or should she just kill her parents off?

Tell me where I go wrong.....

where you go wrong? You are (correctly) describing the need for growth. BUT

- The planet is finite Problem.

- Productivity translated means an ever greater use/harnessing/leverage on resources which we already have hammered to death

- technology only ever sits on the back of available resources - not the other way round

- efficiency only cuts it IF it lowers cost of production (not if it reduces demand ) But then there is Jevons paradox ...

- Tech is losing to diminishing returns, higher debt loads and general depletion of resources

- population overshoot on the back of the past easy resource base

Why am i right? The proof is in the debt load.

Debt and the need for debt escalation as a resource proxy since the 80's to keep the ponzi ticking. If tech/productivity gains were awesome you wouldnt see the need to bring consumption forward (through debt) to keep demand afloat. Hence interest rates go ever lower as we rob the collective future to provide our current "income "...

Perfectly put.

Now wait for the media and academic silence. This is how it is now - more and more folk have worked it out, but the combination of fear, belief and denial in high places means it won't ever make the front pages.

why thankyou.

Yes it is unfortunate that it isnt openly discussed ... let alone proactively planned for ... You would think academics would have figured it out but its the silo effect in action - no one looks outside their discipline to the system as a whole.

To startle the sheep wont change the fact we have driven into a cul de sac and the ugly consequences that must come with that. So we print more of the same.

That appears to explain why I wait the same length of time at an airport baggage claim in 1980s as I do now, in 2020s.

Remember for all the criticism of National - Bill English proposed to raise the retirement age slowly and well done the track if re-elected. Taxinda made the same promise as John Key - Not on my watch and the voters loved it.

Didn't help Bill much did it.

It is very hard to persuade workers to lift the age they retire. For manual labourers it can be physically impossible. The only people who have the life experience to handle tough issues are the elderly so when we are more than 50% of the electorate then we will let retirement age creep up and up.

"The only people who have the life experience to handle tough issues are the elderly" what a conceited load of bullshit!

I think you meant to say once they've got theirs the elderly will pull up the drawbridge behind them.

I can't see anyone can argue with my first two sentences so I expect you disapprove of the tongue in cheek conclusion. Yes my 6 adult children are finding life is tough and I am lucky enough to find myself quite comfortable now I am retired. Increasing the age for super in NZ is important - a future debt is being compiled that will not affect me because I will be long gone when my children reach their retirement.

Some people of any age are selfish. It is possible for the elderly to identify with the problems of their children but however kind and considerate the young do not have the experience of being old. One thing is certain however wealthy we old timers are and however hard life is for the young I can assure you each and every retired person would love to swap places.

I can't see anyone can argue with my first two sentences so I expect you disapprove of the tongue in cheek conclusion. Yes my 6 adult children are finding life is tough and I am lucky enough to find myself quite comfortable now I am retired. Increasing the age for super in NZ is important - a future debt is being compiled that will not affect me because I will be long gone when my children reach their retirement.

Some people of any age are selfish. It is possible for the elderly to identify with the problems of their children but however kind and considerate the young do not have the experience of being old. One thing is certain however wealthy we old timers are and however hard life is for the young I can assure you each and every retired person would love to swap places.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.