Westpac is raising most of its fixed home loan rates, effective Wednesday, March 18.

Given the recent rise in wholesale rates, they are likely to be the first of a series of increases from most banks.

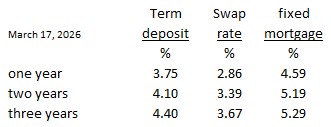

Westpac's increases range from +10 basis points (bps) for its one year rate, to +30 bps for its two, three, and five year fixed rates.

At the same time, it is increasing its term deposit rate offers for terms of one to five years, some also by as much as +30 bps.

Readers who check the swap rate graphs at the foot of this story will find clear evidence of the rising background cost of money. These are costs no bank will be able to ignore.

But while these costs rise, it does open up the opportunity for banks to pay retail depositors more (otherwise they will have to pay the wholesale rates).

Using Westpac's retail rates as a foil,

Westpac's new one year term deposit rate of 3.75% is the highest rate of any main bank for that term, about +20 bps higher than those main rivals. In fact the highest of any bank.

To compare mortgage rate offers in a way that includes the application and account fees costs (or break fee costs if you need to do that), and applying the impact of a cashback/legal fee reimbursement, or other incentive, you can use our home loan comparison calculator. You can find it here. Or, for convenience, we have added it to the bottom of this article.

Negotiate. How flexible banks may be will depend on the strength of your financials.

One other useful way to make sense of the changed home loan rates is to use our full-function mortgage calculator which is here.

And if you already have a fixed term mortgage that is not up for renewal at this time, our break fee calculator may help you assess your options. Break fees will be minimal in a rising market. But they become important in a falling market, like now.

Here is the snapshot of the lowest advertised fixed-term mortgage rates on offer from the key retail banks at the moment.

| Fixed, below 80% LVR | 6 mths | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| as at March 18, 2026 | % | % | % | % | % | % | % |

| ANZ | 4.49 | 4.49 | 4.69 | 4.89 | 5.19 | 5.89 | 5.99 |

| 4.59 | 4.59 | 4.75 | 4.95 | 5.19 | 5.55 | 5.69 | |

| 4.49 | 4.49 | 4.64 | 4.69 | 4.99 | 5.19 | 5.29 | |

| 4.49 | 4.49 | 4.89 | 5.25 | 5.69 | 5.79 | ||

| 4.49 | 4.59 +0.10 |

4.85 +0.16 |

5.19 +0.30 |

5.29 +0.30 |

5.39 +0.20 |

5.59 +0.50 |

|

| Bank of China | 4.38 | 4.48 | 4.48 | 4.58 | 4.88 | 5.28 | 5.28 |

| China Construction Bank | 4.69 | 4.49 | 4.49 | 4.54 | 4.90 | 5.10 | 5.20 |

| Co-operative Bank | 4.49 | 4.49 | 4.69 | 4.89 | 5.19 | 5.55 | 5.69 |

| ICBC | 4.39 | 4.39 | 4.49 | 4.59 | 4.99 | 5.09 | 5.19 |

| |

4.69 | 4.49 | 4.69 | 4.89 | 5.15 | 5.55 | 5.69 |

| |

4.59 | 4.39 | 4.75 | 4.69 | 4.99 | 5.19 | 5.29 |

Fixed mortgage rates

Select chart tabs

Daily swap rates

Select chart tabs

15 Comments

The rest will follow.

like night follows day......

So it begins, the great tightening of borrowing conditions and rates.

Banks need to make a doĺlar and with wholesale rates approching 5%.......mortgages moving back to 7 and 8% become a reality to factor in, when borrowing.

The first of many to raise rates this week, with more raises due throughtout 2026.

Inflation chewing at one end and higher cost of debts funds at the other... this recovery sausage, getting bitten to death!

The now years of falling property values, are set to downleg deeper, as the fragile green shoots get blackened and carbonised, like bubbling, burning, crackling crude!

Agree, this is the end of any green shoots for housing.

If mortgage rates stay in the 5's I suspect house prices will be flat

If they get back into the 6's it could get very interesting. The people holding on waiting for it to get better may just give up waiting.

and the closer we get to Nov election the more people might just wait and see.

NZGecko, please don't ever change, your wordplay is entertaining, informative and often hilarious. Glad to have you on this site

this recovery sausage, getting bitten to death!

Very generous, thanks.

I'm just one of many realists, more outspoken types here, who laugh as the general "bought and paid for" NZ media. I'm one who has skinned my shins over time and know we must see what going on clearly, make our own calls.

Glad to chuckle with others here and learn some different views, some of it rubbish and much is self-interested.

- I see some poor sops here, who are obviously trying to raise their own mud bogged Titanic's ...... of bad investments calls, much of them languishing in a housing market circling deeper into the bog-hole.

Banks need to make a doĺlar and with wholesale rates approching 5%.......mortgages moving back to 7 and 8% become a reality to factor in, when borrowing.

Westpac's share price up 37% past 12 months and and 6.9% YTD. Investors have faith that the Ponzi has legs (at least in Aussie) and the cost of credit isn't overly onerous.

Pension funds will keep piling into the stock regardless. Where else can they dump these funds? On paper, everything looks hunky dory with the Aussie banks.

Ouch, another constraining and dampening impact on house prices incoming!

So the 2 year rate is up about 0.7% in a few months, ouch!

Westpac is a whopping 0.5% higher than BNZ for 2 years, obviously not wanting customers at the moment.

Watch them all raise, by weeks end!

Definitely. Looks like I fixed at the right time for once.

Aussie 10 Year bond yields near 15-year highs at 5%. Water cooler guy said 'meh' and irrelevant to Aotearoa in terms of the Ponzi and associated cost of debt.

Not sure why anyone would think that.

Took out two TDs from Westpac about 6 weeks ago for 6 months. Website an hour or so ago no change.

Seems like just bit of a speed bump tbh

Seen swaps move like this before and it doesnt usually flow through into mortgage rates pushing higher for long, still looks more like a pause than another drop

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.