Property information and analytics company CoreLogic - whose information is widely used by the Reserve Bank - is predicting that the RBNZ will further relax the loan to valuation ratio (LVR) rules in November.

And interestingly, CoreLogic suggests the RBNZ may reduce the deposit limits required by owner-occupiers - effectively changing the current definition of a 'high' LVR.

This prediction is one of 10 made for the rest of the year in CoreLogic's latest Weekly Market Pulse publication.

With the steam having come out of the housing market in recent times, the RBNZ has already twice loosened the LVR rules, the last of these applying from January of this year.

At the moment owner-occupiers have to either find 20% deposits or hope they can fit inside the 'speed limit' that the banks have for loans in excess of 80% of the value of the property. This 'speed limit' restricts the banks to advancing no more than 20% of their new mortgage money for such 'high' LVR loans.

Investors on the other hand have to find 30% deposits, or hope they can squeeze into the very small 'speed limit' for this restriction of just 5% of new bank lending available at 'high' LVRs for investors.

The next time the RBNZ will likely look at the LVR rules is in its next Financial Stability Report in November.

CoreLogic senior property economist Kelvin Davidson believes there will be a relaxation of the LVRs in November "reflecting our expectation of steady market conditions" in the housing market.

"Possible options include lowering the owner-occupier deposit requirement from 20% to 15% and/or raising the investor speed limit for high LVR lending from 5% to 10%."

Such an approach, if taken by the RBNZ, would be a departure, given that from the introduction of the LVR rules in 2013 the so-called 'speed limits' have applied based on deposits of 20%, so reducing the deposit threshold would effectively change the definition of a 'high LVR' loan.

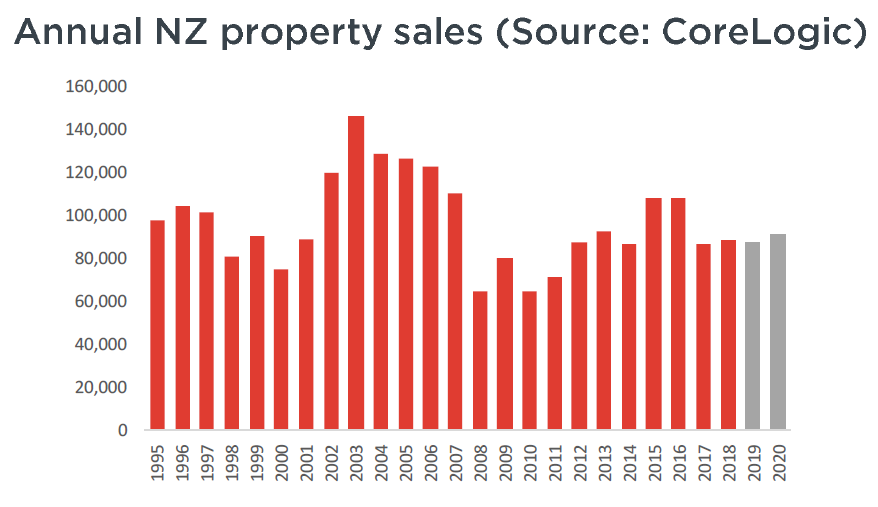

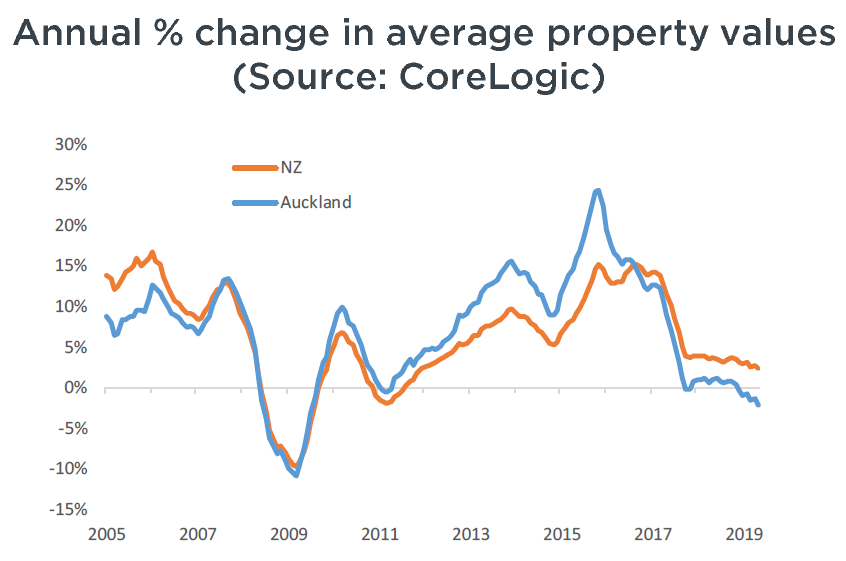

CoreLogic's predicting that house sales volumes will stay pretty flat for the rest of the year, with average property values still rising "but in a restrained fashion".

Davidson said CoreLogic's sales model points to an annual total in the range of 85,000-90,000 for 2019 as a whole, about in line with the average for the past decade.

In terms of prices the more affordable towns and cities in ‘regional NZ’ likely to record the largest increases.

"By contrast, it wouldn’t be a surprise to see further weakness in Auckland – as buyers bide their time."

This is the 10 predictions CoreLogic have made:

1. Sales volumes to stay pretty flat

2. Average property values still rising but in a restrained fashion

3. Further loosening of the LVR rules in November

4. Imposition of extra capital requirements on the banks

5. Banking sector competition to remain intense and ‘rate wars’ to be a recurring theme

6. Foreign Buyer Ban to remain a contributing factor to softness

7. More homeowners potentially ‘trading up’

8. Rental yields to continue to rise

9. Residential building consents to flatten off

10. Buildings insurance to come into starker focus

In terms of the prediction of more homeowners potentially ‘trading up’, Davidson believes they may take advantage of the subdued market, especially in Auckland, to get a bigger or newer property, or in a better location.

"This will of course depend on not already being at the limit of their borrowing capacity."

And in terms of building insurance becoming a bigger issue, Davidson says this will "come into starker focus", especially given the issues already seen in Wellington with changes to pricing methods and big increases in premiums.

"This will have implications for property values, especially apartments, and needs to watched closely – not just in Wellington either."

30 Comments

"Rope, give them more rope..."

Yes, well this would be entirely consistent with recent Central Bank behaviour around the world.

Totally abrogate their responsibility to Financial Stability in favour of extending the business / credit cycle well beyond its natural / undistorted limit.

I don't know how/why CoreLogic would have the inside word on this though.

Seems like mischievous / wishful thinking.

nobody wants the blood on their hands so its a "we must do something....... anything!!!" situation

.

In the months and years ahead, the RBNZ are no doubt going to reverse most (if not all) the speed limiting restrictions as they try and prevent sliding house prices infecting the broader economy. We have no control over the shed load of weakness that's about to be exported to our shores, by way of reduced demand for what we produce. It's worth noting the RBNZ now openly points to the need to arm itself with unconventional tools, mandating the increase of banks capital and a negative OCR. It gives a pretty good indication the consensus is that asset prices are soon heading down in a more broad like fashion and probably in an unusually extended Japan style way.

When will the property bears realise that property is the safest investment that investors can have.

Stop,trying to continually talk negatively regarding property, when you really know that you should have invested yourselves in property.

Property investors are providing a necessary service to many and without them there would be far more struggling!

It doesn’t matter what any of the property bears say in trying to crash the property market, because it isn’t going to work!!!

Being jealous of people whether it be property investment, business or whatever is not beneficial to your own lives, it will just make you more negative.

What I sincerely suggest is to become more financial yourselves by investing wisely.

Not talking about the Auckland market, buy positively geared property with upside and you won’t go wrong!!!

"become more financial yourselves by investing wisely."

rollingeyes.gif

I'm not jealous of anyone.

And I have "become more financial" and invested wisely - BCom, CA, CFA.

Tell us your story, how did you "become more financial"?

And I still think, if this is true (which I question), that it poor judgement by the RBNZ to reduce LVRs at this point in the cycle.

Tell me, with all your 'more financial' brilliance, why is it a good time in the cycle for a Central Bank to loosen restrictions on leverage?

I agree with you. The housing market is tipped to collapse as a result of macroeconomic trends, domestic and global. Loosening LVR restrictions in an attempt to keep the housing market alive for a little while longer risks inflating the asset bubble even further before it ultimately pops.

Remind me how it ended the last time a central bank reduced lending restrictions to push more unqualified people into home ownership!

"It doesn’t matter what any of the property bears say in trying to crash the property market, because it isn’t going to work!!!" TM2, your comment reads as though ones ideology is now under real threat. The Speculandlording herd made this market what it is today. No matter what myself or other "DGMs" say, it's all heading down regardless. My mission here is to warn first time buyers that they risk destroying their financial future by providing greedy speculators a graceful exit at current prices. Only a blind besotted fool buys at the top.

Disclaimer "I've also amassed wealth on my Central Auckland property. The difference is I'm not stupid enough to rest my finances speculating on its future value"

I agree that investement in property is good and one should invest but not at this level when the bubble is being deflated and the process is still on.

Buy but wait and watch.

Unfortunately, I think you may be right

we are turning japanese...

I don't understand, the graph shows the average property going down, but point 2 says

2. Average property values still rising but in a restrained fashion

The % change is going down. For Rest of NZ, heading towards 0. For Auckland, already below.

But potentially its correct that the average values are still seeing a >0% change, i.e. rising

I don't think lowering LTVs provides any relief at all. If LTV ratios remain where they are buyers aren't chasing the market ~ the market will need to come to them as it's a question of affordability.

LTVs are set as they are for good reason ~ protect the public from bank bailouts if things go pear shaped and protecting borrowers from over leveraging.

Its seems incredibly short sighted to adjust policy when the only effect will be to support property prices, exactly the opposite of what's needed for FHBs.

I am sorry to disappoint many of you, but most seasoned property investors are doing very nicely at the moment!

Speculators in Auckland not so much, but then they have probably done pretty well over the past few years.

we are not speculators at all, we buy positively geared property, under value and with upside, and this method has and will always work!

You can bemoan property investors as much as you want and hope that they go broke, but you are wasting your time.

Interest rates are as cheap as chips and will remain so!

“The Man” predicted that rates would remain low despite many on here stating that they were goingg to rise to 8 or 9:% a couple of years ago!

What I suggest many of you to do, is to get alongside a successful property investor and tap into their knowledge!

Term Deposits won’t even keep up with inflation, shares are very volatile and in the future will get a hammering!

Stay on topic.

The NZ property market is so fortunate to have Nostradamus investing exclusively in this one asset class when he could have been earning (almost) infinitely more money elsewhere.

cmat, prey tell where you believe that I could’ve made more money elsewhere, that was legal?

In the bond market. Heard of it?

It's just a small thing - US$100-odd trillion market (yes, actually, that's not a made-up number).

If you can pick interest rates then it's the place to be.

You're 'more financial' though so probably all over it.

Lol, the man hasn't got a clue. To describe this dude as a one trick pony would be criminally unkind to the pony. Incidentally my long bond position is performing quite nicely too :)

So what have been the returns you have been making on these bonds?

Have you been able to borrow money secured by these bonds with no money down?

I would be surprised if you have made more on bonds that I have on investment property in the last few years, without having to shell out any

Money?????

You can access margin accounts for Bond trading (you know that though).

If you're as good as you say you are at predicting interest rates, you could have made almost limitlessly more than in NZ investment property.

*If* you're as good as you say you are, obviously you are.

And *if* you know what you're doing, but you're 'more financial' so obviously you would.

I mean NZ Property is obviously ah-mazing if you, the smartest person in the world, is invested in it.

But I just wonder why I've never heard of billionaire NZ property slumlords, but lots of billionaire bond traders?

I'm calling your bluff. Yes there have been solid capital gains on most fixed income instruments over the last 12 Months but I doubt very much you were leveraged and on it. There are no billionaire bond traders either (maybe a few fund managers). 95% of the people I know who I consider financially successful did so from property. I personally couldn't care less what you do with you money, in fact stay well away from property, but you are in denial if you don't believe property is a good investment.

My bluff?

I don't know how you can call my bluff when I've not claimed anything.

I'm invested in the Bond market, but never said *I* was leveraged.

My point is only that TM2 obviously thinks he's a financial genius who's amazing at predicting interest rate movements - why not really put his money where his mouth is and make real money in the bond market where you live and die by how well you predict rate movements.

To say there are no billionaire bond traders is hilarious and quite how you delineate bond traders from fund managers (i.e. by definition, those who trade in equities and/or bonds) is interesting.

Quelle surprise that the only people *you* know got rich from property. We're a country of unsophisticated lemmings that buy and sell property to each other, that's not exactly an epiphany to say most people you run into here with money got it from mindlessly buying property with the Bank's money.

I don't dispute that property is an 'OK' investment within a balanced portfolio and on people's individual circumstances.

Property and endless leverage are not appropriate for everyone.

People like TM2 will tell everyone who'll listen that property is the *only* way to go - because it's the *only* way they *know* to go - they've only been benefactors of dumb luck and totally unpredictable loose monetary policy globally. Anyone who says they could have predicted the last 10 years based on fundamentals is either ignorant (most likely), naive, lying, or owns a special DeLorean.

Cmat, I can guarantee that the most successful investors in the world have made more money on property than the Bond market.

Bond market if you are trading is a total gamble and I know several people,e who have gone broke basically trading!

Where there are winners there are certainly just as many losers!!!

Real Estate done correctly is unbeatable and that is why Banks take it as a security first.

Property investors that are successful will have made a helluva lot more than Bond traders and by leveraging so no mo eye being put in.

You get both income plus capital gain!!!

Cmat, I will offer you the same challenge that I have been offering Gordon for many years!

Haha, you're like a fountain of unfounded rubbish.

Not one of those statements can you back up and I'm almost certain you don't even know what a Bond is.

You can get income and capital gains on bonds too Einstein.

It's beside the point.

You wanted to know where you could make more money than property given your unique incredible-amazing skills at predicting interest rates.

Bond market is a total gamble if you don't know what you're doing - but you're the bestest at knowing what interest rates will do.

.

"So Miss New Zealand. If you had one wish if you became Miss Universe - what would it be?"

"I wish.... that the Reserve Bank of New Zealand would establish some kind of lending guidance to ensure most of the credit issued in New Zealand is channelled into productive sectors of the economy, and that we can move away from creating asset bubbles in the erroneous hope that these historically failed schemes will bring us any lasting or stable success in the future. Thank you."

"Well there you have it Ladies and Gentlemen. And if the Governor of the RBNZ is watching, consider yourself put on notice Mr Orr. Even the hot chicks have done their research."

Haha go the man ! You are correct 100% correct the DGM's just can't stomach success, the end is always nigh ! anyone seeing silly statements like that we will become another Japan dismiss stupidity !

Be wise buy under valued, well positioned, spend time improving it, gain valueable skills and keep you rents competitive, pay down your borrowings, a recommend path to financial security as part of your investment strategy.

Don't be silly Shoreman, its to hard for the younger generation, they cannot control their "discretionary spending", probably will need to Google it to know what it even means. A home that you live in is still vital for your financial security in later life, you can still work your way up the property ladder if your prepared to DIY. You don't need to start buying rental houses however, you just need to end up with a mortgage free house by the time you hit 60.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.