ANZ economists say they wouldn't rule out the possibility that the Reserve Bank could actually tighten its loan to value ratio (LVR) restrictions again if the housing market shows real signs of taking off.

The suggestion is in the ANZ economists' first Weekly Focus publication of the New Year in which the economists examine some of the issues they will be closely watching this year.

They say the housing market is "always worth watching".

"...And it’s got the bit between its teeth again. Around the nation, towns and cities are racing to set new records for the unaffordability of housing. Auckland annual house price inflation is back in the black (just), with very limited listings providing the price impetus."

The economists say record-low mortgage rates "are clearly working their magic", and banks have an incentive to try to grab market share in this sector as its relative attractiveness compared to other forms of lending has increased.

The ANZ economists are forecasting annual growth in house prices of 5-6% this year. Other economists, notably those at Westpac, have been saying for some time that there would be a resurgence of house prices and the Westpac economists have a longstanding forecast of price rises hitting 7%.

All this comes not so long after the Reserve Bank had been widely expected to further loosen its LVR restrictions.

At one point the LVR restrictions featured a 'speed limit' of just 10% on new owner-occupier lending at LVRs above 80% of the value of the property. Tough deposit rules introduced in 2016 for investors saw them having to find 40% deposits.

In the past two years (January 2018 and January 2019) the limits were relaxed and are currently as follows:

Investor loans – 30% deposit / 5% of investor lending

LVR lending restrictions are tighter for investor loans due to the higher risks associated with this type of loan. The current policy classifies investor loans as high-LVR if they are more than 70% of the property’s value, and restricts high-LVR lending to no more than 5% of a bank’s total new investor lending.

Owner occupier loans – 20% deposit / 20% of owner occupier lending

This class of loan is for borrowing secured against owner occupied property. The current policy classifies owner occupier loans as high-LVR if they are more than 80% of the property’s value, and restricts high-LVR lending to no more than 20% of a bank’s total new owner-occupier lending.

As said earlier, the RBNZ had been widely tipped to signal further relaxation in the rules in its November 2019 Financial Stability Report, but instead said this:

"...Given the uncertainty around the future trend in housing lending risk, it would not be appropriate to ease LVR restrictions further at this point. We will continue to review LVR restrictions, and will adjust them in line with changes in the overall risk environment."

Clearly the RBNZ was alert to signs then - which have strengthened since - that the housing market is awakening in a serious way.

The ANZ economists say that "on the plus side", a strong housing market supports sentiment and GDP growth.

"On the downside, it’s not the sort of growth we need. Household debt is already very high, housing affordability is already a significant economic and social problem, and house price rises further exacerbates wealth inequality.

"If things really start to get silly, the RBNZ has the option of tightening up LVR restrictions once more.

"We wouldn’t rule it out."

Of course, housing is just one of many things that will feature in the economic landscape this year.

Other things the ANZ economists are particularly looking out for include: watching credit availability, business sentiment activity indicators, the details of the Government’s infrastructure spend-up announced prior to Christmas, and indicators of resource stretch and inflation pressure in the economy.

"Those are the main things we will be watching this year, but as always, it could be that something comes out of left field," the economists say.

"The main theme of our forecasts remain the same: the New Zealand economy is navigating some typical late-cycle challenges that make high speed more difficult to achieve, but as things stand, there is nothing that suggests a derailment.

"That said, global risks resulting from a decade of unprecedentedly easy monetary conditions have not gone away, and markets and sentiment can turn quickly, so to be honest we wouldn’t expect to be able to see that kind of thing coming.

"But while building resilience into one’s business is very important, planning for the worst case scenario at all times will ensure a legacy of missed opportunities. New Zealand businesses appear to be returning to a mind-set of seeking out openings and possibilities, and it’s great to see."

65 Comments

How about we tighten the immigration rules?

Nah...we ain't allowed to have that debate are we. The AUS immigration situation is just as grim..our leaders are so f-up, the msm corrupted by corporate ownership.

Logic tells us that the majority of 'stakeholders' are going to argue for continuance of that which their stakes are held in.

That goes for the advertising-dependent MSM, as much as for the dedt-issued-at-a-keystroke banks. Nobody wants to call a halt.

But it's ponzi - and ponzis tend to call their own halts, This one already did, a decade ago. It's been on steroids since, aided by the ignorance which is called economics - ignorant as in 'of the physical underwrite'. What's the proper price for house in Auckland? The answer is in how much the future can support the repayment, once capital gains (increasing computer-held numbers registered against a piece of decaying physical infrastructure) have run their course.

Nah...we ain't allowed to have that debate are we

Entirely agree, but I guess any modelling of the impacts on the economy due to reduction in immigration might frighten the horses, so best kept under lock and key.

Well a 'narrow' assessment on GDP might.

I am pretty sure a balanced economic assessment of reduced immigration would show benefits outweigh costs.

Well a 'narrow' assessment on GDP might.

Hence the problem. As far as I can see, the ruling elite sees GDP as the "broad" report card of almost everything. And to be honest, with the NZ economy heavily weighted towards consumer expenditure, I understand why the "open the gates" approach is taken. It's the easy option.

Yep.

And beyond sloganeering don't think the wellbeings mean much.

Ministry of Business, Innovation and Employment (MBIE 2019) found no evidence that a higher share of new (international) immigrants in an area is associated with higher house prices.

The answer is NO when you run an immigration economy.

So ANZ economists says: "On the downside, it’s not the sort of growth we need. Household debt is already very high, housing affordability is already a significant economic and social problem, and house price rises further exacerbates wealth inequality"

Well WTF do they expect when their employer is the key enabler of lending money into existence for speculating on house prices and creating the false economy that accompanies it?

Ironic, ey

Couldn't the banks show some initiatave and introduce it themselves without need the heavy hand of the RBNZ.

As far as immigration goes if we can't house Kiwis how are we meant to house immigrants.

No wonder house prices and rents continue to rise.

IMO that would be a good idea. I remember an interview with one of the banks CEOs, and this very point was discussed. I think their argument was that they are in competition with other banks, and if they didn't lend, the others would, and they have to lend to make money. So we do need very heavy regulation in this sector IMO

I 100% agree with that argument and cannot see a bank voluntarily making such a change, as disappointing as it is. Any bank that raises their LVR higher than their competitors, is going to be voluntarily excluding themselves from a large share of the market.

I think that argument is very weak and points to CEO short term incentives creating a musical chairs scenario i.e. if the market rolls over and defaults emerge, then the bank that gave up market share and maintained underwriting standards, while the others pursed growth at all costs, will be the clear winner and shareholders would rightly reward good management. But clearly CEO's aren't incentivised that way, and are only in the job for 5 years so happy to keep dancing and hope that the music doesn't stop before they get their golden handshake. All this points to is regulators having to manage banks rather than the CEOs themselves which is what Hisco (since eased out for questionable practices) effectively said - which can't be a good thing either.

There isn't enough supply, because we have let all these people into NZ, but didn't build houses for them, nor infrastructure for that matter. So their housing needs are encroaching on NZers who have always lived here who also need to buy a house to live in. I think they should have had a policy that for every 2-3 people coming into NZ, a new dwelling needed to be created before that occurred.

Also I thought the Reserve Bank wanted house prices to increase at one of last years announcements. OK, they may not want them to get out of control, but I don't think LVRs make much of a difference, partly because most people who own rentals, actually only own 1, and NZ is full of mum and dad landlords.Very few own 3 or more. Plus a high LVR on a rental means that the landlord is potentially able to rent the house out for less, because they would be borrowing less. Potentially this could help to keep rents down a bit, because the servicing costs on the mortgage will be less, due to it potentially being a smaller mortgage. But longer term, renters will be paying a lot more especially when interest rates do eventually rise. Currently I have done some figures of local houses which would be considered rentals, and the rent would only be enough to cover the mortgage, and not even maintenance. So those property owners would be relying on capital gains, when the prices are already very high.

We are talking about a 650k , 3 brm house, in a small NZ town, and the rent would be about $500 per week.

Because house prices have risen so much, people cash in the bank has effectively less buying power for the biggest ticket item we usually buy, a house. Our official inflation figures on paper be low, but they don't include things like houses, not sure why, but it seems too convenient.

'Renters will be paying a lot more'.

I am not sure it will be 'a lot'. Certainly it's likely to increase, but peoples' limited ability to pay will limit increases like any economic good.

Also further rent increases will make buying more attractive, assuming prices don't boom.

So all kinds of equilibrilising factors at play

I am not sure it will be 'a lot'. Certainly it's likely to increase, but peoples' limited ability to pay will limit increases like any economic good.

You are correct. H'holds run on fixed budgets. Housing costs increase then less is spent into other consumption. Effectively, you're creating a feedback loop as less revenue for business and more resources must be used (promotion and price discounting) to meet incremental sales.

Over a long period it will have to rise quite a bit. But incomes aren't increasing enough to cope with that. I am guessing that raising things like the minimum wage is supposed to also help increase wages across the boards. But where is that money going to come from to allow wages in increase, as effectively it has to also increase inflation, as prices of goods and services have to rise.It is all an equilibrium, because when one thing changes, it also affects everything else. I feel that we are currently caught in this low interest world trap, and having low interest rates aren't really a good thing for many, as IMO it is a indicator of major problems that someone has to fix down the track.

"So those property owners would be relying on capital gains, when the prices are already very high."

That is the game. A lot run at a loss. Great business plan.

I thought negative gearing rules had changed. I guess it depends when you buy in the property cycle if someone is solely buying based on capital gains I don't think that is a good idea, because it is speculating and gambling that the house has been purchased at the right time, and will appreciate a certain amount each year.. Some of the costs are very high,such as insurance, I was quoted about $80 a week. Then rates are another $60 a week. Then maintenance costs could average out at about $60 a week.. That is already $200 a week deducted from a say $450-500 per week rent. It doesn't sound like it is going to be enough to cover the mortgage on a $650k house with a 30% deposit. Renters look like they could be getting a very good deal, and it appears they are subsidized in part by taxpayers who potentially get less tax.

"I thought negative gearing rules had changed"

They have changed for the current tax year to end 31 March 2020. Many part time property landlords who are in loss making, negative cashflow property investments may be unaware of the changes. Their realisation of this may only be in May or June 2020 when they file their tax return and realise that they can no longer offset their property investment losses against other taxable income.

Some with loss making property investments located in Auckland who purchased in the last 3 years, may then decide that in the absence of capital gains in the last 3 years, that property investment is no longer worthwhile.

Well there doesn't appear to be much movement in the NZ housing market at the moment, it's been almost a month and no auction results. Could we see an avalanche of sales in the next few days..? Perhaps then they'll need to tighten the LVR rules.

"ANZ economists 'wouldn't rule out' tightening of LVR restrictions"

Must be joking. People who are buying 1.5 Million or 2 million houses, will it matter to them.

As have been said many time on this forum that to have ROCK STAR ECONOMY - It is imperative that this housing ponzi continuew as also elections approaching and Rock Star Economy is must for JA survival.

FHB are out of Auckland market.

If house price jumps the way it has been in last few moneths even the hope that FHB had to own a house in Auckland is over.

Now all speculatots and so called investor can play buy and sell among themselves or better sell it overseas business / trust set up in NZ

FHB are out of Auckland market.

On what data/evidence are you basing this statement?

What data/evidence? It's all about the feelz. All the data that contradicts how I feel are lies or fake news. I know, because my mates inside my echo chamber agreed with me. Also global warming caused the Australian fires too because warming = fire. My echo chamber mates said so and it feels correct :)

Stev-O,

I would like to think that your post is pure irony. I certainly hope so. On the Oz fires, I came across this. In 2007, Professor Ross Garnaut was asked to produce a report on the potential impact of climate change on the Australian economy. The Garnaut Climate Change Review was published in Sept. '08 and in it he said this; "Recent projections of fire weather suggest that fire seasons will start earlier, finish later and generally, be more intense". "This effect increases over time, but should be directly observable by 2020".

It was of course, totally ignored.

The fact that teachers are leaving the city because they can’t afford, causing shortages of teachers should be a bit of a hint.

Your vague anecdote means little/nothing. I'm sure you don't care, but here is the actual data.

Will be out as how many can afford - what is selling now for 800s goes to million.

Correct stuart786786 - need no data but common sense.

If FHB were struggling earlier to raise 700s to 800 despite such low interest than how will they manage to raise 900 or million unless now they with their family decide to moves to one bedroom from 2 bedroom in Auckland which was already shrinked from 3 bedroom.

This JA government has already acted by confirming the status of tax free heaven to NZ - need say more.

First you said FHB "are out", now you say FHB "will be out". Are you saying that house prices are going to increase by 25% (houses currently worth 800k will in the future sell for $1M), and then FHB will be out of the market?

Anyway, here is the latest data -

That doesn't seem to mention locations in NZ. The OP referred to Auckland FHB

Well then, perhaps OP can provide the Auckland data to back up their claim. And if you think Auckland is bucking the national trend, then I invite you to provide evidence of that ("Auckland is expensive" won't cut it).

Not 25% at the moment but if it continues, will be fast

Definitely houses that were in 800s are going in 900s and 900s in million plus so FHB if not already will be out if this trend continues.

Few houses in mid million plus category which were not getting any interest are now definitely going 10% to 20% above. Though FHB do not compete at that level but this houses are and will lift the overall sentiment.

Wait and Watch.

At the same time, I'm seeing plenty of asking price drops on TradeMe. It's a very strange market at the moment. Still low volumes, and as Mikekirk highlighted, the pick-up seems to have been in pretty distinct bands. Doesn't seem like a very clear picture, perhaps until we see higher volumes of sales.

Where are asking prices dropping? There are a dearth of listings in my area. Putting savings in TDs is proving to be a death of a thousand cuts and we are not renewing but can't find the property to buy.

The real damage occurred in the hyperinflation years of 2012-2017 in Auckland’s upper quartile. Lowering of home ownership rates, and birth rates of the nation’s innovators and entrepreneurs. Doesn’t bode will for the future when you eviscerate the growth engine of the economy.

What you really mean is poverty-stricken local-NZ-citizen FHB's are out of the market

Whereas ....

Fully-cashed-up newly arrived non-citizens with deep-pockets looking to buy their first NZ-house are FHB's

Investor loans are NOT higher risk than owner occupied risks at all!!!!

It is just something that the Banks say rather than it being the truth!!!!

An investment property is always able to be sold and the investor still has his own house to live in!

There is income from rent to fund the mortgage and generally if an investment property needs to be sold it isn’t due to the rental property, but more so a business failure that is secured by the property.

Generally that investment property has been purchased at good fundamentals if the investor is reasonably intelligent.

An owner occupier is reliant on having a job or income coming in to pay for the mortgage on the property and if he loses this then he won’t have funds to pay the mortgage!

Personally I would be more comfortable lending to a borrower for a well bought rental property than an owner occupier.

"Generally that investment property has been purchased at good fundamentals if the investor is reasonably intelligent."

Only if you consider anticipated fingers crossed tax free cap gains as a 'fundamentals'.

If lending for property investment was at the same rate as business lending, which apparently residential investment properties are - a business - the whole game would be a different shooting match. I cant get better than 9% for my business (secured against the business). The whole banking system is so skewed against the productive economy.

Banks like property investment because theyre a neccessity people require and also if the owner can't pay their bills, they have the property as collateral. Given the current housing market, repo'd homes are not too hard to sell on in a mortagee sale

And that is why banks need house prices to continue to rise, because they don't want to be forced to sell a house for less than they lent out, if there is a crash or even stagnation to the housing market. .

"An investment property is always able to be sold"

Residential real estate is not always easily saleable, and is dependent upon market conditions. There are sellers markets and buyers markets. In a buyer's market, real estate could take months to sell if the vendor is unwilling to lower their price expectations.

Have a relative who listed their residential property for sale over 12 months ago and it has still not sold. If she had been time constrained, she would have had to lower her selling price to sell the property. It is all a matter of price - if she lowered her sale price by 50%, then there would likely be interested buyers, and even more interested buyers if she lowered her sale price by 90%.

Is this in a desirable;e location? Or are they just asking way too much for it. The RV is a pretty good idea of what a house is worth. I have found that there are quite a lot of people who list their house, but may not be in rush to move, but as they have time, they list it for a very high amount, just to see if they can get a bite . I know houses that have been on the market for years, some on and off, but never sell.

"Generally that investment property has been purchased at good fundamentals if the investor is reasonably intelligent."

Does an investment property purchased at good fundamentals include an investment property purchased with a negative cashflow?

"Investor loans are NOT higher risk than owner occupied risks at all!!!!

It is just something that the Banks say rather than it being the truth!!!!"

Can you please direct us to some evidence / data to support this assertion?

I see a solution to these issues: just increase the interest rates. The higher they go the less money that will be lent. This is entirely within RBNZ's power given that the OCR is artificially low.

Too simplistic. Would mean even more money sucked from consumer spending and could quite possibly be negative for the wealth effect.

So let's just keeping spending and speculating our way forward on artificially low interest rates. What could go wrong?

Consumer spending takes a hit every time they lower the rate - as it signals a troubled economy, i.e. time to save.

The RBNZ is living in opposite world.

That consumer economy is really adding to the country's productivity. No point letting all the hard work of hoarders going to waste.

The wealth effect is just a state of mind which is separate from actual wealth.

Is there actually any evidence that Lower rates = more spending?

Most consumers items are not purchased with loans.

And regardless of the ocr, credit card or loan rates haven't come down much if at all.

Is there actually any evidence that Lower rates = more spending?

No there isn't as far as I'm aware. In fact, in low-interest-rate Japan, the govt increased sales tax to encourage people to spend today as opposed to tomorrow. However, I think that rising interest rates are not good for consumer spending without more credit and high propensity to borrow.

Newly arrived "princelings" with $ millions at their disposal don't need to borrow

"record low mortgage rates working their magic" On?

Sales in Sept-November are down between 10% and 24% in Christchurch, Nelson and Dunedin.

Sales are well up in Auckland City (+9% in Oct and Nov compared to 2018) and on an improving trend.

Seems like rising prices in non Auckland centres of pop are cutting sales, despite falling rates.

Yet in Auckland this is not so. Question is why?

Yes, incomes are a lot higher for many in Auckland than elsewhere in NZ but is this sufficient info to explain the last 3m improvement? This question remains open

Christchurch at one stage had record house price growth. I wonder why people don't want to live there these days?

People do want to live in Christchurch and is the second quickest growing city in NZ.

More houses being built percentage wise than Auckland I would say!

So much building going on it isn’t funny and has been this way since the Earthquakes, so not sure how you come to the conclusion that loop,e don’t want to live in ChCh, you are totally off the mark there!!!!!

If that is the case, why aren't house prices there rising? The price rises are driven by demand. I am wondering then, if it is still popular, if it is an oversupply of houses in Chch, maybe as a hangover from the earthquakes?

Yes, you are right, there is a lot of building, but that is partly because a significant amount of houses needed rebuilding. Then a lot now are probably needed to be redone as the initial repairs were done in a rush to get people back in their houses quickly. SO a lot of the existing housing stock had to be either replaced, or repaired, which is all building work

ChCh is building plenty of houses and that many new sections have become available

I am actually amazed at how many of these new houses are actually being lived in!

ChCh has the best most stable market for

Both investor and buyers at the moment.

There are a lot of investment and first homes being bought as well as as is where is property.

What I will guarantee is that ChCh is going to be the city of choice in Australasia going forward.

Ozzie is stuffed from the fires and the ramifications are huge for Kiwis living there at the moment.

ChCh is exciting in the future.

Renters will be required to pack into houses like sardines to afford to pay landlords mortgages.

Saying that, it's always darkest before the dawn. Though everything is relative based on your financial holdings/investments.

New Zealand is a bunch of islands and not devided into states like America or Australia, so it's hard to move to a more conduisant municipality.

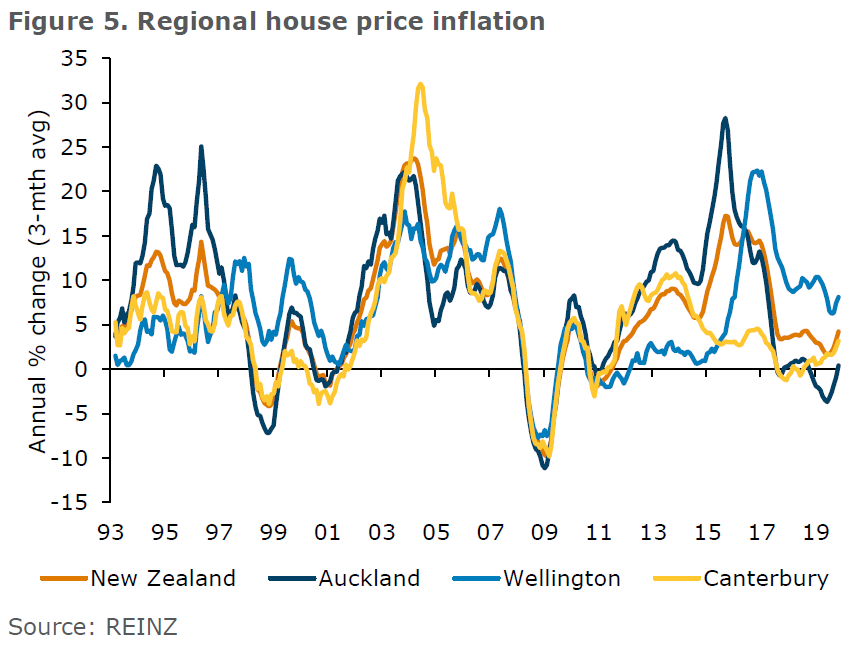

I find that graph really interesting.

Generally speaking, the peaks and troughs across the three main centres and rest of NZ have been strongly correlated.

This is suggestive that its macroeconomic factors, more than local market factors and local supply and demand factors, that are influencing price movements.

I'm alarmed by ANZs view. It's the persistence of income and debt-to-income banks should worry about rather than LVR. Someone relying on investment or rental income is more likely to see their income disappear than say a doctor or miller. If they treat house values as fixed they will find themselves in real trouble when the tide goes out.

Ministry of Business, Innovation and Employment (MBIE 2019) found no evidence that a higher share of new (international) immigrants in an area is associated with higher house prices.

Can’t do that unfortunately. If IR go higher NZD goes higher and out Exports become uncompetitive.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.