Confidence in the housing market has been savaged by the Covid-19 outbreak, with the latest ASB Housing Confidence Survey showing a huge knock to house price expectations over the next year and overall confidence in the housing market falling to a near eight-year low.

And the ASB economists are expecting confidence to fall still further.

ASB chief economist Nick Tuffley said confidence in rising house prices had been "whipsawed" by Covid-19. Perceptions of whether it’s a good time to buy also declined. And interest rate expectations flicked back to "lower for longer".

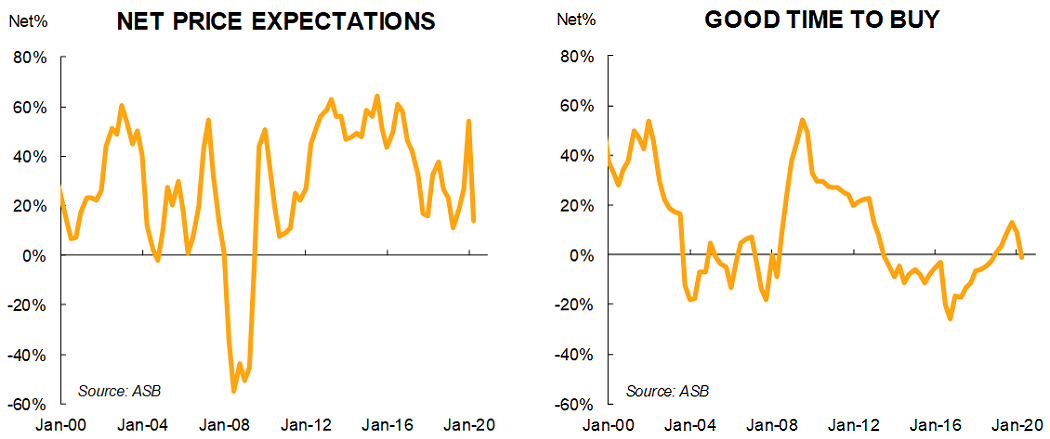

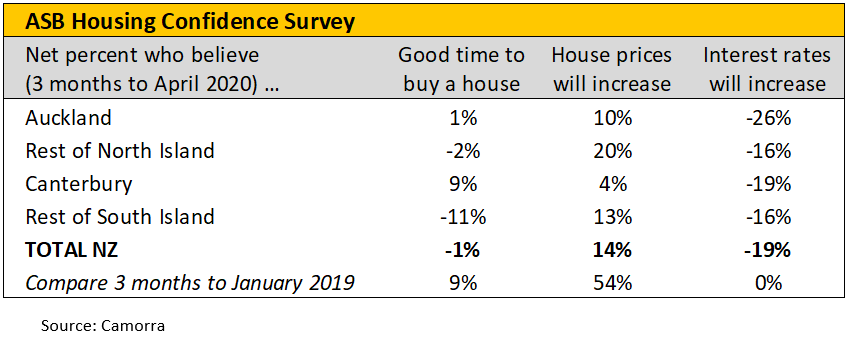

"House price expectations took a substantial knock in the three months to April, with a net 14% of respondents now expecting higher house prices over the next year, well down on last quarter’s 54%," Tuffley said.

"The housing market was literally stopped in its tracks during the lockdown. And respondents will be increasingly aware that there are tough times ahead. Some people are likely to have added concerns about their job security and take a more cautious attitude towards jumping into the housing market. The jump in the number of people receiving income support and mortgage holidays highlights that homeownership conditions are more challenging and that recent price momentum is likely to stall," he said.

Similar to house price expectations, interest rates also took a hit in the quarter, with net 19% of respondents now expecting interest rates to fall.

In terms of house prices, the decline in expectations was by far the largest in the South Island (excluding Canterbury).

"A very high starting point of 65% was no doubt part of the story in the 45 percentage-point drop, and the loss of foreign tourist visitors and flow-on to the Central Otago lakes district may also be shaping perceptions," Tuffley said.

"Auckland experienced the smallest decline, with net price expectations slipping from 42% to 10%."

Meanwhile North Islanders, excluding Aucklanders, remain the least pessimistic on the house price front, with a net 20% of respondents still expecting house prices to rise over the coming year.

Tuffley said that, if anything, the ASB economists had actually expected the falls in house price confidence would be larger.

"Our latest research points to a house price decline of 5-10% in the wake of the COVID-19 crisis," Tuffley said.

"This is broadly similar in magnitude to what we saw during the Global Financial Crisis. Yet during that period, we saw housing confidence collapse to -50%. Either we are too pessimistic, or housing confidence has further to fall. Next quarter’s results will reveal all."

Tuffley said that in terms of house buying sentiment, this "continued to stutter" in the three months to April.

"A slim majority of respondents now believe it is a bad time to buy a house, down from a net 9% saying it was a good time to buy last quarter.

"Perceptions of whether it’s a good time to buy are generally closely linked to housing affordability. With COVID-19 disruptions prompting job cuts as well as slamming the brakes on household income growth, it’s no surprise we’re seeing house buying sentiment take another hit. Further falls appear likely."

Household interest rate expectations were also "whipsawed" in the second quarter of the year.

"Last quarter respondents were split on whether interest rates would rise or fall over the coming 12 months, however this quarter, the 'falls' have it again with a net 19% expecting interest rates to fall," Tuffley said.

In terms of the detail, 14% of respondents expect higher interest rates over the coming year, while 33% expect interest rates to fall. Aucklanders were the most negative on interest rates with a net 26% expecting a fall, compared to just 5% last quarter, he said.

"Government bond purchases, or quantitative easing, are now the [Reserve Bank's] main weapon in the fight to keep economic stimulus flowing. So it’s not that surprising that surveyed participants didn’t expect lower interest rates en masse.

"There may be some scope for mortgage and business interest rates to move lower though, if the RBNZ quantitative easing keeps downward pressure on wholesale rates – as we expect – and credit conditions continue to gradually normalise. But the housing market is likely to feel further pressure over the remainder of 2020."

61 Comments

Thar she blows. Sharpening my harpoon for the hunting season.

Good luck Captain! Well-insulated, affordable houses in NZ are much rarer than white whales.

Hi everyone,

The same sort of negative sentiment was being bandied around about the sharemarket a couple of months ago.

I'm not a close follower of share prices - but it's obvious (even to me) that they've risen remarkably since the trough of a couple of months ago.

We need to be very cautious of surveys of so-called "consumer confidence" and "business confidence"....... They can be fickle and easily mislead.

TTP

TTP - I'm getting the feeling that if you were the captain of the Titanic you'd still be screaming 'full steam ahead' from the bottom of the Atlantic. Forget the icebergs or the cut in the hull, or the water in the bridge, full steam ahead I say.

You can just say fake news..

But TTP, overall the Sharemarket is still lower than what it was last year and way way lower than the peak in late Jan, early Feb.

The RBNZ and multiple governments have worked very hard to make that so.

Aye aye Captain..

Hold fire captain, it's not a whale.. it's someone sunbathing on the beach!

I was expecting a negative result.. but not to be

10 percent expect auckland values higher and of non aucklanders 20 percent expect growth. A few Interest.co commenters seem to be out of step. There are many would be buyers watching and waiting

I think it's more just catch up.

Anecdotally speaking to people in my workplace the realization that house prices are dropping is only just starting to hit.

I also have some FHB friends who are suddenly looking for a home due to the removal of LVR (and little understanding of the current situation).

The psychology of society completely changes when a housing market starts to fall. Suddenly that roof and mortgage becomes a crippling burden that feels like it could break you, especially if your job or income is at risk.

At least that was my experience dealing with Americans during the GFC and their mortgage crisis. Could we see the same here? Yes and it could be worse because our housing market is far more inflated than what theirs was in 2008 (like a lot more).

First home family buyers? then Yes. It's always good time to buy a house for first home family buyers if they really need it. Investors and singles? Maybe not so much. Lets face the reality, investing into houses is not attractive at the moment.

'Lets face the reality, investing into houses is not attractive at the moment.'

Absolutely agree, unless you are able to get a huge bargain - which could be possible in the looming downturn.

Most people are oblivious to what is going on because their focus is not on the housing market or the economy as a whole. Any poll will also included some skewed opinions. Someone pointed out that the quakes west of Levin had around 25 people reporting in Auckland that the earthquake they felt extreme, which means they experienced building damage or collapse of a building. Consider that these are the people that think it's a good time to buy.

10% expect prices to rise.... What about the other 90%?

Don't 8% of people have 40% of our housing debt? Funny that 10% then expect prices to rise.

Thats a Net 10 percent MW. Decliners outweighed by advancers 60/40

It's incredible that the level of comments is so low on a financial site...

This morning at the bank, the customer being served was arranging a term deposit. She along with her 40ish son were asking the most basic questions you can think of. I felt sad for them

Financial literacy here is shocking. But, to be fair a lot of people would have never had the luxury of enough savings to open a TD or understand the benefits of compound interest.

Ah! thanks HW, I stand corrected.

You're very welcome MW

Hi Houseworks,

You're exactly correct.

There's a huge pent up demand for housing in NZ and it's not going to disappear anytime soon...... Thus, it's pretty obvious that relatively small decreases in house prices will lead to relatively large increases in the number of houses demanded.

An economics lecturer I know told me this effect is known as "price elasticity of demand [PED]" and that, in the case of the housing market the PED is "elastic".

I guess "PED" is just a technical/jargon way of saying something that we all know perfectly well. So we don't have to get carried away with economics-speak - we can just use our commonsense.

TTP

The CFO (i.e. head-honcho accountant) of an Auckland company told me that an economist is a person who lacks the personality to be an accountant.

I assume he knows what he's talking about - but neither seems particularly charismatic to me...... Give me a dentist or an undertaker any day.

TTP

I'm just gonna take a wild stab in the dark and say the commentators here might have a higher degree of financial literacy than Joe public....

House prices will be going south no doubt about it at least 20 percent

The best time to buy a house is when you can't afford to buy food.

Hi Becnz,

Actually, I heard that house prices will be going south by at least 21.63 percent.

Where did you get your figure from? Or did you just put on a blindfold and take a stab in the dark?

TTP

The property spruikers know that no matter what the crooked reserve bank won't permit house prices to fall.

They are probably right too. The whole system is rigged beyond imagination.

Only a negative OCR will save the housing market from falls greater than 10-15%.

And it would seem that is not a possibility until late this year.

Savers will be crucified. Debt stackers will be rewarded. We've seen this movie before.

Don't underestimate the depravity of the central banks and the property lobby.

Central banks don't create jobs and that is what we need to avoid economic catastrophe:

https://www.newshub.co.nz/home/money/2020/05/coronavirus-survey-reveals…

I agree, and that's why I've always disagreed with the opinion that prices might crash 25% or more. But I also think that there will be significant property price falls before the RBNZ act to take the OCR negative.

Provided you have job security, we might finally see some relief for FHBs - lower prices and lower interest rates.

I just wonder whether them choosing to do that will lead to violence.

Never attribute to malice that which can be adequately explained by stupidity.

Doom and gloom.

Don't worry, it's not a drop coming, it's a "correction".

Wait till the interest only period is up. Every day hundreds of people are being laid off left and right. That will flow into households holding back on discretionary spending. Latest ASB survey has some very depressed results, especially with respect to houses in the South Island.

Current RBNZ policy suggests we may actually see a rate with a "1" in it.

Trademe insights has Whangarei house prices ALOT lower than pre COVID. Its the start, but much further to go.

This time the fear in housing market is more because house price are highly inflated compare to GFC.

Job and Business loss along with pay cut where not redundent and earning fall in businesses which are still operating is for Real which is bound to impact the overall economy and housing sector could not be immune. 10% to 15% fall in current situation may not create as much mayhem as will, if the fall is much bigger.

Real effect will be felt after few months as for now government stimulus like wage subsidy, mortage defferal....will help to control the speed of the damage that is and will be done as a result of Corona virus.

Yep, and interest rates have much less room to fall... Its going to get Fugly. Was going to happen at some stage anyway (as the OCR was already approaching zero per-COVID), but COVID sure has brought it to a head.

"Real effect will be felt after few months as for now government stimulus like wage subsidy, mortage defferal."

i) Wage subsidy is a 12 week program, so expires in July / August.

ii) mortgage payment deferrals by banks are up to 6 months I believe. That would mean expiry about October.

How many of these people will lose their jobs after 12 weeks?

More than 40% of New Zealand’s workforce is now being supported by the Government’s wage subsidy scheme.

1.073 million people, or 41% of those in employment as at December 2019 (the most recent labour market figures available), are being supported by the subsidy.

https://www.interest.co.nz/business/104453/number-workers-being-support…

Yep the country is on life-support, I wouldn't be surprised if the Government extends the wage subsidy into the new year.. buying some time before they borders can open.

They have extended it for another 8 weeks for those who businesses who need it so that would take it until August / September.

From the RBNZ May report.

The largest fiscal response has been the Government’s Wage Subsidy Scheme, with more than $10.7 billion having been paid to employers by

mid-May. To date, the scheme has helped to cover 12 weeks’ worth of wage costs for 1.7 million employees. An eight week extension to the scheme

is available to employers whose revenue remains low following the move down from Alert Levels 4 and 3.

The psychology on the street is amazing. Huge numbers of people on wage subsidies think their jobs are waiting for them - even when it is obvious that is not true. Relatives are pushing me to buy a house to stay in for ski season despite the huge number of cheap, quality rentals available. Someone boasted to my wife that "jobs are really easy to get in Queenstown!".

Unless people have been personally affected by what has happened they don't believe it is possible. Once reality starts hitting late this year the social mood is going to get ugly.

100% agree. A lot of the sheep are oblivious to the damage that has already occurred, and more importantly at the carnage that is coming.

This just shows how ill informed most people are. It's quite staggering.

You could say that's dangerous. You could also say it's sometimes good to be oblivious...

We are all affected by biases. When you are loaned up on your house, car, boat and TV you have to hope for the best. Option two is that you just throw the bank the keys.

Some people just don't get out much, even less recently. Apparently they are unaware of the 80% of jobs affected in Queenstown.

So many people live in a perpetual state of recency bias. "What it's been like for the past 2/5/10 years will be what it will continue to be like forever!".

I could see this thinking in Jan/Feb when quite a few people I know were heading overseas. I pleaded with them to not go because they are likely going to have to shelter in place if they get stuck somewhere during their trip due to the outbreak. Only one listened and told me later "Thank god you convinced me not to go!". One is still stuck somewhere, the last I heard was UK with extended family, desperate to get home. Another barely made it out of Europe, surprised his trip had to be cancelled.

I am convinced people can no longer predict what will happen tomorrow, let alone in a few months. It's either a perpetual state of denial, an overly optimistic view of the future or the desperate imaginations of simpletons. This applies to our extreme resource draw down and continual wrecking of the environment as well as the current situation. Despite all of that, I still remain hopeful, but prepare for the likely eventualities.

I'm going with perpetual state of denial.

I’ll second that one.

This is a very large drop in confidence but I suspect it still has a long way to fall yet. We haven't scratched the surface of the full economic fallout due to all the short term stimulus the government is pumping out. There will likely be another large drop in confidence once the wage subsidy and COVID-19 income relief package expire later in the year. We will need to wait until summer before we can get a good idea of how things will look going forward.

Perhaps people should stop buying "below market values" because their actions distorted the statistic, especially in CHCH!

Affordable - Ignore Rateable Value!!!

https://www.trademe.co.nz/a/property/residential/sale/listing/264001064…

283 Waimairi Road, Ilam, Christchurch City

A couple of observations:

1) short sales window (trying to create urgency with buyers? or urgency by seller?)- listed 27 May 2020. Deadline expires in 7 days, 3 June 2020

2) Purchased in October 2019 for $465,000

i) owned for less than 7-8 months - so could be property trader seller

ii) vs asking price $619,000

3) CV is $690,000 (which was amended upwards)

This is rocket science , and news worthy, apparently

Well over 20% drop is well possible

I dont think the housing market is elastic at all. It certainly isnt in small town NZ where the market is obviously small and illiquid. The Ak market is obviously more liquid.

To me the question is what effect the flow of new money or invested money out of housing might have even in Ak. We have see new money coming in, in the form of housing investors, migration and the FHBs (population growth). This is an old story. Prices have risen a lot because the stock of houses has not increased enough relative to new loans created to buy them.

It would be interesting to know by how much prices have increased in relation to new loans versus stock. A tricky thing to work out and I dont have the time or inclination. But armed with that knowledge it might be possible to work out by how much prices would fall if flows versus stock reversed. If you could determine those variables.

Sources of flow versus stock reversal are simply the reverse of the inward flows from investors, migration and FHBs relative to the stock of houses including new supply.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.