A chorus of criticism about the effect Credit Contracts and Consumer Finance Act (CCCFA) changes are having on first home buyers may be premature.

Since changes to the CCCFA took effect on December 1 last year, when the Responsible Lending Code was also updated, there've been no shortage of horror stories blaming the new legislation for preventing potential first home buyers from getting into their own home.

Unfortunately most of the evidence offered to support those claims was anecdotal, while the Reserve Bank's lending data up until the end of last year suggests first home buyers more than held their own in the home loan market in the first month in which the CCCFA changes were in force.

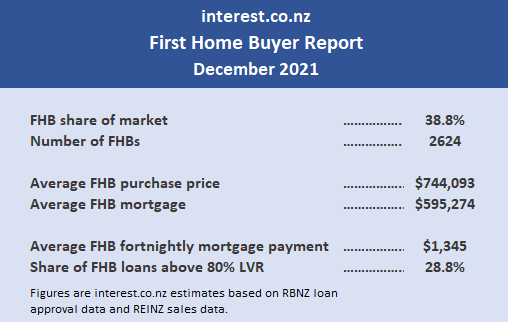

The figures show banks approved 2624 mortgages to first home buyers in December last year, which was down 21% from the 3338 approved for first home buyers in December 2020.

Because the CCCFA changes took effect on December 1 it would be easy to conclude this was responsible for that downturn in lending to first home buyers. But that probably wasn't the case.

Firstly, there was a significant downturn in overall real estate activity in December last year, with the Real Estate Institute of New Zealand recording 6755 residential sales in December 2021, down 29% compared to December 2020.

Secondly, although mortgage approvals to first home buyers were down 21% in December year-on-year, mortgage approvals to non-first home buyers declined 31% over the same period.

To put that into context, the number of mortgages approved for first home buyers in December last year declined 714 compared to December 2020, while approvals to non-first home buyers declined by 7817 over the same period.

At the same time, the number of mortgages approved to first home buyers expressed as a percentage of residential sales was 38.8% in December 2021, up from 34.4% in November last year and 35.0% in December 2020.

What that means is that first home buyers more than held their own in December, both in terms of their share of new mortgage approvals and as a percentage of buyers in the market.

Where there has been a significant decline in lending to first home buyers was in low equity loans - that is loans where the borrower has less than a 20% deposit. The Reserve Bank reduced the amount of lending banks can do to low equity buyers from November 1 last year.

In December last year low equity loans made up 28.8% of mortgage approvals to first home buyers, down from 33.9% in November and 34.7% in December 2020.

So the downturn in mortgage approvals to first home buyers that has occurred, has been at the riskier end of the market, which is probably not such a bad thing, because the average amount being borrowed by first home buyers and their subsequent mortgage payments is continuing to rise.

In December 2020, the average size of mortgages approved to first home buyers was $505,093 and by December 2021 that had increased to $595,274, up by $90,181 in 12 months.

That, combined with recent rises in mortgage interest rates, has pushed the estimated amount of mortgage payments paid by first home buyers on new mortgages, assuming a 20% deposit and a 30-year term, from around $1141 a fortnight in December 2020 to $1345 a fortnight in December 2021. That's an increase of just over $100 a week.

So while affordability is undoubtedly an issue for many potential first home buyers, the causes are much more likely to be high house prices and rising interest rates rather than the CCCFA.

However it's still early days in terms of the available data.

The lending figures for January, due out in a couple of weeks, will throw some more light on the subject and February's figures, which will be based on more robust levels of market activity, will be even more informative.

In the meantime, we need to maintain a degree of scepticism about some of the claims being made about the effects the CCCFA is having on the market and first home buyers in particular.

The comment stream on this story is now closed.

155 Comments

I have deleted your comment Brock because it is way off topic. You'll have a chance to make that type of comment in other articles later in the week. Cheers. Greg.

My imagination has gone wild. Wonder if it was something similar to the meaning of 'like lambs to a slaughter.'

Nah. Just mentioned today's auctions...

thought it was very relevant -- if no houses are sellign at auction -- clear sign that FHB's are not getting suitable levels of approval to purchase -- aka the legislation is having a significant impact ?

Very strange to see - so what if it's relevant to an article later in the week? Surely the author could have just noted that as a reply rather than delete the comment itself.

Perhaps was too risqué saying what could be bought in QLD for the price of the only thing that sold. ¯\_(ツ)_/¯

In defence of Greg, he does mention in both the title to the article and in the the first sentence of the article a little word in the English language that has probably been subconsciously misconstrued by some readers as they desperately wish the article to say something that accords with their deep-seated views on the subject: That little word is "may"; this little non-descript word is called a modal auxiliary and is placed before a main verb to indicate the degree of certainty that the reader should attach to what is expressed by the main verb.

In my experience I have never seen the word "may" used to express a firm certainty; I have only seen it used to indicate a ho-hum possibility.

Nowhere does Greg state that the CCCFA is categorically not having a negative effect on FHBs buying houses.

Greg has merely noticed what appears to be some correlation in the data that catches his attention and floats a possible interpretation of that information. He's not saying it is correct...just that it's a possibility.

And while he MAY well be right, the two lines of evidence he used to make the assumption dont appear to align with the assumption.

While I agree a lot of the feedback around CCCFA has been anecdotal and perhaps cherry picked by interested parties, are you SURE you have proved that above?

Using dropping sales as the reason for dropping new loans seems a little circular. The dropping sales could be precisely BECAUSE of reduced credit off the back of CCCFA changes (which many lenders starting progressively moving to well in advance of the 1 Dec deadline) and higher interest rates.

Also, CCCFA impacts not just FHB but every single borrower, whether moving, topping up or FHB.

No, because every article just claimed CCCFA is bad because FHB were being hit hardest. This directly contradicts that narrative.

Why wouldn’t overall sales overall be slowing when interest rates have increased substantially, LVR’s were reintroduced and prices are very high compared to rents and wages?

It's a bit of all those things. Much higher interest rates are probably having the biggest impact, and they will only go higher, so kiss goodbye to the housing market.

On trademe today 26888 houses for sale over 10500 in Auckland gone up around 6% in a week, with interest rates raising its not looking good for the market if anyone advises you to buy now just ignore them as in a few months prices will be considerably lower.

Yes, if heaven forbid I was a FHB right now, I most definitely would not be buying. Might be some good options come July/August.

Gone up to 26908 while I was posting at this rate it will be 27000 tomorrow.

People are not stupid interest rates raising is a huge concern if you are taking on a million plus mortgage if rates go too 7 or 8% you could lose everything you have worked for over the years. I just feel a bit for the people who have bought in last couple of years because of FOMO.

Most people who bought 2 years ago, like me, will be fine. My property's value has increased more than 40%.

It's more the people who have bought since about August 2021 who might need to worry. They might get in to negative equity, AND have much higher mortgage payments later this year.

Would it be difficult to find out how many people - particularly FHBs - would be impacted?

I don't quite see what is so bad about negative equity apart from a bad feeling. You still owe exactly the same amount of money that you owed before.

You are also in a much stronger bargaining position if repayments become unaffordable because of interest rate increases than positive equity. Here is an example:

Positive equity, house value: $1,500,00 loan $1,000,000 can't make your repayments bank sells your home loses nothing.

Negative equity, house value: $500,00 loan $1,000,000 can't make your repayments bank sells your home loses $500,000 the bank is going to bend over backwards to make sure you continue to pay them. After 3 years buy an equivalent home for $500,000 saving $500,000. Also if the bank starts foreclosing on a large scale that will only drive house prices down further.

But its in the financial sector interest to spreed the fear of the evil negative equity so they don't loose money.

I guess another option could be take your time and make offers with 7-8% rates in mind? I guess sellers will be reluctant to lower prices at this stage, but it'd be nice to see buyers taking their time and not kowtowing to agents and sellers.

I reckon we are still at least 2-3 months away from lowball offers being a strategy worth trying. Waste of time right now, but it won't be soon...

My point was simply that the data presented to highlight "see FHB were hit by market forces, not CCCFA" is not up to scratch. It doesn't imperically disprove the impact of CCCFA on FHB just by saying "see the whole market went down"

I dont disagree that the front page MSM callouts of FHB being hit hardest by CCCFA are patently misguided if they are attributing this SOLELY to CCCFA and ignore rising rates and speed limit changes. Of course, naturally they may well be over-indexed in impact because loans are larger, so servicing tighter.

MisterB, the dropping sales are indeed because of the dropping number of mortgages, not the other way around. You need finance first, before you can settle on a house

feels like a make the numbers suit your narrative type of piece --- right down to using a 30yr term to highlight affordability costs - FHB are significantly down in numbers form last year -- and unlike investors who are driven by returns and a heap of legislation - FHB are always desperate to buy if they can so if they have dropped by over 20% -- thats very significant especially when many investors are in a wait and see mode -- and of course -- where are all the foreign buyers .... Be interesting how long the RE can continue to eat with no sales before they start demanding price drops from sellers !

So housing demand is still here. Surprise surprise. FHB's are still actively buying with some having a 'wait-and-see' approach. Been there done that. I will no longer fall for this trap of "a housing crash" fake news. Housing is a necessity and nothing will change that. Better than putting my hard earned money in 2%pa term deposits. Looking forward to continued steady price growth over the next 5-10 years.

-7

"Housing is a necessity and nothing will change that."... just so I understand, is housing in NZ more of a necessity than in other countries that have (shock/horror) experienced a house valuation crash?

You seem to imply the market can never contract, due people needing houses. Presumably that means infinity and beyond, even with poor wage growth?

Please tell me you're being a facetious troll on this one.

Don't expect a response to this. I'd be far too embarrassed to if it were me.

Sorry who are you? Another cheeky person behind a computer screen who should be working during 9-5, but since the boss isn't looking decided to flipping through screens to post comments that add no value? Just like adding no value at their day job? Great. Another unproductive workforce labourer in NZ. Just what we need to jumpstart our economy again.

No need to respond back. I'd also be too embarrassed if it were me.

-7

I never said markets cannot contract, however the point was if your horizon was zoomed out, you will see that even with all contractions, the growth is always up. Happy to be proven wrong if you can name countries that have "crashed" and has never recovered over the last 50 years.

Wage growth will come as it always has. But it is naive to think that wage growth is the only way to pay for a house in this day in age. If it's not parents financial support, it's side jobs, it's entrepreneurship, it's side investments, and and and.

Have a look at house prices in Japan today compared to 1990, and Ireland compared to 2006.

Their markets have recovered over time but don't think they are generally much above those peak prices, if at all?

Ireland still hasn't got back to the peak, but its now close.

Japan is similar, getting close to peak prices again now, 30 years later.

I guess you’ll be voting Labour given they also want steady price growth. And here I was thinking National were the pro-capitalism party in this country, usually well supported by the property investor types…I’m wrong yet again…everything is upside down and back to front.

No matter which party we vote for, it doesn't matter. It would be naive to think a decision like "electing a party" would really help on anything in NZ. Not what people want to hear, but that's the honest truth.

-7

On this, at least, you are right.

Green Party it is then with rent controls and comprehensive capital gains tax 😂

Thank goodness for interest.co.nz. Instead of regurgitating the PR generated sob stories from mortgage brokers that misrepresent why people were declined for lending, Greg has actually looked at the data and come to unbiased conclusions.

Top work as usual

Wouldn't it be nice if Int.Co became the 'go to' for TV1 etc when commentary was required - and not just to real estate players or Joan from Dargaville.

But the commentary in this specific article isn't especially logical.

Headline: 'Early criticism of the effect credit contracts law changes are having on first home buyers may be misplaced'

Commentary:

'Firstly, there was a significant downturn in overall real estate activity in December last year, with the Real Estate Institute of New Zealand recording 6755 residential sales in December 2021, down 29% compared to December 2020.

Secondly, although mortgage approvals to first home buyers were down 21% in December year-on-year, mortgage approvals to non-first home buyers declined 31% over the same period.'

Question: Not clear how the reducing sales and the fact that non FHB also impacted (who are also subject to CCCFA of course) actually proves CCCFA is not at least a factor?? One could just as easily argue this shows it was a larger factor than speed limits, since speed limits should have hit FHB more but they weren't (I dont necessarily believe that, but just pointing out the same second bullet point could be used to prove the exact point it is trying to disprove)

Miguel, use your brain, lending to FHB has gone down 21% in December, come to your own conclusion

Did you even read the article? The thrust was that the claims in the media that first home buyers were being hit hardest is not backed up in the data. Lending is down across the board, which you would expect when interest rates are rising, LVR restrictions have been reinstated and banks are now actually performing stress tests using real (not fictitious) expenses figures.

Is any of this bad for FHB? No, because it will remove upwards pressure on prices and the data so far shows the impact is not falling disproportionately on FHB.

I suspect you might want to "use your brain" a little more an actually read the article before commenting.

No one is discussing if it's good or bad for FHB (I think the CCCFA is a positive law). I'm making the point that it does reduce borrowing but others disagree!

The future bag-holders, still going strong.

So Stuff can stop making articles about a guy who ate nothing but bread and dirt for the past year but the banks still wouldn't approve him because he splashed out on a chocolate bar*.

(*and is 18 years old and he just quit his job and purchased a $50k car)

The bread one was a shocker... it was NOTHING to do with CCCFA. It was because he wanted to borrow 90%. Banks have limited capacity there, by legislation, and it's all used up.

https://www.stuff.co.nz/life-style/homed/housing-affordability/12764095…

People still look at stuff and harrold?

I stopped looking at them about 3 years ago which was about 10 years after I should have stopped looking at them.

Haha.

Herald isn't great but at least they still have a handful of good journos, and they do have some good guest articles.

Stuff is *really* bad.

Labour want you to live in a house, sorry.. unit.. THEIR unit.

My fellow millennials/citizens are living in a fantasy world if they believe self-described Socialists want higher rates of property ownership.

READ A BOOK

Why read a book when you can watch an "expert" on YouTube.

..best to put -CNN in the search bar after your query or find a better platform..

good.. luck

So while affordability is undoubtedly an issue for many potential first home buyers, the causes are much more likely to be high house prices and rising interest rates rather than the CCCFA.

Says it all really... why is this so hard for some to understand?

I think there are multiple causes, including the CCCFA, but it's less significant than the other causes.

Sorry if I use a bit of logic, high house prices, LVR's and other factors have not changed from November to December 2021, what HAS changed is the introduction of the CCCFA on the 1st of December. The outcome is 21% fewer mortgages made to FHB.

So what is the most likely cause of that significant drop ?… (hint it's not X-mas falling on the 25th)

LVRs restrictions did change Yvil on 1 November...many would of not been able to roll over existing preapprovals... why aren't you crying over this for FHBs? Also your mate Tony says FOMOs gone... it clearly fueld the market.

https://www.rbnz.govt.nz/news/2021/09/reserve-bank-tightens-lvr-restric…

So restrictive legislation is OK as long as it doesn't actually affect anyone? What is the point in it then?

It affects plenty of people and it's a good thing as it IS slowing borrowing!

So restrictive legislation is OK as long as it doesn't actually affect anyone? What is the point in it then?

Its not what the grandparent is saying, if the legislation did not affect anyone there would be no point in passing it. The whole point is to affect borrowing.

Oh no legislation intended to restrict borrowing, restricted borrowing /sarcasm.

Maybe this fear that law changes is adversely effecting FHB was a lie propganded by RE lobbyist as they badly need speculators to fuel the ponzi.

7 sold out of 31 today in Barfoot Auction

https://www.barfoot.co.nz/auctions-live/upcoming

22% Result is bad and if it continues for next few weeks, will be disaster. Normally any dip is short lived as people enter to buy ( buy the dip) but this time it seems that we are in for a long time.

Just heard, how RE Agents are trying to fuel FOMO by creating fear in FHB by saying Buy now before border opens in July.

That's an awful result. The slump has well and truly commenced.

Be patient.

Such an awful selection of properties too! No wonder they aren't selling. These will likely be owned by "investors" who want to cut and dash

Dont talk about auctions, you'll have your post deleted for some reason.

Maybe Auckland is experiencing a few hiccups, but its still booming in the regions with properties flying out the door for crazy prices (de-linked from any previous sales stats - ie: someone names a figure they might be dreaming of, and someone will come along willing to pay it) in the places I'm looking. Maybe Auckland really is now too expensive, and being able to work from home or retirement plans is just shifting the focus of the craziness.

Yes when you look at Auckland prices and the crap you get for your money, the regions and here in Tauranga you get twice the house for the same money. Those now working from home should bail to the regions for better weather and a better lifestyle.

I was down in Tauranga a few weeks ago. It did seem a fairly pleasant, I have to admit. There was a notable lack of diversity and of young people though.

Boomers and bogans on most visits I’m there.

A lot of "car enthusiasts" around...

Neighbourhood watch is mostly just the boomers checking in on the bogans living in the rentals

Brock Landers.Seriously,you don't half spout some shite.

Thank you.

You're welcome.

Once the slump really starts, there is no real estate agents' BS that can possibly keep the Ponzi running for much longer.

Does anyone know if banks are stress testing at 7 or 8% now, rather than 6%?

Banks had better do it already - I do not know about 8%, but mortgages at 7% are a very clear possibility indeed. I would not be at all surprised if it started happening before the end of the year.

Regardless of any banks checks, debtors who already know that they could not cope with this level of interest rates should seriously be thinking about their options.

Yeah. The whole point of stress testing is to test ability to service a mortgage at a significantly higher interest rate than what is available now.

Given many interest rates are at or approaching 5, it wouldn't really make much sense to test at 6, you would think it would be at least 7.

What an astonishing article, mortgages to FHB in December are down a whopping 21%, conclusion: the CCCFA that came into force on the 1st of December had no impact on FHB's being able to get a mortgage… Logic beyond belief !!!

Could just be that higher interest rates and extreme pricing has made aspirational buyers think twice?

Anecdotally, I had zero problems getting approval after CCCFA. But I wouldn't touch this market with a 10ft pole.

Did interest rates or prices get significantly higher between November and December? No, what changed? The CCCFA came into effect on the 1st of December. Outcome: 29% less lending, 21% less to FHB. Conclusion: must be because I cut my left toenails before I cut my right ones...

You can view the steep increase in mortgage rates in the latter half of the year here:

https://www.interest.co.nz/charts/interest-rates/fixed-mortgage-rates

The 21% less is year on year. Not from November to December.

Conclusion: Must be because somebody got out of the wrong side of bed this morning.

Yes, December 2020 to December 2021.

Not November 2021 to December 2021.

Got that Yvil?

Now, not defending Yvil specifically (I personally dont believe CCCFA was the only driver) but the article does nothing to disprove that it was a factor, as it seems to claim.

Month on month (Nov 21 to Dec 21), values were well down - 10% less lending to FHBs, 13% overall... when this time last year they went up (5% and 4%) from November to December. You dont think that might indicate that CCCFA may well have impacted? Lead measures like credit request and approval data also indicate a drop from Nov to Dec and again in Jan (beyond seasonal drops).

Oh, I totally agree. Which is why higher up the thread I said a couple of times that I think CCCFA is of least some significance.

However, I don't think Greg has dismissed CCCFA at all. Rather he has questioned the dominant narrative that it's largely the CCCFA that is killing the market.

Interest rates are much higher in December 2021 than they were in December 2020. And the cost of new build townhouses, which many FHBs have been buying, are also much higher.

You make the valid point though of a significant fall off from November to December (caveat - watch out relying on changes between only two months, as well!).

However, Yvil has fundamentally got things muddled and needs to take a deep breath - the 21% drop is not from Nov 2021 to Dec 2021, as he was portraying it to be.

Makes sense... but it seems like Greg and Yvil might be two sides of the same 'i told you so' coin straying heavily into assumption territory... which is the challenge with reading way too much into a single point. I may well be missing something but for the life of me can't understand how the C-31 stats confirm either narrative.

Side point, if Greg is reading - these are not loan approvals (as most will read), these are "loan commitments", as in documented loans about to draw down...and will actually reflect credit approvals given in the months prior (noting that many banks progressively introduced the spirit of CCCFA changes prior to Dec 1)

Overall mortgages, to everyone, were down 29% in December. Mortgage approvals to non-FHBs were down 31%. You could probably calculate the number of Cantabrians affected and try to claim that the CCCFA discriminates against Crusaders fans, if you really wanted to.

I know of many Cantabrians that are not Crusaders fans. Are we even allowed to call them that anymore?

That's not the conclusion at all, its that FHB have not be seem to affected MORE than other groups of borrowers.

Your living in fairy land Greg, you need to get out more.

Got to the Barfoots auctions in Highbrook like I did today and tell me you think your article is even close to being right.

Do a bit better research buddy before you start printing this rubbish.

Greg's using the actual data, while you seem to be using your opinion of an auction you saw today?

This article is reporting on mortgage data released by the Reserve Bank, isn’t it?

Are you suggesting it would be better if based on anecdotes and vibes?

There could be lots of factors to cause sales drop. It could be raising interest rate, higher inflation rate, US feds hawkish tone, houses becoming extremely unaffordable or tightened lending restrictions. But there is no solid evidence show that it was due to CCCFA. That's why this article argues criticism towards CCCFA has been anecdotal.

Could also be that at some point people collectively go ‘you know what, these houses are overpriced and not worth buying at current market value’.

But then again, this is NZ and house prices always go up so that could never be the case under any circumstances

I see that property spruikers are now getting really worried, coming here to troll...

there was a significant downturn in overall real estate activity in December last year, down 29%

Yep, that is precisely the point of the CCCFA, to limit borrowing, to stop the runaway RE market. How do people not understand that the CCCFA is working by reducing borrowing???

Bit late for the stable door isn't it?

Unless CCCFA builds in accomodations for CPI and wage inflation it's useless anyway.

The CCCFA wasn't put into law to slow down borrowing, it was meant to stop predatory lending. The govt didn't actually realise that it would have this effect. It seems pretty clear to me that the law is having a significant effect on lending. Not recognising the unexpected effects of legislation is not good for governance.

It seems pretty clear to me that the law is having a significant effect on lending

Well you're one a very few. I wonder if people are really that stupid or if they are just totally unwilling to admit being wrong

Maybe it was intended? Putting FHB in the squeeze between rocketing rents and ridiculous house price inflation will ultimately lead to one thing: Predatory lending which is at 8 to 10 times their annual single earner's income before tax.

The surprise will be in Januay's numbers as there will be a lag effect. In December there was mad scramble by FHBs to use their low deposit pre approvals before they were cancelled and not renewed on expirey. So the funnel was emptied. This was though more LOW LVR speed limit driven not CCCFA-what one is likely to see is a reversal if not further decline in FHB share in Jan, Feb and March-typically FHBs servicing generally not an issue. While there won't be a falling off the cliff pull back of FHBs there will likely be a reversal plus more.

The LVRs don't apply to new builds, and in Auckland many FHBs have been buying new builds.

However, while the LVRs will not kill demand for new builds, the soaring cost of construction (and hence sales prices) plus rising interest rates will. And CCCFA could factor in too.

I don't think we should be surprised by a sharp drop off in FHB from this point onwards, pretty much everything is going against them and it will be even worse with rising rates and believe it or not continued house price increases. Lending restrictions have only really cut the tail off but the rest got through just in time. Many FHB now have only one option, wait and watch the market.

Will just wait for the onset of the next recession and wait for the RBNZ to remove all restrictions that are used in normal times to ensure prudent lending takes place..

If a recession is probable then you don’t need to worry about prudent lending so you remove things like LVRs and let everyone have as much debt to speculate with as you like.

That’s how modern central banking works right as the regulator of the banks? If risk is high, the RBNZ removes that risk by allowing more credit to more and worse mortgage holders…or was 2020 a one off that shall never be repeated?

I can imagine it now….we head into a recession later this year and the new lending restrictions from CCFA will be abandoned to protect house prices…can almost script it

Fun factoid:

A state controlled central bank is the 5th plank of the communist manifesto.

Further fun factoid:

The most meaningful things the government have done to slow the housing ponzi have been unintentional (CCCFA, and halting immigration due to covid)

Under rated comment of the article right here.

I hope investors vote Labour in again, I hope they do another term so I can milk some more money out of NZ housing. Thankyou Jacinda!!

Yvil and MisterB is right, the problematic use of data has lead to a wrong conclusion.

Like I said many times, if you can't buy on the way up; you won't be able to buy on the way down.

DGMs hoping for a miserable crash on fellow FHBs to buy it cheap can dream on.

Parents take note, this is the golden opportunity to send your kids ahead in life above the crowd.

There's always a good chance of a higher ROI by investing in your children.

Why would one want to buy on the way down? Only an imbecile would attempt to catch a falling knife.

Imagine if the whole country had the ethos of investing in its children instead of selling them out.

Brock,

I often disagree with you but this is spot on; "Imagine if the whole country had the ethos of investing in its children instead of selling them out".

Sadly, successive governments have failed to provide us with a decent education system.

No government in NZ cann afford the house craziness to stop as this is what is keeping NZ ticking.

Under Jacinda their is no difference between Labour and National as both are working for one goal, only difference Jacinda to silence our critic may throw extra dole, otherwise no difference.

In this scenario, opportunity for smaller parties to rise provided they play their cards well.

CWBW you give everyone a laugh but you come out with bad advice every day.people should just do opposite to whatever you advise to have a good future. If you are buying right now you should go back to asylum for treatment.

You do sound like Retired-Poppy with your daily advice not to buy.

Let's see if you can beat his 4 years record.

Have you taken your own advice and are buying now ? I guess not as it would be crazy so why are giving out bad advice daily? This market is going down end of story you should start buying property on Metaverse.

We are buying and selling every month, regardless of what the internet thinks.

Buying and selling what ? and when you say we who are we or is just your Alter ego. Also you do know internet is not a person.

We, because it's a business and not sole trading.

The opinions on the internet collectively can be singularly classified, therefore the source with reference to its medium is an entity.

Is the world getting a little too complex for you to live in?

Just a little advice if you buy high and sell low the business which is not a sole trader so is it a limited liability company will be a failure ,

Oh well, at least we are getting something decent out of you - tax revenue.

"selling" I thought investors always buy and hodl?

That's why most newbies never make it on the ladder, fail to get ahead in life or make any money- they're too lazy to figure out how making money and investments work.

If you're serious enough to make the property investment business work, you need to have at least 2 business units (not to be confused with buildings) to work.

The first is the rental business which are the long term investments, the second are the flips which are short term turnarounds.

Both are investment with differing time frames.

Pairing them gives you the hedge against volatility on the buy-sell market with the rental market and vice versa. If they can't buy, they will need to rent; if they can accumulated enough money and are leaving to buy, you can sell.

Lazy minds and unmotivated bodies never make money and they will always blame those who are successful for their life circumstances- the world hasn't changed since civilisation.

Who are ‘they’?

Sound like you’re attempting to oppress an enemy - like the poor.

By the way for the record retired-poppy will be correct just 3 year early with predictions obviously did not see pandemic and government making crazy rates cuts.

If only.

What he didn't see does not change the outcome that he had been wrong for more than a thousand days and counting.

Those who bet against him had more than a thousand days of joy knowing what they owned has doubled in value and enjoyment of a home that they can truly call their own.

That thousand days is still adding up as time waits for no one.

Yes one step closer to nirvana for you, one step closer to hell for a large segment of society.

You are obsessed with Retired-Poppy. Seems like they're long gone yet this is the second time I've heard you mention them in the last fortnight.

It's cute.

"Parents take note, this is the golden opportunity to send your kids ahead in life above the crowd." err, 100% NOT what I was saying.

For clarity.. for what it is worth, my views:

1. The fact that FHB fell less than the market is not evidence that CCCFA has not been a major driver. CCCFA applies just as equally to movers, investors and those topping up. All have to prove serviceability on much more stringent terms

2. Evidence in other segments - like credit applications falling off a cliff post changes - indicates that CCCFA is a material impact

3. CCCFA changes amplify impact of higher interest rates, given intense scrutiny on servicing. Interest rates started rising from July/August and July, August were still up on prior year, September and October were slightly down (and September was impacted by Auckland lockdown), so it's not primarily interest rates

4. Greg is right that higher prices have slowed people down, but they have slowed people down precisely because the value of approvals they are getting are necessarily lower due to the impact of CCCFA prescriptive requirements

5. I believe it is a good thing for house prices to come down. People may need to be saved from themselves and ridiculous loans of 6,7,8,9,10+ x income. So, in that regard, if high interest rates, CCCFA and tougher lending restrictions help with that, that's not a bad thing. Will people who splashed out in 2021 be impacted? Sure. But the savings of a much larger portion of people has been eroded.

The end.

The CCCFA is a legislation designed to reduce lending to marginal borrowers, note the words reduce & lending. Then, after the law comes into force, data shows lending has reduced by 29% yoy and 21% yoy to FHB. For some astounding reason, some people then doubt that the reduction in lending may be correlated to the CCCFA...

Calm down mate, you are getting your knickers in a twist.

I don't think anyone has said CCCFA isn't a factor.

Just that it *might* be exaggerated as a factor.

Several things have happened between December 2020 and December 2021 that have influenced the market.

So while affordability is undoubtedly an issue for many potential first home buyers, the causes are much more likely to be high house prices and rising interest rates rather than the CCCFA

From the articled and also quoted by Nifty

I agree he is being too dismissive of the potential significance of the CCCFA.

Everything steams from high house prices... the higher they get the harder it is for FHB's. Simple.

CCCFA hits everyone, unless you're mega wealthy. I suspect this is why Yvil is so upset.

WOW, thank you for finally admitting that the CCCFA affects everyone, including FHB's

Interest rates raising is the main reason for this tumble just the same as when government put emergency low rates prices and sales went sky high not rocket science Yvil. Just to give you a tip house prices are going to fall and if you bought in last 3 years expect to lose your deposit and be in negative equity in next six months the best you could do is try and sale quickly if you are over leveraged. Good luck

DTRH, from your multiple posts above, it is very clear you don't own any properties and you have not made a fortune through real estate. Therefore you are the last person one should take advice from regarding real estate

Interesting Yvil could it be that I am correct and a downward trend is happening and you are probably going to struggle with you little empire as you have only ever seen a upward market. When the market is slumping and inexperienced people like yourself keep promoting it,you need to be called out , you and CWBC have been way out touch with was happening . Myself and many others on here have been warning others that you and CWBW are just pushing FOMO . The market is going down and you have not been listening many times I have said smart investors would already have left the market it’s a shame you are not one of them a costly mistake for you but you will learn we all make them. Now go look at interest rates going up inflation at all time high people over leveraged NZD tumbling and you think market is still trend up you are totally naive.

I do not at all think the RE market is going up, if you were honest you would acknowledge that I have been calling the RE market to have a big slowdown in 2022, long before you.

Exactly. A renter with a pipe dream.

A pipe dream or smoking a pipe?

Might be 80% interest rates, 10% reduced FOMO after the no LVR madness, 10% CCCFA.

Interesting, but Tony Alexander completed a survey for REINZ.

"First home buyers have been hit especially hard by lenders applying new rules contained in the Government’s CCCFA legislation. A record net 65% of responding agents have reported seeing fewer first home buyers in the market. FHB presence has collapsed from November after showing little change for virtually all of 2021".

Therefore, your comment "Because the CCCFA changes took effect on December 1 it would be easy to conclude this was responsible for that downturn in lending to first home buyers. But that probably wasn't the case" perhaps should be treated with some scepticism as it probably is the case by the look of it.

65% of responding agents

Open to self selection bias. While the survey may be true, it's a self selecting set of respondents - it may be that there are some agents who sell one property a quarter are in the pool and are reporting based on the one house on their books. Or it could be the reverse. Impossible to tell so I wouldn't make investment decisions based on TA's survey. It's worth a little bit more than nothing, but not much.

May be, but probably not. That's the point, whatwillhappen.

As an adviser/broker I am seeing the CCCFA having a bigger impact on older clients looking to do top ups for renovations/medical costs/purchasing vehicles etc, these are clients with long histories of paying their mortgage on time (and usually paying more than required) but are getting declined over petty issues, god forbid someone has an afterpay type facility or is helping support their kids while at uni/tech.

Yes first home buyers need 20% deposits at the moment and that has locked a lot of them out but that will swing back around as the banks capacity changes. However if you are older and need some cash for something then you will be in for a surprise next time you ask for a top up.

FHBs don't need 20% for new builds right?

Never ceases to amaze me how often you see those two phrases in the same sentence...

'First home buyers' and 'new builds'. Since when did this become a thing?

Since several years ago when very small, new townhouses built under the Unitary Plan became the only real option for many FHBs.

That's right, the correct sentence should be "Landlords" and "New Builds".

Yep new builds are exempt from the LVR rules however the banks can limit low deposit borrowing still, for example ANZ will normally only lend to 85% regardless (they have tweaked that though) and you still need at least 10% deposit at all of the banks - unless you can find a property that fits the First Home Loan Grant criteria

Not much will change I'm afraid Ken. Not while Directors and Senior Management are personally liable and cannot insure. It's the same with the crazy H&S responsibilities put on businesses, the work that needs to be put in drives up costs and prices everywhere. Unintended consequences and all that. But only unintended, because the intellectually bereft Ministers have no idea what they are doing.

Personal responsibility under the health and safety at work act may have pushed business costs up but is literally saving lives. It concerns me that anyone thinks it is ok to put profits over their workers wellbeing and safety. But hey, everyone else does it so what's the problem? Well now that's been fixed and if it's reasonably in your power to do something about it you must. Yes there is a reasonableness test and that does cover affordability but the bar is now much higher. Thank goodness.

The same stands for for the financial industry. The rot that zero accountability has created to the average New Zealander through irresponsible lending to the housing market is clear for all to see. Directors and senior management get paid how much? And for what if they are not accountable to anyone else other than shareholders. Customers and the NZ public are being abused on a daily basis by their greed, and it needs to stop.

Wouldnt buyers in December have their mortgage pre-approvals already locked in? So they would be unaffected by both the lower LVR requirement and the CCCFA. Its only if pre-approvals are withdrawn or they expire, and new ones are not issued, that the changes will become apparent. Banks have only just started doing this. I have also heard that there was a big rush of buyers in December as they were told to "use it or lose it" (their pre-approval).

Dated 18 Jan: https://www.rnz.co.nz/news/business/459734/would-be-homeowners-face-ban…

"There were a couple of banks prior to Christmas that withdrew some existing pre-approvals, we're hearing stories that some other banks may withdraw their pre-approvals.

"That will be based on how many of their clients that are pre-approved are purchasing at the moment, so if they are close to their cap they are going to have to withdraw their pre-approval if the person hasn't purchased," he said.

If the pre-approval wasn't locked in (i.e. offer accepted on a property and settlement date locked in) then it would have been withdrawn. There was only one main bank doing less than 20% deposits at that stage so it didn't affect a huge amount of people (but very stressful for those that were affected!).

There is always a mad rush in December and the threat of pre-approvals being pulled just compounded the situation.

I can guarantee that the CCCFA changes are having a significant affect on all borrowers and that started late November as the banks started implementing the new rules.

I don't necessirily agree with housing price crashing per se.

Even with a 10% drop , it will only go back a few months, 40%drop will take you back to pre covid.

So those hoping for a bargain are been led astray by so called doomers.

Same doomers who said dont buy few years back to FHB. How many are still waiting after all these years ?

House prices may fluctuate a little bit due to all the factors discussed , but If i had 500k - 1M sitting in my bank I know what I would do

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.