Quotable Value (QV) is warning of more bumps in the road yet for the housing market, which hasn't reached the bottom despite the biggest fall in 2022 for more than 15 years.

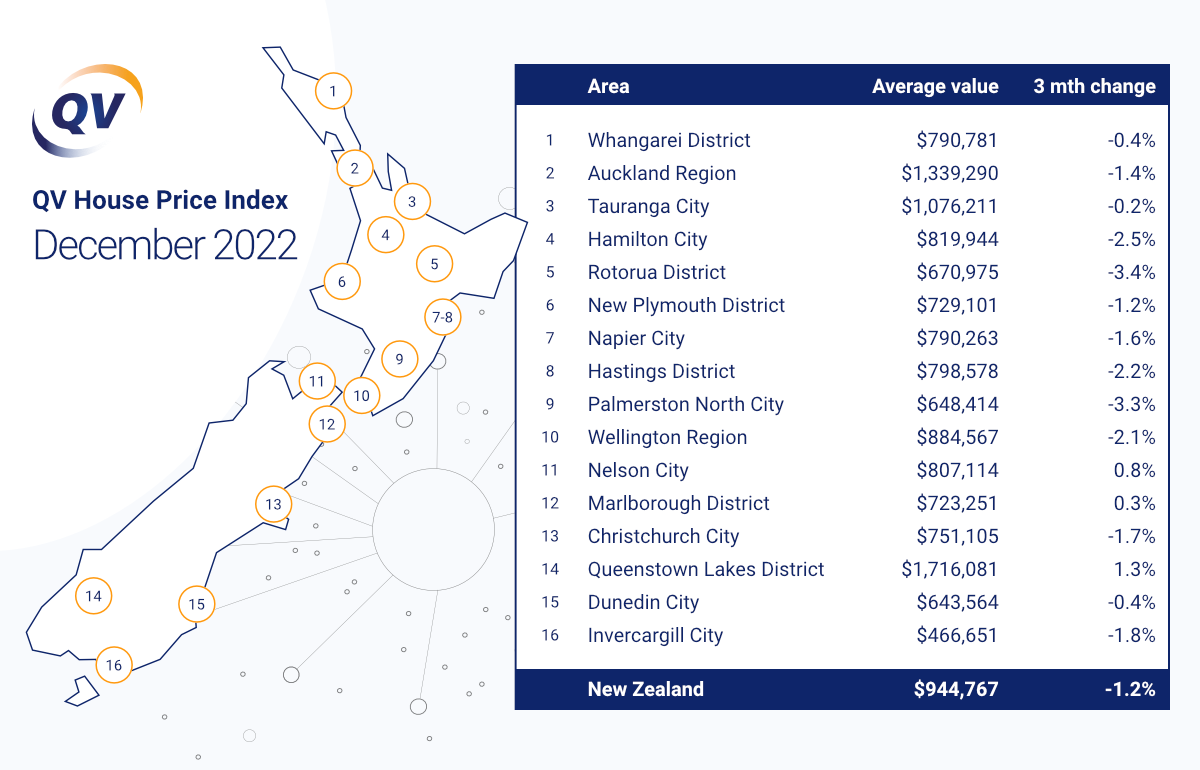

The latest QV House Price Index shows home values fell nationally by an average of 10.3% last year, which compared with increases of 13.3% in 2020 and 28.4% in 2021.

During that period the average home value increased from $724,185 three years ago to $1,053,315 at the peak of the market.

It now sits at $944,767 at the start of 2023.

According to the latest QV figures, from January 1 to December 31 last year, the largest recorded drop in average home value across NZ’s main urban centres occurred in the Wellington region (-18.6%). Palmerston North (-15.7%), Hastings (-13.4%), Auckland (-12.3%), and Napier (-11.6%).

New Plymouth (-2.5%), Marlborough (-1.5%), and especially Queenstown (+5.9%) proved to be the most resilient. The latter saw the only average home value increase across these centres in 2022.

However, QV chief operating officer David Nagel says the market hasn’t bottomed out yet.

"The latest figures show the average home value slipped a further 1.2% on average this quarter, which is a slight improvement on the 2.9% negative growth reported for the November quarter, but not really the usual ‘summer surge’ that we’d expect to see in the run-up to Christmas - and certainly a stark contrast to the last couple of years."

In terms of some of the regional detail, Auckland home values fell further last year than they did in the wake of the Global Financial Crisis.

From January 1 to December 31, 2022, the average home value in the Auckland region went down by 12.3%, compared to a 10.4% average reduction in the 2008 calendar year, which also the last time the region experienced a double-digit calendar year decline. Papakura (-13.1%), Waitakere (-13%), Auckland City (-12.3%), and Manukau (-11.7%) all averaged double-digit declines last year. Rodney (-8%) and Franklin (-9.3%) were the most resilient of the Super City’s former territorial authorities.

Local Auckland QV valuer Hugh Robson said it was predicted that Auckland's downward trend will continue until at least midway through 2023, as it’s been primarily driven by increasing interest rates and the rising cost of living.

"Many buyers are now waiting to see how far sale prices will eventually fall. Some agents have reported that numerous ‘cheeky’ offers are now being presented to sellers, while the number of development land sales has also dropped off considerably, indicating developers are now being very cautious due to rising building costs and declining sale prices."

Home values fell further in Wellington last year than in any other New Zealand city. In the full calendar year the average home value dropped 18.6% to $884,567.

Despite this, the Wellington market still has some way to go before home values are back to pre-pandemic levels. Values climbed by an average of 19% and 25.5% in 2020 and 2021 respectively.

Local Wellington QV senior consultant David Cornford said the rate of decline is slowing, "which could be a possible indication that we’re getting closer to the bottom of the market now".

He said the Wellington market is likely to remain subdued in 2023 and further value declines are expected, particularly as interest rates continue to rise and put further pressure on mortgaged home owners.

"Buyers continue to have plenty of choice and bargaining power in the market."

Nagel notes that it has been a relatively quiet start to the summer, "which hasn’t been helped by some of the atrocious weather we’ve had to endure".

"More significantly, people seem to be taking note of widespread forecasts of further interest rate rises and a likely recession to come in 2023 and they’re now being much more cautious than they have been these past few years. That’s understandable given the outlook."

In terms of the year ahead, Nagel thinks people should be cautious.

"It looks highly likely that we will experience a good deal more economic pain to help curb inflation this year, particularly if a recession does come to pass and unemployment figures start to climb as a result. Increasing interest rates will continue to impact the residential property market, with those who purchased around the peak of the market in 2021 most likely to bear the brunt of that," he said.

"Covid-19 isn’t going anywhere anytime soon, the situation in Ukraine is ongoing, wild weather events only appear to be increasing, and this is an election year to cap it all off. So it’s fair to say that we could well be in for a fair bit more volatility, a few more bumps in the road before things maybe start to level out somewhat in the residential property market during the latter part of 2023."

148 Comments

Remember, folks, “volatile” means up as well as down.

Happy Anniversary Weekend to the good people of Wellington!

TTP

From Investopedia

Analysts watch the direction of market movement when there is a sharp increase in volatility as a possible indication of a future market trend.

Yes, we should be thankful that 2022 was less volatile than 2020 or 2021. Let's hope for another gentle ski slope of a year in 2023.

Well I am hoping for a crash of epic proportions!

It's the only way to remove excessive greed and profits, make things affordable again, clean out the filth, and allow competitive behaviours.

Off course you think Orr, the Commerce commission and the finance Minister would do this... But Alas they are useless.

I agree with you ideologically, but I would argue that it is the constant boom-and-bust that our economy has been through several times in our recent history that has led us into this very mess.

Every crash in the last few decades has widened the prosperity gap between us and our island neighbour, sending planeloads of our remaining skilled workers on a one-way ticket across the Tasman.

What Covid has reminded us of is we may be good managers in times of crisis, but we are awful at rebuilding after the crisis has passed. In fact, we often let minor issues turn into crisis before jumping into action.

Can't even run a bloody bar in this country without navigating through crises everyday 'You name it and there’s a shortage' says stressed hospitality owner | Stuff.co.nz

There is no country in the world that has ever engineered a 'soft' housing crash. And we are falling from a much higher boom than ever before.

What we should be doing now is coming up with a plan to prevent a boom again, and then rise only to a level of stable affordable housing, The fall never hurts as bad if you don't climb too high, to begin with.

But there is no party that has shown a plan/policy that says we won't have a repeat.

Dale,

I dont think there will be a "crash".

A crash requires High Unemployment and very high leverage, with very high debt servicing levels...... resulting in foreclosures.

I'm thinking Banks will try to 'manage " mortgagee stress, like they did back in 2009 and also in the farming sector.

Maybe inflation will raise nominal incomes ( I think 8% in 2022 )... and House prices will start going sideways...with the shitty stuff going lower.

Check these 2 charts and compare today with the 2000s'

https://www.rbnz.govt.nz/statistics/key-statistics/household-debt

ps.. the only solution i see govt doing ...is opening up the immigration floodgates again..... ( which , of course, is not at all a solution )

pps... I very much feel for any FHB who bought in the last 2 yrs....sucked into "affordable" by the RBNZs' ultra low % policy.

I despise our Central Bank and view their actions as ruthless and criminal ( in a moral sense ), as well as ignorant ...

First they fuck savers, often retirees, dependent on income from savings and then they fuck FHBs'.... who are now squeezed into a "zombie existence", of working to simply pay the mortgage.

A bunch of pretenders , hiding behind "Monetary policy" and "Macro economics"....blind to the damage they have done and smug in their hindsight justification of their policy response to covid.....pricks.

It's not only FHB that have a mortgage they can't handle because of rising rates. Plenty of over 50s find themselves with a marriage break-up and consequently a mortgage to re-house themselves. Chatting with a neighbour who has recently put up a for sale sign, the interest rate increases have forced their hand. Being too old now for a bank to look at offering practical help they can only sell up and buy a motor home to live out their days.

It is well known that it takes on average 12-18 months to feel the full weight of each rate increase...the worst is yet to come...hold on tight.

Volatile, from Oxford - "liable to change rapidly and unpredictably, especially for the worse"

Given a Spruikers mentality, it seems the "up and down volatility" TTP alluded to only erupts when they're easily aroused. 😍 Given the current state of play, perhaps "volatile" also describes a sellers mood.

Hi Retired-Poppy,

There’s not much hope for anyone who has to use a dictionary to find out the meaning of “volatile”……

But given your litany of failures here (often joked about) there’s not much hope for you anyway.

TTP

"QV warns of 'bumpy road ahead'

TTP, when inside one of life's potholes, why keep raising your head? 🚙

Like a boulder making its way down hillside

Agree, Juzz. Well spoken.

TTP

TTP advocating for crypto.

I imagine that things will get a lot worse for Wellington when the National government takes the knife to the public service.

In this context it’s a euphemism for saying the rate of decline will fluctuate. But declines will continue into 2024

Indeed. After a decade of over inflation fueled by central stupidity, and speculation behaviour like IO funding, downwards is in ascendency. It's a long way back to yield making sence.

Do the math.

There's certain aspects of property that never make financial sense, because they're tied to aspects like vanity, greed, fomo, etc. Unless those change, it's unlikely they'll find a price level that's purely yield based.

Maybe somewhere in between, but GLHF trying to envisage where that is.

Some people will need to buy and some people will need to sell for a variety of reasons. You can have a cheeky but respectful offer that's well below asking, just like you can have an asking price that reflected market reality 12 months ago instead of now. Hopefully we just see a new normal emerge, although it would be great if wages got the chance to catch-up in real terms for a while even if it meant house prices didn't drop any further in nominal terms.

Any additional wages catchup will continue to propel inflation and thus OCR rises. The ponzi has overshot by some margin and needs a big correction to restore any form of balance.

But let's see what will happen.

It won't though. A huge amount of fixed mortgages will roll over and mop up a decent chunk of whatever else people can manage to get in pay increases. So you're going to have to see some pretty big increases in wages going forward for us to see sustained or even increased demand for goods and services at a CPI level that isn't being driven by price-setting, because it seems business is happy to panic about a wage/price spiral but never seem to take up the option of not hiking prices to sustain it.

If you wage bill is rising to maintain the staff you have, not increasing pricing to cover that inflation can only have one outcome. Bankruptcy.

Probably better if the overpriced assets return to their fundamental values.

I don't consider these 'cheeky' offers cheeky at all. No more so than vendors expecting 30-50% more than a properties CV in the hype of the last two years. As real estate agents often say when asked about how much will a property sell for, "the market will decide".

That's the great thing about an offer - you can always say no. If you need to sell in the next 12-18 months, I would be very cautious about declining any offers being tabled currently. Consencus seems to be around prices declining further and very often the first offer is the best offer.

The monthly HPI renders this stale data as totally redundant.

Agree. QV are a government-funded redundant entity. Last stop on the employment train for the unemployable in the private sector.

The average values were in the range of 740k a couple of years ago and now they are at 940k.

Why would anyone with a sane mind say that it's a drop? In the last two years most of the world was closed, economy activity was artificially boosted and leisure and business travel was at the minimum. Still we are up by a considerable amount.

How can this rise be sustainable? Can an average kiwi make 100k savings over an year after taxes. The house prices are inflated by artificial money pumped into the society by naive policy makers.

I wouldn't call it a drop, crash, correction etc until the average values go below 740k. So i guess nothing to panic about. These are just paper values.

Some might feel the pain but if they were intelligent, could have seen that world is at a standstill so don't jump into the uncertainty.

Being able to sit still is in itself a privileged position and people need to appreciate that.

Pre-Covid prices but adjusted for subsequent income inflation since makes the most sense IMO if you want to call a bottom. Ideally enough downward pressure to keep prices there for a while going forward in nominal terms while real wages increase for a few years. Probably the best outcome at this point.

No. Pre-COVID prices were also unsustainably high. They need to fall back to around 2017 levels to be realistic. I believe they will - by a fairly long period of small monthly falls averaging about 1% a month. There will be pain for some obviously but also significant benefit for many others, esp the young who won’t have to emigrate just to affordable house themselves. This factor alone will be a massive Med/long term benefit for society at large.

The problem with your 2017 theory is the price to make a new house has doubled and it's not going back.

So unless something changes at a fundamental policy level a new house is unlikely to exist for under around 600k (free standing 3 bedroom).

Even the brave new world of off site home manufacturing or imported flat packs seems to be able to lower the construction costs ... yet.

Is there a place for new processing methods Pa1nter

I think the manufacturing needs to be done offsite but you need a total system that integrates all the site establishment and prep.

Plenty of stories of people buying bespoke kitsets or prefabs then getting someone with no experience to install and it costing more than a traditional build.

Property investor here. The only thing that matters to me is the loss of interest deductibility. Interest rates can make up, down, sideways. A lot of owners are going to downsize or lose their properties, but that's normal cycle stuff... you pay the price for not being sensible and not getting advice. In Rotorua the high end suburb of Lynmore is taking a hammering and if you invested there then you must have either done it a long time ago or failed school C maths.

CGT, fine, tax me on a profit, that's fair. Tax everyone else on profits too tho please. The endgame of the deductibility policy is that all rentals will be held through state housing providers and that is not a good outcome.

Relief for tax deduction is good for getting more investors to the market but when those investors sell these houses for huge profits after a few years, then shouldn't they give this tax deduction back to the public coffers and also pay taxes on their profits like every one else?

I know begging is a one way street but for a normal society to function, it needs to work both ways.

That's a CGT you're talking about. Australia has a good model. We should copy theirs.

Look to change your investment model. You can deduct interest if your tenant is the government.

It is a flawed model, both as an investment and politically where the Govt. in power grants certain benefits to themselves as a tenant that they won't give to private landlords and their tenants.

If interest deductibility is good for them, why isn't it good for others?

The short answer is it's the government and they can do what they please.

The longer answer is they can justify it because it's trading reduce tax intake with increased public spending on social housing.

Whether or not the general public has a stomach for less diverse housing is another story.

please explain the meaning of "tax relief" ???????????????????

Common misconception that some sort of magical "tax back" happens in the business of property investing.

All that has ever happened has been paying TAX (full 100% tax as per any other company or business would be expected to pay) on the PROFIT your rental business generates.

Profit = income - operating expenses

(not capital expenses, and in 2011 other genuine expenses like depreciation of building itself also taken off property investors, whereas depreciation is common in all other businesses where the actual asset decays overtime).

Operating expenses for all businesses always includes finance expenses - including INTEREST on money borrowed that is used to generate the INCOME that is being TAXED.

"tax relief" is a wierd phrase.

There is no logical reason why interest expenses should not be allowed when calculating net profit for which tax is to be paid upon.

IRD defines customers receiving income from business (eg, rental property, shares) as an individual. Don't confuse obtaining an income from business as being a business. People derive an income from shares, are they a business too? Or is it income FROM business?

Individual

Customers not registered for GST or PAYE and not belonging to large enterprises (LE) or non-profit organisations (NPO).

- This includes individual customers receiving income from business (eg, rental property, shares) but not registered for GST or PAYE

Simon you forgot to factor in the tax relief in the form of WFF that us taxpayers (who can't claim deductions on their home interest) are 'relieving' to you.

Time to pay the piper.

So coal burning Genesis Energy get "Tax relief" too in the form of the winter energy payments??

Duopoly supermarkets get "tax relief" in the form of WFF too.

Or in the WFF and the many other benefits end inside the local pubs pokie machines - then by your genius logic - the pokie machines and pubs are also receiving tac payer funder "tax relief"

It's pure envy due to past capital gains (which were fake and all being reversed as we speak) that makes rental owners easy targets and singled out by discriminatory laws that apply to them but not the pub, not the local pie and smoke shop, not the local car dealer, not the local knock shop - all seem to get away with being held in high regard while struggling honest hard working accommodation providers get stuck dealing with riff raff entitled tenants who all think we have magical tax breaks and are all multimillionaires without any of the immense effort it takes to be in this business for long periods of time constantly repairing damaged rentals and improving them all the time while all our costs sky rocket and we get hammered the jealous risk-adverse have nots who think investing is putting money into a term deposit scared of taking on any debt or risk or trying to provide any value to others.

Your point is understood - and yeah, given yields have been so very low, and (in a large percentage of residential rental business entities) profitability has been pitiful if not loss-making - it is hard to understand why anyone would put work effort into rental accommodation provision. Yet so many did - so many in number such that for nearly as long as I can remember, first-home-buyers have had to compete with buy-to-let purchasers.

FHBs of course not having the same business/taxation advantages.

That's nuts - for both upwards and downwards market mobility, as well as general market confidence, new entrants in the own-your-own sector have to be the driving force.

Any data that the 15-25% of sales going to investors has this sort of ridiculously assumed impact on prices compared to the 85% of sale going to owner occupiers????????

Your data is wrong, your assumptions are wrong, your conclusions are WRONG.

Yesh except its closer to 40% of transactions going to investors, compared to around 25% FHBs and 30% Movers. So that puts investors at a much larger market share and if you took the top end of property out which is only of interest to movers up, then the investor market share gets closer to 50%. So, yeah, and I said that without bold or underlining.

Here's some data from RBNZ C31, 2014 to 2017. There were 2.5x more investors than FHB taking out mortgages over this period.

Total Lending per month

- FHB Average $656m

- Investor Average $1.6b

Total Number Borrowers per month

- FHB Average 1800

- Investor Average 4700

FHBs are always a tiny portion 15% max.

The vast majority are owner occupiers upgrading and as prices increase they gain equity and can upgrade. On average around every 5 years.

Dumb investors might compete with fhb's but in general what makes a good investment is rarely makes a good first home.

RBNZ C31, 2017 to 2022. Still more investors than FHB taking out mortgages.

Total Lending per month

- FHB Average $1.05b

- Investor Average $1.2b

Total Number Borrowers per month

- FHB Average 2266

- Investor Average 3079

Yes, I've got some data. An apartment auction conducted over the phone due to covid rules had three bidders (auction bought forward and was on the market from the start). One bidder dropped out early (phone call ceased) and I continued to bid up the price 50k with the ultimate winner. The apartment was on trademe for rent within weeks and before the intended settlement date. That investor both raised the marginal price and stopped me from switching from renting to owning in the complex. Investors are shutting out first home buyers and they are raising the prices everyone has to pay. As for your WFF point, I agree. How about the accommodation supplement? That surely isn't just for landlords.

The best solution I see is The Opportunities Party land tax so at least anyone who owns more than they need to live in will contribute to the billions spent supporting those outbid from ownership.

Thanks for sharing your experience. What I like about the TOP housing policy package is not only the introduction of a land value tax, but also the concomitant restoration of tax deductibility for investors in the provision of housing as a business;

- Introduce a land value tax of 0.75% - a small annual tax paid on the value of urban residential land.*

- Remove the current Bright Line Test and allow tax deductibility of interest for landlords, which is replaced by the land value tax.

- Require a deposit of 100% of the value of an existing home when purchased for investment purposes.

- Return the GST on new residential builds back to the local councils to fund further infrastructure development.

- Establish a $3 billion development fund for Community Housing Associations with the goal of clearing the public housing waiting list within its first 3 years of operation.

- Support more urban densification for central cities and transit nodes. Councils will be required to demonstrate that they have enough land zoned for new residential housing in line with the NPS-UD and MDRS.

https://www.top.org.nz/affordable-housing-policy

Not sure about their idea about limiting an investors ability to use leverage with respect to growing their portfolio (I assume this intention is there in order to prevent the unfair playing field with first home buyers).

Alternately, they could have a specific consideration/policy to make renting more affordable.

And in my opinion that can only be done through regulation of the rental housing market - some form of rent control.

Does TOP have any chance of making it to parliament, being in coalition or finally, having their policies implemented. No, no and no.

So they can say whatever the hell they like including this contradictory claptrap

- allow tax deductibility of interest for landlords

- Require a deposit of 100% of the value of an existing home when purchased for investment purposes.

IMO best chance is winning Ilam - Raf Manji is a highly regarded member of the community.

Not a good outcome for you maybe. But the houses won't disappear. Having investors outnumber FHB 3:1 over the last 10 years, outbidding them through generous tax advantages, interest only lending, and no money down deposits hasn't been a good outcome either. That doesn't include the number of people who choose to rent out their first home when upgrading to something new, with the deposit being bankrolled by equity.

You can always be productive, and invest in new builds, if you want to deduct the mortgage interest.

The generally poor quality of the new builds (i.e. the tiktok videos of people doing pre-settlement inspection) of Williams and Wolfbrook townhouses with their bad building design ensures that they will be the next disaster of leaky homes proportions (not saying they will leak, just their poor build design will cause heartache down the line).

Then there's the frustration that people will experience when it comes to painting and other exterior maintenance. Having to get consent of everyone to pay to paint will just be a nightmare.

I would not want to be in the shoes of anyone who purchases one of those shoddy, ugly, and ableist townhouses.

Standalone houses on their own land will hold their value, and will continue to do so. Today's townhouses will not be anywhere near worth their purchase price in about 10 years time.

Well the good news is that the Landlords don't have to live in them. They might be shoddy, but look on the bright side, there are perks such as deducting mortgage interest and the satisfaction of knowing you're providing a net + to housing stock.

Maybe Landlords could insist on a new build design that exceeds building code if they're concerned about the quality?

Hi James Thrace,

That’s a very helpful, insightful post.

You are exactly correct. 😇 Many new townhouses are an accident waiting to happen.

TTP

Even with interest deductability, the numbers simply don’t work for townhouses - regardless whether you are an investor or a FHB

That’s why they are an accident about to happen that will pull down the rest of the market down even further

For proof of this look at the cashflow/top-up required to break even (based on TA’s incorrect prediction of the 1 year rate topping at 5.25% in 2023, then coming down)

https://www.opespartners.co.nz/investment/property-investment/managing-…

Rough numbers at current rates are about $30k a year top-up if it’s even rented

There is such an oversupply coming that Banks will likely stop lending on these once the mortgagee sales start for them

Without capital gains, residential property investment is a mugs game as a poor return on capital

This is going to be an incredibly painful wake up for many new investors, who only calculated cash flow positive at 3% rates.

It's also going to make it very hard for spruikers to spruik residential investment property going forward, I suspect you will see commercial propertyu investment spruiking taking off....

It's also going to be tough for real estate agents taking listings from investor sellors, who have too high expectations re obtainable value, given there will be not many investors to sell too.

It's got PONZI writen all over it. In a 5-6% interest rate world we need property to fall by 50-65% for it to make sense vs term deposits if you get no cap gain.....

Yep, it sure will be - Propeller/Opes/Property Apprentice etc and all the other ‘property investment educators’ have sucked in a whole lot of naive 'Mum and Dad' investors - on the promise of wealth creation and a better retirement income

In reality they will need to work for another 10+ years to get out of the financial hole they are in - if they even manage to keep their own home.

New investors or FHBs are the lifeblood of the market.

Investors simply can’t get the finance to leverage even if they want to, and once FHB's realise it’s cheaper and no risk to rent it’s all over for the Ponzi.

Owner occupiers trading up or down aren't enough to keep the music playing and stop further market falls

New builds are exempt which has certainly had a positive effect on housing supply. There’s nothing stopping you from investing here. The fact that a large chunK of investors are sitting on the sidelines highlights that they were only ever interested in capital gains and thus speculation which the IRD defines as a taxable intent.

The fact that a large chunK of investors are sitting on the sidelines highlights that they were only ever interested in capital gains and thus speculation which the IRD defines as a taxable intent.

Are you sure it's taxable, where do you get that idea. Intention to sell is the key. Buying a property or share to produce a taxable income from revenue would therefore counter your argument.

Stuart Nash as the minister of revenue, made the argument that the govt defines a longterm investor as someone that holds a property longer than 5 years

Just looked at a new build actually. 4.5% gross yield, interest rates 6.5%, rates, insurance, property manager and accounting. I think I worked out the owner would lose $300 pw on interest only. $400+ on P&I. No value add, nothing interesting you can do to develop the section, and supposedly in 20 years when it's time to sell up and retire you'd be trying to sell a ratty old 3 br townhouse with no section and the new owner wouldn't be able to claim interest costs so you'll go backwards there too.

No thanks. I'll stick to buying wrecks on big sections and bringing them back to life, if the rules are changed, if they're not I'll stick to fishing.

If you are young a first home buyer or care about your children then the last thing you want is Luxon and his shadow running things. They will give Investors like nktokyo the advantage of tax deductions of not only mortgage interest but the cost of renovation under the guise of maintenance or as nkt puts it. Bringing them back to life for a tax free capital gain at sale.

I've got no issue with CGT. Made a profit (supposedly or there would be no tax) so it can get shared around.

I wouldn't mind if my house value halved if was good young kiwis. Would you?

I bought my current house in 2021. It's our "forever home". I too am not too phased with large house price falls, so long as we are left alone by the bank to pay the mortgage should negative equity come along.

Maybe my apathy is due to the majority of our equity being gifted by the FHB that purchased from us, so not really "our" money.

I agree. Even if you just care about society as a whole going forward. I see more young Kiwis leaving if National get in. Why stay loyal to a country that is voting to make your hard future even harder so they can continue to make excessive tax free gains?

The loss of interest deductibility for investors has the potential to change the housing landscape in NZ for the better, permanently.

While National plans to repeal it they're not getting my vote back.

If you are a young FHB and don't have parents to spot you a house deposit, you should be boarding a plane.

Luxon wont get voted in lol. Any first year marketing undergrad would be able to work out to run a survey and prove the majority of the electorate want less inequality and affordable housing as priorities.

Its now quite simple for the new labour leader to dump labours unpopular policies, distance themselves from the economic mess and point to National as a party of rich landlords representing the elite property owners... with no policies for lower and middle class

Wlll be another easy win for labour(maybe with one coalition partner)

As a traditional conservative.. i wouldnt vote national as they are too in it for themselves and their mates and will screw everyone else. Would far rather a handbraked crap labour govt until one party finds a proper visionary leader.

Haha - me too. I should be a natural Nat/ACT voter, but haven't voted for National in 30 years, and never for ACT, because I believe they stand for short term gain for those who are already winning, which eventually weakens the economy for everyone.

I don't mind winners, as long as it's not mostly by govt decree.

who under 40 could be encouraged to vote for National, unless the entitled and privileged of course. They are a shipwreck looking for an iceberg. Captain Conehead will steer them there.

Obvious problem is that under-40s don't vote as much as over-40s, ie property owners. It's the foundational problem of our politics. National could promise to feed all renters into a literal mincer and they'd still get the landlord vote. And the average renter would rather dive head-first into that mincer than consider voting for a party with policies that would actually help them...

You under estimate the younger voter . Times have changed. The National party is a relic stuttering into extinction. Keep up the good work .

Younger voters are notoriously under represented in elections. Which is crazy, because they have a lot more at stake.

I still think some sort of social-media connected party where supporters poll for the top policies and those get leveraged in to government via MMP. Young people should be able to get what, 30% of the vote? That'd basically be the keys to the kingdom.

The poll surveys will tell soon enough.

There is a long way to go for the election. when labour replace Jacinda the game will be largely reset -> and polls will shift a lot over a few months as we see the policies shape up.

It sounds like Hipkins will be the likely replacement. he is a smart operator - he will easily get my vote to see what he can sort out... over 7-houses-luxon and his merry band of rich landlords .... all he needs is some better deputies

is there a way to start a case against IRD/Govt for taxing specific assets based off someone's intent and then ignoring others?

It seems the rules and tax law applies for some assets and not others, which is partly why property is where it is in $ values, yet younger gens are stuck having to invest in assets where they get taxed to oblivion in hopes of some investment gains to have a deposit for a first home.

Albert 2020 "The fact that a large chunk of investors are sitting on the sidelines highlights that they were only ever interested in capital gains and thus speculation which the IRD defines as a taxable intent"

You are totally correct! If investigated, the onus would be on the Speculator to prove otherwise: https://www.ird.govt.nz/property/buying-and-selling-residential-propert….

For some reason HW2 and others need repeated reminders of IRD's "intent rule" and its separation from Brightline. Ignorance is bliss.

As future Governments become more desperate to cover black holes, this is potentially a cash cow.

Interesting that the key issue is tax rinsing. My vote this year will be introducing a land tax to ensure tax is actually collected and that it is impossible to avoid.

Imagine TOP getting some clout in coalition. The other polies would be looking at them like they are the Antichrist. haha!

If TOP get in then I don't see their tax switch (from labour to land) being too controversial with a coalition partner i.e. Lab or Nat could implement it and they have the ready-made excuse that they had to due to TOP so no net damage or loss of support to their respective voter bases (would save on working group and consultant costs for butt covering purposes).

A flat property tax, and with that lower the overall income taxes.

Home owner here. If you get interest deductibility then I want it too.

kthanksbai.

That’s why it is so important that interest deductibility is not reinstated for investors. It’s cruel to give investors interest rate immunity while genuine home owners suffer. Property investment should not be classed as a business. Business lending and consequent interest deductibility was deemed beneficial to society as business provide goods and services, hires people and generally lifts society up and moves it forward. Property investment is a leech, it’s a tax. Banks lending credit into existence to allow added competition in the housing market and deprive people and families of their first home is frankly disgusting. Investors seek to destroy the fabric of society and caused so much inflation buy collusion with banks and pumping up our cost of living buy using homes as a conduit for unnecessary and unproductive credit creation. Property investors were implicit in creating this mess so must be subject to the pain of rising interest rates. It’s fundamental.

You are confusing investors with speculators.

And everyone is gaming the system as the system has set up the rules so housing can be gamed.

Buyers are now making 'cheeky' offers, but no more than the 'cheeky' selling price owners were getting over the last decade or two.

All most all buyers want to buy a house as cheaply as possible, but once they do and are now an owner, they want it to increase in value as much as possible.

A new system with a new set of rules needs to be put in place, and the best time to do it, is at the bottom of a cycle.

A new system with a new set of rules needs to be put in place, and the best time to do it, is at the bottom of a cycle.

It's an interesting perspective.

But I suspect any transformational policy change in the urban residential accommodation market will always have perceived winners and losers. My observation is that for many government regulation/policy changes, the already losing lose more with incremental change. So perhaps you are right that a big reset is the way to go.

Keep any eye out as I'm writing an article on regulation of the rental market next week and will be really interested in your thoughts.

If property investment is not a business then its profits are not taxable, the removal of business expenses like interest and depreciation certainly indicate in Govt eyes it as not a business or else Govt is deliberately discriminating against a specific section of society. If you agree then discrimination is OK then look at "Charities like Sanitarium and Maori Trusts (Nga Tahu a property developer and Tourism operator) and either tax their profits or change charitable status to organisations that distribute 75% of net profit to its members or causes and whilst you are at it charge rates on all Maori Land and leave the tribe to sort out who pays.

Yes, it is a mess, all out of whack. They are trying to fix a problem they created by having solutions that are not equitable, rather than just removing the exiting problem to begin with.

Those poor property investors being discriminated against. Their struggles are, as you loosely insinuate, comparable to maori.

Look me in the eye and tell me property investment in this country is not the most advantaged investment class.

If property investment is a business it should be lent money at commercial rates. I borrowed 250k for my business at 7.24%. This was the rate given in March last year when mortgage rates where 3 ish %. My revolving loan (OD) is at 9.75%, I had to negotiate this, they wanted to charge over 11%.

I think you have answered your own question. The fact CGT was backed down on meant some other way of capturing tax on rental property investment was introduced.

Without knowing your circumstances, given the extraordinary increase in property prices over time, surely you would rather have no CGT but be unable to deduct loan interest?

"CGT, fine, tax me on a profit, that's fair" - out of interest were you saying that 5 years ago when Labour wanted a CGT?

I said it was fine and they should copy the Oz model which allows for inflation in a simplistic but workable way.

To me it felt that it flopped because they didn't allow for inflation at all in their proposal. There were big fights within the working group if I remember rightly. Michael Cullen let ideology get in front of common sense.

45.% increase over 2020 & 2021 was never going to be sustainable!

Yes with finance at 2.5% it was petrol on the fire.........

Looks like QV didn't take inflation into account? Isn't the drop in values 10.3% plus the inflation for the 13 months since the peak i.e. ~ 10.3 + 13 x 7/12 = 18%

"which could be a possible indication that we’re getting closer to the bottom of the market now"

Not so certain that we are near the bottom of the market jajaja? IMO, property prices are about to slide like a drive thru.

QV are just another mob heavily invested in the property ponzi. Take any notions of objectivity on their part with a grain of salt.

Yeah - the RE Agents, mortgage brokers, 1roof etc etc will all be claiming the property ship is safe even as its deck disappears under the water.

.. i cant quite understand how anyone would think prices are anywhere near bottoming out when Orr predicts a manufactured recession, mortgage rate rises are imminent for the majority, and globally the economic storms are just starting. There will be less money to go round in the next few years, more unemployment, global conflicts will drag on and grow in number, globalisation will reverse and the ongoing cost to own a house in NZ will increase way faster than incomes - we will end up with a crappy coalition government which wont be able to get anything done and will stagnate the economy in a dangerous time.

Expect another 20% off houses in 2023.

HouseMouse

Another baseless comment in which you are shooting your mouth off which I call you out to justify.

"Take any notions of objectivity on their part with a grain of salt".

QV derive from the former Government Valuation Dept whose purpose was to provide objective valuations most notably for local bodies (RVs) - they continue this role for most councils. A simple objective process generated from recent sales. They provide Registered Valuations which must again be objective as they can be legally challenged with penalties.

As they are principally valuers they have no vested interest to see the market rise or fall.

Do you really believe that Printer8 or do you work for QV?

Did you even read the article?

QV are far from objective - and far from only reporting the facts without personal opinion.

They are fully vested in the buoyancy of the property market and this press release from them is their attempt to spin a narrative that the market will stabilise mid to late this year.

If you didn't know, PR 101 is quote 3 different people in an article having the same personal point of view, to create a clear narrative for the reader.

Simply ask yourself this when you read it - do they sound like facts or person opinion?

Local Wellington QV senior consultant David Cornford said the rate of decline is slowing, "which could be a possible indication that we’re getting closer to the bottom of the market now”.

Local Auckland QV valuer Hugh Robson said it was predicted that Auckland's downward trend will continue until at least midway through 2023, as it’s been primarily driven by increasing interest rates and the rising cost of living.

In terms of the year ahead, Nagel thinks people should be cautious.

"Covid-19 isn’t going anywhere anytime soon, the situation in Ukraine is ongoing, wild weather events only appear to be increasing, and this is an election year to cap it all off. So it’s fair to say that we could well be in for a fair bit more volatility, a few more bumps in the road before things maybe start to level out somewhat in the residential property market during the latter part of 2023."

What I can't figure is how QV is going to respond to RV reviews for those regions where the current RVs were reviewed in September 2021 at the peak.

I have never seen blanket decreases in RVs across a district before. Take Wellington for example, these decreases could be huge if they get re-valued during this downside.

Been watching a WGN property, RV Sept 2021 of $2.03 million - current mid point market valuation is $1.6 million. I suspect for it to sell in today's market it will need to slip back to 30% below RV at a minimum.

I just wonder how banks will respond to such across-the-board value declines, even if defaults on mortgage repayments remain low. Do they reweight the risks of their residential RE lending portfolios -and thus drive up interest rates, regardless of what the OCR is?

I wonder if we have any historic examples of significant de-couplings of OCR from retail interest rates? In other words, is there a possibility that reserve banks start easing quickly without a concomitant response from the retail banks?

Good question. If the banks start provisioning for losses via greater margins then it all bodes ill for leveraged speculative debt

Starting to see some decent provisions in investment banking internationally with traders warned bonus pools will be small this year. Expect to see the big four in NZ take some property hits this year, but i cannot see profits being swallowed by losses in 23..... the profit numbers may well be worse 24.

Already happening.

This is the question, isn't it? It's hard to think there's much leeway in the social license of banks to hold increase premiums over the OCR itself when they've made use of the FLP program to their benefit and also have a track record of large dividends paid to overseas owners.

If we found ourselves in that situation then I think the government of the day would need to make it clear that they will consider legislation to normalise more flexible and favourable mortgage terms than we currently get from our retail banks. Comparing what other banks offer for basic residential mortgages in terms of repayment conditions and options - even during a fixed term - as the result of bigger economics and better competition is kind of depressing. It's going to be a big part of how we help Kiwis get out from negative equity if this all goes seriously wrong and it's a part of our economy that needs serious modernising.

I have never seen blanket decreases in RVs across a district before.

Do you think there is a reason for that. Is it a conspiracy to hold values up. Or more likely, just never happened from one review to the next

Don't know. The previous departmental government valuation office was made an SOE in 2005 and I think the 'automation' of RVs based on recent sales data came in shortly after that. Used to be that every time one applied for a mortgage, the bank required a registered valuation (by a private sector valuer) - which seems not to be the case anymore. Perhaps there is a connection (not sure I'd label it a conspiracy, but...?).

The percentage of properties that were actually traded at astronomical price is pretty small though (figures I've read say 1.95 million residential properties and around 80,000 traded per year).

Most people have been sitting in their houses watching the price go up and the price come down again, makes no difference to them, and if they're smart and have a mortgage they would have paid down extra while interest rates were low so have a nice buffer.

Which is why I've never favoured the methodology adopted with respect to a dollar valuation of properties for taxation purposes. With GIS systems being as sophisticated and detailed as they are today, we could instead assign a numerical value (say on a 1-10 scale) with higher numbers reflecting proximity to public goods (e.g., infrastructure) and common pool assets (e.g., parks and reserves).

The percentage of overall rates that are based on the General Rate (requiring a property valuation to calculate them) is I believe less that 30% of overall residential rates these days. Far more services are provided via a fixed rate, a universal annual general charge (UAGC), a targeted rate or a user-pay rate.

Hence, the distortion of RE market prices that the QV method applies (i.e., all prices go up in value in concert with the - as you say - extremely small proportion of actual sales) has been to my mind a significant contributor to our over-priced land/housing market.

Cannot see any link between CV being a contributor to over-priced land/housing. All Council is interested in is a ballpark ratio between one property and another to apportion rates. They are more interested in the differential between properties, rather than the value per se. As long as they are measuring with the same methodology, the real market value is irrelevant.

You can see this is how they 'really' value properties. In the 'good ol' days' valuers used to look under the floor and up into the attic, to really assess the true state of the building relative to its age. Now many only do a walk-through, or drive around, or just online.

And because of the shortage of supply, the differential in price between properties in need of a big upgrade and a newer property is not as great as it should be, because FOMO makes many people ignore what causes a true differential.

But as demand drops, and regulations change, this is becoming more important, although this is a lagging indicator. For example, because of the legislation for 'healthy homes' only applies to rental properties, not owner-occupiers, most rentals are more compliant than owner-occupiers. So a rental investor should make a price discount allowance on an owner-occupier purchase than they do on an existing rental.

Are they doing this? Are valuers making this distinction?

Cannot see any link between CV being a contributor to over-priced land/housing.

It's got nothing to do with how Council's percieve and/or use these valuations - as you are quite right, the only intent is to redistribute rates on a relativity basis.

All the more reason to just assign a number (from 1-10) and do your relativity (re)distribution once every three years based on that number/change, if you are a council.

But, where sellers of property are concerned - CV is everything. There is no reason why all sections in a new subdivision end up with similar values on a per m2 basis. A vacant section to my mind has no value until someone wants to build an asset on it. Developer/landowners depend on the CV system to put a price-floor on all their sections, regardless of demand. Same goes for existing sellers of properties - CV is everything - (up until now) few homeowners would consider selling a property at less than its CV. I know in the past, we've waited for the re-valuation to click over with respect to the timing of our sales - as not only do prospective buyers accept that number as the price-floor but (our experience is) they willingly bid above that with the knowledge that the valuation will go up with time and seller expectation will be above that valuation.

I could be wrong, as I haven't seen any quantitative research in this area, but I believe QV re-valuations under their current methodology could well be the most significant factor influencing our over-priced market. Our valuation system has been a "go-one-go-all" upwards market re-valuation, courtesy of the need to do this in terms of setting property tax (rates).

People completely misunderstand CVs because they have been misled as to what they mean, especially by people like RE agents.

For starters, developers couldn't care less about CVs unless it is to use them for marketing purposes. A developer is building to a price point for a certain market, and the only consideration he will give to its worth is 1) the price is more than the cost, and 2) since a bank will normally be involved, this price being asked has to be at least equal to what an independent valuer values it at using the methodology they do.

If a developer can sell it for more than what a valuer's 'evidence' shows it is worth, the banks will not try and stop them from doing this just because it is more than the valuation.

And once it has been bought and sold at least one more time by an arm's length (independent of the developer) sales transaction, then this price will become the valuers new comparable.

A bare section has a cost to produce, so has a value, and the infrastructure that attaches to that section still needs to be maintained whether it is used or not.

As a CV is only done every 3 years, it would only equal market value on the day it was done, otherwise, it is up or down as a ratio eg on the day the ratio would be 1:1, and if property prices increase then it would be, say 1:1.2 or if it was to drop would be, say 1: 0.8. There are tables that show this relationship to present prices.

So when prices are rising fast, then FOMO makes people ignore the CV if it is lower, and if prices are falling and CV is now higher, then it makes them think they are getting a better price.

A CV should not be used to assess the real market value of a property, at best it can be used as a quick rule of thumb to give you a rough idea.

Look forward to reading it.

I recall that when I looked at your formula, nothing jumped out at me saying why it couldn't work if some other changes were also implemented.

Other considerations would need to include things like whether depreciation and interest detectability was also included and how much, plus healthy homes regulations etc..

It's part of a package that has to work for both the landlord and tenant.

Thanks, Dale. Absolutely agree. And it is my thought too that depreciation and interest deductibility (i.e., a return to standard business practice/rules) would need to be part of the overall package. My idea/intention is to put buy-to-let (rental accommodation provision) back on a business, as opposed to speculative footing.

I don't see the use of unrealised capital gains as a means to expand such a business activity as a negative thing for society as a whole (that risk is between a business owner and his/her bank) as long as there are rules around retail pricing (weekly rents). It also means that booms in terms of asset price gains become de-coupled from rents (rents instead being 'coupled' to wages/household incomes).

great question, Kate. I hadn't thought about this

Kate

"I have never seen blanket decreases in RVs across a district before".

Yes, Hawkes Bay in 2011 (and I suspect other regions) just after the GFC when most HB property RVs fell by about 5 to 10%. Over the past 50 years I have known times when my RV has been flat or seen a minor decrease (e.g. the1990s).

QV don't respond any differently in a falling market - the algorithms will continue to calculate the RV on the basis or comparable recent property sales.

Quite possibly your observation of lack of district falls is that for the most times over a three year time span property tends to increase - and until 2022 that has been the case for the previous decade.

Thanks, printer8. Good to hear of an actual fall in line with market conditions.

No reason for anyone to buy right now, the recession will smash values down until the market finds a fair price.

I'm surprised at the lack of desperation so far. My previous landlord tried selling our rental in November 2021, took till April 2022 to sell, after dropping the price from 1.3m to 930k. He bought it in 2012 for 400k. We tolerated real estate agents for months and watched as about 10 people in total viewed the house over that time period. Rent was originally 625, new landlord upped it to 750.

It couldn't have possibly been profitable, that is 4.1% yield excluding any costs of being a landlord. It wouldn't even cover the mortgage cost. The property was a very early state house, built in the 1930s with brass doorknobs, native wooden wood used throughout, built of brick. Three bedrooms, one bathroom, double garage in central lower hutt.

I'd buy it for maybe 550-600k, which was slightly above its 2016 RV.

Thanks - a really good bit of actual data/experience with respect to the rental market these days. Supports my opinion that rental market regulation is needed. I'll be writing an article on it next week.

This example is a 20% increase in the weekly rent, despite a near 30% drop in asset price expectation on sale/purchase.

Do you know what the current RV (Sept 2022) of the property is?

Hard luck "my house is my pension" people, you will just have to work forever.

Very Hard for NZers who have a higher % of wealth tied up in real estate then most developed nations. If you have low debt you will still have decent cashflows from rent, but many who believed the spruikers that they could use the equity in thier house to buy a second for retirement are in trouble

Very Hard for NZers who have a higher % of wealth tied up in real estate then most developed nations

That depends. If your economy is based around property transactions like selling / buying; property management; etc, it could be a good argument that wealth be tied up in residential housing. Probably what is important to consider is the contribution to the economy. For ex, the mining sector is a reasonable contributor to the Aussie and Canadian economies; perhaps more so than agriculture to the NZ economy (too lazy the validate).

Also, when you mention "wealth tied up", that's a bit of a cop out. What's happened is the credit has beem created out of thin air to bid up the prices of exiting housing stock. That's not really "wealth" and is really more about monetary destruction.

Lunar New Year tourism hopes wane as Chinese stay home

Lunar New Year tourism hopes wane as Chinese stay home - NZ Herald

V8 been running on 3.5 cyclinders for about 3 years now......

That’s exactly what I said would happy when the likes of HW2, Yvil and the cheerleaders at Granny Herald were getting all excited about Chinese tourism, a couple of weeks back.

I said pretty clearly that East Asian people are generally very conservative about travel, when pandemics and other major global events are broiling.

I said pretty clearly that East Asian people are generally very conservative about travel, when pandemics and other major global events are broiling.

Yes. And spending. See my comment to Guy Trafford's post here.

https://www.interest.co.nz/rural-news/119272/guy-trafford-looks-ahead-h…

Exactly. A point well made.

Looks like there is plenty of ill informed, wishful thinking floating around these days.

Looks like there is plenty of ill informed, wishful thinking floating around these days.

Reports from Bangkok and Saigon from a supermarket shelf price check suggest that discretionary spend getting hammered. The store is where upper-mid to high income shoppers would go. You may be familiar with UK brand Waitrose, a higher priced brand. Many of their products are being discounted 50% to shift stock. Furthemore, in Saigon, domestic brands of higher priced cooking oils are being discounted up to 20% before Lunar New Year. What does this mean? It means that they're also trying to shift stock to meet end-of-year sales targets.

People struggle recognising how long things can take to unfold.

China suddenly opened up what, a month ago, with almost no notice?

It's 6-12 months easy before theres air passenger capacity to move a significant number of extra travellers around. Globally there's already a shortage of pilots, engineers and cabin staff. And requisite airport staff, customs, that sort of thing.

The revival of tourism in NZ is going to be staggered. Coincidentally though, the country appears to be flooded with American, German, and English tourists. The Chinese will be back later in the year.

Do you want a medal ?

me me me squeak squeak

🤣

That single Barfoots auction result today is not going to help the numbers....... 29% below CV on a 2008 built home, looks decent build brick clad so no leaks

is there an article or link to this, keen to read

https://www.barfoot.co.nz/auctions-live/upcoming they make it hard to find....

https://www.barfoot.co.nz/property/residential/waitakere-city/te-atatu-… sold 918k

Not just CV, but:

- Homes.co Estimate: $1.22m

- QV Market Estimate: $1.21m

would have made those numbers nov 21

Daaaamn....29% below recent CV. More like this to come I'm sure.

Thats one of the worst I have seen but again long ownership rated 550k after build, so can take a loss, still not seeing properties selling at a direct loss via auction ( some def by neg)

127 billion of New Mortgage commitments to 406k borrowers April 2020 - September 2021.

Apart from those who just switched banks and did not take any additional debt.

Everyone else has been the victim of a giant rug pull. That's a legacy

Everyone else has been the victim of a giant rug pull. That's a legacy

Well said. Rug pull of epic proportions. No wonder Cindy quit, even if she could easily pass the buck.

Exactly how investors felt when they were getting 0.8% on their term deposits.

If you want to blame anyone blame the realestate industry who told you low rates were here for ever. Blame the the banks who at the time were advising people not to fix for more than a year. Most importantly blame yourselves for your complete lake of knowledge of the history of NZ interest rates.

And in other news, printer8 is back 😂😂😂

Maybe he had committed to returning once Ardern was out of power

HouseMouse

So if I'm back, buckle in and for a starters begin by justifying your baseless slagging off of QV comment above. How about you being objective for a change rather then relying on an inflated ego to slag everyone off.

Buckle in for what? More Vested Commission Muppet drivel about how wonderful the property market is and how rising house prices are so good for everyone?

Please spare us.

Kiwis have been conned for far too long by a crooked industry, and now some people are facing serious financial hardship through only wanting to provide a basic home for their family.

Up 40% in last 2 years

If followed by 30% drop in 2 years….

would roughly mean in Auckland that median was up to $1.35m at peak; 40% off that for starting point 2 years ago gives you $830k

30% off $1.35m will leave median at about $935k

Hence will end up $105k above where we’re 4 years earlier ie in 2020

Diddums

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.