By David Hargreaves

The sharp backing off of investors from the housing market after the announcement last year of the Reserve Bank's new 40% deposit rules intensified over the slow summer month of January.

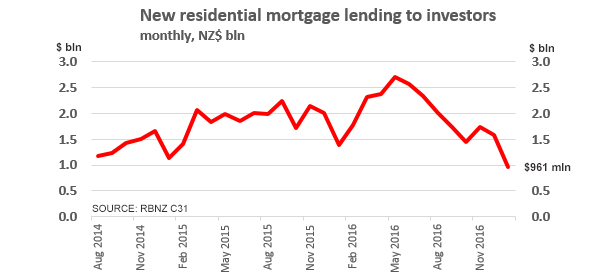

According to the latest lending by borrower type figures from the RBNZ, housing investors borrowed 31.1% less - dollar terms over $400 million less - than in January 2016.

They accounted for most of the over $550 million (14.2%) overall drop in borrowing last month compared with January 2016.

Investors accounted for little more than 27% of the total borrowed last month.

Before the new RBNZ rules were announced in July 2016 investors were borrowing about 38% of the total.

Meanwhile though, the belief that the backing off of the investors may leave more room for first home buyers (FHBs) appears to be coming to pass.

The $462 million borrowed by FHBs in January actually beat the $459 million FHBs borrowed in the same month a year ago.

Borrowing by owner occupiers was at lower levels than in January 2016, but the 7.2% drop was much more subdued than the one seen among investors.

In Auckland the share of investor action was still considerably higher than in the rest of the country, at about 40% ($685 million) of the the $1.71 billion borrowed for houses there.

This, however, was well down on the 48% share investors were taking prior to the RBNZ rule announcement.

The Reserve Bank has been reluctant to talk up the success or otherwise of its lending restrictions so far, and will be waiting for the February/March housing figures before reaching firm conclusions.

It will, however, be happy with the way the steam has come out of the market in recent months.

The debate will continue though as to just how much of the easing in conditions is due to the new rules and how much is down to the fact that banks have been 'rationing' credit and pushing up borrowing rates as they face a squeeze caused by deposits growing at a slower rate to lending.

The RBNZ has been very keen to back up the latest restrictions by getting permission from the Government to incorporate debt-to-income ratios into its 'macro-prudential toolkit', although it has promised it would not use them right now.

However, the Government's now effectively kicked that into touch until after the election by insisting the RBNZ publicly consult on DTIs before going back to the Government and seeking approval for them.

18 Comments

Interesting, yet with migration flowing in at records levels, it will now become home owners driving prices up again.....

We need to remember a lot of people coming to the country generally have a bit of money to sustain themselves, some are coming from stronger economies and they are not just buying a home in New Zealand, they are buying a lifestyle, what price will they put on their lifestyle? Will be interesting to see if Investors creep back into the market in the coming months to facilitate the rental market for the inflow.

Lifestyle ?

Ignorant of what life in NZ is like more likely. Parking money in Auckland RE more likely

Lifestyle compared to India or China maybe, maybe not , depends how much money you have in those countries.

Isn't the "lifestyle" being eroded by mass migration year upon year ?

That seems to be what I see everyone complaining about here !

Yes, Lifestyle NL, things like unpolluted air, beautiful beaches, peaceful country, with plenty of space, freedom of speech, wellfare, ACC, free schooling, etc

Yes, and pretty much the way we'd like to keep it

Any proof of that or are you just making it up as you go along....

Maybe we'll see interest rates fall back a bit.

Wow close to half a billion wiped off credit in one month only for little New Zealand...in a time when we need new homes built...what a shambles...

Hopefully this is a sign of investment moving out of absurdly high cost Auckland to other parts of the country. An improvement in efficiency of production that could result in an increased numbers of homes being produced.

We have record migration yet credit growth has stalled since mid 2016. A shame that the 'experimental ' C16 data was scrapped, it clearly indicated what was about to occur., with all indices going negative in September. January's C31 data is consistent with my view that there has been no pickup in real estate sales in Auckland, for the month of February, and sales will be lower than the month of January. . The small increase in FHB value, could easily be explained by the very fact that prices have increased , and by the increase in Kiwisaver use. We now have Auckland sales listings on both main sites reaching highs, yet we are told there are shortages. My gut , tells me that Barfoots February sales will be the lowest since 2009, and that they are churning listings so quickly to fudge the true market , that they are giving cheese away with every sale. Auckland has grown because of credit growth, what happens if it continues to reverse.

You are definitely not a" Cowpat"

A cowpat is a good thing. Because it is on land, not floating in a stream.

Nice to see intelligent study of Reserve Bank figs on credit growth. As Steve Keen observes, a Ponzi begins its collapse when credit growth ceases to increase its rate of growth, ie stops growing exponentially. This happened to mortgage finance last April 2016. One person on here claims that some FHB increase in borrowing is taking up slack of the $400m drop in "investor" borrowing, in past year. This is irresponsible thinking. FHB will, as in all good Ponzi's, be the last suckers to join party and first to suffer as interest rate rises cripple those with most debt relative to their earnings. The market in is declining and will continue to do so, high migration and housing supply shortage not withstanding. High house prices are a function, PRIMARILY of bank lending and the huge extension of that lending up to 50% of a FHB couple's income, is a recipe for trouble, for them and society. Interest rates are too low and have been for 2-3 years. national does not want the party to end as that will cost them about 2-3% in polls. Now Trump is threatening to raise tariffs on China. NZ over-dependence on Chinese middle class money (through student or company buyers, cash buying) will see a radical drop off. This is not a normal slow down for summer. If something cannot go on, it will stop.

Excellent news , speculators disguised as "investors" were wreaking havoc .

The only building work going on in my neighbourhood is that old houses are being demolished and new big palaces going up. All due to the huge value increases. Does this help? Probably not one iota. Hopefully the council/govt doesn't include these consents in the number of new houses being built that they are crowing about.

Good point, do the 'experts' subtract house demolitions off new house consents to get a net new housing figure? As all brown fields redevelopment will involve getting rid of the existing housing.

No, had it confirmed to me from folk advising New Zealand's banks that New Consent figures are gross, not net, and do not reflect the dwellings lost in the process. They said it's pretty typical for two consents to be for houses replacing one house that was formerly on the land, five units replacing two houses etc.

So the net dwellings being added are lower than the consent figures first suggest.

To me, this makes sense. You now need 40% deposit as an investor... in other words, you can only borrow max of 60% . So naturally, with these rules in place, investors are using a lot more of their own capital instead of debt.

So, if I understand your point correctly, you're suggesting that property investor purchases may not have fallen proportionate to the fall in recorded mortgage lending to investors because said investors may have just made up the funding difference using their other "capital"?

I guess that's feasible but it depends on the methodology of the mortgage stats generation and the source of the "capital" (funds/liquid assets) for your typical investor. On the methodology front, I wonder whether the stats consider the net change in all investor lending - i.e. they'd catch increases in revolving credit facilities on existing properties as well as new lending - or only new lending arrangements. I'd certainly hope/assume the former. In which case if the source of investor capital was leveraging accumulated equity in existing property investments to borrow against - the typical scenario - then the stats would catch this.

The stats would only miss the scenario a property investor uses separately maintained deposits (that aren't aggregated or offset against existing lending so don't affect the mortgage stats) to fund the difference. Given the interest rate differential between deposits and mortgages I'd be surprised if investors maintained sustained non-offset deposits at a level sufficient to fund the differential.

In a nutshell: funding from other sources is unlikely to be statistically significant, so provided the mortgage stats methodology is sound then I reckon the level of mortgage lending to investors is a good proxy for the level of investor purchases.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.