The prospect of a "reasonable correction" in Auckland house prices "grows by the day", according to BNZ economists.

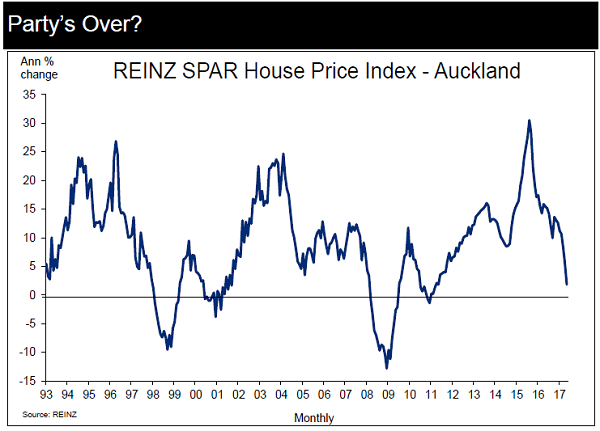

In BNZ's latest weekly Markets Outlook publication, BNZ senior economist Craig Ebert says recent housing market trends show prices, generally, to be going sideways in Christchurch, modestly down in Auckland and up almost everywhere else.

"We expect the [forthcoming] REINZ June data to show more of the same.

"But with Auckland’s large weighting, nationwide house price inflation is expected to fall further."

Ebert said that, importantly, the recent decline in Auckland house prices was now getting significant media coverage.

"This can be self-fulfilling to the extent that folk fearful that a market might correct are more likely to withdraw from it (buyers that is) and sellers will either delist their properties, simply not sell or, if under pressure, accept lower prices than might otherwise be the case.

"Certainly, there is already anecdotal evidence of speculators looking to exit the market for fear of getting burnt.

"All of this can lead to a sentiment-driven price correction over and above what market fundamentals might dictate.

"We still think genuine excess demand will underwrite the Auckland housing market but, equally, the prospect of a reasonable correction in prices grows by the day," Ebert said.

"From a Reserve Bank perspective, housing market developments will certainly play into its 'lower-for-longer' rates strategy."

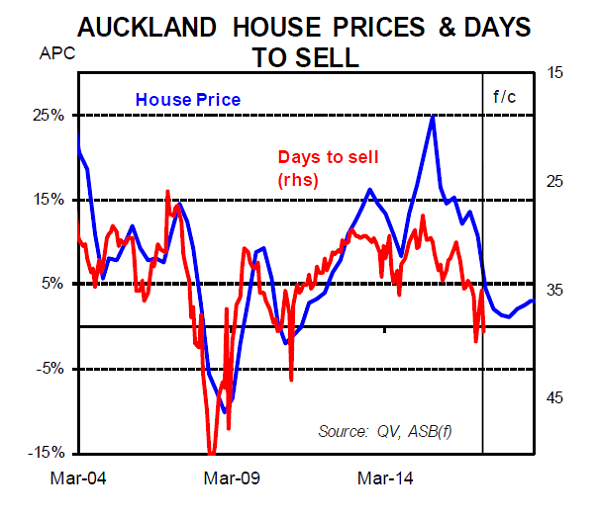

ASB economists say in their Economic Weekly publication that the market is coming in for a soft landing, "one that is well under way in Auckland".

"Auckland house sales turnover has fallen 30% over the past year.

"Yet over that period the trickle of new listings on to the market has been pretty steady.

"These two factors together mean that the number of outstanding listings on the market are up 66% over the past year, according to realestate.co.nz figures."

The ASB economists say buyer demand has tempered in Auckland, for a variety of reasons. Some key ones are: the added Loan-to-Value Ratio restrictions; lifts in mortgage rates, and affordability challenges.

"On top of that is psychology: the more it appears that prices are no longer soaring, the more the Fear of Missing Out evaporates.

"As a market of would-be buyers and sellers, housing is going through adjustments in behaviour. Buyers are being cautious and can afford to take their time.

"Increasingly, we will see the sell side adjust. Some of the people with their homes on the market who don’t need to sell will pull out of the market. Others will become more realistic about the price their home will sell for and move to meet the market. Still other would-be sellers will refrain from listing for the time being.

"We are likely to see a combination of developments in Auckland over coming months. Prices will remain flat or edge down slightly, the number of new listings coming onto the market will eventually slow, and the total number of homes for sale will start to stabilise."

The ASB economists say that due to house price measurement issues (such as Barfoot & Thompson's prices being impacted by compositional changes) they have tended to focus on QV’s quarterly House Price Index.

"The most recent figures released last week for Q1 show Auckland house prices up 0.8% qoq (ASB seasonal-adjustment) and 10.6% higher over year.

"However, as recent data have suggested, the slowdown in price growth appears to have accelerated in Q2.

"As a result, this week’s release of the REINZ’s house sales and price figures for June will be particularly timely.

"Specifically, the REINZ’s new House Price Index (launched April 2017) should reduce even more the impact on figures of month-to-month shifts in sales composition. And given the delay of Core Logic data, the measure is the most up-to-date read on house prices, as it is based off unconditional sales over the one month. In 2017 to date, this index had shown a marginal fall in Auckland house prices and a 0.8% increase for NZ overall.

"On this measure, it is conceivable that Auckland house price growth turns negative in the year to June 2017."

189 Comments

nothing new here. financial markets are built around confidence. talk a market down in the press, and do it often enough, and the likelihood is that price will follow the sentiment. Likewise mention a bank run, and hey guess what, all the sheep will queue up at the atm given the impending crisis.

Well if the Bank thinks media commentary of a declining market will be 'self fulfilling ' then bring it on .

Its not the media's fault , they are simply reporting post the event and taking note of something called "sentiment" which traditionally influences buying decisions .

The market was always going to correct , it just could not continue ad infinitum

Toronto House Prices Crash 192k in just 3 months.

https://www.youtube.com/watch?v=hGL0ysImPCo

Auckland Albany House Prices Dive 13.5%

https://www.stuff.co.nz/business/property/94154549/house-prices-dive-in…

The Mainstream Media keep this very Quiet.

Geeeze, that graph is a rather: "Excel for beginner's" one.

I found the top one pretty interesting actually, it shows shows a repeating cycle and so we are due for a dip. The most important thing to take out of it however is look at the area above the zero as opposed to the area below the zero. Basically it recovers any loss almost immediately and then away we go again. Its kind of a shame that most people here didn't even bother to look at it and just rushed to shoot off their mouths below....

yeah provided the future is a replica of the past. Also with respect to the graph, who wants to start integrating a negative area from the get go? (translation - catching a falling knife).

Hmmm ...don't see it that way this time for a variety of reasons.

Last time the following strategies were employed to kick the can and caused an overshoot of values...

1. Global QE (easy and loose credit..)

2. Global ZIRP (or lowest we've seen in NZ for a very long time)

3. Huge Immigration increase in NZ

So...if we have a global slowdown again these levers are already maxed and not there to pull again.

I was getting over 6% on deposit last time the effluent hit the fan...

What do they use this time?

They'll do the same again. People will lose faith in currency and it'll be a Venezuela style currency collapse. crack up boom hyperinflation but with official denial and hence continued low interest rates. perhaps..?

To be fair to TA (which I dont like to do) .,.. that article is from June 2016.

And it did continue to rise from there. Until about 3 months ago, now we're back down to June 2016 values. ;)

That being said, I do notice in his current weekly wrap up he says

"The challenge for those interested in residential

property is to continue to make sure they do not

get lost in the woods from focussing too much on

the individual trees of price shocks. The

underlying picture for Auckland is the same now

as it was a year ago, five years ago, even ten

years ago."

This does appear at odds with other BNZ commentators, but he is publishing on his own site. How many other bank economists have their own domain name? #GodComplexMuch?

"Party's over" - damn right.

Visited about 15 open homes on Sunday in the Millwater suburb (new area north of AKL) to get some ideas on bathroom renos. Saw about 4 other groups of people in total at the open homes. Most homes had blank visiting logs. One house the agent was asleep in his car with the house still locked up as he did not think there would be any viewers.

Bring it on!

Hardly surprising if Auckland house prices "remain flat or edge down slightly" in the immediate future.

But in the medium/long term, demographic factors will underpin a rising Auckland market.

Love how people will read this article but selectively ignore the bit where Ebert says "We still think genuine excess demand will underwrite the Auckland housing market".

People with no skin in the game can't wait for a crash. Luckily facts don't care about feelings.

"Love how people will read this article but selectively ignore the bit where Ebert says "We still think genuine excess demand will underwrite the Auckland housing market".

Why would anyone ignore it? It could be framed in a number of different ways:

"Based on past history, ......"

"From our understanding,......"

If you really give a hoot about the differences between sentiment and reality, you would need more from KOLs such as bank economists. For example, you would need a rationale and / or understanding of the analytical construct that they're using. You don't have that, so others are no more guilty that you as to the difference between feelings and facts.

Finally, you are a pot calling a kettle black. If Ebert really is a seer, then you would not selectively quote from him. You would quote in full.

"We still think genuine excess demand will underwrite the Auckland housing market but, equally, the prospect of a reasonable correction in prices grows by the day"

IMO, that is little more than weasel words and an exercise in ass covering.

"We still think genuine excess demand will underwrite the Auckland housing market but, equally, the prospect of a reasonable correction in prices grows by the day"

People will ignore the first half of this statement and play-up the second. If I thought they would ignore the whole thing, I would have quoted the whole thing. My point was that they will ignore the first part, so I only quoted the first part.

As for why anyone would ignore it - I think that people (particularly in this forum) resent investors/speculators that have made massive capital gains without lifting a figure. They therefore hope for a crash and cling to any data that might suggest this is coming. All the while ignoring factors such as the massive imbalance between new builds and population growth.

I prefer to rationally weigh both sides of the equation - lower availability of credit, low number of new builds, high population growth, election uncertainty, winter time, high number of listings, lack of infrastructure in new unitary plan zones etc.

You're worried about people selective quoting only half the statement, so you selectively quoted only half the statement? Your fears appear to be very real.

The quoted sentence has two diametrically opposed things in it! It shows that he just does not have a clue!!!!

The quoted sentence has two diametrically opposed things in it! It shows that he just does not have a clue!!!!

Not at all. He's hedging his bets. Typical comms strategy when one doesn't know what the future holds.

"As for why anyone would ignore it - I think that people (particularly in this forum) resent investors/speculators that have made massive capital gains without lifting a figure."

One correction: "...have made massive capital gains without paying any tax". Lifting a finger (unless it's the middle one) has nothing to do with it.

Did you accidentally buy high? (i.e any time in the last 12 months)

January 2011

The rental return underpin is about 30% south of current market prices, so you are not wrong there.

"Increasingly, we will see the sell side adjust. Some of the people with their homes on the market who don’t need to sell will pull out of the market. Others will become more realistic about the price their home will sell for and move to meet the market."

Got it. So if you're a seller, but don't need to sell, then don't sell. That way, your house value will remain high.

But if you are a seller that needs to sell (forced or otherwise) then you have to meet the market in order to sell. That lowered sale will drag house values down.

Oh well, everyone is coming with figures or an index ... just to make it more confusing for uninformed buyers .. ..

QV concluded that Auckland prices changed on average by 0% in the last 3 months to June and UP by 7% YoY ... I dont believe it is going to be herd mentality, houses are not cars or shares ... they are solid brick and mortar the only Asset that is called Real Estate ,, few have-to or desperate sales will not shake a market that is powered by strong demand and diminishing supply ... everything else is wishful thinking and twisting of numbers.

House prices in MillWater are rising by the day, and they will go up by another 5% come October - they are already at the 1,100 to 1,200K mark

I think the myth in your numbers is reflect a strong demand. The strong demand was the result of prices going up - with everyone climbing on the band wagon. The result is that prices well exceed fundamentals (construction cost or rental value).

I don't know MillWater - but I suspect that by the end of the year you will be able to buy cheaper than you can now

I think the myth in your numbers is reflect a strong demand. The strong demand was the result of prices going up - with everyone climbing on the band wagon. The result is that prices well exceed fundamentals (construction cost or rental value).

I don't know MillWater - but I suspect that by the end of the year you will be able to buy cheaper than you can now

Wait, what? You're picking Millwater to INCREASE in value between now and October by 5% (so, 20% annualized) .... that's a very BIG call. Want to make a bet?

FYI - Just because something is physical ("real"), doesnt make it impossible to have volatile prices - think Oil, Gold and yes, "Real Estate" in California, Ireland, Italy, Greece, etc etc.

I did not say between now and October , i said " come October" that does not make it annualised 20% lol, however, prices Last year have moved up by more than 5% in the same development.

5% in 3 months is the same as saying an annualized rate of 20%.

Regardless, please provide source for year on year improvement in prices of 5% from July 2016 to July 2017.... and you're implying a FURTHER 5% increase between July 2017 and October 2017. That's what you're saying?

@MisterB, Yes you're think too logically for the RE's all the see is dollar signs. Now they're in price and sales withdraw, like drug addicts they need their next fix of fresh top end buyers. Sadly they're no longer in sight and won't be fore the foreseeable future.

China’s PBoC Announces An Army of Over 400,000 To Prevent Money Laundering

https://betterdwelling.com/chinas-pboc-announces-an-army-of-over-400000…

CJ099, when you sold your rentals at the top of the market did you warn the buyers that the price was going to drop seeing as you were so certain? That would have been the moral thing to do.

@Zachary: Well didn't you give us all assurances that the Auckland market couldn't possibly fail and you still believe that don't you Zac. Besides I'm pretty sure they went to other investors.

Does Bob Qin still have a job? Anyone in the game knows that Millwater was predominantly sold to mainland China buyers. Bricks & Mortar mean diddly half way across the world - especially when the man is suddenly looking into your offshore dealings. Could be some nice uninhabited homes going cheap sometime soon.

Re my previous comment on open homes in Millwater I also noted a couple of houses were previously sold at 1.5m and now they were hanging out the comment of "accepting offers over 1.2". From the family pictures noted in occupied houses it appeared that the sellers were largely Chinese in origin.

The new houses were amazing. 5/6 beds/ 5/4bath,3 lounges. All same colour roof, same colour walls as the next and next and next.....

Govt: Nah, the people in the photos were wearing masks...

Why would the Chinese buy properties in Millwater? Surely it's not DGZ and at least 2 hours drive from the CBD during peak hours or 4 hours daily commute?

Anyway you're all welcome to our Remuera Bastille Day Festival on 15th July 2017! See you there my neighbour Cowpat :-) http://ourauckland.aucklandcouncil.govt.nz/articles/events/2017/07/remu…

DG - I don't know why but the couple of European agents I met described the area as full of Chinese "boxes".

Most of the agents were Asian origin and seemed a bit perplexed when we waltzed in.

One hopes that the builders / developers know their market else there is one hell of a ghetto gestating there.

It's called Millwater because every house there is at least a Mil LOL

Leaky too? Haha.

Oh yes. So we can split Millwater up to Mill and Water, where:

Mill = Every house is worth at least a Mil

Water = Every house is at least leaky to a certain extent

LOL

Auckland is spending several $billion building a new sub-city up there and Millwater is in a good location to take advantage of this. Of all the places in Auckland, Orewa could easily have the biggest long terms under the existing unitary plan - there is land to grow and unlike Auckland people are actually allowed to use it.

20 more years of Auckland paying for its development and Millwater will be central to a booming coastal city enclave.

"Ebert said that, importantly, the recent decline in Auckland house prices was now getting significant media coverage.....This can be self-fulfilling to the extent that folk........"

Translation " FFS stop reporting things as they are....."

It was all fun and games until somebody loses their turn for capital gain

There's plenty of demand however until the prices come down to an affordable level the sales will remain stagnant.

The question is at what point in this downward cycle will buyers decide they have the income to service the loan and go ahead with a purchase.

Maybe they won't come down to an affordable level, because this is not yet a downward cycle - in the macro sense. We have high immigration, low interest rates and a good economy.

Auckland prices seem more likely to stagnate and only slightly fall. The rest of NZ and most of the rest of the world will continue to make capital gains whilst the good macro remains.

First interest rates go up, then economies go down, and finally people start to leave, and then what do you have? Falling prices.

Yeah, but an interest rates increase to stress levels (for the rest of NZ) is 2 - 3 years away. The rest of NZ is building a lot faster than Auckland and in 2 - 3 years will have a surplus of supply. An exodus from Auckland will in large part end up in the rest of NZ. Medium term looks bad for Auckland, but not the rest of NZ.

Since I've started tracking available listings for rent on the shore back in November 2016, its never been higher than today at 425! Pressure is building everywhere as those that choose not to sell, might not have that option if their property remains empty for a few months.

An interesting stat - and it could be a very positive development for the overall housing crisis!

Its reported 30,000 homes in Auckland are currently vacant and untenanted due to the owners choice - largely due to the hassle of renting not being worth it when there are $2K a week capital gains to be had. If these same owners are faced with no capital gains and even falling prices, they could be forced to start renting properties out to cover expenses and interest payments and in which case the overall pressure will drop considerably both for rents and then you would imagine also prices as yields drop even further.

It may not be a huge correction - but certainly a return to Rental Yields being an indicator of price would make a lot of sense - and falling rents would only add to the resulting price fall

Why is it that all the property bulls quote " demographic factors will underpin a rising Auckland market." when they can also underpin a dropping market if the factors change course? Who can really predict the future medium and long term factors?

http://www.stats.govt.nz/browse_for_stats/population/estimates_and_proj…

This projection also has a chance of flat growth to 2068 or is this an unbearable thought to entertain?

A good way of reducing the real cost of house ownership is to reduce the transaction costs of buying and selling.

In my view, vendors ought to step-up their bargaining with real estate agents right now. It's a prime time to shop around and drive a hard bargain! Get quotes from several agencies and play them off against each other. Don't be afraid to go back a second time and re-open the negotiations. Prune back those commission dollars. And refuse to pay for extras - like advertising - or impose your own limit on what share you're prepared to pay for.

REA's have had it easy through the housing boom of 2014-2016 with some making huge incomes. But in a tougher market, they might be expected to work harder for less income. Or, if they don't like it, they can exit the industry and find work elsewhere........

So, make competition work. Haggle with the real estate agents! In doing so, you'll likely be better off - and you'll also be helping other buyers and sellers.

This doesn't make sense. So a vendor gets a few thousand off the REA's fees do they then sell their house cheap or would they still want the maximum they can get from the market?

I'm not aware of agents working any less in other countries where 1% is the norm, they still need to maximise price to maximise their pay. The question of whether any agent really has the incentive to push for that final 10-20k is valid even now (how much more work do you put in for the extra few hundred dollars when you've already got 20k coming your way?)

I was stunned with the commissions charged over here when I arrived, and even more amazed that people see it as an acceptable charge, particularly now most of the marketing can done by sticking a few pictures and an quick blurb on Trademe.

Also reduce friction by making LIM reports and builder's reports just information that must be disclosed to all sellers - i.e. a cost for the seller rather than a cost of multiple different buyers. The current waste of money makes no sense and discourages buyers.

I've always thought that... it's crazy the ticket gets clipped so much!

A few years back I overheard a RE Principal asked by a client 'how's business?'. To which he replied along the lines, It's bloody tough - everyone's clipping our ticket. I had to clean the long black off the table which I had just spat it over...

Good idea, this kind of thing is already done in the UK where the vendor must provide an energy performance certificate rather than each interested party having to get one. Sadly I don't think it's extended to building surveys yet.

https://www.gov.uk/buy-sell-your-home/energy-performance-certificates

absolutely - A full sellers pack arranged by the RE agent as part of their service - LIM, builders report by independent builder of a qualifying list, meth test report - and available to all potential buyers free of charge electronically.

Just think how much wasted time and energy could be saved - freeing up builders to build more homes! Again its not quantity that will improve quality of life its increasing productivity and reducing waste

I think this is another thing that National will not do.

Or they may ask someone to conduct a nine month cost-benefit analysis of it first, or at least until after an election comes around.)

Or promise to do it in 2040 or something

Harcourts in Tauranga seem to already be doing this for properties going to auction. You can register your interest and a link to the LIM, title & sometimes the council property file is emailed to you. Saves some bucks for sure.

Vendors can supply LIM and Building reports But the banks don't want to read them as it is too easy for a vendor to remove a page or change some words. Banks and solicitors want the information addressed to the purchaser.

That should be a crime.

However, suspect that wouldn't stop some, especially the likes of the recent husband and wife team facing charges over mortgage fraud.

Neither my bank (ASB) or solicitor cared that the documents (LIM, weather tightness) were supplied by the vendor. My solicitor did pickup a missing page from the emailed LIM document (just an admin cock-up, not deliberate trying to hide something).

Yes sounds like a good idea, the problem is many buyers don't trust the builders report you provide so they get their own commissioned.

I agree builder report is subject to personal preference, but documents like LIM which is going to be the same fro every potential purchaser should be provided.

Auckland is a high cost market due to the inefficiencies of Auckland Council (high land costs, low economies of scale, high compliance costs). Which means that in the wind down period before the end of a boom it hits the wall first. The good news is that the boom hasn't ended.

BNZ senior economist Craig Ebert says recent housing market trends show prices, generally, to be going sideways in Christchurch, modestly down in Auckland and up almost everywhere else.

Time to diversify out of Auckland.

That time was about 2 years ago ie the same as the time to stop buying in Auckland.

Too late now...

It is still a good economy, with low interest rates and prices are going up everywhere (apart from Auckland and Christchurch).

Auckland embraced the stupid, with a somewhat unique approach to planning and went through an explosive period of price inflation on its land. And that ended.

But why would that matter to the rest of NZ?

If you see most new listings are of investors who had purachased last year for fast money and now are trying to sell for no loss no profit or with minimum lose.

Can check past sale of the house in market specially in Auckland and can check.

Next few months are very crucial to make ( no rise but even if it is flat would be positive) or break the market.

send links please

"The prospect of a "reasonable correction" in Auckland house prices "grows by the day", according to BNZ economists"

Shame they don't have the courage to quantify "a reasonable correction" does the BNZ Economist mean 5% ? 10% ? maybe 20% ? ...

They are not the font of all knowledge, so even if they were to guess at a figure, it would not do you one iota of good.

Its like Mary Holme of the Herald, asking for her input all the time is imbecilic.

at least they do not pretend to know .

After the crash, I’m thinking of buying 2 maybe 3 houses in Remuera at 100k a pop.

I was going to get more, but I don’t want to appear greedy!

Everybody is focused on Auckland property prices, while nobody is taking note of the absolute disaster that has unfolded in Wellington over the last two years! I can give 3 examples in Khandallah alone where the same houses have been sold after barely two years for almost $200k more. With NOTHING done to them!

Even the same bloody photos from the previous sales were used on the trademe listings. I've never seen anything like this before.

I've seen houses that would kill you with black mold if you looked at them long enough sell for 600K+

There's a major problem in Wellington and it's not going to end well.

In Wellington, the letting market is even more of a dilemma.

Rents have soared through the roof over the last year.

Two bedroom grottos are achieving $600+pw if they're located close to the city.

Toothepoint 2 bed medium rents in Wellington have risen 1.3 percent over the past year. Someone telling porkies.

They stagnated and sometimes dropped in the years previously.

I've been a property bull for many years as most on this forum can remember. I've rightfully called out all the doomsters and their 'property crash' rubbish since the GFC.

Mate, no more. The wellington property market is in a bad place. Rents, property prices, all bad. The end game is here.

Onwards what is the 'end game' A property crash?

A recession. The property correction will just be a preview/trailer.

I own townhouses in Central Wellington, predominantly Mt Vic. Rents are rising, the most recent let 4 weeks previously was put up on trademe on Thursday night and we had 16 parties through on a Saturday open home (40hrs post listing). There were 8 applications and the property was let that evening. We also had phone calls from Auckland and Christchurch stating they could not attend and could we let them know if it did not let over the weekend. There is a shortage of property in Wellington, so I cannot see prices falling. As even at present purchase prices with 100% financing, properties tend to be cashflow positive and the cost of construction is now over $3000 per sqm for decent spec. But don't let me spoil the doom fest with info from the real world.

From OnwardsUpwards comment I thought house prices and rents had suddenly doubled or suddenly halved or something in Wellington. I go on TradeMe and check what's happening and see many houses for sale or rent at the usual prices. Nothing much is markedly that different from six months ago. Unemployment is low, NZ is at the very top of the Legatum Prosperity Index and has been since it clawed its way to the top four years ago.

Wellington is a lovely city. Just a few weeks ago Welington was named the world's most livable city by Deutsche Bank. Watch the video. Auckland #13.

Absolutely no decline whatsoever in Wellington. In fact it is quite the opposite. TradeMe listings clearly show there is only one way traffic and that is UP.

That's exactly what happened here in Auckland over the last few years, except recent articles have confirmed that the peak was 12 months ago and we're in a decline now. Wellington is just playing catch-up, I would say the peak is now and 12 months from now we'll see the same downward trend in price.

Agreed, however the decline in Wellington is going to be brutal. Wellington just isn't much of a city. I love the place, its home, but the facts are that Wellington is small, cold, windy, damp, tiny industry, hyped up tech industry consisting of mostly 10 year+ old 'startups', banks and some coffee shops and government jobs.

Average house prices here should never have reached over 450k-500k.

Agreed. I have family in Wellington and they struggled to purchase just with the craziness of the market. They found something earlier this year for around $500k but the RV is just around 300k. Craziness.

Volatility in the market is causing stress for people, especially FHBs and bank managers. If I was the government I would pass a law that would guarantee no loss of equity for first home buyers. This would take a huge weight off their shoulders and enable them to spend more quality time with their families. The benefits would be huge. Not such a silly idea? Vote Zachary Smith for a safe and secure future.

I think you could argue that the govt and institutional framework is implicitly doing its best to protect house prices. It's not a guarantee, but it's probably the best you can hope for.

Zachary, I usually like your ideas but not this one. Govt guaranteeing prices? No thanks. Meddling with market forces creates distortions.

A correction might be 5% until after the election, but then I put my money on a price jump again as more population pressure builds every day. Evan if NZ First gets to slow the incoming flow, the pressure is already building.

Northland Hippy, thanks for usually liking my ideas. I had meant for the comment to be satire but then J.C. makes a good point about it almost being a policy already.

A Sanctuary Found - for you Zachary!

http://www.trademe.co.nz/property/residential-property-for-sale/auction…

Ever heard of moral hazard?

Haha...you sound like a National party finance minister approaching an election :-p

New Zealand property market generated nearly $4 billion (yes, billion!) in profits for owners in the first quarter of 2017. It looks like we are all one big family after-all...over 96% of New Zealand property owners profiting from resales. Yippeee https://shar.es/1BSCmA

You say you're making profits, eh, DGZ? If you're making profits, aren't profits taxable?

It's capital gains that aren't yet.

Just as media coverage of rising house prices proved self-fulfilling.

If sheeple rushed into buying a house because they believed every NZ herald headline, I have no sympathy for them when the value drops. It doesn't matter what RE agents say, it doesn't matter what the media predict and it doesn't matter what houses cost in other countries - affordability for each buyer has to be the over-riding consideration (factoring in the potential of increased mortgage rates, insurances, repairs and maintenance and council rates)

I see "deferred maintenance" on half a million dollar crap shacks in South Auckland everywhere! Wealthy homeowners on paper that can't even afford the basics of everyday to live on. The market is so out of whack against fundamentals that it makes sense to step away from the madness and leave the carnage for all the existing owners to sort it out.

If the banks' RE lending bubble does not stay puffed neither will our RE price bubble. RBNZ capital review anyone?

I am looking to buy in Wanganui, nice life out there apparently and good yield %

Palmy North might be a better choice. High yields, still relatively low house prices compared to most small cities and the city is a new hub for call centre workers and many businesses are actively employing new staff on good rates. The cost of living in Palmy is cheap as chips compared to everywhere else, which means more disposable and discretionary income compared to other areas. There is also a shortage of good rental houses now.

Onwardsupwards, yeah resession, or close , where Auckland had overseas investors, the rest of nz is worse of by far, they had Aucklands moving in or investing, that's really bad because when Aucklands prices come down, aucklanders can't get the money they need to move on, sales will dry up big time, buyers will buy of people willing to meet the market but the buyers don't earn enough for high prices, someone will always sell but BIG STALEMATE, the rest of nz will lose there buyers real quick, at the moment it's ok because aucklanders are willing to move in there price and that price is excellent money elsewhere

I've heard so many stories of aucklanders hitting Hamilton, Tauranga, papamoa, Wellington etc, driving prices up and rents, lock ups full of people's furniture why'll they crash wherever they can, I have friends selling and paying of there mortgage and moving to little places like martin levin etc, everyone's moving all over the country, all the rest of the country needs is bad sales numbers, not necessarily a larger drop in house prices and nz as a hole in for a big shock, specially some of these land developers that are late to the party and oversupplied, yeah worry more out of Auckland

I agree that people a lot of people are pissed off at the stupid house prices and the crippling infrastructure overload that is now Akl, and what caused this big crappy mess. Namely specuvestors, overseas money and the Govt that just looked the other way and fiddled while kiwi workers/tax payers hopes and dreams burned.

Imo Nat has massively underestimated the resentment that has built up against them on this issue in the last three years. It looks like third term blindness, just like the Clark govt before them. Perhaps they do, and thats why Key bailed.

So keep posting how great your portfios are, and how great it is to keep lifting rents, how great it is to get extra rent for occupying garages, how great its to keep buying more houses, and how great you are for investing when you did. Yes... keep it up.

75 odd days to go. Crux of the election.

Why would people be pissed off when majority of us are home owners and we see our capital gain sky-rocketed to unprecedented level in the last 6-7 years. There are a lot of people out there who can't wait to celebrate the $4 billion made in the first 3 months of July this year.

Because nothing has been "made" from NZ's perspective...

Some individuals have made a killing but at the expense of others who now have massive debt. Zero gain.

GDP per capita has barely gone up despite allowing half of Shanghai and Mumbai to come in - productivity per capita or hour worked v rest of OECD is still crap. All whilst overloading our already stretched infrastructure - schools, hospital's and roads are a MESS.

Its all done from an enormous increase in private debt, its illusory and sooner or later it will come home to roost......for all of us.

And yes...I own a house and earn a very decent income but strangely care about the COUNTRY not just my little fiefdom which at this rate will have to be enclosed in razor wire as we let the rest of the place fall to bits .

I think "Zero gain" is generous, given that the "made" money is really debt, and the interest on most of that debt is repatriated straight out of the country by our masters across the ditch. And that interest is real money that is not only lost to our economy, it ultimately has to be earned by fellow citizens who actually work for a living. Did I also mention that at some point (probably when things are looking a little dicey on the economic front), our masters will also want their capital back? Just like a heroin or fentanyl addict, the high right now is good. The future, not so much.

Because it's a fiscal drag on the economy. We would be collectively better off if debt had been used to grow businesses and increase productivity.

Because I give a fuck about my fellow citizens. Houses are places to live. I don't care if my home value drops 50%. I actually welcome it, if it means my coworker, his wife, and their daughter will actually be able to afford a house to call home.

Exactly

As someone who only has a small residual mortgage I agree except there is one huge issue. Negative equity and in-solvent banks and then an OBR event(s).

So maybe someone can tell me based on NZ banks leverage ratio etc just how much of a drop in house prices the banks can sustain before the become technically insolvent as their assets are not worth what they say they are? (I am not a "guru" on this so I am struggling a bit with the possible issues/damage)

As an example of what I mean say a NZ bank holds a title deed to a mortgaged property worth $100 in today's market. It has a 90% mortgage so the house owner has put in $10 and the bank $90. Lets say the home owner defaults, no biggee the house is sold at 95% of its value (to get a quick sale), the house owner after estate agent charges, bank fees etc sees the $10 wiped out but the bank gets its $90 back, the bank is "happy" its probably still made some money in fees anyway and its lost no capital.

Lets say we see a 30% collapse in-house prices. The bank is now staring at a $20 to 25 loss per property in one way as long as the house owner continues to pay on time the loss is made back. However how does that effect the banks leverage ratio? and its capital reserves? What happens if this occurs on a bigger scale, ie thousands of home owners? I assume then the bank has to go out and raise capital to cover this loss of $s and will have to pay whatever the rate is for that and that could be crippling. How far is an OBR event off then? Of course here I am assuming a business as usual, economy is doing OK-ish scenario. The thing is to cause the above we are likely to be in a severe recession and see an increasing un-employment rate which means increasing defaults.

What gets me is the banks only look at the micro view and with their effective lobbying of Govn have stopped the RB etc in taking an effective holistic view all in the name of profit.

So if your 50% loss occurs, in my case I loose $s I never had, no care. What I will care about is as a tax payer I will be lumbered with a multi-decade debt. A debt that even my kids will spend much of their life paying off let alone me. All really down to greed, pure and simple.

My understanding from a Banks perspective is that a 3-5% of non-performing loans which are less than 90 days in default but in early stress and vendors already in default being 3 months with loans gone bad will have a huge impact on the banks in a fractional reserve banking sector. One thing that I was taught years ago, was that when one customer turns bad, the banks needs to write 10x the amount of the loss, just to break even, because the banks profit margins are that slim! Our banks borrow heavily from the US banks because New Zealanders are so poor at saving, therefore when the US Fed Reserve raises rates, our banks need to keep up with the pace fast or they become insolvent and take down their depositors with them.

Question is, where should savers be moving their money to now to be safe from OBR events?

I'm with you on this Gooki. I'm Gen-X and was lucky enough to have been able to afford to buy my home back in 1994 as a single woman. I have been debt free for some time now and i DO NOT WANT my house to increase in value, because that would mean my daughter will be locked out of the market and won't have the same opportunites that I had. I will not prop up this housing bubble by mortgaging my own property to give her a helping hand and she would never ask me to anyway. She is just planning on leaving Auckland and taking her builder boyfriend with her.

You never want the middle class to get poorer or shrink.

When that happens, bad things follow.

Agreed, but that is exactly what is happening.

Seems to me it's in part because we have a generation of voters (and their leaders) who grew up benefiting from socialism, but then also benefited bg-time from the liberalisation that followed in the 1980s, and have quite forgotten what role earlier efforts played in their wealth and well-being. E.g. they forget the benefits they received through free education, earlier government builds, housing affordability aided by the Housing Corporation.

So they associate what's happening now with being the best way to manage everything, despite the fact the stacked deck (in their favour) is making the next generations significantly worse off (for the first time in NZ's history).

Likewise we forget how hard the fight was in NZ to get reasonable rights for labour. Having a significant other from a country where this is not the norm, she notes that NZ's don't realise how lucky they are in terms of protections for workers from exploitation. (Notwithstanding the examples of scum like Joti Jain from the Masala restaurant chain.)

RickStrauss, don't you think that generation of voters and leaders benefited from more than just socialism in the past? This documentary is well worth watching to get an idea of the sort of world this generation grew up in:

Documents the final years of the British Empire. Pretty sad to watch actually. One thing that struck me was the high immigration level from Britain to Canada, Australia and NZ after the war. Many working people couldn't get anywhere in the UK on the low wages and moving to the above countries was the only way for them to buy their own house and secure a better future for their children at that time. It made me wonder about my theory of the Global City network being an empire of a sort. Now the common worker has to move out of this new empire to have a decent life leaving only the lucky, the exceptional, the elite and the slaves behind.

RickS,

Your big mistake is to mention Socialism. For a whole bunch of people on this site,that;s a dirty word and is little more than communism in disguise. For them,the Market is sacrosanct and any perceived market failure can be attributed to government 'interference' in the holy Free Market".

This total lack of any historical perspective would be funny,if it were not so sad.

Doctors lawyers and engineers PhD's scientists, accountants etc can no longer afford a house in Auckland. Double income no kids cant afford a house in Auckland. The 90th percentile high income bracket can no longer afford a house in Auckland! Its not just the middle class!

Nothing special about them some might say. I have a Bachelor and a Master but I certainly don't think I am special but I can still afford a house or more...

The issue of affordability doesn't affect those who were of the age to get into the market a long time ago, of course. No one is questioning that.

Excluding your negative geared rentals, how much do you earn in your 19th floor

Quay St office job Zac?

There is an easy solution to that. Live anywhere else in New Zealand other than Auckland. Problem solved.

What do you think will happen to Auckland if young professionals leave?

There will be old Boomers, Chinese investors, and overqualified Uber drivers.

National's brighter future.

Auckland will become a blue rinse city.

WHEN young professional leave Auckland will continue to implode. It will start with lower paid but skilled workers - teachers, nurses, police officers, firemen etc (it most likely has already started).

Screw that. Young professionals should move overseas and upgrade their life. New Zealand doesn't deserve them.

Fat pat, that is a dishonest comment

Long time listener, first time caller, morning all.

There's clearly an out of whack market, built by unprecedented levels of low interest debt, foreign investment and immigration. For those bullish people, NZ is too small for a select band of people to play monopoly, particularly when that money is not their own, and that will change either through market forces or political will. From a fiscal point of view, QE is done, interest rates are on the rise - 28% of mortgages are owned by "investors" of which nearly 50% are interest only, meaning that any pressure on interest rates or slowdown/fall in house prices has a massive knock on effect.

Foreign investment, China has had a major crackdown on finances leaving the country and is facing it's own burgeoning debt crisis.

Immigration is a major talking point of this election, I'm for structured immigration (Where do we lack skills? Where can we import those skills from? - Doctors, Teachers, Engineers etc etc), I am an immigrant and had to jump through many hoops to come here (thank you for having me).

Politically, more than 1 million people now are renting, that is a significant portion of the electorate, if the market does not normalise, then that disaffected block will vote for change. Alongside that, as evidenced here, there are numerous people who believe in the kiwi "fair go" ethos (the egalitarian nature of NZ is what drew us here in the first place), who will also not necessarily be against a normalisation of prices. Typically middle class professions can no longer afford a house, or do not have the inclination to gamble in a market that is massively over-heated.

Solidname, Solidlogic. Look forward to your next call

well done, solid analysis there solidname

looking forward to more of your contributions

Welcome Solidname. I agree with your sensible thoughts.

Great observations mate. Welcome to the 'banter' of interest.co etc.

Flushing out the property speculators at a low price is exactly what is needed.

Yes, it’s a shame we live in an age where market corrections are seen as abhorrent and best avoided at all cost. If a market isn’t allowed to correct the mass misallocation of capital, it must die.

Toronto House Prices have crashed 192k in the last 3 months. Thats over 2k per day for 3 straight months. Chinese money has slowed or stopped, creating the start of what may soon be a compete crash if its not already. Auckland has the same ingredients for a complete collapse like Toronto. The mainstream media keep this very quiet from us though.

Got a source or link for that Toronto info?

Yes its going to take a dive but as soon as it starts going negative, the sharks smell blood and that pent up housing demand is unleashed. We almost have the perfect storm with the election coming up, the dip could be very short lived this time around. The trend in the market is going to be pretty clear come Christmas, interesting times.

This "pent up demand" can only be "unleashed" if the banks allow it, cause its only locals left in the market, who cannot afford current prices. See the banks are the landlords that decide whether locals can afford the "rent".

Or possibly it all starts to deleverage, interest rates go up alongside the defaults and the mortgagee sales, the economy goes sour, people leave, demand falls and we get a real crash for the first time in a long time. The bigger the mania the bigger the crash. It was a pretty massive mania.

It's amassing how some on here look only at there tiny little greedy world, one town house in the middle of Wellington do ok NOW, or bloody Remuera, the 1% shit, its the other 99% of the houses are the problem, Auckland and more so the rest or the country, its more or less just starting and frankly needs to happen with pain to come right, buying and selling homes in 2 to 3 years at 30% less would be better all round, and it needs to happen and will solely because of wages, I've owned over 20 houses and commercial buildings and seen many slowdowns to flat just about every 10 years, 2008 wasn't that bad but once again that wages barrier, wages have gone up a little but very small really, what's going on now is the worsed ive EVEN SEEN, so many People holding houses so over priced, yes some people can just hold onto them and talk themselves in there value but really if they owe about 70%, in a few years NOT TODAY, they'll be forced to stick with that house for a while, hopefully they can, the election is giving some people hope but things have been changing in houses even with national for a while, there's a lot more to this than national, immigration and Auckland

Why do you have to put a 'bloody' in front of Remuera?

Autocorrect maybe? Probably meant "boring"...

Well, then don't come to our Remuera Bastille Day Festival this weekend then...

http://ourauckland.aucklandcouncil.govt.nz/articles/events/2017/07/remu…

I rest my case!

Fall in Toronto home prices 'a big surprise,' says broker

http://www.ctvnews.ca/business/fall-in-toronto-home-prices-a-big-surpri…

Is this what is happening to all the specuvestors in Auckland?

negative equity

https://www.trademe.co.nz/property/insights/address/Auckland/Mission-Ba…

And negatively geared as interest payments on that mortgage is about 700-800 a week. compared to rent of 550 a week

https://www.trademe.co.nz/property/insights/address/Auckland/Mission-Ba…

What an astute investor...

LOL, shots fired.

I really don't think Trademe or homes.co.nz should be able to give out those estimates on value.

The variance on them is incredibly high and there is no methodology available on how they calculate it.

And, as we even see here, the people who hang on every estimate they provide are typically the ones who have poor financial skills.

I agree that the valuation metric is a bit wonky but in the land of lies and mis-information a reference is better than opinion.

When you don't have a good argument, an insult is not a good retort...

I was going to give Nymad a solid 'LOL'! But your comment moneyphobe, was better :)

Funny it's largely specuvestors who hang on them to feel like paper millionaires and pat themselves on their backs for their collective investing brilliance.

That is not my investment, I was just posting it as a rental example for Mission Bay.

by Double-GZ | Mon, 10/07/2017 - 19:48

Yes I agree tothepoint. If you are a landlord you don't have to worry about finding tenants at all especially if the property is close to the city. A good illustration would be my rental in Mission Bay. I'm currently looking for tenants, very close to Eastridge shopping centre and public transport. I am expecting it to be snapped up within the next 2-3 days.

http://www.trademe.co.nz/property/residential-property-to-rent/auction-1...

http://www.interest.co.nz/opinion/88708/analysis-expected-future-popula…

wow talk about Hoist with your own petard.

Maybe DGZ meant the rental on his REA books....

It was meant to be just an example. I got carried away and put myself in the landlord position, a bit like telling a story. I don't own this property in any way shape or form. Glad I can now clarify.

Keep digging DGZ, just don't get carried away...

Was that an isolated lie, or should we be similarly skeptical of everything you say?

It is not mine, and I have clarified. There's no point to keep digging now and we should put this to an end.

You understand it looks bad, right? I'm constantly in two minds about whether you're just trolling for a reaction or being serious, this doesn't help your credibility.

I have only one mind as to whether DGZ is just trolling for a reaction.

I've already worked out that he is a troll who in reality just lives a dreary life of existence. His only joyous moments are when he finishes his 8-5 job at Macca's, arrives home to his rental and then

unleashes his miserable life on interest.co.nz

LOL too funny, love it!

Thanks for the likes hehe

DGZ has so many nom de plumes.

Based on this latest I am sure one of them is Simon English - the Billshitter from Double Dipton

That doesn't clarify anything at all. How do we know you're not lying right now?

Explain your wording?

Double-GZ: "A good illustration would be my rental in Mission Bay. I'm currently looking for tenants, very close to Eastridge shopping centre and public transport. I am expecting it to be snapped up within the next 2-3 days."

"A good illustration would be a rental in Mission Bay. The landlord is currently looking for tenants, very close to Eastridge shopping centre and public transport. The landlord is expecting it to be snapped up within the next 2-3 days."

That's a re-write, not an explanation.

So, similarly, do you really work in IT or something like that in the city, and are not an RE?

How would you even know this info unless you were the agent?

The community has already established that DGZ works for B&T, in IT dept.

OMG this is so wrong and out of whack. Please give me a break thank you.

I think you've forgotten all of the things you've given away about yourself over time mate. You may need to dump this log on and re-seed. Seems to have worked for Ted.

[ personal abuse removed. Ed]. Nothing he says is true!

Personally I struggle with those in the buy vs rent camps. For me the decision to buy was not so much of a financial decision but overcoming a mental barrier. Basically when you buy its a commitment and a realization that your going to be paying for the next 25 years, many people simply cannot handle this because they see renting as a "week to week" thing that they can opt out of anytime, thing is you have to live somewhere and the mortgage was little more than the rent and if your smart with flatmates its way, way less. Sure you have to start in what you probably consider a shit hole, but too many people are worried about impressing their friends, my advice is get new friends.

"For me the decision to buy was not so much of a financial decision but overcoming a mental barrier" and therein lies the problem.

People are treating it like it's a trademe auction for that Sega console they really really wanted and getting pulled in way too deep. But, instead of being left remembering that actually, Sonic wasnt that great, you're stuck with a $900k mortgage based on affordability at the historically low interest rates now.

You do have to live somewhere, and for Auckland, in the now, that somewhere is likely better rented than bought.

I couldn't have said it better myself!

Auckland landlords will thank you for this comment. Thank you Mr. B ;-)

Yes, I am sure they'll swan away in their 1% yields.

Also buying a house isn't a commitment for 25 years necessarily as you can always sell and go back to renting. Generally that option is less attractive than owning though as the "mental barrier" has been overcome. Not many home owners long for the days when they rented even with all the maintenance and extra costs. And if they did why not just go back to renting?

I used to live in a house I (still) own, now I rent. Life is much simpler, frees up a lot of time for more exciting stuff. I'm expecting to buy another house in a year or two to live in, the extra hassle and expense of DIY is somewhat balanced by being able to settle down in security and plan for the future. I certainly wouldn't recommend buying a house to live in unless you're planning to stay in the same place for a long time and are ready to settle down.

Its not the commitment that's the issue, its the scale of that commitment...

Scale that when compared with income seems more daunting than climbing Everest with no oxygen. Scale that directly results from the pricing distortions created by foreign and domestic speculators, all injecting cheap cash like runaway junkies. But the Banks have enjoyed their best run of profits ever... old boy.

Thanks National for doing nothing. Even worse, it kinda looks like they wanted this to happen, and they continue to make play to support status quo.

Thanks Zach, "as you can always sell"

LOL!! Love it

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.