By David Hargreaves

Expectations of house price gains over the next two years have rebounded quite strongly in the latest quarterly Reserve Bank Survey of Expectations, an influential survey closely watched by the RBNZ.

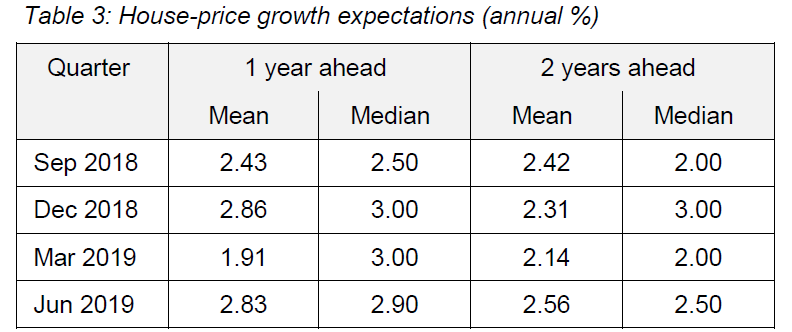

Respondents to the latest survey expect house price gains over the next 12 months on average to be 2.83%, which is pretty much a straight reversal of what happened three months ago in the survey, when 12-month expectations slipped to just 1.91%.

In terms of the expectation of house price gains over the next two years, this figure has bounced to 2.56%, up from just 2.14% in the last survey.

ASB senior economist Mark Smith said the outcome on the house price expectations indicated that recent cuts to fixed mortgage interest rates "look to be gaining traction".

The survey, released on Tuesday, came just one day of course before the RBNZ was due to make a call on the Official Cash Rate. Regardless of the decision on Wednesday, some reduction in the level of the OCR (from the current 1.75%) is widely expected this year and this theoretically should be stimulatory for the housing market.

The figure that's generally of most interest to the RBNZ in the survey is the expectation for overall inflation in two years' time - and this shows that inflation expectations are again very much 'anchored' around the 2% level, which is the explicit target level for the central bank.

In the latest survey the two-year ahead inflation expectation was 2.01% compared with 2.02% three months ago. The shorter term (one year) expectations have risen somewhat (from 1.82% to 1.97%), presumably in reaction to a recent spike in petrol prices.

This survey, a New Zealand-wide quarterly survey of business managers and professionals, carries a lot of clout with the RBNZ.

The central bank has been known to make changes to the Official Cash Rate largely based on the outcomes of this survey in the past.

The question about house price expectations is a relatively recent addition in the survey having only been added towards the end of 2017.

In regard to more general economic forecasts, the latest survey shows a drop in the expectation for economic growth (2.17% GDP growth in two years' time, down from 2.36% three months ago), but unemployment is expected to remain at subdued levels (4.32% in two years' time).

27 Comments

Seems like they’ll leave rates where they are...

I reckon that most of the turnaround can be explained by the Govt kicking CGT into touch.

With the threat of CGT out of the way, the housing market will have a bit of a boost.

TTP

"I reckon that most of the turnaround can be explained by the Govt kicking CGT into touch."

Really?

That sounds a bit unrealistic given that the survey was conducted prior to the recommendations of the tax working group being announced.

Not at all, Nymad.

The outcome was widely anticipated as the public debate progressed.

TTP

I'm still thinking 1.75% all year. If they cut today I think it'd be a silly move. At this point the effect of each 0.25% cut is very limited. Edit: Wrong.

BLSH, agreed. A cut today would be a silly move. Best they store up ammunition for when its really needed. Its near ground zero for Central Banks as a whole, not far from it for RBNZ. Post another GFC, should deposit rates go negative and mortgage rates approach zero, you can bet the housing market and the economy is viewed by the RBNZ as being in freefall. Those with deposits would be encouraged to invest in a spade and bury cash in the backyard. Positive returns abound against a backdrop of widespread deflation.

Your investment advice sums up your personality and world view perfectly - "bury cash in the backyard". Was going to advise Saving4AUhouse to follow your words of wisdom, but I see he's been banned by the powers that be.

BLSH, so now the official rate has been cut to 1.5%, do you wish to revisit anymore of your unrealistic predictions such as "Auckland HPI: +1%, Auckland Median 0%"?

Just think of what would happen to the banking system if depositors could make money by storing it elsewhere! Like I said, we are near ground zero.

I'm happy to be wrong given that one of my fixed term mortgages is expiring next month. Will be sure to get sub-4% fixed for 2-3 years. You on the other hand must be disappointed that I was wrong given your portfolio is all in on fixed term bank deposits.

Not at all :) I have another 3 1/2 years to run on a specially negotiated 4.26% paid monthly. Better risk/return than a rental! The key difference is that I will have my entire principal returned under an overseas parental bank guarantee. If your hard out speculating on expanding your unbanked paper wealth, the reality is that some of it will be stolen while you sleep at the wheel. Are you aware that increased bank capital requirements will put a floor under mortgage rates into the future?

In fact, 4.26% is not a very high return for a rental house these days.

Rents have hiked up markedly in recent times owing to the shortage of accommodation - especially in Auckland and Wellington......

And then there's the capital appreciation on investment properties over the last umpteen years. The figures are eye-popping, as we're all too aware.

As term deposit interest rates fall further, there'll be more people who'll wish they'd invested in property over their working lives. Property provides for better security in one's senior years.

With a property portfolio, one doesn't have to worry about interest rates and all that sort of carry-on. You can just get on and enjoy life.

TTP

Agent TTP, it's cheaper to rent with soaring house ownership related costs. I couldn't care a less what my house is worth but it certainly matters to some. Its always been a well maintained 60-year old house with fond memories. Merging demographics and skittishness will only serve to unwind the property portfolios that the boomers have accumulated. Add a cyclical slowdown into the mix and it's not going to end well.

4.26% risk free. I don't have to pay rates, insurance or worry that my bank is going to ask me to fix something ;-) As opposed to unbanked paper wealth, the return of my principle is more assured than with housing.

Renting is often labelled "dead money" by tenants themselves. That's largely because it represents a transfer of money (and wealth) from tenant to landlord - as recognised since times immemorial.

"Once a landlord, always a landlord - but once a tenant is enough."

The combination of rental yield and capital appreciation means few landlords have cause to complain.

One doesn't come across too many property owners/landlords divesting into bank deposits - especially at today's paltry interest rates. And, sadly, the latest news from RBNZ makes matters worse for bank depositors.

TTP

Agent TTP, there are many landlords exiting under a cloud of toxic legislation. The sad fact is they're being replaced by first home buyers who know no better. The leverage risk to the banks is shifting from one group to another.

You are missinforming first time buyers because you are yourself misinformed....

Sounds legit!

Positive Thinking but will it help.

Joke :)

I wish they had separate stats for the Auckland and 'the rest of NZ' markets. Even I, a so called DGM, expect house prices to increase in the next year - albeit only on average, outside Auckland.

I wish they had separate stats for the Auckland and 'the rest of NZ' markets. Even I, a so called DGM, expect house prices to increase in the next year - albeit only on average, outside Auckland.

No offence, but I think most people's expectations about asset prices (especially houses) should be in left in the trash. Why do I say that? People expect things to occur mainly becuase of their hopes / desires; subjective percetion of reality; and what is fed to them through media and peer groups (his element is especially important for the boffins).

I love how the question on expectations was only added to the survey at the end of 2017.

Who do they actually ask? I’m on their mailing list but not been asked any questions? Or do they just ask the banks, brokers and highly leveraged?

from: https://www.rbnz.govt.nz/statistics/surveys/survey-of-expectations

"Institutions surveyed:A sample of economists, business and industry leaders"

It should be pretty self evident who they ask, just read the doc.

Phew, glad we're going to dodge that crash then! It's not like there's any overbuilding going on or anything here. All will be well, now is the time to buy!

https://www.stuff.co.nz/business/112485541/surge-in-auckland-building-a…

Plenty of choice, it’s a great time to be a buyer.....what overshoot?

Here's a question worth considering: did the RBA have access to REINZ's April figures when making their decision to reduce the official cash rate? :-)

Reserve is trying to reduce the risk by dropping rates. Of course it only has the effect of putting costs up in other area with the fall in the dollar.

I believe we will follow Australia. For those who say the prices will only drop a little because of the so called shortage supply.. have a look at the supply now .. people have got to be able to afford property to purchase and those that are looking cant buy at these price levels.

https://www.dailymail.co.uk/news/article-6871241/Australias-housing-mar…

Dead cat bounce but otherwise flat for the next few years

Anyone here living in Tauranga or Katikati way ? Thinking of moving down that way. Had several properties on my TM Watchlist since January and nothing is selling, it must be pretty dead down there and there is a huge inventory of standard houses in the burbs going for "Kiwibuild" pricing.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.