The Reserve Bank's conceding that the first iteration of the loan to value ratio (LVR) restrictions in 2013 "disproportionately restricted" purchases of houses by first home buyers.

The RBNZ has undertaken an extensive review of the LVR regime as part of the "phase 2" review of the Reserve Bank Act currently under way.

The review has found the LVR policy has been effective in improving financial stability, which was the objective, but the RBNZ does say all prudential tools have an efficiency cost, which must be weighed against the benefits.

"The LVR policy is likely to have had a larger impact in constraining mortgage borrowing capacity than alternative macroprudential tools," the RBNZ says.

"This suggests that the LVR policy should be deployed primarily when housing and household sector risks are high, to maximise the benefits of the policy relative to the efficiency costs, which are reduced credit access for credit-worthy borrowers and the potential for slower economic growth in the short-term. The speed limit of high-LVR loans is an important calibration tool to mitigate the efficiency cost of the policy."

'Tension with goal of housing affordability'

On the constraining impact on FHBs, the RBNZ says the difficulty for FHBs getting into homes created "a tension with the public policy goal of housing affordability".

"The LVR policy is likely to prevent some households that wish to purchase housing from doing so, which is part of the process of safeguarding financial stability. However, this means that the LVR policy can negatively affect a public policy objective of housing affordability, including for first home buyers," the RBNZ says.

"A uniform LVR setting for all borrowers tends to disproportionately affect first home buyers. First home buyers are generally young and in an early stage of their careers, therefore their savings tend to be smaller than other buyers. Moreover, first home buyers have never owned any housing, and have not benefited from previous house price inflation.

"Related to this, in a rising market the impact of LVR restrictions are generally temporary for investors, because continued house price inflation will boost investor asset values, but the effect on first home buyers is more durable."

The RBNZ says based on Corelogic sales data, the first home buyer share of house sales fell from around 25% before the LVR policy took effect in October 2013, to below 20% by early 2014.

'Disproportionate reduction in lending to FHBs'

"While data on lending breakdown by buyer types were unavailable for most of this period, banks and mortgage brokers point to a disproportionate reduction in lending to first home buyers."

However, the RBNZ says in some contrast to the decline in first home buyer activity, house sales to property investors were "not significantly affected by initial LVR restrictions", leading to their share of sales increasing.

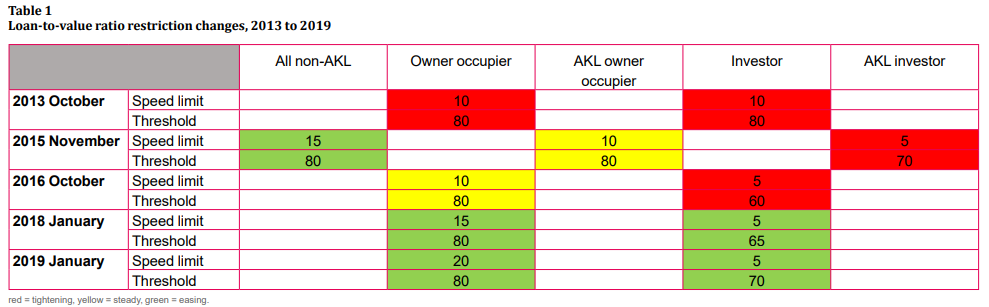

"Starting in 2015, the LVR restrictions were incrementally calibrated to be more targeted at investor lending, which was viewed as a greater risk. New lending to investors declined sharply after the introduction of the nationwide investor LVR policy in October 2016, and house sales to investors fell as a share and in an absolute sense. This contributed to the rising share of FHB purchases after 2016. The share of new mortgages going to FHBs has risen to 17% by the end of 2018, up from just 10% in 2014 and 2015.

"The appropriate calibration of the LVR policy can make restrictions more targeted at risky areas, and reduce the potential tension with other public policy objectives."

Auckland LVRs contributed to prices taking off elsewhere

The RBNZ's also conceding that a move to Auckland-centric LVRs in 2015 may have contributed to house prices taking off in other regions.

"The Auckland regional LVR policy (applied for about a year starting in late 2015) contributed to a spillover of housing demand from Auckland to other regions, despite being effective at addressing risks in Auckland itself," the RBNZ says.

It says the implementation of the Auckland LVR policy was followed by a large decline in house sales for Auckland and in house price inflation from an elevated pace.

"However, it also coincided with a strong pick-up in house price inflation and house sales in the rest of New Zealand, led by regions in the North Island, including the Waikato, Bay of Plenty and Wellington.

"Analysis of sales data suggests there was a significant increase in Auckland investors purchasing in neighbouring regions (Corelogic, 2016).

'The regions follow Auckland'

"That said, the regional markets tend to follow the Auckland market, and low affordability in the super city had probably already driven some home buyers to search for cheaper options elsewhere. Therefore, the Auckland LVR tightening is just one contributing factor to the surge in nationwide housing demand in 2015."

The RBNZ says the experience suggests that a region-specific LVR policy has the potential to displace housing demand from the targeted region to elsewhere, potentially undermining the policy aims at the national level.

"That said, a region-specific LVR policy can be effective in having a braking impact on housing demand and address the concentration of risk in a regional housing market. Whether a regional policy is appropriate depends on how unbalanced the risks are across regions and the capacity for regional policy to create spillovers."

'House prices are not an end goal'

The RBNZ says it aimed to moderate house price inflation because it is concerned that this can exacerbate a future downturn, "and not because house prices are an end goal".

"However, some of the Reserve Bank’s past communications have heavily emphasised the concern with house price inflation, which may have led to a public view that LVRs would only be a success if they stopped house price growth," it says

"...The Reserve Bank would not be concerned about house prices when they are considered not to heighten the risk of a future correction. To put it another way, the long-run level of house prices or housing affordability are not an objective of the LVR intervention. The intermediate aims of LVR intervention by the bank have been rebalanced over time towards strengthening household resilience and mitigating the scale of future economic downturns."

Financial system 'more resilient' to housing downturn

The RBNZ says by mitigating the scale of house price falls during a potential downturn, and limiting the indebtedness of households, the policy has made the financial system more resilient to a housing-led downturn. Declining risk weights for housing loans have offset some of the resilience benefit of LVRs, although the Reserve Bank has adjusted baseline housing capital calibrations to stabilise risk weights and support bank resilience since 2013. The LVR policy has also mitigated the likely decline in household spending and economic activity during a stress scenario.

“By improving the resilience of both households and banks, LVR policy has played a useful role in promoting financial stability during a period of heightened housing market risks,” Deputy Governor and Head of Financial Stability Geoff Bascand said.

Along with the evaluation of LVR policy, the Reserve Bank on Wednesday published other papers that explain the role of macroprudential policy, how the policy is conducted, and its effectiveness at enhancing financial stability. Macroprudential policy aims to limit the adverse impact of boom-bust cycles in the financial system and is one of several ways the Reserve Bank helps to maintain financial stability.

“This work is timely. Macroprudential was established as a new policy function in 2013, and based on the experience of the past five years we’ve updated our strategy for using the tools,” Bascand said.

'It's not about eliminating risks'

“Macroprudential policy is not about eliminating risks for banks and households, reducing house prices, or managing the business cycle. Affordability pressures on the housing market and the rental market require a much broader policy response,” Mr Bascand said.

He said that other macroprudential policy measures could also be used to build additional capital and liquidity buffers in the banking system, so that banks could support the economy under stress. The Reserve Bank has recently consulted on a more prominent role for a macroprudential tool called a counter-cyclical buffer.

Phase 2 of review of the Reserve Bank Act will include consultation on options for the future macroprudential framework. The Reserve Bank’s evaluation of macroprudential policy and LVRs has been completed to assist this review. Bascand said the Reserve Bank believes that it should retain the ability to use macroprudential policies, supported by clear and transparent communication of how they can be used.

15 Comments

This just in: restricting borrowing to levels sensibly related to NZ incomes is not helping investors who have paid a lot for houses to on-sell the same to new entrants to the market.

What does your comment mean?

I like the LVRs exactly where they are right now. They were put in place to protect the public, reducing the risk of a huge bailout if the property market significantly falls.

If FHBs as a percentage of buyers has reduced, I would argue this is because affordability ratios were blown out of the water by hot foreign money ratcheting up prices. The FBB will slowly address this as will lowering rates for domestic borrowers.

I object to this on a few levels.

First, the evidence from the lending data has shown that more lending is going to first home buyers so to present the impact as negative in terms of first home buyers is misleading. It advantages first home buyers relative to investors.

Second, you can’t treat buying a house as success and not buying a house as a failure, therefore more houses bought is a success. Rather there needs to be an analysis of of the long term implications of people buying houses at different prices. It might be advantageous to have less first home buyers buying houses at lower prices rather than more at higher prices with crazy debt.

Finally, where is their inflation mandate in this. High house prices are likely to have long term inflation impacts as people struggle under crushing debt obligations and seek salary increases to compensate. We can already see that with teachers, nurses, paramedics, etc and it’s only going to get worse. Auckland in particular is really struggling because nobody can afford to live their. So there must be an argument that higher house prices have a greater impact on long term inflation than the CPI suggests.

You could come to the conclusion that beyond a certain point high house prices are correlated with lower economic growth - through housing inefficiency (I can’t live near where I work) and crowding out other spending. If the reserve banks approach to low growth is to lower rates which then increase house prices then you could get into a negative feedback loop. It therefore makes sense to have LVRs and have DTIs such that house prices are moderated irrespective of interest rates.

Hi David.

Do we know yet which lender started Reclassifying their first time investor loans as first home buyer loans? It was disclosed by interest.co.nz that one of the lenders had changed the way they were reporting things to the RBNZ. My guess (speculative assumption as they have recently been in trouble) is ANZ and if that were true, then as the biggest lender that would skew the weight of true FHB lending as a proportion of the total. Any further insights on this would be appreciated. Then we can tackle whether the reporting of loans to value are amalgamated loans of different terms as the C31 total ‘loan’ numbers are currently running at over 2.5 times the monthly transaction levels reported by REINZ. (And Some of those will be for cash) So the numbers of new loans against transaction levels are wildly mismatched. So many questions to try and make sense of it all. Any help appreciated

Joe

Derivatives and MBS crushed banks last time - not as RBNZ seems to be curve ball distracting, due to FHB or investor borrowing. People cannot take on more debt now so extend and pretend has reached zenith. Foreign ponzi land price sales now dried up and prices will drop quickly when sales are needed to pay debts and no buyers can be found

They were a debacle and could be considered among the worst policies seen in this Country. As badly implemented as the misguided anti inflation policies of the 1990s, just as destructive. The lvrs deliberately kept fhbs out of the market at a time when they should not have been and it simply created a convenient vacum that investors were only too happy to exploit. Of course I wonder if it was coordinated for the banks who were only too happy to support it all because property prices shot up which was good for increased lending. The lvrs should have been implemented firstly and only at investors. Now look at the mesd we have on our hands as a result. I bought my first home in 2005 on 10% deposit and never missed a beat, its unfair so many other fhbs have had the ladder pulled up.

New builds and Welcome Home loans were always exempt anyway. The problem is that housing prices were allowed to grow too much prior to LVRs. At least things have gone "flat to falling" since then. Best bet is to look for house prices to slowly go down so that more FHBs can afford the debt required to own.

The implementation of the Auckland LVR in late 2015 was followed by the 15% increase of median Auckland house prices with the market hitting record pricing in early 2017. Yet oddly the RBNZ says the implementation of the Auckland LVR policy was followed by a large decline in house sales for Auckland and in house price inflation from an elevated pace. Really? And these are the people running our central bank? They appear to have very tenuous grasp on reality.

https://www.interest.co.nz/charts/real-estate/median-price-reinz

Was the LVR not implemented in the middle of large price rises? Seems a stretch to claim a causal relationship.

And yet that is what the RBNZ did.

Now that the housing market is flat, LVR's should be removed to help FHB but their first home

What does your comment mean?

In a falling (Akld) market LVRs should stay for FHB to try and avoid them getting into negative equity.

Others will argue that the younger generation have time to learn their lesson and work their way out of a negative equity situation, but given the general lack of resilience it might just be better to protect them from themselves.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.