Reserve Bank Chief Economist Yuong Ha says the emergence of the Omicron variant of Covid-19 hasn’t changed the central bank’s outlook when it comes to the way it sets monetary policy.

“It hasn’t fundamentally changed our picture. It’s just reinforced that there are still huge uncertainties and big risks on both sides to our employment and inflation outlook,” Ha told interest.co.nz.

“There is still a lot of uncertainty that we see, but we are starting from a position where the economy by and large has weathered the worst of the Covid storm and is in a pretty resilient position in terms of both the inflation outlook and the employment outlook.”

Asked how effective higher interest rates can be in suppressing inflation, when much of this pressure is coming from supply chain blockages, which might be exacerbated by Omicron, Ha said: “The global shortages are simply adding to a domestic economy that’s already running above potential.”

Ha recognised Omicron will add volatility to market interest rates, but questioned whether it will be enough to “unseat” upward pressure on rates stemming from higher inflation expectations.

Ha’s comments follow the RBNZ last week lifting the Official Cash Rate (OCR) by 25 points to 0.75%, and signalling its intention to keep lifting the rate in small increments for now.

Ha said the RBNZ is “pretty comfortable with where monetary conditions are sitting”.

He noted market rates had increased “quite significantly” between the RBNZ releasing its August and November Monetary Policy Statements, and said this was “broadly in line” with how the RBNZ’s outlook for the economy had evolved.

RBNZ can only sell its NZ Govt Bonds back to the Government

Ha reiterated what the RBNZ said in its Monetary Policy Statement - that the RBNZ intends to reduce the size of its New Zealand Government Bond holdings.

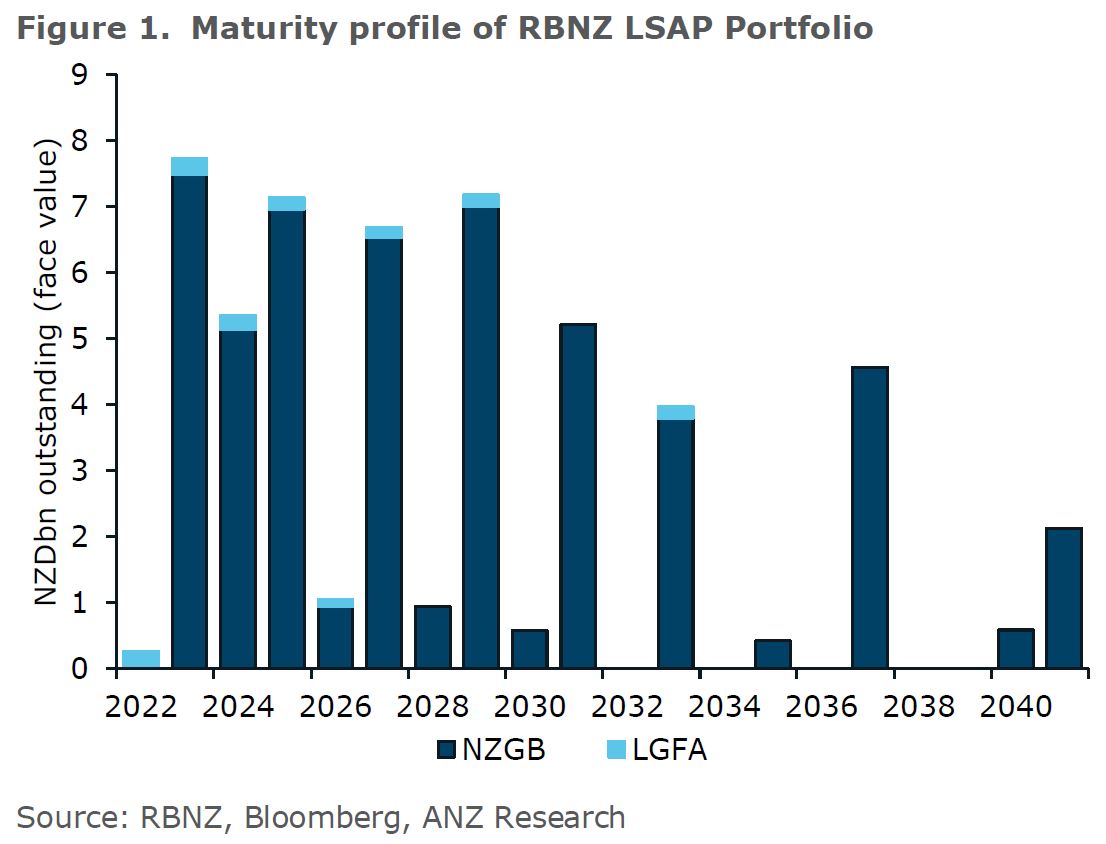

The RBNZ bought $53.5 billion of New Zealand Government Bonds between March 2020 and July 2021 via its Large-Scale Asset Purchase (LSAP) programme, otherwise known as quantitative easing.

It bought these bonds via the secondary market to lower interest rates and support smooth market functioning at a time Treasury’s Debt Management Office was issuing a lot of debt to fund the Covid-19 recovery.

The RBNZ now plans to gradually manage down its bond holdings, all the while using the OCR as its main lever to adjust monetary policy.

It can do so by selling its bonds and/or letting them roll off its portfolio when they mature. It can also reinvest some of the proceeds when the bonds mature to smooth the downsizing of its portfolio.

However, Ha made the little-discussed point that under the indemnity provided to the RBNZ by the finance minister when it launched its LSAP programme, the RBNZ is required to sell any New Zealand Government Bonds back to Treasury’s Debt Management Office.

If the RBNZ chooses to sell its government bonds, it can’t sell them on the open market to the banks and fund managers it bought them from.

Ha explained the reasoning behind this is to ensure the market functions smoothly.

The market could become distorted if Debt Management was issuing new bonds while the RBNZ was trying to offload its massive portfolio.

“It’s about being co-ordinated and understanding our impact on market functioning,” Ha said.

“The idea of whether we actively sell the bonds - we haven’t actually discussed what that would look like yet.”

He said the fact the RBNZ is still working through the logistics of how it could sell the bonds isn’t a sign that it isn’t keen on this option. It isn’t ruling active bond sales in or out at this stage.

QE hard to unwind

ANZ senior strategist David Croy, in a recent research note, said there’s no urgency for the RBNZ to detail its plans for reducing its bond portfolio, as the next major tranche of bonds (worth $7.7 billion) doesn’t mature until 2023.

He said it will be more difficult for the RBNZ to pull off quantitative tightening (QT) than it was to embark on quantitative easing (QE).

“QE was only supposed to be temporary and as it morphs into QT, that will bring with it a reduction in liquidity… It is akin to the “printed money” being “burnt”,” Croy said.

“It is not clear what impact QT will have on the economy, but historic international experience and logic suggest that it will have a negative impact on growth, and that could temper the need (or the ability) for the OCR to go higher.

“In essence, QT could see longer-term interest rates rise (which affect business and the government more), leaving less room for short-term interest rates (which affect households more) to rise.”

Detail on how the RBNZ and Debt Management need to co-ordinate

Coming back to the logistics that Debt Management and the RBNZ need to work through, Croy said, “If the RBNZ decides to go down the road of allowing its bonds to simply roll off, this will have little bearing on NZDM’s [NZ Debt Management] funding needs into the future. That’s because NZDM’s issuance projections already incorporate the need to repay all maturing bonds, whether they are held by the public or by the RBNZ.

“But if the RBNZ does elect to partially or fully roll over its holdings at each maturity date, it will reduce the refinancing burden that would otherwise fall on the market.

“Similarly, the impact that unwinding QE will have on the Settlement Cash Level [the Government’s cash account with the RBNZ] will depend not just on how many bonds the RBNZ elects to roll off or sell, but also on how much cash the Treasury is sitting on, how much it wants to keep on reserve as a buffer, and how much needs to be funded via taxes or borrowing.”

Interest.co.nz also asked Ha about his upcoming departure from the RBNZ, and how the organisation has changed over the 25 years he has been there. Listen to his response towards the end of the video interview.

17 Comments

If the RBNZ chooses to sell its government bonds, it can’t sell them on the open market to the banks and fund managers it bought them from.

Ha explained the reasoning behind this is to ensure smooth marketing [sic] functioning.

"Ensure smooth market functioning" here means "prevent price discovery". Imagine $53b of government bonds suddenly being repriced at market rates.

You don't have to imagine it - the LSAP liability (price paid minus current value) is clearly listed on the RBNZ balance sheet https://www.rbnz.govt.nz/statistics/r1. It shows that the market value of the bonds is currently around $50bn ($5.7bn paper loss).

What the balance sheets don't show you is the savings that the Crown have made by paying interest on bonds to themselves, or the tens of billions of paper profit that Govt made by using LSAP to inflate the price of financial assets during 2020 and early 2021.

Silly question. Can they off load the excess bonds now? Or is that not an option (or just less desirable?) and what happens if they did?

The great juxtapose of outlook- we just need one more événement force majeure.

If the outlook is uncertain; how are we certain in our new policy?

Ha said: “The global shortages are simply adding to a domestic economy that’s already running above potential.”

A domestic economy with 100,000 people looking for work and another 200,000 wanting to work more hours is 'running above potential'. RBNZ are saying here that 300,000 people wanting work or more work is 'too few' - apparently we need more people on the dole for the good of the economy? Like having more unemployed people will persuade the Saudis to reduce the price of oil, or persuade profiteering banks to extract less money from our economy? What a ridiculous way to run a country.

Yeh, that amazing offhand remark leaped out at me, too. What does he even mean? It really typifies the blunt, ineffectual regime RBNZ administers. Useless, misleading metrics like CPI (which tells one nothing about the actual price variation of individual goods and services) beget unhelpful statements like “...already running above its potential”, which in turn results in lusty swings of the sledgehammer (OCR) in an attempt to shave a walnut. In fairness to the Governor, he has pushed back on the Government’s insistence that he should be able to do all of the above in the housing context...

"The govt will need to be the buyer"

Yeah right... the money's gone, frittered away. Now rbnz is suggesting govt buy the bonds where they were the recipients of the cash in the first place. Much like pleading with banana republic's to please start making repayments

Ardern and co will have little to nothing to show in the way of permanent improvements for the billions. Everyone is more in debt, the nation is and certainly first home buyers are. You can bet that Ardern will be crowing about how she got nz through (by locking up auckland for what she said was short and sharp). Now even former PM Bolger is complaining loudly about the wealth disparity. It all makes me angry.

Govt has $37bn sat in the Crown Settlement Account - and a huge interest free overdraft. There is no problem with Govt buying the bonds from RBNZ - but why would you bother when you own the bank and you are not paying any interest on the bonds?

So QE was only supposed to be Temporary, However we haven't thought about how we sell bonds. Not many Reserve Banks ever think of QT and are scared of Tantrums.

See the Feb has not been able to do much QT since Greenspan started this QE mess after the Dot Com failure.

https://fred.stlouisfed.org/series/TREAST

Looks like the RBNZ balance sheet may be large for a while apart from the bonds that expire in the next few years. In the next crisis they can scoop up all remaining Government Bond.

It's way above my pay grade to comment on RBNZ machinations, apart from noting that an anagram of 'omicron' is 'moronic' (ht ZH).

But I do idly wonder how Ha's soothing words re LSAP's unwinding being to Da GubMint alone, nothing to see here, move along, squares with Michael Reddell's view that $5-6 billion has gone Poof.

Edumicate me....

Michael should know better than to pick one line from the balance sheet. LSAP boosted the worth of Govt owned financial assets significantly and will save the Crown billions in interest payments over the term of the bonds purchased. The net impact of LSAP on the Crown balance sheet is almost certainly positive.

This is not to say that inflating the price of financial assets and increasing wealth inequality is a good thing of course, but claiming that LSAP has lost the Govt money is a politically motivated attack line.

Spent $50+ billion without an exit plan, and haven't started talking about it in the year since.

Disgraceful.

Yep sending money is always the easy part. Trying to be more productive to earn it is the hard part, the government have failed to understand this part. But I guess if you have only ever worked for the government, you don't earn revenue, you are given it through taxes so always just get a budget to spend.

Great interview Jenée - as always a good insight into the inner machinations of the RBNZ.

“QE was only supposed to be temporary and as it morphs into QT, that will bring with it a reduction in liquidity… It is akin to the “printed money” being “burnt”,” Croy said.

There is no money in QE.

A recent Bloomberg article described central bank easing with the phrase “pumping money into the economy.” That’s a misconception. Monetary easing is actually an asset swap. The public was holding savings in one form, and now it holds it in another. The Fed buys Treasury securities from the public, and replaces them with currency and bank reserves (base money) that someone has to hold, at every point in time, until the Fed sells its bonds and retires the cash. All monetary policy does is to change the mix of government obligations held by the public. Only fiscal policy – specifically deficit spending – changes the total amount of those obligations. - courtesy of Hussman

The futility of mainstream economics when the RBNZs own chief economist doesn't understand that the bank is part of the government and is on the same side of the governments balance sheet as is the treasury.

It all goes to show the futility and pointlessness of having sovereign currency issuing governments issuing debt in the first place. Just have them pay interest on the central bank reserves that are created when the government spends and the problem then disappears.

No debt issuance to reduce these reserves for interest rate control is then required and the rate of interest can be adjusted according to monetary policy..

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.