The Reserve Bank (RBNZ) reducing the interest rate paid on settlement cash balances it holds on behalf of banks and others below the Official Cash Rate (OCR) doesn't appear to be on the agenda despite a big increase in the cost of these payments following the RBNZ's near $53 billion quantitative easing (QE) programme in 2020-21, and the rising OCR.

Both Treasury and the RBNZ provided advice to Finance Minister Grant Robertson on the idea. However, a spokesman for Robertson says he has not requested any further advice on the issue at this stage. That's despite a suggestion from ex-Bank of England Deputy Governor Paul Tucker that central banks' remits could be tweaked to encourage the implementation of monetary policy in ways that least adversely affect public finances.

Treasury appears lukewarm at best on reducing interest rates on settlement cash balances, suggesting it could give the impression the Crown is undertaking monetary financing, or the funding of government deficits by money creation. This, it says, could impact inflation expectations. And the RBNZ is dismissive saying there's no reason aligned with its objectives to introduce such a policy, which would "amount to a de facto tax" on holders of Exchange Settlement Accounts (ESAS), likely to be "passed through to both [their] wholesale and retail customers."

The RBNZ's ESAS are basic current accounts. An account holder can undertake settlements with other accountholders, the Crown and RBNZ in central bank funds enabling the receiver of those funds to have "absolute faith" in the quality of the funds received, the RBNZ says. It calculates interest for each account holder daily, with account holders receiving the OCR, now 5.25% after a 500 basis points increase since October 2021, on balances. No credit is provided.

The RBNZ says the goal of its settlement account policies is to promote the development of an efficient, open and flexible payments system with a high level of integrity that's robust in the face of financial crises.

ESAS account holders are; ANZ, ASB, the Australian Stock Exchange (ASX), BNZ, Bank of China, China Construction Bank, Citibank, HSBC, ICBC, Kiwibank, NZX, the RBNZ, TSB, CLS, or Continuous Linked Settlement, which operates a global multicurrency cash settlement system known as the CLS System, the Local Government Funding Agency, Treasury's New Zealand Debt Management (NZDM) unit, the NZ Superannuation Fund, Rabobank, and Westpac.

The RBNZ is currently reviewing the provision of settlement accounts, and could make the accounts available to a broader range of financial institutions. A group of non-bank deposit takers - building societies, credit unions and finance companies - are interested, for example, in obtaining a settlement account to improve their competitive position against banks.

Is it necessary to pay interest on all settlement cash balances?

In its advice to Robertson Treasury says the RBNZ paying the OCR on settlement cash balances is a key feature of the implementation of monetary policy. But, it adds, there's a question as to whether it's necessary to pay interest on all settlement cash balances, or whether a zero-interest tier could be introduced.

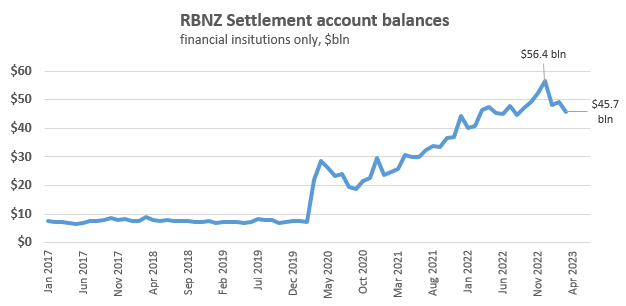

Settlement cash balances were relatively low and stable before the RBNZ launched its large scale asset purchase (LSAP) programme in March 2020 at the onset of the Covid-19 pandemic, averaging around $7.5 billion in the decade up to 2020. The introduction of the LSAP, a form of QE, saw the RBNZ issue a significant volume of settlement cash in order to buy government and local government bonds. The RBNZ's subsequent Funding for Lending Programme (FLP), through which it loaned banks $19 billion at the OCR, further increased settlement cash balances.

The LSAP aimed to lower borrowing costs to households and businesses by injecting money into the economy. It ran until July 2021, with the RBNZ buying nearly $53 billion worth of bonds in the secondary market.

Settlement account balances peaked above $56 billion. They are now declining as the RBNZ undertakes quantitative tightening, or QT, by selling down its LSAP government bond portfolio to Treasury's NZDM at a rate of $5 billion per fiscal year.

Setting a floor

Treasury notes paying the OCR on settlement balances is an important part of monetary policy implementation, setting a floor below which short-term interbank interest rates won't fall.

"Generally, no bank would lend to another bank at a lower interest rate than they could get from the Reserve Bank," Treasury says.

"This model is particularly important if the supply of settlement cash is significantly above what is required by the banks as part of their operations. With a large quantity of settlement cash in the system due to the LSAP, and in the absence of a price floor created by paying interest on settlement cash, the interbank rate would be driven towards zero through basic supply and demand dynamics," says Treasury.

However, it goes on to highlight several examples of central banks creating tiers where settlement cash is remunerated at different rates than the headline policy rate.

"What is important is that the OCR is paid on the marginal dollar held by banks – so that there is no incentive to lend below this rate. For example, several central banks, Denmark, Japan, Sweden, European Central Bank, that have introduced a negative policy rate [taking their OCR equivalents negative], chose to remunerate an initial tier of settlement cash balances at zero whilst paying the negative policy rate on settlement cash above this initial tier. In this instance that was to the benefit of the account holding banks, at zero, the interest paid on an initial tier was above the policy rate. Therefore, whilst it may add complexity to monetary policy implementation, there is a question about whether a zero-interest initial tier could be introduced."

The Reserve Bank of Australia currently has the interest rate on exchange settlement balances at 3.50%, which is 10 basis points below its 3.60% cash rate.

'Beneficiaries of $10.5 billion hard to find'

From a whole-of-Crown perspective Treasury says the RBNZ’s LSAP has withdrawn fixed-rate government bonds from the market and replaced them with floating-rate settlement cash balances. This means the Crown has more floating rate liabilities and has thus been more exposed than it would have been to rising interest costs.

"Our best estimate of the expected direct fiscal loss from the LSAP is approximately $10.5 billion, noting that we expect this has been partially offset by the estimated fiscal benefits of the LSAP through stabilising the NZ government bond market and providing economic stimulus at a time of heightened uncertainty," Treasury says.

It goes on to say it's hard to trace the ultimate beneficiaries of the Crown’s expected $10.5 billion in higher interest payments.

"We expect that it is some mixture of non-resident investors and financial institutions that would have been holding low interest fixed rate bonds if the Reserve Bank had not purchased them. However, the ultimate beneficiary depends on how those investors shifted their asset and liability portfolios more broadly in response to [the] LSAP."

What we do know is who the "eligible banks" were when the RBNZ bought bonds, at a premium, from banks on the secondary market, after the banks had themselves bought the bonds from NZDM. The eligible banks included ANZ, BNZ, Citibank, ASB's parent Commonwealth Bank of Australia, Deutsche Bank, HSBC, JP Morgan, Morgan Stanley, Rabobank, the Toronto Dominion Bank, UBS and Westpac.

Treasury points out that losses stemming from larger exposure to rising interest costs is common across the numerous countries to have undertaken Covid-era QE, given the global inflation that has emerged over the past couple of years.

"As a result, there is now greater questioning, from commentators and academia, of whether these fiscal costs could be avoided by not paying interest on some initial tier of settlement cash balances and whether this would be justified." (See more from Tucker at the foot of this article).

Shifting cost to the banks, or their customers?

Paying zero interest on an initial tier of settlement cash balances would shift some of the cost of funding Crown expenditure on to the banking sector, which would be required to provide zero interest loans to the Crown, Treasury says.

"If the [Reserve] Bank were intending to hold its LSAP bond portfolio to maturity this would have the potential to avoid most of the LSAP losses not already incurred under the indemnity - depending on the size of the initial tier of non-remunerated settlement cash. However, over the next five years the Bank intends to sell its LSAP bond holdings back to NZDM and settlement cash balances are expected to decrease significantly, which will reduce the benefits to the Crown of this change," Treasury says.

"Nonetheless, we estimate that paying zero interest on half of all settlement cash balances would save the Crown approximately $3.3 billion over the forecast period to 2027, based on the forthcoming HYEFU [half-year economic and fiscal update] settlement cash forecasts and the market pricing for the OCR on 24 November 2022, and assuming introduction at the start of 2023/24."

The $10.5 billion is the total expected increase in interest payments directly resulting from the LSAP. This, Treasury notes, is different from the value of the indemnity. This, at $9.2 billion as of October 2022, is the marked to market loss on the value of the bonds.

Suggesting that requiring banks to provide zero interest loans to the government is effectively a tax on the banks, Treasury told Robertson it hasn't assessed the efficiency or fairness implications of such a change.

"Whilst the banks would bear the immediate cost of the policy change, we would want to provide further advice on the extent to which they would be able to pass this on to their customers. If the aim of this policy is to raise revenue, in particular from the banking sector, then there would be alternative mechanisms to consider. As a revenue raising measure, it would give rise to a relatively volatile revenue stream - the savings would vary with the OCR and the scale of settlement cash balances," Treasury says.

Treasury lukewarm at best

Ultimately Treasury sounds underwhelmed by the idea.

"Whilst we tentatively consider that it is possible to change the way reserves are remunerated without undermining the [Reserve] Bank’s objectives, we would want the Bank to provide more thorough advice on the implications for the implementation of monetary policy and any impact on financial stability."

It argues that such a change could have implications on perceptions of the RBNZ's much vaunted independence, and imply the Crown is undertaking monetary financing, or the funding of government deficits by money creation.

"Opting not to pay interest on settlement cash could give the impression that the Crown is engaging in monetary financing or intends to in future. As long as issuance of settlement cash remains under the control of the Reserve Bank, this would be less of an issue, although market perceptions that the government intends to engage in monetary financing could impact on inflation expectations. It is difficult to assess how significant a risk this is," Treasury says.

It goes on to advise Robertson to request advice from the RBNZ if he wishes to pursue this option. Additionally Treasury says it could also provide more advice including on who it expects would bear the cost of any policy change, and any alternatives.

RBNZ dismissive

If Treasury sounds lukewarm at best, the RBNZ is positively dismissive in a report to Robertson authorised by Assistant Governor Karen Silk.

"In the current, and foreseeable, environment, remunerating all settlement cash balances at the OCR is the most effective way to ensure that the RBNZ meets its monetary policy implementation and payment system objectives. Different forms of tiers have been used historically and in different jurisdictions, but this use has been clearly linked to a central banking objective. There is no reason aligned with the RBNZ’s objectives to introduce a zero-interest tier in a positive interest rate environment," the RBNZ says.

"This would amount to a de facto tax on ESAS accountholders, which is likely to be passed through to both wholesale and retail customers, with impacts for financial system efficiency. The RBNZ would lack public legitimacy to make a range of decisions around this policy. The policy is also likely to be in tension with the RBNZ’s objectives; specifically, it may risk effective monetary policy implementation, constrain the future efficacy of monetary policy tools and draw into question our operational independence. These risks far outweigh the modest and variable reduction in interest expense for the Crown. As a result, it is the RBNZ’s continued view that all settlement cash be remunerated at the OCR."

The RBNZ says the purpose of its monetary policy implementation framework is to ensure short-term market interest rates trade near the OCR, and to manage liquidity in the banking system to facilitate payments and settlement flows.

Noting the level of settlement cash has increased significantly during the Covid-19 pandemic due to the implementation of additional monetary policy tools such as QE, the RBNZ tells Robertson this framework is in line with international best practice, given most advanced economy central banks with large balance sheets remunerate all settlement balances at or near their respective policy rates.

"The floor system - where all settlement cash balances are remunerated at the OCR, supported by various facilities for a broader set of market counterparties - is the most efficient way to ensure short-term market interest rates continue to trade near the OCR and that the intended stance of monetary policy is transmitted to the economy."

The RBNZ acknowledges that historically in NZ and elsewhere, different interest rates have been applied to different ‘tiers’ of settlement balances, with tiered remuneration used for a monetary policy and/or financial stability objective.

Examples include:

* Prior to March 2020, the RBNZ remunerated settlement balances above a bank’s respective ‘credit tier’ at a lower interest rate. This was for the monetary policy implementation objective of ensuring a sufficient distribution of settlement cash across institutions. As total settlement cash balances were kept below aggregate credit tiers, essentially all balances were remunerated at the policy rate.

* In jurisdictions where a negative policy rate [negative OCR] has been deployed, some central banks have used a zero-interest tier. The monetary policy purpose of this is to support the pass-through of the lower policy rate to lending rates.

'It would be unprecedented internationally'

In the current context, however, the RBNZ says there's no monetary policy implementation rationale to introduce tiers.

"It would be unprecedented internationally for an advanced economy central bank to introduce tiers for reasons unrelated to their own objectives."

Additionally the RBNZ argues introducing tiers could create other problems, by:

* Reducing the future efficacy of additional monetary policy tools, as market participants would be reluctant to run high settlement cash balances. And;

* Discouraging membership of the ESAS by creating an effective tax on balances, potentially reducing financial system competition and efficiency.

On top of this, the RBNZ argues that if interest wasn't paid on a portion of settlement cash, it would probably only generate modest and variable cost savings for the Crown. The primary way it anchors short-term interest rates in NZ is by remunerating all settlement cash balances at the OCR, the RBNZ says, making some similar points to Treasury.

"Banks and other financial institutions hold deposit accounts with the RBNZ, within the ESAS, and use these accounts to settle interbank payments. Market participants who do not have an ESAS account can still access the RBNZ’s facilities and operations, which allows a broader range of market participants to access facilities and operations priced near the OCR. The RBNZ determines the total settlement cash level."

"Remunerating all settlement cash balances at the OCR is the primary way that the RBNZ anchors short-term interest rates, as ESAS account holders have little or no incentive to lend settlement cash in the market at rates lower than the OCR. This creates a floor under short-term market interest rates," the RBNZ says.

"The framework is robust to the use of additional monetary policy tools [such as QE]. It is operationally simple, as the focus is on maintaining settlement cash above a sufficient level rather than tightly managing changes in settlement cash levels. Under the floor system, as long as there is a sufficient supply of settlement cash to prevent upward pressure on short-term interest rates, variations in settlement cash balance levels have negligible impact on short-term market interest rates or the payments system."

The RBNZ goes on to tell Robertson it has recently committed to continuing to pay interest on all settlement cash at the OCR.

"Not remunerating a portion of settlement cash would create challenges for monetary policy implementation."

'Forcing financial institutions to provide interest-free loans to the government'

The RBNZ does raise the idea of implementing a required reserves regime, where financial institutions must hold a certain level of settlement cash balances to be exempted from remuneration, thereby preventing them from taking actions to lower their settlement cash balances substantially to avoid the penalty interest rate.

However, it says this would effectively mean forcing financial institutions to hold more settlement cash than they need for payment and settlement needs so that they can be taxed on it. Such a regime "would face significant challenges and represent a radical departure" from the RBNZ's current monetary policy and financial stability frameworks. Thus the RBNZ doesn't consider this option feasible or desirable.

"Another option is to not remunerate a small and static portion of settlement cash - a zero-interest tier. This would still have implications for the RBNZ’s monetary policy choices and implementation, as well as unintended consequences for the wider financial system and significant operational complexity. It would also be counter to our public communications about how this framework will operate as the level of settlement cash declines."

"Globally, negative policy rates have sometimes been accompanied by exemption tiering for monetary policy purposes. In New Zealand, a decision on whether to accompany a negative OCR with exemption tiering would be made by [the RBNZ's] Monetary Policy Committee at the time," the RBNZ says.

The RBNZ has never operated a negative OCR and says it expects the OCR to be in positive territory "in normal times."

"There is not a monetary policy or payment systems objective for exemption tiering in a positive policy rate environment."

"Introduction of a zero-interest tier in a positive interest rate environment amounts to forcing financial institutions to provide interest-free loans to the government. This may create a perception that the RBNZ could deploy sub-optimal monetary policy for fiscal purposes, which could harm our ability to achieve our objectives. For example, the RBNZ may be perceived as preferring quantitative easing, and wishing to delay quantitative tightening, so it can maximise the fiscal benefit of unremunerated settlement cash. This would draw into question operational independence," the RBNZ says.

It also suggests a a zero-interest tier would distort incentives for ESAS account holders, who might look to reduce cash balances to a level below their zero-interest tier.

"For example, eligible banks may terminate their FLP loans to reduce their settlement cash balances, which could put downward pressure on short-term interest rates," the RBNZ says.

'Not clear it would address concerns about bank profits'

It argues the "de facto tax" could be passed on to retail customers, resulting in lower deposit rates and higher lending rates, to recoup the lost income.

"This policy would amount to a tax on a specific section of the financial sector, which RBNZ lacks public legitimacy to make decisions around and would be in tension with RBNZ’s other objectives...Using a zero-interest tier to reduce the Crown’s interest expense would amount to introducing a de facto tax on ESAS account holders. This would be a fiscally motivated policy, not supported by the RBNZ’s objectives, and therefore the RBNZ would lack public legitimacy in implementing it."

Meanwhile, the RBNZ argues it's not clear that a zero-interest tier would be an effective way to address any other financial system policy concerns such as bank profitability, or as an attempt to recoup costs from the beneficiaries of LSAP.

"Instead, it is likely to result in greater financial system inefficiencies, negatively affect pricing and participation in financial markets, and may reduce innovation and competition. These outcomes would be counter to the encouragement of a competitive financial system aimed at ensuring financial efficiency and inclusion."

"Introducing a de facto tax within ESAS is likely to disincentivise account holding, undermining these core policy objectives, to the detriment of New Zealand financial market development," the RBNZ says.

It also tells Robertson the reduced Crown interest expense from such a policy change would be variable, modest, and conditional on Monetary Policy Committee decisions.

"Treasury has provided estimates of potential fiscal savings from this policy. We view that it could be possible, but still undesirable, to implement static zero-interest tiers that aggregate to $5 billion of settlement cash balances in total. A static $5 billion tier would be consistent with a strategy of exempting 10% of settlement cash balances initially, but this proportion would increase to 20% over time as settlement cash balances decline. The total amount would likely need to be reduced beyond 2026 as settlement cash balances decline further," the RBNZ says.

"Market pricing for the OCR over the next four years is about 4.5% as of January 2023. Based on a $5 billion zero-interest tier, we estimate savings of about $225 million per year. This central saving estimate is highly uncertain given the ultimate path of the future OCR is unknown."

No further advice sought as Tucker offers a suggestion

A spokesman for Robertson acknowledges he received advice from Treasury and the RBNZ on the RBNZ potentially reducing the interest rate on some, or all, of its settlement cash balances below the OCR.

"He [Robertson] has not requested any further advice on introducing a tiering system at this time," the spokesman says.

Former Bank of England Deputy Governor Paul Tucker is one of the people Treasury is likely referring to when it notes greater questioning of whether the fiscal costs of QE could be avoided by not paying interest on some settlement cash balances.

In a report for the lnstitute for Fiscal Studies, Tucker, now a Research Fellow at Harvard University's Harvard Kennedy School, weighs in.

"Just as the country’s current macroeconomic regime rightly stipulates that government debt management, strategy and tactics, should not interfere with the independent Monetary Policy Committee’s monetary policy, so too should central bankers aim to implement monetary policy in ways that least adversely affect the public finances," Tucker writes.

"That simple statement leaves hanging the awkward matter of who, given the political incentives of finance-ministry debt managers, gets to judge what monetary policy techniques interfere too much with the public finances. The best course, we suggest, would be to put the [Central] Bank under that obligation when making choices among options to which the Monetary Policy Committee is otherwise indifferent (i.e. in terms of the implications for monetary conditions and, hence, the outlook for inflation relative to the Monetary Policy Committee’s target)."

"Had an obligation of that kind existed, public resources could have been saved without impairing monetary-system stability. A carefully drafted version might usefully be added, together with codified hurdles for monetary financing, when the Monetary Policy Committee Remit is updated," Tucker suggests.

25 Comments

If you f*ck with your lenders they might not lend to you in the future.

But who is lending to whom?

The Reserve Bank’s financial market counterparties have ‘standing facilities’ at the Bank. These facilities allow them to obtain settlement cash overnight in unlimited quantities from the Bank at an interest rate 25 basis points above the OCR...

https://www.rbnz.govt.nz/-/media/project/sites/rbnz/files/publications/…

Perhaps we should work on cutting out the middle men and having the equivalent of yesteryear's Housing Corp loans again. Rather than sending billions in corporate welfarism to overseas owned companies.

"It argues that such a change could have implications on perceptions of the RBNZ's much vaunted independence, and imply the Crown is undertaking monetary financing, or the funding of government deficits by money creation".

All government spending involves money creation, how else would the banks end up with NZ Dollar Currency in their exchange settlement accounts in the first place to then purchase the bonds with. The government spends first and any taxation or borrowing must occur after this fact.

It is ludicrous to think that the government can borrow back its own currency and then spend it a second time. It would make no difference to the governments overall liabilities anyway as issuing bonds only changes the format of government liabilities, bonds instead of reserves or swapping one type of IOU for a different IOU. Spending that IOU a second time would only create a new liability anyway just as all government spending does. Only taxation can eliminate the governments financial liabilities. (MMT).

Settlement account balances peaked above $56 billion. They are now declining as the RBNZ undertakes quantitative tightening, or QT, by selling down its LSAP government bond portfolio to Treasury's NZDM at a rate of $5 billion per fiscal year.

Surely, this just circumvents the immediate public insolvency issue if the market value of RBNZ"s QE bond portfolio is below the associated Bank Settlement Account liability, rather than realising it by sale to the market place which is considered QT.

As economist Bill Mitchell describes it, it is just swapping liabilities from the left pocket of the governments trousers to its right pocket and nothing really changes, its all smoke and mirrors and a conjuring trick.

Except the banks are made good at taxpayers expense and get the luxury of underwriting new issuance of the extinguished maturities purchased by Treasury.

Just follow the money trail. The government spends and reserves are created, bonds are then issued and these reserves become bonds. QE, these bonds are exchanged for reserves again, QT, the reserves become bonds again. The only loss for the government is in interest rate margins and which are considerable. MMT suggests that bonds shouldn't be issued in the first place and just pay any interest on the reserves or leave them at zero interest and let the market decide its own interest rates and manage the economy through fiscal policy rather than monetary policy and which is rather a failure anyway by causing boom and bust economic cycles.

We provide a Crown overdraft facility to help the Government manage short-term fluctuations in its cash flows. We temporarily increased the overdraft from $5bn to $10bn for a three month period to 1 July 2020, to assist with the potential for some larger-than-usual changes in cash flows. The overdraft facility was utilised for a short period coinciding with the Government’s April 2020 bond maturity, and the account has since been replenished following the issuance of additional bonds and Treasury bills. Link

It's all left pocket right pocket stuff, they talk as though they are not a part of the government but a separate entity but the government is just lending money to itself, it's all nonsense. Economist Steve Keen explains how things work by using his Minsky software here. https://youtu.be/WtO8cGww_dA

He has a number of videos on YouTube and is well worth following.

by Audaxes | 3rd Apr 23, 8:45am

The RBNZ is ending March with fat balances from its depositors. They have been substantial for many months now. These balances are known as Settlement Cash. And they pay interest on them, at the OCR level. The owners of these balances are the Government (Treasury) and the banks.

If a syndicate of banks underwrites a NZ Government bond issue, the created out of thin air credit is lodged at the RBNZ's Crown Settlement Account. Simultaneously the Bank Settlement Accounts are debited the same amount for the participating underwriting banks, since they are in receipt of the accruing coupon payment from the issued bond. Once the government disburses the underwritten bank credit to eligible beneficiaries' bank accounts, the banks are re-credited the deposit credits since they have an obligation to reward the new private bank deposits. Taxes collected from depositors' bank accounts are lodged at the RBNZ's Crown Settlement Account ledger which causes the Bank Settlement Accounts to once again be debted. There is hardly any need for the RBNZ to credit OCR to the Crown Settlement Account. Link

There are several errors in that article and it revolves around the belief in fractional reserve banking. Bank lending or lack of it makes no difference to the levels of reserves that the banks hold. Banks also do not "underwrite" government bond issues or create credit out of thin air for such. This is all mainstream economic garbage which university courses still teach. Listen to Steve Keens video and study MMT.

Banks also do not "underwrite" government bond issues or create credit out of thin air for such.

When the Australian Government borrows from the banking sector, it holds the borrowed funds as a deposit at the Reserve Bank until the funds are spent. As the Australian Government spends these funds in the economy, such as in the form of JobKeeper payments to businesses, it adds to deposits held by businesses and, subsequently, to deposits of the household sector through employees of those businesses. Link

Bank lending or lack of it makes no difference to the levels of reserves that the banks hold.

Historically, the RBNZ engages in FX swaps with our banks' foreign branches to credit the local branchs with NZD reserves, thus raising USD foreign reserves for the nation . See D10, section FX swaps and basis swaps

That has nothing to do with their lending, banks don't lend out their reserves so any lending will not effect their levels which is what fractional reserve banking say's.

Read this article from Standard and Poor's, https://www.hks.harvard.edu/sites/default/files/centers/mrcbg/programs/…

Banks also do not "underwrite" government bond issues or create credit out of thin air for such.

According to Richard Werner, banks do create money (credit) out of thin air.

The empirical facts are only consistent with the credit creation theory of banking. According to this theory, banks can individually create credit and money out of nothing, and they do this when they extend credit. When a loan is granted by a bank, it purchases the loan contract (legally considered a promissory note issued by the borrower), which is reflected by an increase in its assets by the amount of the loan. The borrower ‘receives’ the ‘money’ when the bank credits the borrower's account at the bank with the amount of the loan. The balance sheet lengthens. Through the process of credit creation 97% of the money supply is created in the UK today (Werner, 2005), and similar proportions apply to most industrialised economies.

https://www.sciencedirect.com/science/article/pii/S1057521914001434

They don't create credit to finance the government is my point, which is what the article was suggesting. Banks use their reserves and then exchange them for bonds, banks don't finance the government.

Gotcha

So rare to get an exploration of the mechanics in such detail - great work Gareth.

The key issue here is that if RBNZ pays less than the OCR on settlement balances, then the OCR and monetary policy itself is undermined.

Why? Because the OCR is the *risk free* interest rate set by RBNZ - and if banks are only getting OCR minus X pts on their settlement balances then they willl accept lower yields on govt bonds... and before you know it your long-term interest rates are heading south.

The OCR sets the floor for interest rates - that's why central banks have to pay it on settlement balances. Now don't get me started on why monetary policy is dumb ass.

Yes, I have read this. It's inevitably incomplete though - far too many moving parts. to track accurately, as Michael would no doubt accept. It is also important to note that if we are back down at 2-3% OCR by the end of the year as we try and pull out of a recession, these losses will evaporate.

The RBNZ should be sacked for the ~$20 billion they lost.

That $20bn was false - Herald have corrected it.

Also these are paper losses - RBNZ are holding financial asset (bonds) that have lost some value. They may well appreciate again through this year as interest rates come down. Also, is anyone having a cry about the ACC fund losing a billion or two (this Govt fund holds around $10bn of bonds). Or the $60bn of bonds held by overseas investors?

Also these are paper losses.

These bonds, issued by Treasury, were originally purchased around par by banks and later sold by them to the RBNZ at a price significantly above par. The higher settlement price is recorded as bank reserves. That sum above par plus the payments of O/N OCR returns above the associated bond coupon payments accruing to the RBNZ is the estimated loss over time, until Treasury completes the buyback programme.

Nothing like shifting the goal posts, what a mess this government and RBNZ have made of this country, the most incompetent ever, on both counts.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.