If the Reserve Bank ever uses unconventional monetary policy tools, its goal will be to ensure a strong and sustained increase in economic activity, with inflation expectations remaining well-anchored on its target mid-point of 2%, says Governor Adrian Orr.

Orr made these comments in a speech entitled Navigating at Low Altitude: Monetary Policy with Very Low Interest Rates. Despite the snowballing coronavirus crisis and interest rate cuts from other central banks such as the US Federal Reserve, Reserve Bank of Australia and Bank of Canada in response, Orr reiterated that the Reserve Bank's next Official Cash Rate (OCR) assessment is scheduled for March 25. There has been speculation the Reserve Bank could make its first emergency out of cycle OCR cut since September 19, 2001. The OCR is currently at a record low of 1%.

ANZ Business Outlook figures released an hour before Orr's speech show NZ firms’ export intentions are the lowest they’ve been since at least 1988 when ANZ first asked the survey question, with firms’ own activity intentions the lowest they’ve been since 2009.

In a long planned explainer on the Reserve Bank's approach to the potential use of unconventional monetary policy, Orr said the Reserve Bank has no immediate intention to use alternative monetary policy tools.

However he did speak of the Covid-19 virus, or coronavirus.

"The eventual economic impact on global supply and demand will depend on the location, severity, and duration of the virus. The optimal mix of policy responses are driven by these same factors. The severity in terms of disruption to economic activity depends on how the virus is contained and controlled, how long this will persist, and the collective response of governments, officials, consumers, and investors to these events," Orr said.

"The Reserve Bank’s Monetary Policy Committee will be picking through these supply and demand issues. We will need to account for international monetary and fiscal responses, financial market price changes (e.g., the exchange rate and yield curve), and domestic fiscal responses and intentions, to inform our response."

"We also remain in regular dialogue with the Treasury to assess how monetary and fiscal policy can be best coordinated. We need to be considered and realistic as to how effective any potential change in the level of the OCR will be in buffering the New Zealand economy from shocks such as a lack of rainfall [drought] and the onset of a virus," Orr said.

"The Reserve Bank is also well practiced in its business continuity roles both for our own team and for our role in the economy. For example, ongoing business and consumer access to credit and liquidity through the banking system, and ongoing orderly access for New Zealand institutions to global financial markets, are a key focus of our mandate. We will ensure a stable payment and settlement system, so that money and cash can flow as usual under all circumstances."

"For us, these monetary policy and financial stability decisions are repeat processes as the duration and severity of events play out. We are in a sound starting position with inflation near our target mid-point, employment at its maximum sustainable level, already stimulatory monetary conditions, and a sound financial system," said Orr.

OCR at 1% 'below neutral rate'

Orr noted that the OCR at 1% is "well below our estimate of the ‘neutral rate’ of around 3%."

Orr said the chance that the short-term interest rate in New Zealand could be 1% lower than now in two years’ time is about 20%. This means that while an effective zero bound for interest rate is far from the most likely outcome in New Zealand, it can’t be ruled out.

"This is not a prediction, just a statistical observation outlining the challenges of setting monetary policy," Orr said.

"The work we have been pursuing has involved:

• Identifying the suite of possible ‘unconventional monetary policy tools’ available to us;

• Defining and making explicit the criteria we would assess these tools with, against both each other and also alternative policies all together (e.g., fiscal policy options);

• Considering the relative benefits and costs of the tools, so as to operate on a ‘least surprise’ basis, and to ensure we are working in collaboration and with the agreement of the fiscal authorities;

• Considering not just the monetary policy efficacy of the tools, but also broader considerations related to our financial stability and efficiency mandate; and

• Ensuring the tools are actually able to be utilised, including working with the important financial institutions that make up our system."

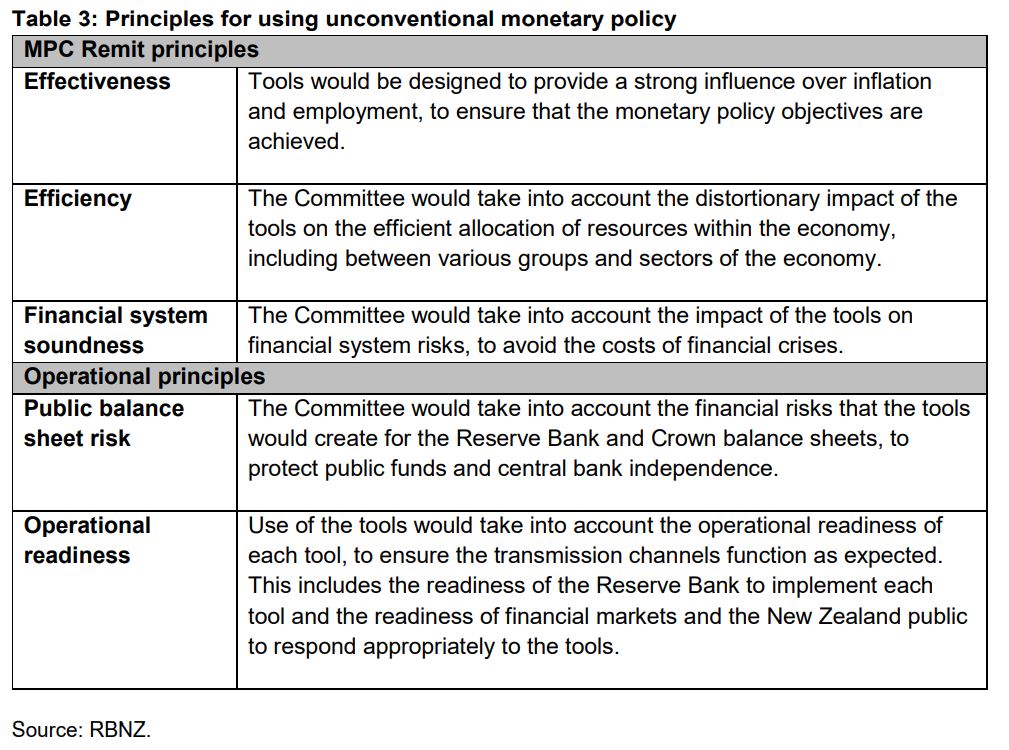

He said table three below outlines the principles the Reserve Bank would use to guide the use of unconventional monetary policy tools.

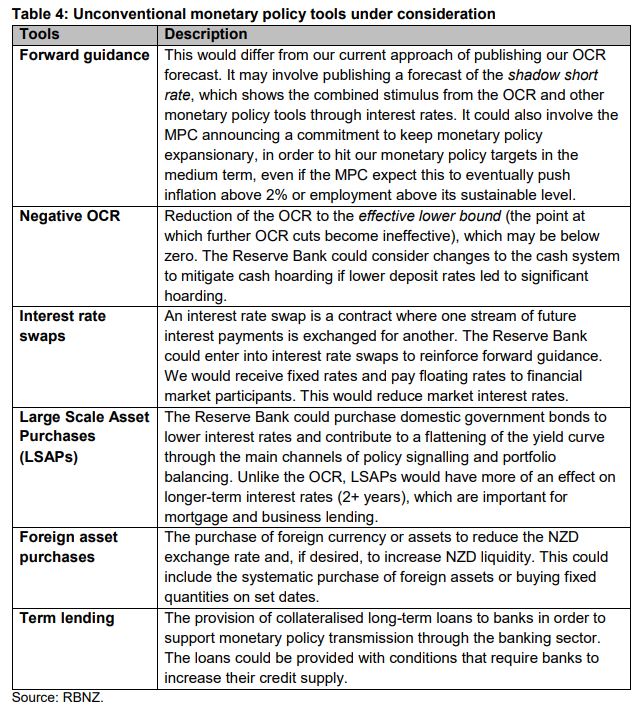

And table four, also from the Reserve Bank, provides short descriptions of the tools themselves.

Following Orr's speech Westpac NZ senior economist Michael Gordon concluded that the Reserve Bank prefers measures that work by influencing interest rates over those that increase the volume of money in the financial system and create a risk exposure on the Crown’s balance sheet.

"The Reserve Bank’s preferences differ in some respects to other central banks. For instance, the Reserve Bank of Australia has said that it views 0.25% as the effective lower bound for the cash rate – that is, the point at which further cuts would not be passed on to bank lending and deposit rates. In contrast, the Reserve Bank believes that the cash rate can go mildly negative before this option is exhausted. How negative was not specified, but we estimate it to be as low as -1%," said Gordon.

"Entering the interest rate swaps market is not an option that other central banks have explored, to our knowledge. However, it reflects the makeup of New Zealand’s financial markets, where the swaps market is more active than the government bond market and tends to act as the benchmark for other long-term interest rates."

Translation to plain English required

Orr said the Reserve Bank will provide full analysis of each of these tools against the principles it holds over coming weeks, so "people can fully understand our thinking and, of course, provide input." He also noted that the monetary policy tools considered all vary as to their effectiveness, efficiency and impact on financial soundness and are at various stages of readiness to be used.

"In light of recent international experience, some of the key considerations we now have are:

• What is the optimal sequencing of these tools if monetary policy is increasingly called upon to stimulate the economy? We are near ready to be able to implement a zero or slightly negative interest rates in our operations, and forward guidance around our future actions is standard practice for us. But we also must decide at what point we use additional tools and in what order.

• What agreement is needed between the Treasury and the Reserve Bank with regard to the use of our balance sheet, and is it materially different to how we manage it now? We are currently working with the Treasury to finalise the institutional arrangements that will enable us to effectively use all of the described unconventional monetary policy tools, if they are ever required. This includes the arrangements for handling the balance sheet implications of unconventional tools. More fundamentally, we also need to ensure we can coordinate an appropriate mix of fiscal and monetary policy responses if so desired.

• What additional policy responses might we need to consider to manage some of the consequences of low interest rates and market functioning? We could consider additional macro-prudential tools and specific market interventions to ensure liquidity and credit flows. But we need to assess how best we communicate to all participating in the New Zealand economy as to the purpose of our actions, and our desired outcomes."

Orr went on to say that New Zealanders are used to the terminology associated with the central bank's current monetary policy activities. Thus it needs "to outline how we could best translate activity in, for example, the interest rate swap market or asset purchases, into meaningful concepts for all."

"We need a meaningful ‘shadow’ OCR concept for ease of discussion. To ensure they operate effectively and efficiently, we also want to ensure market participants (e.g. banks and payments operators) can respond appropriately to the use of unconventional monetary policy tools. While we have done a lot of this preparatory work, we have more to do. These considerations are all well advanced, and we continue to speak with relevant decision makers, market participants, and technical experts over time."

"Any deployment of unconventional monetary policy tools will depend on the prevailing economic conditions, the functioning of the financial system, and the efficiency of the various monetary policy channels. This leads us to currently favour a baseline decision set for the purposes of cyclical demand management, assuming it is needed and superior to alternative policy responses, of:

•Lowering the OCR;

• Using forward guidance;

• Using mildly negative interest rates if more stimulus was needed;

• Considering the use of interest rate swaps to reduce interest rates for New Zealanders,

• Considering asset purchases (e.g., government bonds) for further impact; and

• Utilising a combination of all of the above, as needed."

"We could also introduce term lending activities if the above combined actions proved insufficient and if retail banks are not passing on the very low rates to customers. Foreign asset purchases could also be useful if a specific economic shock was from offshore and resulted in an overvalued NZ dollar. The underlying principle is that we would choose the most appropriate tool or combination of tools, and policy coordination, for the situation at hand. For example, if an economic disturbance resulted in significant disruption to the functioning of the financial system, this would naturally alter the stylised ordering outlined above," said Orr.

Monetary policy needs mates

He also said both conventional and unconventional monetary policy interventions are more effective when coordinated with supporting whole-of-government intervention activities.

"Changes in government consumption and investment, the use of automatic stabilisers, welfare transfers, and varying tax rates all have cyclical as well as structural/permanent impacts on economic activity in a modern economy. This simple observation appears to be one of the most ignored factors globally in recent economic history. A government’s fiscal policies can deliver similar outcomes for short-term inflation and employment as to monetary policy," said Orr.

"However, fiscal retrenchment occurring simultaneously with monetary expansion is akin to one foot on the brake, the other on the accelerator. At times this makes economic sense, but not all of the time. If a government’s fiscal credibility is low, then investors may be more comfortable with a government focusing purely on debt reduction and fiscal restraint. However, if a government’s debt is low, and there are significant long-term benefits to spending and/or investing, then a more expansionary fiscal stance can make sense."

"Here in New Zealand, for example, the Government recently opted to increase and bring forward its infrastructure investment. This action has supported monetary policy in meeting its mandate, increasing activity and employment," Orr said.

The nature of the economic shock authorities would be striving to mitigate would influence the choice of tools, he added.

"A specific supply shock, where goods and services cannot be produced for some reason, may be better managed through fiscal support, both automatic stabilisers and/or targeted intervention, with monetary policy assisting rather than leading. New Zealand’s current drought conditions in regions of the North Island provide an example of a supply shock. If the drought remains relatively region-specific, and/or short-lived, then monetary policy would have a very limited stabilisation role. Any resulting loss of production may be short-term, and automatic fiscal stabilisers and/or targeted government transfers and spending would be more effective at mitigating any broader economic disruption."

"Meanwhile, monetary policy would remain focused on any longer-term impacts on incomes and wealth, and hence inflation and employment pressures. A similar set of considerations confronts policymakers globally at present with the spread of the Covid-19 virus," said Orr.

"The Reserve Bank of New Zealand has not, and still does not, need to use alternative monetary policy instruments to the OCR. But it is best to be prepared. In the event we ever had to use these unconventional tools, our goal would be to ensure a strong and sustained increase in economic activity, with inflation expectations remaining well-anchored on our target mid-point."

The Reserve Bank's principles for using unconventional monetary policy are here.

19 Comments

This is just a rehash of what they released back in 2018. No new update from the RB. Don't even know why they bothered to give as much guidance considering the initial responses came out of the blue at the time in 2018, and didn't have any market impact whatsoever.

Bring on the LSAP, ASAP, just as soon as the shareholders in the major banks have been wiped out then Govt can LSAP into them and refinance them so protecting the NZ citizens deposits, and guaranteeing future stability by control of all banking systems, (not just tugging at the skirts a bit here and there and allowing them to self-rule), while keeping all the profits on-shore and for the benefit of NZérs forever more.

And why would we want to do that?

I see that theft by further stealth is still the best option.

Jargon does not hide this fact.

This used to be a major crime.

Now it is a fact of life.

Where did we go so wrong. ..pray tell?.

Ban on cash hoarding? Hands off my bitcoin sir!

There's hardly any cash to horde compared to bank loan assets.

That's the problem right? People will all withdraw their money and find that the bank only holds 10% of it in paper.

Less than that - view details.

All the proposed tool aims are embedded in current interest rate levels - further reductions in concert with Japanese and European policies have had absolutely no impact on their respective productive GDP growth. In fact the Bundesbank has noted residential real estate accounts for 80% of total fixed asset valuations in Germany - a country once noted for it's prodigious industrial output.

Every time I read about the 2% inflation target, my eyes water a little.

An arbritrary figure, that over the history of time has proven too low, or too high to be realistically achievable at different times.

You can tell there is no particular science to it by the fact it's a round number. If there were any science to it, the target would be something like 1.942% etc.

We should instead target to be in the middle 2 quartiles of OECD countries for inflation, or another target that keeps the RBNZ accountable for inflation, with their targets being in context of global events.

I wish.....

And perhaps include house prices in the measure of CPI inflation. Leaving it out hasn't worked out so well.

I'd have thought that an OCR cut would be too slow to stabilise CPI? Most mortgage lending is on fixed terms that mean a cut to the OCR wouldn't benefit borrowers for a year...or three (if passed forwards at all by lenders.) Maybe it was too much to expect the reserve bank to skip the rate based foreplay and move straight to the intravenous injections of cash into consumers wallets.

I thought the same. But there is a reference in the article to something whereby the Government lends to you indirectly, allowing you an immediate lower interest rate? This can't wait 1-2 years.

Very uninspiring. The RBNZ is going to have to get their unconventional A into G because the market is pricing the breakeven rate of inflation to be ~0.85 over the next 5 to 15 years.

I only see Bailout hidden in plain sight.

Exactly. OBR in election year - yeah right!

Even if rehashed, it's updating & timing are spot on. No surprises. Well, not too many anyway. We've all helped dig this hole, now we have to see if we can dig our way out of it.

Gareth, can you throw any light on the rumour that the Governor of the RBNZ together with Treasury have just advised all Parliamentary parties that they must form a 'War Cabinet' to fight the virus-induced recession made up of the most competent members from all parties.

If so, it will be interesting to see who is chosen.

"...Considering asset purchases (e.g., government bonds) for further impact..."

Does that mean NZ govt bonds? Is that quantitative easing or does he mean buying existing bonds and borrowing in order to do that?

Who knows, either way its crazy!

If 0.25% is the effective min in Oz, how on earth do they see that -1 is the min in NZ.

Crazy as well!

Crazy 3 is how they think that can mitigate cash hoarding. Its already happening now!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.