Prime Minister Jacinda Ardern is avoiding wading into the debate over whether the Reserve Bank (RBNZ) should reimpose restrictions on bank lending against both investor and owner-occupier property, or just investor property.

RBNZ Deputy Governor Geoff Bascand last week clarified the RBNZ wanted to reinstate the same loan-to-value ratio (LVR) restrictions it had in place earlier this year.

These require at least 80% of a bank’s owner-occupier lending to go to borrowers with deposits of at least 20%, and at least 95% of a bank’s investor lending to go to borrowers with deposits of at least 30%.

Asked on Monday whether she'd be comfortable with restrictions being put back on both investor and owner-occupier lending, Ardern said: “I need to allow the Reserve Bank to make those decisions…

“I am pleased to see that there has been a particular focus on investors and that three of our mainstream lenders have already moved on that in anticipation of likely moves by the Reserve Bank.”

Finance Minister Grant Robertson a couple of weeks ago gave media the impression he was putting pressure on the RBNZ to rein in sky-rocketing house prices on the back of its looser monetary policy. He specifically said he had brought forward a scheduled meeting with the RBNZ.

Then, following the RBNZ announcing it would consult on reimposing restrictions from March 1, rather than May as previously promised, Robertson voiced his approval.

“In the current circumstances this is a sensible decision. I welcome it and I would like to see the work happen as soon as possible," he said.

ASB last Thursday announced it would immediately start requiring investors to have a 30% deposit, rather than 20%, as per its own policy. ANZ followed, saying it would adopt the same approach from December 7. Westpac never lifted LVR restrictions when the RBNZ removed them on May 1.

National’s shadow treasurer, Andrew Bayly, told interest.co.nz he was concerned reimposing LVR restrictions could disproportionately disadvantage first-home buyers.

He didn’t go so far as to say they should only be imposed on investor lending, but said it would be "disappointing" if restrictions were imposed on first-home buyers. Bayly said investors should be targeted.

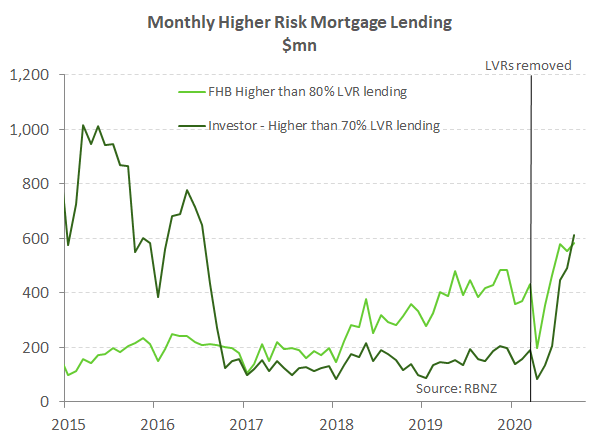

This graph, put together by Kiwibank economists, using RBNZ data, shows there’s been a larger rise in high LVR lending to investors compared to first-home buyers since the LVR restrictions were removed, but the uptick in the latter is still notable.

RBNZ data also shows there’s been an increase in the portion of bank loans to owner-occupiers, including first-home buyers, who are taking out a relatively high amount of debt compared to their incomes.

This table shows the increase in the percentage of mortgage lending to borrowers with debt worth more than five times the value of their annual income. This debt-to-income ratio is considered high-risk by the RBNZ:

| Group | Sep 20 | Jun 20 | Sep 19 |

| First-home buyers | 43% | 41% | 36% |

| Other owner-occupiers | 38% | 36% | 30% |

65 Comments

Total lack of imagination or fresh thinking ... transformative?? To quote Jacinda Arend "I will let you decide"

"Let's keep moving! (Nothing to see here)"

Or should their line be "Let's rule it out"? Since they're really good at quickly and permanently ruling out any and every solution to the biggest crisis NZ is facing.

Ardern and Robertson look alarmingly like a couple of opossums frozen in the headlights of history.

JA is passing the buck as she too is now reaping the rewards of rising housing house price otherwise why not act as Mr Orr has made it very clear that he supports and love rising house price as that is the only solution he has to avoid depression.

Asking someone like Mr Orr who firmly believes that rising house price is must for the economy will not act otherwise instead is and will try everything to pump up the house price.

If interested in reintroducing LVR, WHY THE DELAY....as want the ponzi to continue and does not want the party to stop and by March next year though may introduce LVR but will find some other tools or measures to support the rising house price and is nothing wrong with Mr Orr as his thinking and interest is in rising house price and has made it clear.

Still PM wants to pass the buck....For she too is in favour of ponzi and is coming out with statement as she is being forced to do and no harm in giving sound byte.

Westpac economist agrees that a wealth tax might be the solution to the rising wealth inequality in NZ.

Stephens said he was personally in favour of a capital gains tax although a land tax had wider parliamentary support

https://www.stuff.co.nz/business/money/300160055/a-wealth-tax-is-coming…

Unsure how a wealth tax would be a 'solution' giving the government can't actually intervene in any meaningful way to improve housing or poverty (or at least doesn't want to), so unless you want to drag the average down by just making the upper-middle (we know the top bit won't pay it and even the Greens admitted that in their policy proposal) then it's hard to see what a wealth would achieve.

A land tax calculated on the basis of infrastructure 'value capture' could serve as a better solution.

The tax revenue, in full or partial, should be transferred back to the infrastructure asset owner (Waka Kotahi, KiwiRail, local government, etc.) to fund yet more capital investment in infrastructure.

Hang on, we've been paying taxes for stuff like infrastructure for yonks. Politicians have just chosen to spend that money on vote-winning stuff that isn't basic urban development (rapid transit, water treatment, etc). There's no moral basis to charge taxpayers again for something they paid taxes in good faith to cover already. Otherwise it just becomes an additional cost for the government to do the bit we already pay the government to do.

I’m not a fan but I am happy the Gov is not interfering. The Gov should not be making tactical level decisions, they need to remain strategic and leave their departments to make their own choices based on Gov intent.

That has been a favourite line of fence sitters since the 1980s "that is not my role its outside my mandate you will have to ask the xyz dept". But why take that position and then start giving hints.. why did Arend make any comment

Your thinking is too shallow. the Government needs to regulate residential housing and the rental market. The last count I saw was around 40 k houses sitting empty in Auckland, effectively land banked, that has likely increased now. The 'free market' has and is failing the people dismally, while making a few very wealthy. Tax is not the answer, regulation is. The Government needs to fully regulate the market, and if they don't the final outcome will be tragic.

There is no free market housing market in NZ, or maybe anywhere else on the planet. Everything, other than prices, are fully regulated. You want prices regulated? the government to determine the value of houses and rents? in absence of a market what is the price setting mechanism?

By 'Free' it means lack of Government regulation, and the market is not regulated in any way. There is no regulation on rents, only superficial at best on quality, there is no regulation on what a property can be used for (i.e. no ban or controls on being held empty), no licencing of land lords, and the limits on foreign buyers are only new and don't impact existing foreign owners, plus I have heard comments that there are still foreign buyers active in the market so there may be ways to get around the current rules. Building standards are crap compared to Europe. So no I do not accept that the housing market is regulated. With effective regulation the price of properties will drop, hopefully significantly to allow current generations to buy in without crippling debt. On top of all that land lords are subsidised to the tune of billions every year. Decent regulation will save this country huge amounts, have a dramatic impact on poverty, especially child poverty, and reverse current homelessness trends.

Dr Cullen reported in Stuff this morning says it’s bad enough when rungs are added to the prices of houses at the top of the ladder, but it’s even worse when those rungs are taken from the bottom of the ladder. an awkward personality in politics to be sure, not my cup of tea, but as in this instance, quite capable of the nicely said

Well put - that's have I've being seeing it. The whole ladder keeps moving up and out of reach of those at the bottom. Its only going to cause more poverty and more taxation longer term to support those left behind - yet we give special tax treatment to those who appear to be causing the problem (property investors).

"yet we give special tax treatment to those who appear to be causing the problem (property investors)" - exactly right, I agree 100%.

The amount of welfare and subsidies that the productive part of NZ provides to landlords (if we consider all housing subsidies, the lopsided taxation regime, the ultra-loose monetary policy etc), is simply eye-watering.

Build more .... end of story... fhb homeowner borrowing has been high and climbing for sometime, and you didn't say anything late last year or early this year about that or did you. Yes as investors we bought a property in Sept.... three houses on separate titles all side by side, where the owner wanted them all sold so he/she put them up for sale together as one lot. Fbh shut out. Yes we could sell one or two to fhb but why would we if we got a good deal

The Government got elected on the basis that it was a bloody outrage (indeed, even strongly implied that it was corrupt) that no one was making wide-ranging, sudden changes to fix housing. For them to now just go "Oh, we'll trust the process" is walking back even further from their 2017 sabre-rattling. Actually doing something is less important than being in power.

The Government is there precisely to do so, leaving the RBNZ make this important decisions, when it is not a democratic institution says a lot about the type of political system we currently have.

Who then sets the mandate for the RBNZ, given they're policy has such wide and deep impact, I think it's only right they take at least a vague direction from the elected government of the day. No?

Percentage of FHB has gone up as are been forced by emotion /FOMO to buy anything by borrowing much over what one should be. FOMO has taken over sound decession making and is all driven by FOMO.

One should also look at the percentage to income that FHB buyers are borrowing....it will be much more than 20% compare to last year (Even Last year Was High) though with low interest rate for now moratge may be similar or slightly higher but are deep in depth now.

Short term thinking is leading to path of disaster unless government or RBNZ puts in permanent stimulus and support to people on mortage to avoid the inevitable fall in housing prices.

RBNZ governor must be looking at his term just like our favourite PM looking for next three year as none have vision required to lead the nation.

What is 'sound decision making' for FHBs when no one is ever going to do anything that might mean prices drop? Just sit on the sidelines, get old, get turfed out of rentals year after year, move your kids from school to school, waiting for... what, exactly?

So, where exactly is the increase in the house prices happening ? Owner occupied or Rental properties ?

Who are those bidding high in auctions ? FHBs or Property Investors ? Is the increase happening in Central/Preferred suburbs or at outlying areas ?

Without having such data, how can they introduce higher LVRs for all property purchases uniformly ?

Would it be better to impose higher LVRs for properties of a certain value and above, to protect FHBs ?

Let us have a good analyis...

If you had a low price bracket where LVRs didn't apply, unless it was very high (like LVRs on houses above $3m but not below), them you'd force demand into the lower priced bracket, forcing the prices in that bracket to rise drastically. That would ultimately hurt FHBs.

The l ratio stipulated can be a moving thing, not fixed. Also, Banks would know the status of the buyer, FHB or Investor. So they can be given discretion to waive the higher LVR for FHBs.

Jacinda - 'not my mandate, let's keep moving'

Yes “nothing to see here! Let’s keep moving”

Time to stop the pretence it's not about demand. So. A population policy and a halt to immigration.

But they are too weak.

Technocracy and second hand government - as in, I listen to experts and finance is not our field.

So, as per usual, democratic "mandate" means nil compared to sacred sacrosanct areas fenced off from any State sponsored intrusion. Pathetic abdication. 3 years to go til national elected.

Don't worry, I'm sure there'll be some sort of announcement about something that doesn't go anywhere like the petrol pump price announcement which definitely wasn't a diversionary tactic at all to take the heat off Jacinda and Robertson having no answers and not really being too fussed about it.

Ardern is not fit for purpose.

Housing is a national tragedy and she doesn't give a flying f***.

I had big hopes with her, but unfortunately I was wrong. I thought that she was quite genuine. Now more and more I think she is just a great talker and is just facade. She is just a John key with a compassionate smile but behind that, it is totally hollow.

I still think she’s a wonderful person and my vote for her was well placed. Let’s not be negative. Just accept what she can do for us as the best possible outcome. Kismet voted by more than half of all voters.

I'd already given up on Labour over house prices prior to the election. I did hope that maybe with such a majority they might actually decide they could do things now, but seems not.

I know people who still haven't forgiven the betrayals of the Fourth Labour Government. I don't think people will forgive this betrayal either.

I am reliably informed that house prices have risen, quite substantially so over the past year, indeed the important people at both the RBNZ and banks see a further 10 percent rise over the coming year. As a savvy investor, having crunched the numbers , I note the values of my many many existing properties have risen same, or alternatively, (having considered additional property ) my primary residence has risen same, I also note that my overall existing LVR position has improved wonderfully. My question would be , will moving the goalposts on the LVR deposits have any effect , given that my underlying financial position has improved considerably , ( all things being equal) and I find that I would be currently in a stronger position to purchase additional property, irrespective of any LVR changes. .

Correct, this level of an adjustment to the LVR's will make no difference.

It would make a difference at the margins. Slowing down the increases, not stopping them.

What a leader, promised and voted in on the basis of making the hard decisions on a 20 year housing crises; Ability to borrow at lower interest rates does not achieve house affordability; but the reverse and the failed tinkering on periphery plans end up costing the middle class tax payer and promotes further inequality.

It's hoped the media and bloggers continue to remind JA on the failed policies and dis-ingenious efforts to address their number one mandate to make those structural changes for which Labour has had plenty of time and a majority in parliament to now do so.

By doing this she's throwing new owner occupiers under the bus at the interest of current investors and asset holders who will rid of their investments as soon as they get the chance given the current outlook. Even banks have said LVR restrictions must be re-instantiated, since by not doing so they need to compete with each other for high risk loans to avoid losing market share, why the Government won't support it escapes any logic.

I see - everyone agrees runaway house prices are a problem. We now have excellent evidence that LVRs have an effect on house prices. The Reserve Bank controls LVRs, and house prices are outside their mandate. House prices are within the government's mandate, but they consider it outside their role to interfere with Reserve Bank decisions.

So basically even though we know LVRs affect house prices, there is NO ONE who considers it their mandate it is to act on this fact.

But this type of behaviour is true of nearly every bubble in history.

Its only afterwards that everyone thinks, how could everyone collectively be so stupid? (and that includes the general population, the central bank and the governments)

One day she will be forced to publicly accept that the core Labour theories of compassion, reducing poverty and supporting those in need are completely blocked/negated/obliterated by the endless flow of wealth into the pockets of property owners.

been just over a month since Labour got the vote to go back in by themselves and the moaning from those who voted them in is starting to ramp up as they discovered they have lack of in-depth polices and inequalities between the have and the have nots keeps growing. Maybe they should of looked a bit deeper and past the "lets keep moving" slogan.

Why do you assume the people complaining about their lack of action voted for them? I certainly didn't, for precisely the reasons you point out. In any case, the fact that you did vote for a Government doesn't mean you cede all rights to complain about the stupid things they do.

First Robertson and now Adern. Directionless. No improvement on social inequality, housing availability and relied on the joker of covid to decrease immigration. Big on rhetoric and light on action as usual.

Just goes to show that this neoliberal economic system or way of thinking is broken and lacks an ethical backbone. It requires that the rich become wealthier and inequality increases to save itself, only to make things worse for more people in the future! What a system!

Yet we keep backing it because enough people are still convinced that they can 'get ahead' of their brothers and sisters within the community by taking on more debt than them, and taking rent from them and subsidies from the government.

From a man who knows....

Former Finance Minister Sir Michael Cullen has fired a broadside at both the Government and the Reserve Bank, saying the bank’s extraordinary money printing to prop up the economy has “little measurable positive effect”, and is out of step with the Government’s broader economic goals.

https://i.stuff.co.nz/national/politics/300160059/reserve-bank-fuelling…

Looks like PM has been binge watching again..

https://youtu.be/3zuRkQSx5gs

Life imitating art.

First up Henry, he is saying nothing that other, more qualified people have not already said, plus he is rather stating the obvious. Although he says the RBNZ program 'may' exacerbate the housing crisis, rather than 'is' as Orr has already stated. This topic has already been thoroughly debated in this forum.

As to 'knowing', he clearly demonstrates that while he can identify the problem, solutions are still beyond him. He still believes, as do many others, that building more houses will solve the problem. But more houses are being built, although admittedly not at the rate or amount needed, but prices are not responding to this, but other issues in the economy.

However there are parts of his opinion piece that are quite eloquent and well put.

Declaration; I cannot stand MC. In his terms as Finance Minister when the current housing issues started to be evident, he twiddled his thumbs and denied there was an issue. He was arrogant and conceited. He hides behind a 'Doctor' title but holds a doctorate in history not finance, and is therefore no more qualified than anyone on the street. Rather well known for his "rich pricks" comment without the understanding that for the majority of Kiwis he is one of them!

It's good the poor are stupid, or she wouldn't have any voters

"Whoever despises his neighbor is a sinner, but blessed is he who is generous to the poor."

That's my thinking .. sometimes lol. I understand your frustrations. Being poor doesn't mean someone is stupid though. Some people just aren't overly involved in politics. They want to be good citizens and neighbors. They try hard to raise good children and concern themselves with providing for them the best they can .. even working 2-3 jobs - that love is beautiful.

Hindsight is like foresight but without a future. Moving forward, there are very smart AND wealthy people whom are constantly making mistakes and destroying themselves ..

Give me a person; political or NOT .. someone WISE with wisdom. Wisdom ISN'T knowing everything, or superior mental ability, no no - wisdom is DOING the Right Thing even when it's hard. Give me that over a rich person any day!

Rosenstein

What an awful comment. Funny when you look at the shit-show on the other side - called 'The opposition' you would really have to ask - who are the stupid ones.

Probably the 33% that voted for a brand, rather than a set of policies or good leadership. At least those who fled to Act had some sense.

You're right sorry about that.

Everyone's stupid. Better?

If this government had any balls, it would immediately change the RBNZ mandate and make it EXPLICIT that strict control of asset bubbles (like housing) is a crucial component of its mission.

Ensuring the stability and soundness of the NZ financial system is already part of the RBNZ mandate, therefore Orr & Co. are already in breach of it.

However, making it very explicit would bring to the surface the incompetence, shortsightedness, recklessness and hypocrisy of the RBNZ, and force them to act appropriately.

But hey, let's be "kind" and sacrifice the structural soundness of the NZ financial system, the productive part of the NZ economy. and the new generations, to the altar of the big NZ housing Ponzi scheme. I am pretty sure that when market forces ultimately reassert themselves and the housing Ponzi starts crashing down, Orr and the current government will be nowhere to be seen (and National has had a very poor history too, when it comes to housing).

Local councils need also be given a similar mandate when it comes to land allocation and planning.

Very true. Good point.

A very quick way to cool down the market would be an immediate ban on sale of existing houses to investors.

Let them pay for infrastructure and new built

That would be too authoritarian. But a ban on banks lending to property investors other than for new-home builds wouldn't go astray. Let the landlords go to the non-bank lenders.

Great comment fortunr

Well, our housing market is like musical chairs - when the music stops, more and more people are left holding their d**k. (game rules vary)

With an unlimited amount of money from the RBNZ, chasing a finite number of chairs .. people will bid all they have for just the CHANCE to sit down.

As for Labour, Jacinda has been in parliament for what .. 12 years? Time for her to go as fresh thinking is needed. U-Turn Ardern isn't willing to try anything new .. us Kiwis want new, hopefully Jacinda gets rolled and better leadership emerges.

So disappointing to see Ardern shy away from reining in house prices. The people elected her and labour to sort out the housing mess and not the reserve bank governor but she is simply passing the baton on to Mr Orr.

It's comes full circle and Orr just hands the baton back to Ardern.

ABSURB.

In a land of:

a) rising real house prices since the 1970s/80s

b) inelastic RMA

c) very limited wealth or capital gains taxes,

d) lack of a population strategy

e) falling interest rates since the 1980's boosting asset prices,

monetary policy is a sledgehammer and simply driving house (LAND) prices to even more unsustainable levels.

Sorry, but given the huge systemic distortions above the argument for the government not to be directive towards the RBNZ holds absolutely no weight.

The pumping up of real LAND prices since the 70s/80s is the most unproductive use of capital possible (we just get rich real estate broker middlemen who add nothing to the economy) & part of the reason NZ living standards have fallen substantially over the same period.

The government could:

a) ban recourse mortgages to rebalance the risk between mortgage lending and business lending

b) require banks to reweight the risks between house lending and business lending

c) either through discussion or legilisation require the RBNZ to set certain LVR or income related levels for mortgage lending

The government must:

- fix the systemic distortions a)-d) above.

The housing crisis has been caused by 2 reasons. First, uncontrolled immigration which has been letting a net 50-60k into the country year after year. Second, super low interest rates. The first is controlled by successive governments and neither labour nor national want to reduce it. The second has no one willing to own it. The reserve bank says house prices is not their problem. Adern says it is not her problem either - interest rates are up to the RB. Both Adern and Orr will judged as overpaid buffoons by future historians.

Spot on - Orr causing the problem; Adern won the election to govern on the key isssue/policy of solving housing affordability and neither of them accept responsibility for their actions or provide solutions as promissed and to top it all off where in the biggest reccession ever, what a joke, particularly on the tax paying middle class and future generations. Thats politicians and bureaucrats for ya.

Strange bedfellows Jacinda and Adrian...I mean government and central bank. Unfortunately, like our West Island cousins, we are making the same mistake with conducting monetary policy in a willfully ignorant manner. When the governor himself admits to a 'least regrets' approach, the implicit admission is that he's willing to throw savers (those actual accumulators of capital) under the bus in order to redistribute real wealth to borrowers via negative real rates.

Instead of showing a bit of courage and owning up to a weak ploy to push down the NZ dollar in an effort to engineer a phantom gain from foreign trading terms, said governor comes up with some hokum about 'wealth effects' encouraging people to spend more. Naturally there is no consideration that people reliant on fixed incomes (or saving for a house) will tighten their belts more in response to a policy of financial repression.

All they need is tuppence worth of brains to realise that property prices will tend to rise inexorably when the marginal buyer is a 'prices only go up' investor which can debt fund a high proportion of the price at a rate lower than the rental yield. The only real limiting factor is when the price gets high enough to compress the investor's ROE back down to an indifference point (hint: which is very low because of where alternatives like term deposits sit).

This whole situation is more cringe-worthy than 'Dumb and Dumber'.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.