Change is nigh across the Tasman with "Australia no longer able to bank on the positive wealth effect from financialisation of the abode," Jarden analysts argue.

In a research report Jarden Australia-based analysts Matthew Wilson, Christian Mazza, Blake Dowsett and Daniel Bui detail what they believe will be a step change for Australia's major banks, parents of New Zealand's ANZ NZ, ASB, BNZ and Westpac NZ, and the country's economy.

This follows reforms to capital gains tax, negative gearing and trusts unveiled in May's Australian federal government budget.

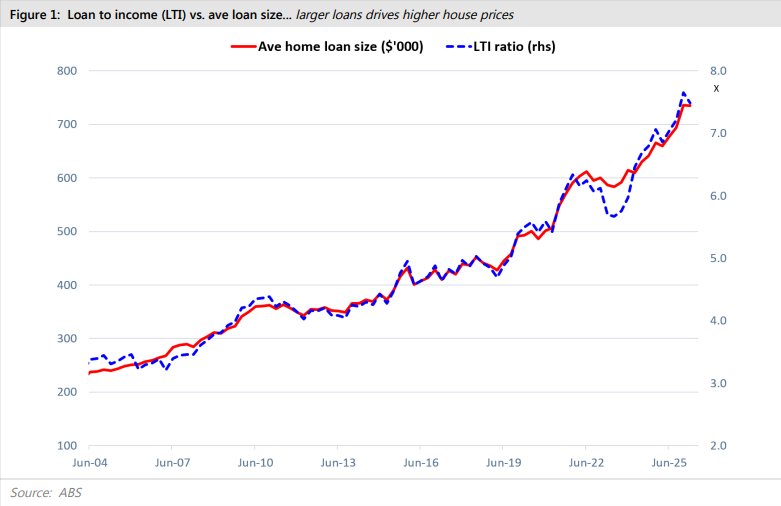

The analysts point out if you walked into a bank branch in the the early 1990s, a bank manager would've happily lent you three times (3x) your income to buy a house.

"Today, the ratio is around 8x and sometimes closer to 10x ," the Jarden analysts say.

"House prices have risen for a few reasons; population growth and insufficient supply but, ultimately, it was the willingness of the bank to lend more and more as a multiple of income that drove the surge in house prices, in our opinion."

"It was the literal 'rivers of gold' for bank earnings - low credit risk, about two basis points, low capital intensity, with 200 basis points of spread and double digit growth."

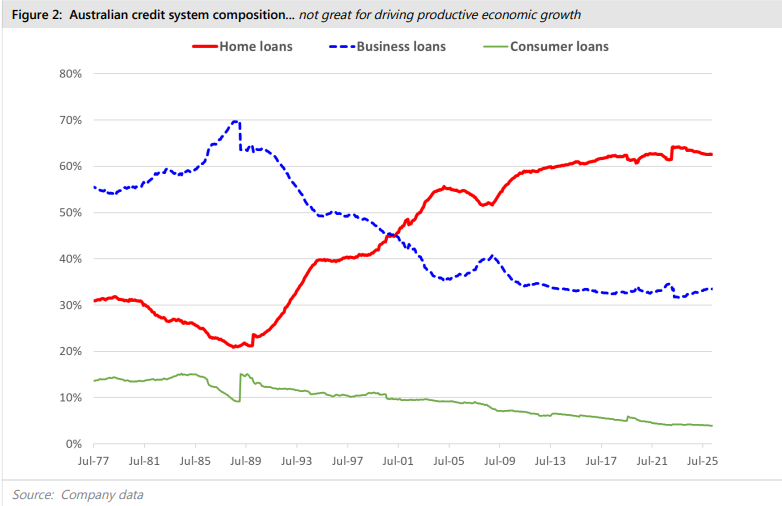

The analysts note home loan risk weights started at 50% in the 1990s, troughing out at 14% in 2014, when Westpac had 51% of its home loan book on an average risk weight of just 4%. They note the average today is about 23%, with ANZ at 24%, ASB's parent the Commonwealth Bank of Australia at 22%, BNZ's parent National Australia Bank at 26% and Westpac at 20%. This follows changes introduced by the Australian Prudential Regulation Authority in 2016, and implementation of Basel III international standards.

Risk weights are used to work out the minimum amount of regulatory capital a bank must hold. The capital requirement is based on a risk assessment for each type of bank asset or loan.

The low risk weights on home lending "triggered the financialisation of the abode and the positive wealth effect," the Jarden analysts say.

"Misguided economic policy in our mind, directing bank capital to non-productive uses, but high bank return on equity, and encouraging households to spend debatable paper wealth."

"Over the last 30 years, A$2.4 billion of credit has been lent to fund home buying: A staggering 2.2x the amount, A$1.1 billion, extended to productive uses in business," the Jarden analysts add.

"And now with the stroke of the policy pen, [the] jig might be up. Indeed, policy change has an uncanny knack of being a negative catalyst."

They note a similar policy change in 1985 had a negative effect, albeit this was reversed due to "political expediency" in September 1987 before the Federal election.

"Rents had ballooned and home loan growth collapsed."

What about those dividends?

Now the Jarden analysts see a major "lift in capital strain" for the big banks, raising the question of whether dividend payout ratios at said banks are too high, having been set when home loan growth topped corporate lending growth.

ANZ's dividend payout ratio is 60% to 65% of cash net profit, CBA's 70% to 80%, NAB's and Westpac's 65% to 75%.

The analysts suggest there may now be a sustained skew to corporate lending for the banks, greater movement of the banks in tandem with the broader economic cycle, and increased interest rate risk for them because; "there is no free lunch from increasing the hedge on free deposits and equity when interest rates rise and remain elevated."

"We see a change in mix of required macro capital allocation. Perhaps one of the reasons for Australia's productivity slump is a lack of productive investment over three decades. The economic need to reindustrialise, re-shore and harden essential infrastructure across energy [both] generation and transmission, information technology - compute/data centres, and civil/ defence [being] roads, rail, ports, accoutrements inter alia, structurally transforms our credit consumption from capital light to capital intense."

"Materials and matter may now matter more. This may also collide with Australia no longer able to bank on the positive wealth effect from financialisation of the abode," the Jarden analysts say.

"This regime change might be more inflationary and thus require a higher level of interest rates."

Given all this, they see a slow down in home loan growth and an increase in corporate lending growth over the next three years.

"We'd expect grandfathered negatively geared residential property investors to consider drawing down available lines and/or migrating to interest only which would slow rate of effective [bank] book run-off...Whilst major bank share prices have retraced by [about] 20%, we think they remain expensive at [about] 18x PE [price-to-earnings ratio] and not priced for any negative regime change," the Jarden analysts say.

Figures 1& 2 in this article come from Jarden.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

5 Comments

Good read. Ever greater Bank credit and acceptance of low equity and high debt multiplier did indeed propel house prices to stupid levels in Aussie and NZ. Don't forget the bank profits to boot.

Its no wonder its referred to as a ponzi.

the end result will be credit rationing

This could result in massive fall in the over inflated Australia housing market, which continued to grow after 2021 when the NZ market peaked and began to fall. Australia is no longer the drawcard for young New Zealanders that it once was. Those who moved there recently were attracted by higher wages, but those wages had no chance of keeping pace with Australian house prices. So your long term prospects in Australia aren't that great.

By contrast the NZ housing market has remain flat which has given first home buyers a decent chance to save and actually catch up. They will be far better off staying in NZ. Now we need New Zealanders to start having children to boost our population to stop our reliance on immigration.

While this may be the case. Many are more than happy renting in desirable places there (was always pricey to buy in SYD, central MLB etc), and bolstering the savings with high wages and lower transportation costs to commute.

Young kiwis in their 20's likely didn't head there with a vision of home ownership. More so they knew someone who had already gone and heard the prospective wages they could be getting. More disposable income, concerts, sporting games to attend, bigger cities, more places to eat out, new places to explore, what's not to love?

I know one person who moved back from Oz last year as was their initial goal (save for a few years and come back to buy a home in NZ). They got bored here after 6 months, and the NZ income couldn't support the lifestyle they had grown accustomed to in Queensland so they moved back again.

From the late 80s/90s, Aussie shifted from a simple capital‑to‑total‑assets ratio to a Basel‑style risk‑weighted capital regime. Under the old system, holding a risky corporate loan or a relatively safe mortgage consumed the same amount of regulatory capital per dollar of assets, which actually encouraged banks to chase higher‑yield, riskier assets.

Banks had just taken large credit losses on business loan books in the early‑90s recession, while housing portfolios held up comparatively well despite high unemployment and mortgage rates.

Corporate demand for credit fell as firms deleveraged after that period. The new Basel‑style risk weights made housing assets capital‑efficient relative to business lending, directly “tilting” the regulatory framework in favour of mortgages. When the Ponzi was released, it became the be-all-and-end-all.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.